(remember, Harkster.com (fixed income tab for this, other tabs for much, much more ‘Knowledge without the noise’ — guys with a vision fashioned after my very own aspirations when I was in my previous seat!)

A decent chart from BBG in light of JPOW yesterday and the bond markets collective sigh of relief after whats been detailed as an epic short-squeeze (which wiped out short profits)

… The Federal Reserve already has less reason to raise interest rates rapidly right now, with U.S. financial conditions already tightening because of the impact of Russia’s assault on Ukraine and the sanctions imposed in response. So, Chairman Jerome Powell signaled caution about how fast the central bank needs to proceed as it dials back the extreme stimulus brought in to combat the pandemic. He did still make it clear he expects the central bank will hike this month, and even declined to rule out an outsized increase at some stage.

The rhetoric was less hawkish, helping equities climb. Bonds tumbled as Tuesday’s epic short squeeze ended, but yields are still well below last month’s highs. As long as geopolitics hurt U.S. financial conditions, Powell is likely to keep a more measured stance on rates.

Now as far as what happened in RATES since 5p here are some,

… Overnight Flows Treasuries were little changed overnight, settling in following Wednesday’s selloff. Overnight volumes were modest with cash trading at 69% of the 10-day moving-average. 5s were the most active issue at 32% while 10s were a close second taking 31%. 2s and 3s combined to take 25% at 14% and 11%, respectively. 7s took 8%, 20s 1%, and 30s just 3%. We’ve seen light two-way flows in 10s…

This recon from today’s morning thoughts from large Canadian bank (and home of THE best in the rates strategy biz, titled Consolidation Cometh before the …

… The technical picture is getting somewhat overextended on the flattening side – as evidence by the steady downward pressure on daily stochastics. That said, the net price action of the last several days has left 2s/10s little changed; closing at 36-38 bp during each of the prior seven trading days. The resulting consolidation has prevented momentum from sliding deeper into oversold territory and therefore keeps another flattening breakout solidly on the radar. Suffice it to say, while we’re not anticipating another massive upside surprise from NFP, even a near-consensus print would serve to exaggerate the flattening trend.

… and for some MORE of the news you can use » IGMs Press Picks for today (03 March) to help weed thru the noise (some of which can be found over here at Finviz).

Given how rapidly the facts on the ground(s) are changing — near and far — I’m going to embrace this mornings RELATIVE CALM and reserve any / all personal views for the moment and go right TO some thoughts and charts I’ve seen which are helping ME to inform my views.

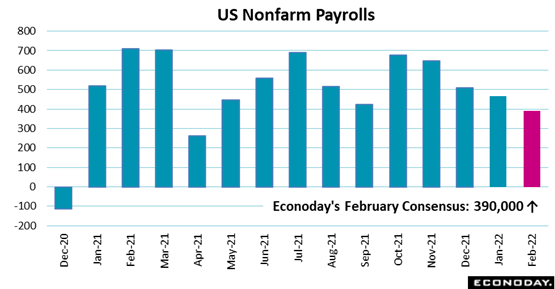

First off, ahead of tomorrows NFP, some independent views from Econoday

Operative word is FEW (and SHOULD) as the last NFP before the Fed meets,

… Although the economy is facing greater uncertainty with the arrival of war in Ukraine, the data through February should look solid for policymakers as they contemplate increasing short-term rates and just how sizable that increase should be.

Now in as far ass PRICES go — some TECHS as there is some truth in price (?).

10yy vs 74dMA (resistance) via large Canadian shop mentioned above

There are SOME firms out there who are ‘adjusting’ positions (ie marking bearishness to market) and it ALWAYS amazes me how even the brightest bulbs in the room occasionally flicker…from the firm with one of the most hated stock jockeys (Wilson), is the following from rates group and latest global macro strat (a couple days ago),

Adjusting Exposure to Realized Geopolitical Risks … USTs: We suggest investors exit 5s30s and 2s30s curve flatteners for now, while maintaining 6m5s30s conditioned bull steepeners. We suggest investors receive fixed on USD 10y10y swaps vs. pay fixed on EUR 10y10y swaps as a flight-to-quality hedge. We think focus will remain on geopolitical concerns in the near term, with the risks skewing asymmetrically toward a sharp reaction in the event of escalation, but a milder reaction in the event of de-escalation. In the medium term, we expect higher inflation to linger, and possibly worsen, leaving the door open for a return to curve flattening in the future…

… The market reaction to the Omicron variant in late 2021 is a good case study here. The Treasury market reacted with concern about the Omicron variant,and 10y yields fell by ~35 bp and stayed there for four to six weeks.

Only after it became clear that the economic effect of the Omicron variant on growth was muted, but the effect on inflation was real, did the market reprice back to higher yields and a flatter curve. Similarly, we think the market may focus on geopolitical concerns rather than fundamental effects – at least tactically.

In the department of haters gonna hate, a large German bank late yesterday afternoon,

Initiating bearish trades in the US As suggested last week, we initiate bearish risk on US rates, as: (1) the direct impact of the Ukraine crisis on the US has been fairly limited, (2) the market is still pricing easy monetary policy three years out, (3) cross-asset proxies have negatively affected the rate rally and (4) there are upside risks to global term premia.

… Valuation metrics: Both cross-asset proxies and the data are consistent with the UST10y being about 100bp higher. More importantly, cross-asset proxies have remained stable over the last few days, thereby adversely affecting the rally in rates.

Initiation then to this (re)new bearishness meant NOT for the amateur and is a short USD1y1y (tgt 245bps and a stop at 180bp) as well as a higher USD term premium trade (aka 5s10s steepener + 20% short 2s tgt 65bps, stop 30bps)

In terms of fundamentals (don’t laugh, they used to matter), I thought a few words on ULC and productivity data from Paul Donovan of UBS worth a look

More about growth than inflation … Fourth-quarter US unit labour cost and productivity data will be revised. While headlines have emphasized higher wages, unit labor cost data shows that fewer people are making more output. Paying people more when they work harder does not create inflationary costs, as every employer of economists should recognize.

The macro effects of higher oil prices We estimate downside risk to US GDP growth from higher oil prices at about an average annualized 0.3pp in coming quarters. While sustained higher energy prices pose downside risk to the outlook, we do not see them as enough to derail the recovery. Changes in spending from confidence and wealth shocks remain uncertainties.

Turning TO the Fed and the research guys at Liberty Street — this one is fresh off the presses,

Speaking of the fine folks at the Fed, on this day in 2020, the Fed was EMERGENCY CUTTING (50bps) Fed Funds and 2yy were 86.5bps, 5s were 88.5bps, 10s 112bps and 30s a mere 168bps …