(nuke 'Armageddon' risks elevated) while WE slept; 'since 1310 bond yields have fallen with metronomic regularity', headed TO / below ZERO (2066) for good...

And THAT kinda overshadows what may very well be the day ahead in MARKETS,

Morning Bid: A 'bad news is good news' kind of day?

This will be a very light ‘post’ ahead of today’s all important NFP where all eyes will be focused like a laser beam on earnings, revisions, the labor force and participation rates, etc … Pick whatever favorite indicator buried by the lead which will support your narrative and P&L.

But first, as I continue to wait as patiently as I can for the next greatest latest installment of HIMCOs Lacy Hunt and his longer-term process of thought, I had to share one from The Economist,

The very definition OF the trend being your friend? I suppose it depends on how you are positioned as well as your view of the ‘long-term’ … among other variables.

For NOW … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…in a morning commentary title, “Good News is Flat News”

… Overnight Flows The modest overnight bearishness in Treasuries took place on moderate volumes with cash trading at 82% of the 10-day moving average. 5s where characteristically the most active issue with a 38% marketshare and 10s took a distant second with just 22%. 2s followed with 17% and 3s claimed 9%. 7 garnered 9%, 20s were underwhelming with just 1% and the long-bond rounded out the curve with a 4% allocation.

… and for some MORE of the news you can use » IGMs Press Picks for today (3 Oct) to help weed thru the noise (some of which can be found over here at Finviz).

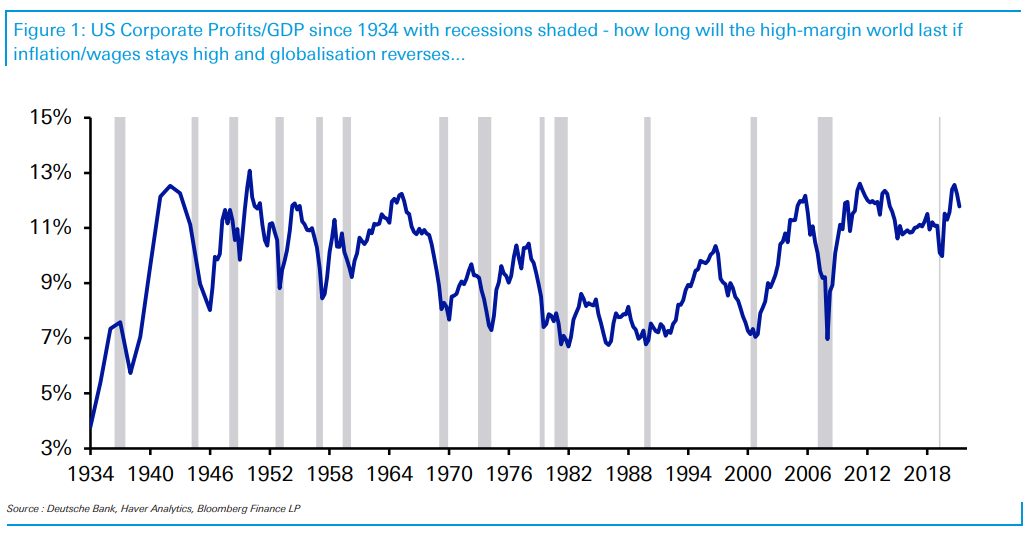

… So average equity valuations must be a decent entry point for the long-term investor? In theory yes, but one worry we would have with this analysis is that profit margins are historically high versus history as you can see for the US in today’s CoTD. In figure 64 in the note, we show a shorter history for many regions/countries around the world with a similar conclusion.

If you believe de-globalisation, higher inflation, higher wages or even environmental costs will erode peak profit margins over time, then equities may not be as cheap on a longer-term basis.

So 2022 has taken bonds from absurdly expensive to rich but has taken equities to fair value (albeit with regional variations). However, for equities you probably need to believe high profit margins are structurally sustainable to be totally confident in this.

Ok so that is that on stocks — rich, cheap, less rich … whatever you wanna say, go right ahead. HERE is another way to think of things from those, you know, AllStars

Ok, then. With OPECs decision to CUT production, snubbing current admin officials, we’ll see about that, I suppose.

Moving along to a comment from someone who’s advice I read and would NEVER question. Largely because the man — Scott Minerd — could benchpress a Volkswagen.

… My biggest concern is that further tightening will test the fragilities of market plumbing. Ever since the Dodd-Frank Act, the Volcker Rule, and Basel III changed the way the bond market functions, the ability of investors to move risk quickly and in size is constrained. Market makers on Wall Street trading desks were historically the primary source of liquidity, but since the GFC asset managers, hedge funds, and other non-banks are challenged to fill the liquidity void created by post-GFC macroprudential policy. We will soon witness how the players perform as market stresses increase as central banks around the world simultaneously remove liquidity at a record pace. Events of the last week demonstrate that shadow market participants, many of which are already highly levered, are facing their own margin calls resulting in them unwinding positions just at the moment when they should be providing liquidity and bidding for securities …

HE details increased vol in both stocks AND bonds and (call ME Captain Obvious … ) how this is NOT a good sign. Look, if past couple / few days and weeks don’t make his point, well, I am not sure whatever will or could.

Now as we await Q3 installment from Dr. Lacy Hunt, there were a couple charts crossed my desk … These first ones come from Global Market Outlook Q4 2022 dropped last night from a firm that may once again become known as 1stBOS … in this chartbook, a couple stood out to me,

… The US Stock/Bond ratio is threatening a significant shift lower and we may be close to seeing the start of an important asset allocation shift as the diversification value of bonds in a multi-asset portfolio starts to return …

… with US 10yr Bond Yields expected to prove more mean-reverting in Q4 …

This NEXT one from Chris Kimble speaks to HOPE charts are right,

Finally, from BBGs Weekly FIX on rate CUTS still being romanced,

… There was slightly more substance behind this latest shot. It started in Australia, with policy makers there delivering a dovish surprise in the form of a mere 25-basis point rate hike. That set off a daisy-chain of perhaps wishful thinking that central banks globally might be approaching peak hawkishness, sending yields worldwide tumbling. A downshift in US manufacturing data Monday followed by a Tuesday report that US job openings dropped in August added further fuel to that fire.

For now, it appears Fed officials have gotten the message across. While a degree of easing is still priced in, wagers on a 2023 cut from the Fed have eased over the past 48 hours, while yields have rebounded. But hope springs eternal …

And on BREAKS, Earl and from BMOs Ian Lyngen & Ben Jeffrey

… We know what the Biden administration thinks, but how does Fed chief Jerome Powell feel about OPEC+?

One could imagine not too warmly after the producer group announced an output cut of 2 million barrels a day — the biggest such reduction since the pandemic’s onset. In reality because many OPEC+ countries are already pumping below their quotas that number could be between 1 million to 1.1 million. Still, the news was enough to trigger oil’s biggest weekly rally since March, with West Texas Intermediate futures around $88 a barrel.

That impulse quickly spread to the bond market. While still well below this year’s multi-decade highs, 2-year breakeven rates are set to rise by nearly 50 basis points this week -- the biggest increase since March.

That’s not great news for a Fed deeply concerned with controlling inflation expectations. Here’s Ian Lyngen and Ben Jeffrey of BMO Capital Markets on the topic:

Earlier this year the specter of WTI sustainably north of $100/bbl and what that meant for prices at the pump as well as utility prices presented the precarious potential for higher prices to persist and accelerate in a way that monetary policy was unable to address. Despite ongoing conflict in Ukraine and the issues surrounding energy infrastructure in Europe, the fact that crude has maintained a consistent downtrend over the past several months has been a positive through the lens of containing headline inflation. Headline and core-CPI are expected to come in at 8.1% YoY and 6.5% YoY, and while there will come a time when monetary policymakers begin to delineate between the two, inflation remains too high for the Fed to be anything other than hawkish.

Again, at about 2.5%, 2-year breakevens are dramatically below March’s high-water mark of almost 5%. But with the likes of Morgan Stanley and Goldman Sachs now calling for Brent to advance back to $100 a barrel in the aftermath of the OPEC+ cut, there’s plenty of room for inflation expectations to run higher. ..

Speaking of BREAKS … and as it is still my belief the Fed intends on breaking something — I want to end with one final link … everything I read on the intertubes is true, right?

Our good friend, King David, just forwarded this Bloomberg headline to remind us of a post we made back in 2018, which we have reposted below. Maybe, or maybe not, but you should have the following analysis in your quiver, at the very least to stress test your market narrative. We do need to update the data, which are quite stunning and rather surprising.

Ok, then … I should very well have quit while I was behind. Since or IF you are still here, I’d ALSO note that I’m on the road again early tomorrow — chasing WPI Engineers football program as they invade DC to play Catholic University.

I’ll be back sometime tomorrow evening and ready for breakfast with the NYG football from the UK as well as Thing 3’s (home)game later on in the afternoon … I’ll make an effort to organize something of an update at some point but for now … THAT is all for now. Off to the day job…