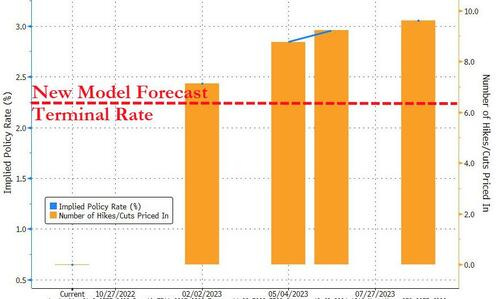

In any case, stocks got hit pretty hard just after CPI but were apparently sticksaved by ECB headlines (via ZH — sorry not sorry) as RTRS details a thought / hope that terminal rate (there, not here) is LOWER than current mkt pricing …

Reuters is reporting that an ECB staff model (presented the model to policymakers at a retreat in Cyprus last week.) puts the target-consistent terminal rate at 2.25%. That is dramatically less than the market is expecting will be required by The ECB to tame inflation...

And so, global stocks off to the races while yields remained largely higher

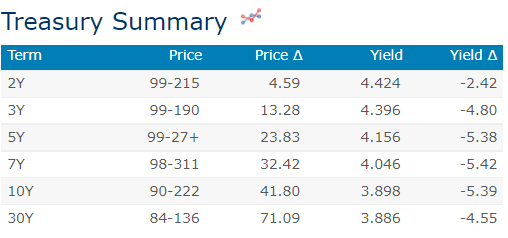

… here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are richer led by the 7y point, but still underperforming a furious Gilt rally (30s -28bps) as smoke surrounding a fiscal U-turn turns fiery. Risk-parity (on) thematics persist, the MSCI Asia Pacific index gaining as much as +2.6% overnight, while S&P minis are currently +11.5pts after yesterday’s counter-intuitive reversal higher. Notably overnight, the USDJPY currency pair hit its 1988 high at 147.66, with Suzuki commenting that he is watching FX “with a high sense of urgency” and will “take appropriate responses against excessive moves.” USTs trended generally richer in Asia and have since been mildly sympathetic to the Gilt bull-flattening. Flow has been mixed with CBs outright selling intermediates into the strength and marginal bank tsy demand in the front end. Worth noting that MoF Data showed Japan was a large seller of foreign bonds last week ( -11.6bn, largest outflow since Feb), the 4th straight week of selling. UST volumes are running ~120% the 30d ave.

… the week’s supply cycle ended on another sour note (3/3 tails), while the largest net outflow seen in Japanese weekly securities investment abroad (for week of Oct 7th) since early February doesn’t paint a hopeful picture of end-user demand. The 4.0% level in 10s therefore, may prove just a rest stop…

… and for some MORE of the news you can use » IGMs Press Picks for today (14 Oct) to help weed thru the noise (some of which can be found over here at Finviz).

As week comes to a close, I’d note a few items from the Global Wall Street inbox which may strike you as interesting before and after this mornings ReSale TALES …

First up is a CHANGED FOMC call (this from Barcap)

Change in Fed call: The number of the beast Following this morning's robust CPI report, we lift our expectations for the funds rate. We now expect the FOMC to hike the funds rate by 75bp in both November and December, followed by a final 50bp hike in February. In the last three meetings of 2023, we now expect the FOMC to reverse course with 75bp in rate cuts.

Who could blame them after the data as ING details,

40-year high for US core inflation heaps pressure on the Fed US consumer price inflation surprised on the upside once again as rapid increases in housing costs, medical care, food and airline fares offset signs of moderation elsewhere. The Fed has admitted it is prepared to inflict economic pain to get a grip on inflation and today's report will ensure at least another 75bp rate hike in November and 50bp in December

Pressure on the sellside to keep up with whatever it is they think they think may be next…at least I thought that was the case. But not from THIS GUY — Paul Donovan of UBS,

Yesterday’s consumer price inflation was stronger than the consensus forecast, and the expectation is that the Fed will continue its chant of “raise, raise, raise.” While the headline dictates what the Fed will do, the details dictate what consumers might do—which matters to investors.

Team transitory was right—last year’s US inflation drivers have turned into deflation. Durable goods prices rose 3.8% m/m at their 2021 peak; in September, they were -1.1% m/m, the largest fall ever. Homeowners’ cost of living remains significantly lower than CPI. Over 40% of the core goods basket fell in price last month, as did 35% of the food basket. Consumers are seeing deflation as well as inflation, possibly increasing their willingness to consume. We get US retail sales data today.

Chinese inflation data was slightly lower than expected—producer prices slumping below 1% y/y, and consumer prices rising on food price gains, but less than expected. Sluggish domestic demand is not giving much momentum to prices.

The UK government is reported to be preparing to abandon its mini-budget, with speculation as to whether the chancellor or the prime minister is abandoned. Markets care most about the return of sensible fiscal policy, but there is also some interest in the overall competence of the government.

Donovan is NOT alone … another of the sellside’s popular kids — Jim Reid — offered a chart yesterday,

… As today’s CoTD shows, global freight prices reflect that nicely as prices are down around 70% since their lofty peaks this time last year. That comes as other notorious supply inputs of last autumn, such as lumber prices, are also well beneath their peaks. In addition, supply-chain pressure indices are easing, the money supply is rolling over, and inflation expectations remain subdued.

Unfortunately there’s more to inflation than this but in positives only week its only fair to mention the big downward price momentum seen in many supply side drivers.

… More recently the US is playing a dual role for a strong USD tends to add to import prices for many countries with weak exchange rates, but also restrains global liquidity measures and related demand as per Figure 2.

Transitorians unite? Celebrate? Let’s NOT get ahead of ourselves … In fact, lets turn TO BBGs Weekly FIX and a look at how USTs are far from ‘risk free’ in one WRITERS view

For the Federal Reserve, the task still looks a lot less complicated, though that just passes on the pain to everyone else it seems. Even before Thursday’s upside move in inflation, US central bankers were hammering away at the theme of higher and higher interest rates. Quantitative tightening is also on the menu, and that’s part of the reason for all those liquidity concerns mentioned earlier. The European Central Bank may join that bandwagon early next year, underscoring the potential that bonds face sustained losses for some time to come.

Markets were therefore well and truly softened up before the CPI release hit, not that we didn’t get a fresh surge in yields. Even as Apollo Global Management Inc.’s John Zito pinched himself at the juicy yields already on offer, many investors simply concentrated on the bruises. US credit markets weakened the most in a month after the inflation print.

Transmission Channels

The Fed’s stance had already been driving the dollar against all its major peers, and many not-so-major ones. Then Yellen endorsed a stronger greenback to confirm that it can keep climbing at least as long as the Fed is hiking. There’s a potential upward spiral for yields and the dollar being put in place, with a range of governments and central banks pushed toward intervening in currency markets to restrain the dollar as the US currency threatens to spur instability — and also inflation by driving up the cost of imports. Japan may already be moving to repeat its yen purchases from last month, given the currency just went to fresh three-decade lows, fueling concerns it may soon sell Treasuries to fund such actions.

Emerging markets are therefore running down their foreign-exchange reserves and pursuing steeper interest-rate hikes of their own. Kenya just bumped rates up by the most in seven years, as its Central Bank Governor Patrick Njoroge warned that nations like his are suffering “collateral damage” from the rich world’s rapid tightening policies. South Korea went back up to a half-point hike. The Philippines will consider another move that large, or even larger.

The monetary policy shock and awe being spread across the globe is generating louder and longer cries of concern that recessions will be the outcome. The International Monetary Fund said Asia’s economies will need to focus on fiscal stability in order to offset surging debt.

AND from the CHARTS department from 1stBOS (one mans bible another’s CoTD)

Chart of the Day: After long-end US yields reversed sharply off their highs, the main takeaway following the strong beat in the CPI report was curve flattening, in line with the view from our Q4 outlook that there is scope for another leg flatter in the US 2s10s Bond Curve towards -70/71bps. Of note now is the potential for a clear bearish “triangle” continuation pattern for the US 2s5s Bond Curve, which would be confirmed below the -29/-30.5bps 2000 low, which would also mark a major break of technical support. The next support thereafter is seen at -38bps, then -50bps and finally -54bps.

That in mind, the firm remains committed to tactically bullish case 10s and 30s while reducing bullishness towards 5s…

And for those watching TECH stocks (with the longer-end of the yield curve in mind), Kimble Charting,

… So if you’re one of the many investors out there mending fresh wounds this week, I want to make one thing clear…

Bonds are a falling knife.

Check out the chart of the 30-year T-bond:

Do you really want to buy this chart?

Read on for more and hopefully will have some time to organize something of an update over the weekend ahead of Sunday night’s futures open … Thing 1 (WPI) has a bye and Saturday evening is Thing 3s final home game under the lights before playoffs begin … THAT is all for now. Off to the day job…