Good morning. risk is off and bonds are quite BID (actually they appear to be more bid than risk is off, imo) and actually the longer end of the curve is lagging.

Central banks must really BE between that rock and a hard place, eh? More (on this and the 10yy area of the curve) in a moment. For now, here’s what happened,

WHILE YOU SLEPT Treasuries are notably higher and the curve steeper as risk-off, inflation-on conditions persist this morning. DXY is higher (+0.2%) while front WTI futures are back near $100/bl or +3.9% right now. Asian stocks were modestly higher almost across the board but EU and UK share markets are sharply lower now (SX5E -3.1%, DAX -2.5%) while ES futures are showing -1% here at 6:55am. Our overnight US rates flows saw a tamer Asian trade today with good real$ selling in the long-end a notable feature during their hours. Once into London hours, flows reversed massively as risk markets came under severe pressure again on headlines (see above). Overnight Treasury volume was solid at ~180% of average- almost across the curve.

… US News: US positioned to withstand economic shock from Ukraine crisis WSJ A new kind of sticker shock hits the US car market WSJ Nightlife inflation: the cost of going out is going up NYT *TRADERS ERASE BETS ON A HALF-POINT FED RATE HIKE IN MARCH (BBG, 6:17am)

… Treasury 10s20s30s 'fly, daily: Somewhat shocking to see 20's trading at the cheap end of their 6+ month range despite significant reductions in 20y issuance. We've said for some time that the 'price of convexity' could keep the peak of the curve at the 20y point- just as it did in the 1980's before Treasury abandoned this most-expensive-to-issue benchmark.

… and for some MORE of the news you can use » IGMs Press Picks for today (01 March) to help weed thru the noise (some of which can be found over here at Finviz).

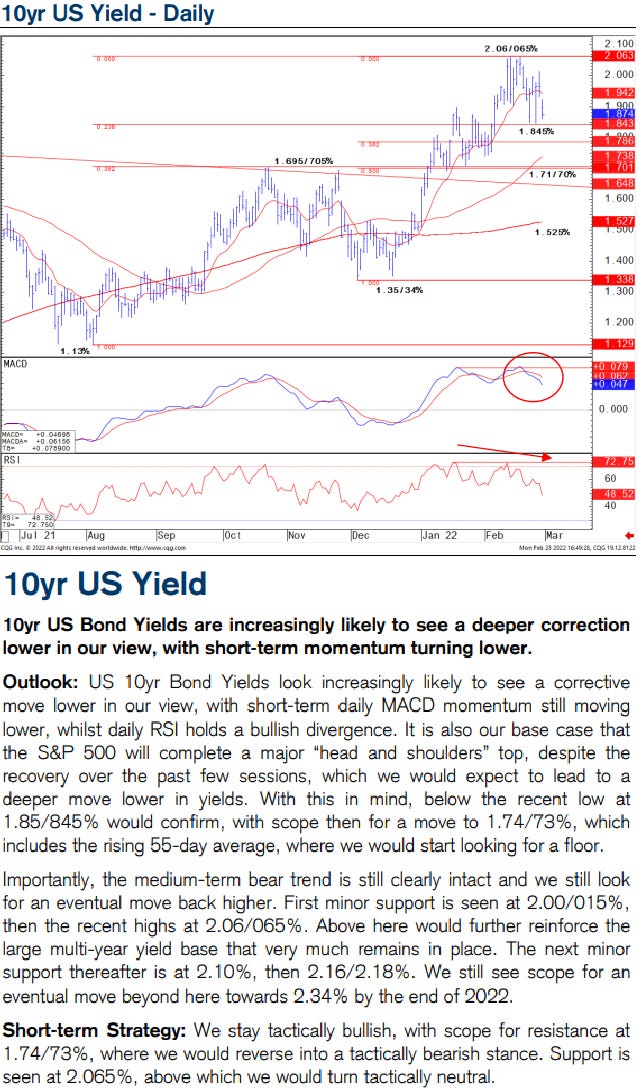

LEVELS / TECHNICALS (10yy) with my limited capabilities which suggested a turn TOWARDS BONDS was near (here) and all-star charts aside, this from a large Canadian operation (and home of THE best strat in the biz, mid morning yest),

What happens after 1.844% 10s? The Treasury market bid has been relentless this morning and the steepening of the curve has offset some of the broader trend established in recent months. We're not viewing the steepening as the beginning of a broader reversal, rather simply re-calibrating to a less ambitious path of policy rate normalization. For this reason, we anticipate the flattening will reemerge as a theme once the proverbial dust has settled. It's within this context that the 10-year chart (attached) offers a decidedly bullish perceptive.

Note that daily momentum is bullish with room to extend in favor of lower yields and there has been a stochastics cross on the weekly chart for the first time mid-October. In terms of key levels, the 1.844% resistance is pivotal. If it holds, there is little to suggest anything other than a consolidation in the current zone. A breakout however would clear the way for a rally to the 50-day moving-average at 1.764% -- with the 1.75% level immediately beyond. 10s are now through the 21-day moving average at 1.92%, which will be the first support of relevance in a reversal. DSIs (also attached) are in the process of reversing from oversold, which further adds to the bullish technical backdrop. Given the array of uncertainties related to the situation in Ukraine, we struggle to see any immediate resolution. Moreover, there isn't much of a path to a Fed 50 bp liftoff at this stage and terminal rate expectations are drifting lower as well. In short, the skew toward lower rates will be difficult to fade into month end.

During QE, Fed purchases USTs. However, increasing fiscal deficits/issuance is typical during QE, limiting the need for obvious sales from a specific investor type.

Inflows from key overseas investors (Japan, Europe, and the UK) increase sharply during Fed easing periods (rate cuts and QE). However, overseas investment in USTs falls during Fed tightening periods, especially QT.

The Fed’s exit as the largest buyer of USTs in 2020-21 and the historic trend of reduced foreign investor involvement in USTs is a concern. The responsibility falls on domestic investors to support US financing needs (and QT).

The increasingly synchronous and fast central bank exit is reducing the stock of negative yield debt, challenging the distribution of UST yields to the upside, despite a lower deficit and lower supply net of QE in 2022.

With increasing convergence of DM central bank policy, the end of negative rate interest policy at the ECB in 2022 could see 10y UST yields back towards 2.50%, especially with much higher fed funds rates. A BoJ exit from negative interest rates could eliminate the entire stock of negative yield debt, and potentially increase the distribution of 10y UST yields even further.

Okie dokie … In THEORY one / all may very well agree AND we MAY see this all come to fruition. In PRACTICE, it does NOT appear that to be the case TODAY and, in fact, when you think about how only this past FRI when STOCKS WERE BID and downright GIDDY, rates about UNCH and 10s just NORTH of 2%. They’ve dropped nearly 30bps … BUT haters gonna hate and shorts in bond market remain a concern and one worth watching (esp for the authors of these type ‘scary’ notes).

Moving right along, then. to even MORE obvious driver of all this, DM central planners are certainly in a pickle — as evidenced by front-ends lapping the field today. Said another way,

ABN Amro | Central banks caught between a rock and a hard place Global Macro: Raising the probability of more negative scenarios – We saw a significant further escalation in sanctions against Russia over the weekend, including a partial ban on use of the SWIFT payments system, and the freezing of Russian central bank assets. As yet, it appears the goal of sanctions is still to avoid disruption in gas supplies to Europe, with attempts at a carve-out for the energy sector.

Rock and a hard place, indeed. On to this mornings very early morning read (from a large German bank strat) with reference to conflict

… As a reminder in this CoTD (link here) we showed work from our equity strategists that using around 30 geopolitical and domestic political events over the last 80 years, the S&P has fallen by a median -5.7% over three weeks before reversing this over the next three weeks on average. The average loss has been nearer -6 to -8% at the peak. It's hard to mark when this current crisis started but I would say Biden's late Friday speech warning of imminent invasion 18 days ago is a good marker. Since the European close on that day the S&P is currently -2.41%. The intra-day low was around Thursday's open when the index was -8.37% lower. You can have a look at the list to assess whether you think the current conflict is more potentially damaging to economies and markets than this. Clearly if this turns into a global war then you have to say that the average is more meaningless. Also much depends on the energy price. Oil is around +8.29% higher from that Biden speech (+3.12% yesterday) but European Natural Gas is +27.34% (‘only’ +3.42% yesterday) even if it was +85.11% at the intra-day highs on Thursday. So far sanctions seem to be carving out energy and as such the spillover is less severe than it could be. Make no mistake the risks of a far worse outcome are there but without this, the historical playbook is holding up nicely. One thing that might be helping risk is the collapse in 10 year US real yields. They fell -20bps yesterday (the biggest since March 2020) and have collapsed -40bps since Biden's address. More on the bond move below…

… Longer-term sovereign yields declined on the continued strained risk environment, with Treasury yields gaining momentum later in the afternoon on the back of month-end index extension buying, ultimately bringing 10yr yields -13.7bps lower to 1.83%.That’s its lowest closing level since February 3, the day before the much stronger-than-expected US jobs report came out that ratcheted up bets on a 50bp hike. Lower real yields drove the decline, falling a remarkable -20.0bps, the largest one-day decline since March 2020, rallying nonstop from the US open throughout the day. Longer term yields also fell in Europe with yields on 10yr bunds (-9.7ps), OATs (-10.1bps) and BTPs (-12.8bps) all falling on the day.

Another ramification of the ongoing conflict was that investors continued to price out the more aggressive reaction functions from central banks they’d been expecting before the invasion. Indeed, the amount of Fed hikes priced for 2022 fell by a sizeable -21.5bps yesterday to 138bps. That compares to the -17.6bps one-day decline in 2022 Fed pricing that occurred around the emergence of the Omicron variant around Thanksgiving. And when it comes to the March meeting in just a couple of weeks from now, the odds of a larger-than-usual 50bp hike dropped to just 3.7% according to Fed funds futures, which is the lowest in over a month, and just shows how the invasion has led to a big change in the market narrative.

Western countries have imposed significant economic and financial sanctions on Russia in the wake of the country's invasion of Ukraine, and these sanctions could impart a devastating blow to the Russian economy.

Countries that have meaningful economic and financial exposure to the Russian economy could also experience negative repercussions if Russia nosedives into a sharp economic contraction.

Countries of the former Soviet Union have the most trade exposure to Russia when measured as a percent of their respective GDPs. Interestingly, the amount of bilateral trade between Russia and Ukraine is small, at least relative to some other former Soviet republics.

Among banks, French and Italian banks have the most absolute exposure to Russia, but the Austrian banking system has the highest amount of foreign bank exposure when expressed as a percent of total banking system assets.

Russia's external debt totaled nearly $500 billion at the end of Q3-2021. If the data on financial exposure by foreign banks is indicative, then much of Russia's external debt is likely held by countries in Western Europe. U.S. financial exposure to Russia appears to be rather limited.

Finally, a monthly performance review from large German bank which shows bonds specifically (from the section on, ‘Which assets saw the biggest losses in February?’),

… Sovereign Bonds: The prospect of higher inflation and more aggressive central bank action hurt sovereign bonds, although there was some relief towards the end of the month. Even so, Treasuries (-0.7%), bunds (-1.2%) and gilts (-1.6%) all lost ground, whilst the underperformance of Italian BTPs (-2.4%) and Spanish bonds (-2.3%) saw their spreads over bunds widen.

Hopefully you are fully all-in on the LEFT side of the above and as for the left or right side of this one, well …