Inflation and macro economic strength fading FAST (and so, Transitorians winning) OR another pivot and headfake.

You decide.

I thought a quick look at 7yy were in order …

Momentum (stochastics) appear to be overBOUGHT (rates go UP or time at a price to resolve) and the range is triangulating so it would appear 7yy are poised for a break one way or another …

Price action then creating it’s own narrative (and in some cases, DEMAND) and ahead of this afternoons final auction AND on heels of being forced to gobble gobble up 2yr and 5yr UST supply YEST …

ZH: Lousy, Tailing 2Y Auction Sees Fewest Foreign Buyers Since March

ZH: Yields Slide After Solid 5Y Auction Reverses Bitter Aftertaste From Ugly 2Y Sale

… SOME of the auction process (5yy) may have benefited from data as …

BondDadBlog: Two year low in new home prices and turndown in sales show renewed pressure caused by increased mortgage rates

ZH: New Home Sales Hammered In October As Homebuilders Hit The Wall, Prices Plunge

ZH: "There's Nothing Encouraging On The Horizon" - Dallas Fed Manufacturing Survey Slumps Again In November

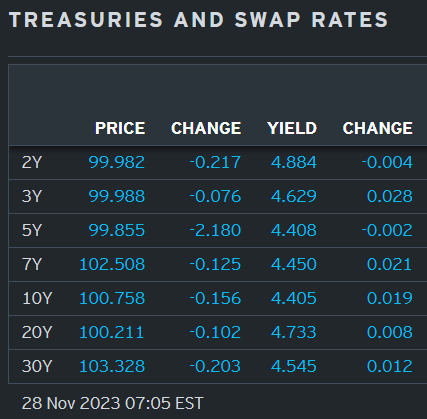

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop (different group than normal as they are travelling to the FAR East) says be behind the price action overnight…

… NY Open - Easy does it Muted price action across markets given looming month-end, and a lack of overnight catalysts. US equity futures, G10FX and USTs trade broadly flat, KRW and TWD traded well following tech outperformance. AUD retail sales missed consensus expectations, though there was limited follow-through in OIS pricing given monthly CPI out tomorrow. Central bank speakers were plenty in HK - the likes of Bullock, Ramsden reiterated hawkish guidance. German 2024 budget uncertainty remains high.

Markets will be more sensitive to downside surprises for US Conf. Board Consumer Confidence at 10:00 EST, regional surveys could also be notable. Fedspeak is back in full force. Waller, Bowman, Barr (twice), Paese and Goolsbee (twice) feature from 10:00 EDT. Waller, Bowman and Goolsbee should offer more market-relevant information. Brazil watches IPCA-15 MoM inflation at 07:00 EST.

… and for some MORE of the news you can use » The Morning Hark - 28 Nov 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

The minutes to the November FOMC meeting didn’t reveal anything new. Despite some good news on the inflation front, it’s clear Fed officials need considerably more evidence that inflation was cooling to be confident that it was tracking sustainably back to 2%. Until then the Fed will remain wary.

There was a lengthy discussion on the factors driving UST yields higher, most notably the rise in the term premium. Participants were unclear as to whether this trend would persist, but if it did it would have implications for monetary policy and thus bears monitoring.

Fed officials felt aggregate demand and aggregate supply continued to come into better balance and thus downplayed the strength of Q3 GDP. Participants also flagged anecdotes and qualitative surveys which suggested activity was weaker than what the official data suggest. Going forward, participants expect activity to ease.

The top line growth story sounds rosy but, looking underneath the surface, cracks are forming. The S&P surveys of manufacturing and service activity suggest companies are becoming gloomier about the outlook, while the composite employment index fell below 50 in November for the first time since June 2020. We also explore other partial data, which point to weaker growth.

… A Bloomberg assessment of the language used in FOMC minutes suggests that the overall tone of the discussions was close to neutral (Figure 1). The Fed Minutes Sentiment Index has been easing for some time suggesting that the fed funds rate (FFR) may have peaked for this tightening cycle.

The divergence between the S&P7 and the S&P493 continues, see the first chart below. Investors buying the S&P500 today are buying seven companies that are already up 80% this year and have an average P/E ratio above 50. In fact, S&P7 valuations are beginning to look similar to the Nifty Fifty and the tech bubble in March 2000, see the second chart below.

Barclays: October new home sales fell alongside downward revisions

October new home sales declined 5.6% m/m to 679k, alongside a 40k downward revision to the prior month. The print highlights slightly lower demand amid elevated mortgage rates. Meanwhile, the median new home price increased, alongside an increase in months' supply to 7.8.

… Barclays Q4 GDP tracker declines 0.2pp to 1.4% q/q saar …

Barclays: U.S. Equity Strategy: 2024 Outlook: No Such Thing as Normal

Whether "new normal" or "old," a roller coaster 2023 proved that this cycle is anything but. We expect US equities to deliver single-digit returns next year as easing inflation is offset by modest economic deceleration. We favor Big Tech & Discretionary among sectors; large-cap over small; Value & Quality over Growth.

We raise our 2024 S&P 500 price target to 4800, from 4500 previously. We increase our FY24 EPS estimate to $233, from $223 prior (consensus $246). Our sum-of-the-parts earnings and valuation framework approach separates Tech from the rest of the S&P 500, based on a decoupling in profitability outlooks. We see modest downside to consensus EPS and price targets as global economic activity begins decelerating into next year, though with more room for active management to deliver returns…

… Positioning leaves room for further upside, but be wary of stocks moving too far, too fast…

CitiFX Techs - Summit attempt for US stocks (note some levels to watch in rates)

S&P 500 and Nasdaq Composite look to rally to their 2023 highs at 4607 and 14446 respectively.

Why it matters: There are no more major resistance levels till the 2023 highs, and seasonality (15y lookback) supports stocks in December. We think both S&P 500 and Nasdaq Composite will rally to their 2023 highs…

… OTHER TECHNICAL DEVELOPMENTS WORTH NOTING US yields: Price posted bearish outside days across the curve, which brings focus back to the support levels we are watching. Weekly closes below would suggest a much larger extension lower. We continue to hold a bull-steepening bias as discussed in CitiFX Techs - Narratives taking shape.

2y yields: Next key support: 4.80%-4.75% (November and September lows).

10y yields: Next key support: 4.34%-4.36% (2022 high, August 2023 highs)

Equity markets remain squarely focused on the macro outlook. For over a year, the economist consensus has been steadfast in calling for a sharp slowing, even as personal consumption, the largest component of spending, has grown trend-like; and lending standards, a key channel for the transmission of higher rates, eased recently. Despite above-trend growth, core inflation has fallen, driven by steep declines in the unexplained component (besides unemployment and the dollar) as factors idiosyncratic to the pandemic recovery eased. Continued declines would see inflation back in its pre-pandemic range without slow growth. The 1970s inflation experience likely precludes rate cuts unless recession materializes.

Earnings growing solidly, though perceptions remain poor; valuations do not look high. S&P 500 EPS fell in H2 2022, then grew solidly in 2023 to reach a new high in Q3. Perceptions remain poor, tied to still low yoy (year-on-year) growth, LTM earnings and low corporate visibility. This may change with Q4 reporting when yoy growth is set to approach 10%. For 2024, the house economics view with a mild short US recession implies $250 (+10%). If instead we get somewhat above trend GDP growth, which was exceeded in the last 5 quarters, we see EPS of $271 (+19%). Are valuations high? No. We see fair value at 18x, which happens to be the middle of the 16x-20x range of the last 2 years, rising to the top on pricing a recovery.

2024 year-end S&P 500 target 5100. We see the multiple well supported at 20x and our base case for EPS remains $250 but allowing for some continued roll forward of the timing of the macro slowdown, we set a target of 5100; our upside scenario with EPS of $271 with some multiple expansion points to 5500. We discuss a number of catalysts that will impact the trajectory: rates vs rates vol; the playbook for geopolitical risks; the selloff around the widely anticipated mild short recession; the Presidential election; and the large potential productivity (and output) upside from tight labor markets.

Sectors and regions. At the sector level, we remain neutral Mega-Cap Growth & Tech, overweight the Financials and Consumer Cyclicals; turn overweight Materials; remain neutral the Industrials and Energy; and underweight the Defensives. At the regional level, we look for broadly similar returns from current levels in Europe as the US over the coming year but are tactically overweight; move Japan to underweight where we see relative performance tied to the yen. We are neutral EM as the discount reflects falling estimates.

… Not looking for the Fed to cut any time soon Rates higher until the next recession

Real rates have just risen from very low levels back into a historically normal range Prior to the GFC, long history of the Fed keeping rates well above inflation as long as growth remained strong Periods with high real rates, such as through most of the 1980s and the 2nd half of the 1990s were amongst the strongest for equity market returns suggesting that real rates reflect rather than drive the cycle

… Will rates vol rise again? Maybe, but not as much as in 2022

…The S&P 500 has moved closely with rates vol (Move index). So, what has been the worst Fed hiking cycle in history for equities looks to reflect higher rates vol rather than the higher level of rates (The Worst Fed Hiking Cycle For Equities: Higher Rates or Higher Vol? Nov 2022)

DB: 2024 <economic> Outlook: Fed WINs in '24, but at what cost? (no such thing as a free lunch)

The US economy was very resilient in 2023. Accordingly, we have become more optimistic on the outlook over the past year. That said, recent data suggest the labor market is more clearly slowing and consumers may be pulling back as long-anticipated headwinds hit. Our forecast of a mild recession in H1 2024 is thus little changed since our last update in October.

We continue to anticipate a downturn driven primarily by softening in consumer spending and capex starting in Q1 2024 in which real GDP falls about 0.6 percentage points. Growth should rebound to an above-potential rate during late-2024/early-2025. This forecast sits between a soft landing, in which inflation is tamed without much upward movement in unemployment, and historical examples of recession, where the unemployment rate rises at least two percentage points.

Fiscal policy and the US election will be in focus. We expect federal spending to evolve broadly in line with the debt ceiling deal, while further belt tightening on a shutdown agreement is a downside risk. The outcome of the election is highly uncertain, and differences in the number of seats in play by party highlight the potential for a split Congress. The candidates will likely push for different fiscal priorities but largely continue recent strategies towards China.

The labor market has come into better balance. Some further slowing in payrolls and stabilization in unemployment would be consistent with a soft landing. Nonetheless, the pace of softening, as well as a weakening in leading indicators and intensifying headwinds, leave us expecting a further deterioration in the months ahead. We expect the unemployment rate to peak at 4.6% in 2024 and then slowly converge back to 4% in 2026.

Progress on inflation should also continue. Aided by a softer economy, core inflation should end 2024 about 30bps above the Fed's target – close enough for the Fed to declare they have whipped inflation now (WIN). Still, near-term progress could be bumpier, and there is tentative evidence that the inflation trend may stabilize around 3% without a softer economy. As such, a more positive outcome for the economy could also delay some of the inflation progress we anticipate.

Recent data strengthen our conviction that the Fed is done raising rates. Further out, our expectations for rate cuts are unchanged: the first cut is in June; there are 175bps total cuts in 2024; and the fed funds rate settles near its nominal neutral level of ~3.1% in 2025. If the economy accelerates, particularly with above-target inflation and looser financial conditions, the risk of further hikes is greater than implied by market pricing.

Goldilocks: New Home Sales Miss in October; Lowering Q4 GDP Tracking to +1.9%

BOTTOM LINE: New home sales declined by more than consensus expectations in October from a downwardly-revised September level. We lowered our Q4 GDP tracking estimate by one tenth to +1.9% (qoq ar) and our Q4 domestic final sales growth forecast by the same amount, also to +1.9%.

The Price Isn't Right Global Rates Outlook: Treasuries Versus Everybody Look for slowing growth to push central bank expectations lower and trigger a broad fixed income rally with USTs outperforming.

Global Portfolio Strategy: Roll Up Your Sleeves and Grab That Carry Spreads in the middle of historical ranges make it difficult to bet against carry and roll. Spreads should provide a hedge for our overweight duration views.

US Running Headlong, Out of Control Tug of war between macro and a supply-demand imbalance to persist in early 2024. As the economy slows and the Fed cuts rates by 250bp starting in mid-2024, 10y yields should decline to 3.15%….

New home sales, while volatile in recent months, have been running close to their pre-Covid pace Sales of new single-family homes fell back to 679K in October (or -5.6% m/m), below our and consensus expectations. In today's report, all three prior months' estimates of new home sales were revised down, by a cumulative 62K, and the jump up to 759K in September was taken back down to 719K, mostly revised away. Smoothing through the recent ups and downs, the 3-month moving average sits at 687K, running at the 2019 pace (685K on average).

The decrease was not broad-based. The West and Midwest reported double-digit drops, while South ticked up. The Northeast posted three back-to-back monthly gains. The median price of new homes sold continues to drop on an annual basis, in contrast to the price of existing homes. Sales appear to be shifting to lower-priced homes…

… US President Biden was critical of profit-led inflation in remarks yesterday (Biden used more dramatic language). The problem for politicians is that this is not, and never has been, the 1970s. Lower inflation was noticeable in the 1970s because consumers were used to price increases. Consumers today are used to price stability, and so price levels get more attention than price changes. Price declines for durable goods are also less noticeable than the price levels of frequently bought purchases—the Snickers bar or Starbucks coffee is the price consumers focus on.

Summary Buyers Continue to Favor New Construction New home sales dipped 5.6% in October, providing some giveback from September's 8.6% jump. Despite October's dip, new home sales largely have remained resilient to the broader housing market slump. In contrast to the recent weakness in resales, more favorable supply dynamics continue to nudge prospective buyers toward new construction. In addition, builders have ramped up their use of price cuts and other incentives to shore up demand. That said, the recent leg up in mortgage rates appears to have placed a ceiling on sales. Combined with downward revisions to prior data, October's lull in demand suggests that the pace of new home sales has flat lined since the summer. Looking ahead, a drop in mortgage rates in November could reinvigorate buyer demand in the near term.

Wells Fargo: Credit Check: Is It Time to Worry About Credit Card Debt?

Summary After paying off credit card debt during the COVID lockdown period, households have levered up at a pace seven times as fast as they did in the prior cycle. Revolving consumer credit, which mostly consists of credit card debt, sits at an all-time high of $1.3 trillion today. Credit card delinquencies are starting to tick higher as well amid the highest average annual percentage rate on credit card debt in data going back to the early 1980s. So, is it time to start worrying about credit card debt? In this note, we summarize the explosion in credit reliance over the past few years and put it into context of the still relatively healthy financials of the household sector.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Here's a weight-loss plan for the Magnificent Seven (Authers OpED on meme stocks and mmkt mutual funds…)

… To Nate Geraci, president of The ETF Store, the meme stock craze has long since passed. “The retail crowd has moved on to polar opposite investments such as money market funds!” he said. “Financial advisers — who drive ETF flows — simply aren’t going to have a meme stock ETF showing up on client statements.”

Retail traders are still alive and well, even if they don’t seem to have gained much in the way of common sense. Their presence can doubtless be felt in the Magnificent Seven. Just this month, they have piled into the shares of bankrupt companies like WeWork Inc. and trucking company Yellow Corp. But the force has waned. Retail traders last month sold nearly $16 billion in stocks, according to S&P Global Market Intelligence, a selloff that reveals fading enthusiasm from day traders.

But if the excitement over memes has gone, retail traders have found other places to go — such as zero-day stock options. August data show that they likely make up at least 30% of the volume in contracts tied to the S&P 500 that expire within 24 hours — and possibly up to 40% — according to Cboe Global Markets. Long-termist this isn’t.

Inevitably 0DTE, as it is known, has now found its way into the $7.5 trillion ETF arena. Defiance ETFs has launched funds that sell ultra short-dated options on the Nasdaq-100 and the S&P 500 as part of their strategies. That should help the excitement last a little longer. With luck, 0DTE ETFs might even survive longer than the MEME ETF did.

Bloomberg: Five Things You Need to Know to Start Your Day (Asia)

… Never mind fears that burgeoning issuance would drive Treasury yields ever higher, there’s a different sort of supply shock that is signaling they can keep sliding down. Crude oil prices have crashed to where they were in July, before they surged along with benchmark 10-year US yields.

While yields kept climbing even after crude topped out, they have turned substantially lower now. Arguably, they can decline further unless OPEC+ can deliver the sort of profound output cuts that would send oil climbing. Even that might not help much, given the strong inverse link between crude prices and US oil inventories — crude topped out in September as those stockpiles hit a nadir.

The difficulty Saudi Arabia is facing in wrangling a deal also underscores the likelihood that the best it can achieve is to stabilize prices. Some of the dynamics at play speak to the potential for further bond rallies. Global demand is soft, and the outlook is looking even softer as central banks insist they will keep policy restrictive for an extended period.

There’s also the more visceral link between oil prices and inflation expectations thanks to consumers’ focus on gasoline costs.

Bloomberg: Just How Bad Is the US Cost-of-Living Squeeze? We Did the Math

… It now requires $119.27 to buy the same goods and services a family could afford with $100 before the pandemic. Since early 2020, prices have risen about as much as they had in the full 10 years preceding the health emergency.

It’s hard to find an area of a household budget that’s been spared: Groceries are up 25% since January 2020. Same with electricity. Used-car prices have climbed 35%, auto insurance 33% and rents roughly 20%…

… “The reality is setting in for consumers that prices rarely go down, especially not in the aggregate. And so really the best they can hope for is prices leveling off and — at the very least — growing at a slower rate,” said Sarah House, senior economist at Wells Fargo & Co. “Hopefully they level off and give a chance for incomes to continue to grow.”

Bloomberg: Consumers Pull Cash From Retirement Accounts Amid Budget Stress (from last week and written ahead of Black Friday / Cyber Monday)

Withdrawals mostly spent on housing and medical expenses

Average 401(k) balances have barely budged in five years

Finally at risk of being a bit too early hard NOT to recognize benefit TO markets from lower Earl leading rates leading stocks (? maybe … c’mon, you’ve heard crazier) as we get Santa Claus rally and in couple weeks a Fed Santa PAUSE,

Investing.com: Santa Came Early This Year As S&P 500 Heads Toward Best November Ever!

IF Powell can maintain a 3% FFR thru to the other side of the economic cycle, I'd call that Mission Accomplished. It's going to get dicey....I'd bet David Hay's thesis that Powell will quit the FOMC before more QE (more QE over my dead body says Powell? Hmmmm), but I do really hope he and I are wrong. Suppose we'll all know the answer long before we know the winner of 2024 Pres election.

IF Powell can maintain a 3% FFR thru to the other side of the economic cycle, I'd call that Mission Accomplished. It's going to get dicey....I'd bet David Hay's thesis that Powell will quit the FOMC before more QE (more QE over my dead body says Powell? Hmmmm), but I do really hope he and I are wrong. Suppose we'll all know the answer long before we know the winner of 2024 Pres election.

Great article !!!

Like the Grocery list....seems those prices rarely go down...

When will Consumer's Debts begin to matter ???.......2024 or never ???