Happy Festivus from a former card carrying member OF 'the sellside' ... and 10yy dating back TO 1790s

Dec 24, 2021

Merry Xmas Eve and a Happy Festivus to the restofus. To those that celebrate(d), May all of your grievances be aired and feats of strength be shown (and doable)!

Since the cancelling of our personal holiday travel plans (never before in the pandemic have we known so many WITH it — most of which HAD it and are fully vax’d and boosted), I’ve got nothing better to do. Sorry. Not sorry.

Also worth noting my travel plans are not unique and it seems lockdowns in China are a once again, a thing

ZH: CCP Locks Down 13 Million People In Xi'an Over 200 Cases As Winter Olympics Approach

The virus continues to impact not only far away, but hitting closer to home, too

CNBC: Airlines cancel hundreds of Christmas Eve flights as Covid hits crews

With all this new found time on my (our) hands, I’ve cobbled together a few excerpts and links (for those who’ve traded flow for the privilege's of reading this stuff…and care) I thought I’d share what I found fun-ter-taining.

Truth be known, tt’s never been only about ‘you’ but as much / more for me, too. The way in which MY (former)sellside brain worked was to understand ALL the ideas bombarding us, trying then to process and ORGANIZE them (see ABOUT link HERE, visual) in such a way that saves YOU time (of reading ALL the research) and finding the RATES-specific ideas.

THESE are the things which traders, money managers, state/local fund employees I know are going to be talking about ‘round the proverbial water cooler, IF they drew the short straw and are working in the week just ahead.

TIME is the one commodity not yet traded on the CME or any other exchange and I hope(d) that spending the time reading / creating / organizing THIS LINK, helps you as much as it helped ME.

The way to spot the good ideas, levels, research, etc. is to read them ALL and delineate the good from the bad. This is subjective, I realize and so, with that in mind, HERE YOU GO.

A few new and UPDATED things which I intend to spend some more time with and which you may find fun-ter-taining over the coming days:

CSFBs technical analysis offers some key themes for 2022 (hint everything from stocks, commods, inter-market relationships and precious metals ALL hinge on HIGHER US REAL YIELDS),

… The main market impact of tighter monetary policy is likely to be higher Real Yields in our view, particularly in the US, where we maintain our long-held view that US Real Yields are in the process of constructing importing yield bases.

Tighter monetary policy should also help to curb elevated inflation, in line with our view that Inflation Expectations have peaked globally. After recessions, inflation expectations tend to move into lengthy mean-reverting phases and we expect to see a very similar rangebound phase during 2022 after inflation expectations established an important peak in 2021 in our view…

… Our current roadmap for US 5yr Bond Yields is that the market is set to reach 1.64% around the end of Q1, however we have repeatedly argued that this is not likely to be a ceiling. Instead, we expect a move to the major 50% retracement level at 1.78% during Q2 and finally 1.985/2.00% by the end of the year. US 30yr Bond Yields are likely to be more rangebound during 2022, in our view.

Our forecasts imply that the strong flattening trend in US Curves will continue, in line with the strongly negative trend following setup, with key moving averages falling sharply and medium-term momentum strongly negative for most US Curves. However, the flattening move that we expect is less aggressive than currently priced into most forward curves, suggesting at some point next year steepeners may offer a profitable carry trade after key support levels are reached.

And there is THIS updated / still BEARISH view of UST RATES from DB

Disturbing the dissensus

The Fed has pivoted from supporting a broad labor market recovery to fighting inflation. However, the Treasury market is only at the beginning of pricing a new regime of rapid stimulus withdrawal and policy tightening. While front-end yields seem adequately priced for next year's rate hikes, longer rates are too low given expected growth and inflation. This is reflected by the low Treasury term premium and real rates sitting 50-75bp below estimates of r-star.

For 2022, we maintain a bearish bias for duration and favor trading steepeners hedged with higher short rates as an expression for higher term premium. We also expect long-end Treasury yields to rise more slowly, leading to a general flattening of 30s versus 5s and 10s. In swap spreads, we favor wider intermediate and longer spreads and a flattening of the spread curve.

Tensions between the market and the Fed, which defined the last two quarters, seem to have largely disappeared after the December FOMC meeting. Except for the very near-term, there is a consensus regarding the rates path. Even a possibility of the monetary policy overshoot is now in the dots distribution in 2024. The immediate reaction of the vol surface was a sharp decline across the board, although the upper left corner was somewhat more restrained. We see less possibility for a more substantial additional vol decline as the mid-term horizon is capable of challenging this consensus.

Despite apparent agreement between the Fed and the markets, there are many things we still don’t know, e.g. the depth and the duration of the pandemic and its impact on the economy, the success of fiscal stimulus and its effects on growth or the outcome of the mid-term election and possible fiscal tightening. In that context, the inflation outlook and Fed’s view of the economic risks could affect the rates path in a material way. Similarly, a pickup in growth and accelerated inflation rise could force additional rate hikes and a general change in the Fed’s position. Because of this, vega should find support not very far from current levels.

There is very little (that I could find) attention to ANY details of RISKS they might be wrong which, in and of itself, presents a HUGE risk, IMO. I’ll let YOU figure out which of Bob Farrell’s rules you’d like to apply.

I continue to FEAR the potential risks in portfolios and lack of hedges. I FEAR that **IF** (or WHEN, really) stocks do correct, USTs will become much more popular than they are right now. But I digress.

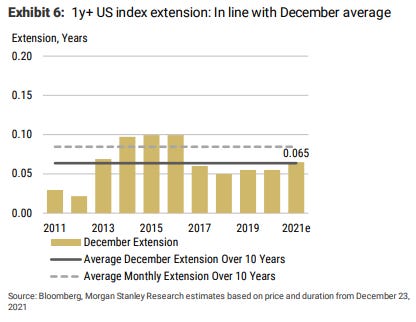

… We expect the 1y+ UST index to extend by ~0.065y, in line with an average December (0.064y) but lower than an average month (0.085y) – Exhibit 7. A total of about US$301bn of supply (offered amount) will affect the extension, and US$174.6bn market value of bonds will fall out of the index. The monthly issuance of 2y,3y,5y, 7y, 10y,20y, and 30y will affect the respective maturity-wise indices.

One 2022 outlook which was only inboxed this past week, was this economic crystal ball reading from the EVER OPTIMISTIC Tom Porcelli of RBC

Strong growth, slowing inflation and a Fed at the crossroads

Let us help you shake off any economic fear that is seemingly gripping so many on the back of omicron: the coming year is going to be another strong one. No one wants to hear that when you are dealing with a variant. We all get caught up in the immediate fear. And we have no doubt that some people will even start talking about the silly idea of stagflation again. But once we move beyond omicron (as we have with each wave, and have come through less scathed each time), the fundamentals are in place for another strong year…

…A common question we field is about risks for the coming year. Obviously we recognize variants as a risk and it is quite likely omicron will slow activity here in the immediate term. But, we also recognize that Powell has been right that each subsequent wave impacts the economic backdrop less acutely. If that remains the case, given the very healthy state of the consumer, 2022 should be another strong year – even if it starts out a bit rocky because of omicron …

…Consider this too. Banks have eased lending standards for commercial and industrial loans rather significantly (inverted in the nearby chart). Guess what tends to follow? A rise in C&I loans. Now, while loans tend to be the classic route for engaging in this type of investment. We should be mindful that companies are also sitting on a mountain of cash if they want to go that route. Either way, companies seem well positioned (and incentivized) to boost productivity.

… Our view is the Fed will raise rates 3 times in the coming year. Right now we think they raise rates in June, Sep and Dec. But we think a key risk around our forecast is they insert a fourth hike early in the year. Let’s talk about that a bit…

… They say the trend is your friend (until it bends) … Has it bent or is it still firmly entrenched? THEY SAY it’s bent and rates are going to embark on its new leg higher. USTs are DEAD money and for losers.

I disagree. Love to hear YOUR thoughts…For NOW, though, a very Merry Xmas and Happy New year to us all!!