Good morning … “Do you believe in miracles?” History.com HEREfor more and for even MORE, tune in today at / near 1pm to see IF Dept of Tsy is able to sell off 5yr notes deploying what may be considered the greater fool theory,

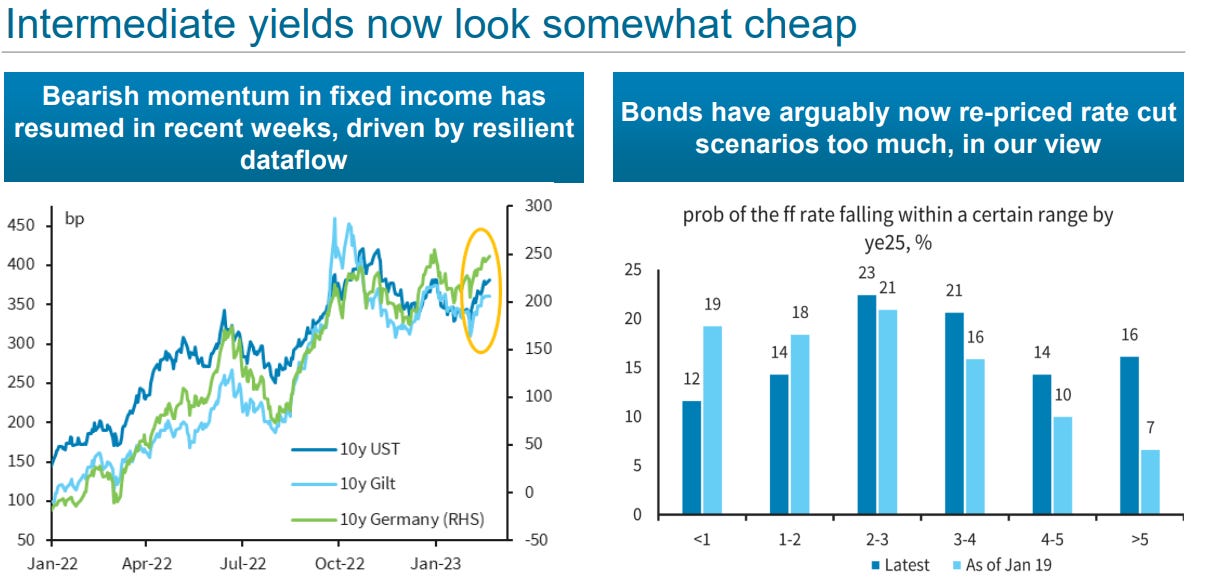

Momentum remains overSOLD (on daily) but outright we’re far away from October / cycle ‘cheaps’ … some ‘out there’ (below) are thinking ‘intermediate yields now look somewhat cheap’. Why NOT as a large German shop details,

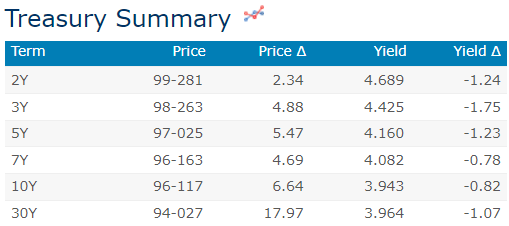

… Five-year yields have risen by 64bps since the previous auction stop-out to trade around 4.17%.

… here is a snapshot OF USTs as of 703a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher while stocks are little changed ahead of today's FOMC Minutes and Treasury 5-year auction. DXY is modestly higher too (+0.12%) while front WTI futures are modestly lower (-0.9%). Asian stocks were lower after yesterday's NY session swoon, EU and UK share markets are all lower (SX5E -0.8%) while ES futures are FLAT at a very early 6:15am for us. Indeed, we were too early to get you desk flow color and overnight Treasury volume was unavailable as well (my sheet broken). Sorry about that.

… 30yr Treasuries like 4.00% too and bonds have so far held support near there (3.986% to be precise) or the turn-of-year rate highs. Weekly studies hint that bonds are likely to breakout bearishly but, so far, support is holding...

… and for some MORE of the news you can use » IGMs Press Picks for today (22 FEB— and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

… What has been missing throughout the Fed’s tightening cycle is a clear narrative as to what rate hikes will achieve. Rates were never going to influence the durable goods inflation of 2021 (and that has plunged into deflation anyway). Fed Chair Powell’s influence over the war in Ukraine is nil. Rates are a clumsy way of tackling profit-led inflation. We hear from New York Fed President Williams today…

While Paul speaks generally of inflation detail, a large German bank offering,

Rates are up for the month, both real and nominal, and breakevens wider. 2Y UST yield is about 60bp higher with 2s/10s about 10bp flatter while inversion between terminal and neutral proxies of real rates has taken a deep dive by additional 35bp. A rethinking of the rates path is taking the center stage as risk scenarios are beginning to compete with the base case. Consequently, volatility has increased across the board with 1Y1Y back above 135bp and 3M10Y, after touching 100bp earlier in the month, is trading again around 115bp. The market is pricing in a highly restrictive Fed, and the Fed seems to be not only in agreement with that pricing, but promises to push even deeper into restrictive territory if necessary. Real curve inversion is back to last year’s levels with the spread between 2Y1Y and 5Y5Y forwards at -25bp. This is, however, less aberrant than when it first appeared in mid-2022 as inversion usually occurs by the end of the tightening cycle.

Aggressive rate hikes and the rise of real rates have overpowered all other considerations in the current cycle and have been the dominant driver of the markets in 2022. The figure shows YTD performance of S&P (inverted) overlaid 5Y5Y real rates. This mode of interaction has persisted as inflation showed resilience despite aggressive rate hikes.

Recent departure of equities from real rates: Temporary or permanent?

From market(s) pricing dictating one another back up TO The Ivory Tower where we check in with Prof. Jeremy Siegel,

… Given the sharp rise in interest rates in the last two weeks, the equity markets held up well. The most bearish forecasters were penciling in a drop to earnings on an economic slowdown. Rates are rising because employment data is coming in strong and the economic data is holding up quite well, so earnings estimates are more likely to materialize.

… Suggesting an economy makes “no landing” makes no sense. Analogies eventually break down, especially this one. Economic activity does not stop like an airplane eventually does, but rather the economy eventually settles in a steady state where growth is consistent with factors such as population and productivity.

So perhaps it’s time to rethink. One suggestion is using the analogy of a runner. Runners often talk about the various phases of the race. One important phase is when runners transition from the acceleration phase, when runners focus on increasing stride length and frequency, to a steady state, when runners focus on maintaining stride length and frequency over time.

What does this mean for you?

The Fed wants to tighten financial conditions so the economy can smoothly transition from the post-pandemic reopening phase, when the economy grew 5.9% in 2021 and 2.1% in 2022, to a more sustainable rate that neither stokes inflation nor stalls economic growth.

If the economy can break the back of inflation without a deep and prolonged recession, investors will likely experience markets that could return to lower volatility and improved conditions for both bond and equity investors. We think this could be a likely outcome, notwithstanding unforeseen global shocks.

Well how’s THAT for making sense of the NONSENSICAL? Feeling better and much more confident as to what it ‘means for you’? Personally, I’m not and couldn’t think of a more vague way to say nothing YET, getting clicks at the very same time!!

Meanwhile, others are far less certain and apparently willing to admit it. First Trust,

… It remains to be seen how shifts in interest rate policy will influence M2 growth in the months ahead. Again, we are in an unprecedented period for policy with abundant reserves, so educated guesses, not definitive answers, are the best anyone can do. One big question is whether the lifting of rates has slowed M2 or is it just that rates are higher. That may sound redundant, but it’s not. Let’s say the Fed stops raising rates at a peak of 5.5% and then pauses rate changes. Will that peak level of rates keep putting downward pressure on M2? Or is it the hiking of rates that matters, so M2 will start growing again once the Fed stops raising rates (even though it doesn’t cut rates, either)?

This is important because monetary policy hits the economy with long and variable lags. We have already seen some weakness in production reports but are not close to feeling the full brunt of the tighter money that started last year. There is a storm headed our way, so please be prepared.

And speaking of crystal balls, interesting thoughts from yesterday to consider ahead of today’s 5yy liquidity event,

The bond market moves to 'higher for longer' Bonds have re-priced sharply in February, driven by stronger growth and inflation data. While stocks are off their highs, multiples haven’t adjusted to the rise in rates, in our view. For a third straight week, we remain underweight risk assets.

As was noted earlier bonds lead stocks leading bonds — or at least there are some noteworthy REAL correlations (and dispersion at moment), Bloomberg notes

Bonds and stocks are back together after they flirted with a trial separation earlier this month, when equities resisted the sell-off that hit fixed-income securities. The steady drumbeat of hawkish rhetoric from policymakers has persuaded investors that central banks mean business when they say they will take interest rates higher than expected, and potentially keep them high for a long time.

Government debt has been selling off strongly for most of this month as a result, but it took a bit longer for equities to get the message. That might have been because earnings season offered some measure of optimism, or because yields were yet to get high enough for stock pickers to fret. A modest pickup in the 10-year rate from under 3.4% could be taken as a signal of economic strength. But with the yield charging to within 5 basis points of 4%, equities took fright. The two asset classes look stuck together at least until this Federal Reserve hiking cycle is clearly finished with.

5yr traders looking for miracles … THAT is all for now. Off to the day job…