One more quick note / thought before the day gets going. CNBC reporting that mortgage rates drop TO 4wk low BUT home BUYERS pull back due to lack of supply.

Perhaps the upside TO PPP fraud (more listings as folks get caught, prosecuted, and then sentenced TO prison) is another example of how there’s still nothing without consequence?

CNBC: Mortgage rates fall to a four-week low, but homebuyers still pull back due to record low listings, key points offered:

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($548,250 or less) decreased to 3.27% from 3.30%.

Applications to refinance a home loan increased 2% from the previous week but were 42% lower year over year.

Applications for a mortgage to purchase a home fell 3% for the week and were 9% lower than the same week one year ago.

Story highlights,

… Even a small drop in interest rates couldn’t bring more buyers in, although it did boost refinance demand slightly. As a result, total mortgage application volume last week was essentially unchanged, falling 0.6% from the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index…

… It is not necessarily that buyer demand has fallen off, it is more likely that buyers simply can’t find a home they like. The number of homes actively listed for sale at the end of November fell to another record low, according to Redfin, a real estate brokerage. Supply is leanest on the low end of the market, and prices are still rising at a fast clip.

So with some of the day’s ‘place holder’ data behind us ahead of GDP (3rd look @ Q3 and Used Home Sales before tomorrows final barrage of inputs (aDurable Goods, PCE, Income/Spending, UoMISSaGain) I thought I’d offer couple more highlights.

Things to consider as you finish up book keeping trades and positioning over the next several sessions. First, from Saxo Bank

Summary: Yesterday's solid 20-year US Treasury auction shows that real money continues to bet on weaker global growth and inflation expectations, which can come together with a significant risk-off event. However, we expect long-term yields to rise as the Federal Reserve begins its interest rate hiking cycle. Even if the central bank returns to its accommodative stance shortly after, there is the chance that inflation will remain a problem, requiring aggressive monetary policies in the future. Therefore, we see considerable downside potential for long-term Treasuries.

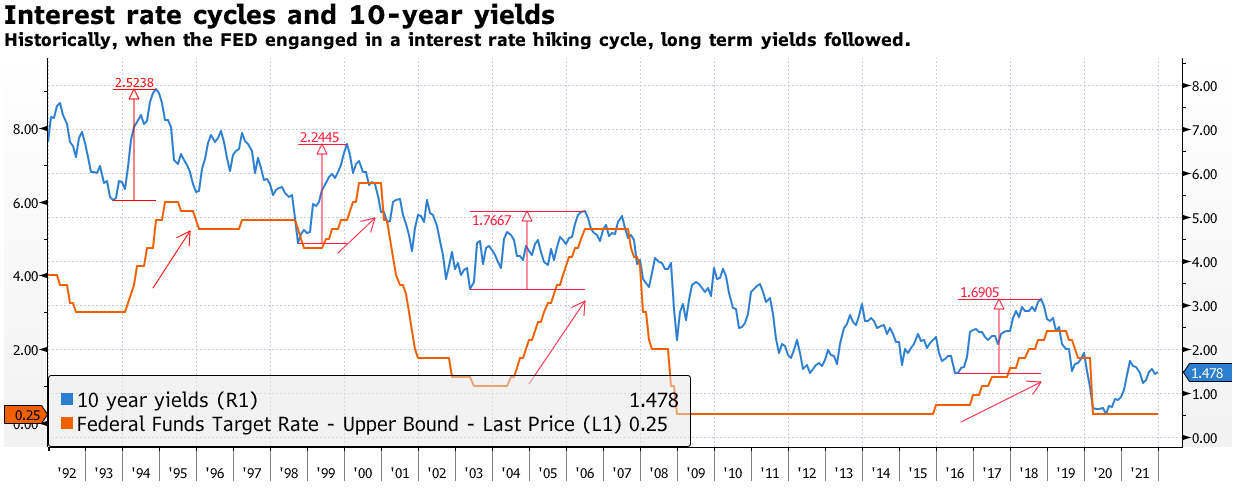

I’d highlight this interesting visual and bit of word salad from an operation that remains steadfastly committed TO a more bearish (higher yield) outcome — so, consensus, if you will

… the long part of the yield curve rally might not last beyond the first quarter of 2022. As the Federal Reserve finishes taper purchases under its QE program, the beginning of a tightening cycle will become nearer, and a rise in yields across the whole curve will be unavoidable. As the chart below shows, 10-year yields have always shifted higher during previous interest rate hiking cycles. It’s prudent to assume that the same thing will happen this time around.

There is another thing to consider: inflation remains an underestimated threat. If the central bank returns to its accommodative stance due to a market selloff soon after it embarks on a tightening journey, there is the chance that inflation might rise even further. In that case, the Fed won’t have any other alternative rather than continuing hiking interest rates.

I still don’t see all that large a difference between inflation’istas and de/dis-inflation’istas when you think about and actually listen to / HEAR what they are saying.

Buy the dip? On THAT note, a couple other items from the inbox which may / may not be of interest to those running big (or small) pension funds.

A large German bank out with a note / UPDATE on funding status / levels (so, think about it in context of asset / fund performance into years end where needs may impact FLOWS). Keeping in mind the most recent / AVAIL data are for Q3.

The latest Flow of Funds data show a marginal uptick in private pension purchase of fixed income assets in Q3 while public pensions stayed on the sidelines.

Our pension flow model points to an estimated $51bn inflow to fixed income ($29bn public / $22bn private) for the current quarter.

Funding ratios fell slightly in the third quarter to 96% and 58% for private and state/local pensions. However, robust equity performance in recent months is expected to boost the metric to 98.7% and 59.8% for Q4.

For the year ahead, rising discount rate is expected to further support private pension funding levels, prompting greater inbound flows into fixed income as private plans reach full funding.

These funds are the large aircraft carriers of asset managers. They don’t typically act as much tactically as they do strategically. While most VIEW bonds and 60/40 as dead (ie haters gonna hate), the note suggests,

…The much anticipated rebalancing of private pensions appears to have commenced as plans approach full funding. In the third quarter, private funds picked up the pace of fixed income purchase, bringing total inflow into fixed income to $10.1bn and equity outflow to $21.3bn. Private pensions’ inflow, despite a $4bn increase from Q2, remains measured. This is consistent with the behavior observed historically as private pensions often look past near-term fluctuations in returns and mostly rebalance to maintain a 60/40 allocation in the long run.

In Q4, significant equity outperformance thus far should prompt some profit taking by public funds and further incentivize private pensions’ reallocation towards fixed income. Our model points to an estimated $51bn inflow to fixed income ($29bn public / $22bn private) for the current quarter.

…To sum up, private pension funds are already on the cusp of being fully funded and stand to reap additional benefit from higher discount rate. The outlook for public pension funding status, on the other hand, mostly hinges on equity performance. It remains to be seen what the discount rate implication is for public plans.

OK then … on the cusp OF being fully funded so as Sgt Phil Esterhaus of Hill Street Blues used to say, lets be careful out there.

With THAT in mind (being careful out there) and for those still in the game, books OPEN ready to enact TRADES if/when levels are hit … And for those thinking TECHNICALLY / tactically over the next few days, here are some updated FI TECHS from a bank formerly known as 1st Boston to us old dawgs.

They are offering a few words on 5s (stay SHORT), 10s (where to GET SHORT) and 30s (stay NEUTRAL) … This hit (US) inboxes mid-day yesterday (21 Dec)

5s … Short-term Strategy: We recently turned tactically bearish following the pullback to resistance at 1.095%, with scope for support at 1.435%, where we would turn tactically neutral. Next resistance is seen at 1.04%, below which we would also turn neutral.

10s … Short-term Strategy: We would turn tactically bearish again at resistance at 1.365%over the holiday period, with scope for 1.775% thereafter. Resistance below 1.365% is at 1.25%.

30s … Short-term Strategy: We prefer to stay tactically neutral at present, with the market looking increasingly looking as though it has moved back into its medium-term range.