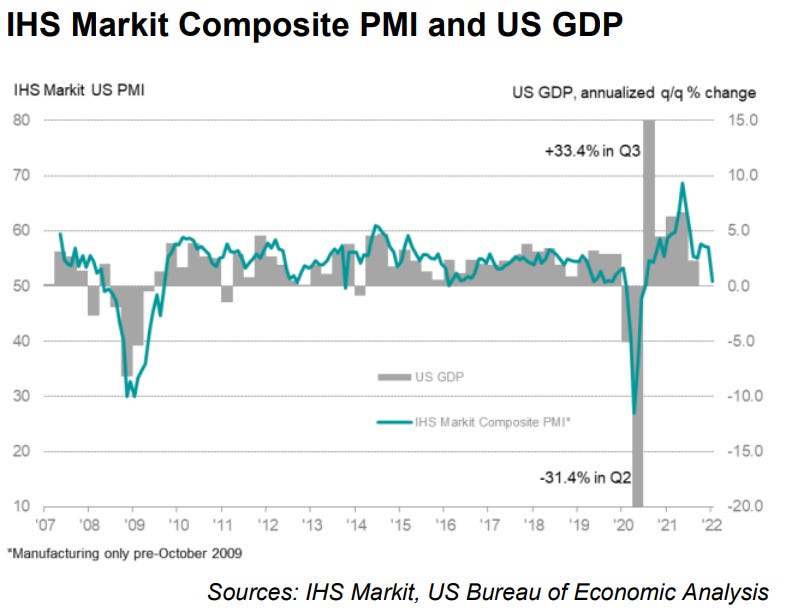

The Chicago Fed National Activity Index (CFNAI) was –0.15 in December, down from +0.44 in November.

You don’t need ME to tell you what to make of it all but as I await further input on current POSITIONS, this email hit inboxes across land not too long ago, as BLK moves to put some hay in the barn,

CLICKING THRU (HERE IS PDF) for those curious and who’d like ALL the devil in the details — you’ll note what they see as a consistent message,

We see the sharp rise in government bond yields this year as consistent with a fundamental asset reallocation driven by investors wanting greater compensation for the risk of holding government bonds. The swiftness of these moves is an example of a market primed to overshoot amid confusion over the macro backdrop, as flagged in our 2022 Global Outlook. We slightly reduce our tactical underweight on U.S. Treasuries as a result, while keeping our strategic underweight unchanged.

Bond BEARS NEED NOT FEAR … they are NOT losing this ally in the fight AND note how this is GOOD for stocks (or NOT bad … errr, ummm….)

… Our base case remains that yields are headed higher on a one-year horizon, yet a short-term reversal has already started to unfold. On a strategic or long-term horizon, we still view the outlook for nominal government bonds as challenging and maintain our large underweight.

What’s striking is the speed of the yield spike. The Fed has effectively abandoned its prior guidance by suggesting it’s ready to start raising rates before achieving its “broad and inclusive” employment mandate. By doing so, it may have added to the confusion about the expected path of rates. Markets have quickly shifted their short-term expectations to include earlier and more rate hikes this year. The hawkish mood has spread to longer-term yields and to markets such as the euro area …

… Our bottom line: Given the speed of the Fed repricing, bond markets may have gotten ahead of themselves in the short term. We reduce our tactical underweight to U.S. Treasuries as a result. But the backdrop for Treasuries remains negative as we see a further resurgence of the term premium pushing yields higher, especially as the Fed prepares to shrink its balance sheet. We don’t see this as necessarily bad news for equities. This year’s stock selloff hides huge shifts under the hood, with tech shares falling and many cyclicals eking out gains. We believe the narrative of “rates up, tech down” is too simplistic given the drivers behind the long-end bond selloff and the broadly unchanged, still-low sum total of expected rate hikes. Indeed, we believe fading Omicron fears have contributed to the tech selloff. We favor a barbell approach in our sector views. We like cyclicals as the powerful restart rolls on, and beyond a tactical horizon we still favor solid tech and healthcare stocks because we see them as beneficiaries of structural trends like digitalization and the transition to a net-zero world.

Too simplistic is KEY … Global Wall Street NEEDS things to be more complicated so that there is some need for THEM to explain it all and help with highly profitable DERIVS (trades, investments, hedges etc) to sell TO poor, unsuspecting widows and orphans.

Oh, wait, no, I mean for them — Global Wall St — to HELP. Right. HELP…

Speaking of HELP, BLK noting how this all isn’t BAD for stocks also notes govt scaling BACK SUPPORT,

I suppose this, too, is GOOD for stocks? Whatever. Head TO p5 of 6 and note under GRANULAR VIEWWS, minor adjustment TO USTs,

A reduced underweight simply putting SOME hay in the barn,