(lower/flatter on above avg volumes)while WE slept; First Boston SAVED (for now) ... a fitting happy anniversary (JPM buys Bear, the day C19 nearly 'broke the financial markets')

Credit Suisse statement said that it will borrow CHF 50bn from the SNB and announced public tender offers for up to CHF 3bn of its own debt securities.

FINMA and SNB statement said that they “assert that the problems of certain banks in the USA do not pose a direct risk of contagion for the Swiss financial markets. The strict capital and liquidity requirements applicable to Swiss financial institutions ensure their stability. Credit Suisse meets the capital and liquidity requirements imposed on systemically important banks. If necessary, the SNB will provide CS with liquidity.”

BOE held emergency talks with its international counterparts over CS.

Feel better as we are once again living, trading and investing through history being made right before our very own eyes?

For now and so allow ME to be the first to wish you a happy JPM BUYS BEAR STEARNS a-versary

History.com: Bear Stearns collapses, sold to J.P. Morgan Chase

..For the fourth quarter of 2007, Bear recorded a loss for the first time in some 80 years, and CEO James Cayne was forced to step down; Alan Schwartz replaced him in January 2008.

Barely two months later, the collapse of Bear Stearns unfolded swiftly over the course of a few days. It began on Tuesday, March 11, when the Federal Reserve announced a $50 billion lending facility to help struggling financial institutions. That same day, the rating agency Moody’s downgraded many of Bear’s mortgage-backed securities to B and C levels (or “junk bonds”).

...By Thursday evening, March 13, Bear had less than $3 billion on hand, not enough to open its doors for business the following day.

...The Fed agreed to provide an emergency loan, through J.P. Morgan, of an unspecified amount to keep Bear afloat. But soon after the New York Stock Exchange opened on Friday, March 14, Bear’s stock price began plummeting.

On Sunday evening, March 16, Bear’s board of directors agreed to sell the firm to J.P. Morgan Chase for $2 per share—a 93 percent discount from Bear’s closing stock price on Friday. (Subsequent negotiations pushed the final price up to $10 per share.) The Fed lent J.P. Morgan Chase up to $30 billion to make the purchase.

But WAITH there’s MOAR … Today IS ALSO rate-HIKE-a-versary (FED STATEMENT HERE, Wiki history HERE) — still time to get cards and flowers for your Fed watchin’ sweetheart

But WAIT, there’s moar … today is ALSO the anniversary of,

… ...The Federal Reserve set the stage for the downturn on Sunday, March 15. Most investors were expecting the central bank to announce its latest response to the crisis the following Wednesday. Instead, it announced at 5 p.m. that evening that it was slashing interest rates and planning to buy $700 billion in bonds to help unclog the markets.

Rather than take comfort in the Fed’s actions, many companies, governments, bankers and investors viewed the decision as reason to prepare for the worst possible outcome from the coronavirus pandemic.

A downdraft in bonds was now a rout...

...“The broker-dealer community was frozen,” said Michael Collins, a senior fixed-income manager at PGIM. “It was as bad as at any point during the great financial crisis.”

...So when Mr. Rao called senior executives for an explanation on why they wouldn’t trade, they had the same refrain: There was no room to buy bonds and other assets and still remain in compliance with tougher guidelines imposed by regulators after the previous financial crisis. In other words, capital rules intended to make the financial system safer were, at least in this instance, draining liquidity from the markets.

One senior bank executive leveled with him: “We can’t bid on anything that adds to the balance sheet right now.”

Jamie lurking ‘out there’ in the waters with FRC hurting? Am I asking the wrong question? Oh, never mind … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower and the curve flatter after and EU bank became the first major global banks to tap an emergency lifeline (link above) since the GFC. German 2yrs (+19bp) have underperformed both Gilt and Treasury peers after that and into the ECB decision. DXY is modestly lower (-0.1%) while front WTI futures are modestly higher (+0.6%). Asian stocks generally followed NY lower overnight, EU and UK share markets are higher (SX5E +0.6%, SX7E similar) while ES futures are showing -0.25% here at 7:05am. Our overnight US rates flows saw a free-fall in Treasury prices after the Europe bank headlines hit with the curve bear-flattening back to yesterday afternoon's NY lows. In London's AM hours we saw modest better buying after the Asian dip with both regions reporting severe liquidity challenges. Overnight Treasury volume was ~160% of average overall.

… Moving on with our attachments, we next show and update of the curve that the Fed/Powell have previously cited as a decent tell of financial conditions and recession risks. It's the 3mo Tsy yield versus the 18mo forward 3mo rate curve which is now closing in on the century low established in 2000 right before to 2001 recession (shaded)

… and for some MORE of the news you can use » IGMs Press Picks for today (16 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

…The situation is fairly binary and you, alongside all the financial markets, are not privy to any of the conversations behind the scenes. In short, Credit Suisse shares fell another -24.24% yesterday, marking its 8th consecutive daily decline (cumulative loss -39.04%) and taking the share price down to an all-time low. Shortly past midnight however, the news came through that Credit Suisse was going to borrow as much as 50bn francs from a Swiss National Bank liquidity facility, and would also be repurchasing certain OpCo senior debt securities of up to 3bn francs. That’s left futures on the Euro Stoxx 50 … It was a wild 24 hours for central bank pricing but since Credit Suisse’s announcement shortly after midnight, there’s been a bit more confidence that the Fed might follow through with a 25bp move at the next meeting. For instance, the hike priced in has gone from 11.8bps at the close last night to 15.5bps this morning, indicating a 62% chance of a move. Investors are also pricing in more rate cuts for the remainder of the year, with the implied rate for the December meeting coming down another -49bps yesterday to 3.75%, and having traded as low as 3.4% intra-day, although again that’s up +10bps overnight following the more positive tone more broadly. Those collective moves prompted an astonishing sovereign bond rally, with the 10yr Treasury yield (-23.4bps) at one point being down as much as 34bps intraday, before closing down -23.4bps, and this morning yields are up a further +2.6bps to 3.48%. Meanwhile the 2yr yield was down -36.3bps to 3.887%, taking it back to a level we haven’t seen since September, with a bounce of +6.3bps this morning.

As far as the USA domestic situation, a note from Goldilocks YESTERDAY

… The macroeconomic impact of a pullback in lending will remain highly uncertain until the extent of the stress on the banking system becomes clear. We estimate it using two approaches. Our accounting approach assumes that small banks with a low share of FDIC-covered deposits reduce new lending by 40% and other small banks reduce new lending by 15%. This implies a 2.5% drag on the total stock of bank lending, which economics studies suggest would result in a roughly ¼pp drag on 2023 GDP growth. Our statistical approach expands our financial conditions growth impulse model to include bank lending standards, which we assume will tighten substantially further, and implies a drag on GDP growth of ½pp beyond that already implied by the lagged impact of the tightening in recent quarters.

We have lowered our 2023 Q4/Q4 GDP growth forecast by 0.3pp to 1.2% to incorporate these estimates of tighter lending standards, reflecting in part a larger downgrade to investment spending…

THAT is interesting and here’s an update from a few moments ago w/supportive factoids

Amid historic volatility & the potential for slower lending in the banking system, we address fixed income investors' top questions about near-term market technicals & key US fixed-income asset classes.

Key takeaways from our questions & answers:

The US banking system is now more constrained, and we expect lending standards will tighten meaningfully.

But the risk of sizeable bank portfolio sales may be overstated given the availability of liquidity through FHLB advances

Downward pressure on UST yields can persist near term as unresolved inflation pressures take a back seat to financial stability concerns

Corporate credit spreads have room to widen further near term given the asset class was a consensus overweight this year & the index carries a heavy weighting toward banks

Munis not set up to rally near term. HTM sales concerns are overstated, but elevated volatility should keep ratios from declining

Agency MBS appears attractive though given spreads near peak COVID level & overstated concerns on bank portfolio selling, though long-term questions on bank demand behavior remain

To be very clear, same firm but economics team reiterating how situation might play out,

Our banking analysts see higher funding costs and tighter lending standards ahead. Tighter lending standards will slow growth and hiring. Weekly lending and labor market data will be the first to show signs of stress, but we're not likely to see the full effects for several weeks.

Our banks analysts see a meaningful increase in funding costs ahead, which will lead to tighter lending standards, slower loan growth, and wider loan spreads.

We were already expecting a meaningful slowdown in growth and job gains over the coming months, and the prospect of substantial tightening in credit conditions raises the risk that a soft landing turns into a harder one.

Tighter lending standards dent job creation. Our models show that a permanent +10pt tightening in lending standards for C&I loans leads to a 35bp rise in the unemployment rate over the next two years.

Smaller firms, which have been a key driver of labor market resilience in recent months, are particularly sensitive to tighter bank financing conditions. Despite recent hot prints, job gains could slow quickly as a result.

While we will be watching lending data closely, it will take time for tighter lending conditions to show up in the macro data. Weekly initial claims should provide the earliest evidence but historically, recessions have arrived more than half a year after jobless claims begin a sustained rise.

For the upcoming FOMC meeting, we still see the Fed following through with a 25bp hike in response to persistent inflationary pressures and a very strong labor market. That said, the Fed has little incentive to surprise markets in this volatile environment, and we think it will stand ready to adjust the rates and balance sheet paths should conditions warrant.

… Our forecast for growth and jobs this year was already for further deceleration into 2Q and 3Q23, but recent developments pose further downside risk. We currently forecast real GDP growth this year at 0.4% 4Q/4Q and 1.2% 4Q/4Q in 2024. In our forecasts, nonfarm payrolls decelerate from 311k in February 2023to a low of 50k by September 2023, pushing the unemployment rate up to 4.0% by year end. With greater risk of tighter lending standards among banks, loan growth, job growth,and overall economic activity could decelerate more significantly. We see risks that a soft landing turns into a harder one.

Lending standards were already tightening

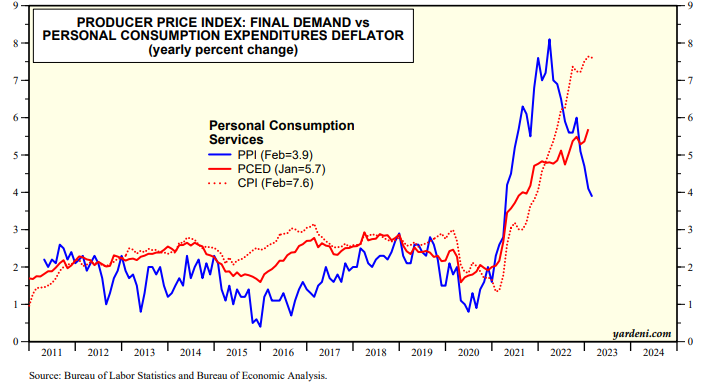

AND to be safe, a Yardeni QUICKTAKE post PPI as the Fed (and global CBs) are,

All of a sudden, we are hearing more chatter about deflation. Yes, that's right: deflation. The story line is that the regional banks will respond to the SVB debacle by lending less to lots of middle market businesses, especially if depositors move their funds to the money center banks or to the money markets. The result will be a credit crunch and a hard landing forcing companies to cut their prices and labor costs by cutting wages and payrolls.

… The PPI inflation rate for personal consumption on services is down from a peak of 8.1% early last year to 3.9% in February (chart). The services components of both the CPI and PCED are much higher at 7.6% and 5.7% because they include rent, which is likely to disinflate during H2-2023.

Over to YOU Lagarde … we’re all watching.

And in as far as an IDEA … from the bank of our great land,

Trades for when the tide goes out

… Buy staples, sell tech for the bear finale US households bought $4.4tn of equities the past two years and never sold, an anomaly versus other bear markets; but also sensible while earnings were rising (Exhibit 7). Falling profits (-9% in ‘23), higher discount rates, and tempting cash yields should spark outflows. Note when lending standards tighten this much, a recession has always followed (Exhibit 10). Buy staples (IYK) & sell tech (QTEC) for the reset (Exhibit 1).

AND finally, some tongue-in-cheeky analysis by John Authers

Markets are behaving as though this is already a crisis — or at least some of them are. Bond markets have been turned upside down across the world, with the two-year yield in the US now some 120 basis points lower than a week ago. That betokensa seismic shift in the financial system. In economics, markets have the ability to create their own reality. Within days, they’ve forced the Federal Reserve and the Swiss National Bank to intervene to aid banks. But is it a crisis?

… And that was all before the banking system began to reveal large cracks hammered in large part by the Fed itself. Thus, many now think that Powell’s plans are unraveling. Stephanie Lang, chief investment officer at Homrich Berg, said that ‘’things are kind of coming to a head in terms of starting to see cracks in the system” following a previous focus on employment.

Just look at Treasuries, whose yields surged across the curve again Wednesday after tightening during Tuesday’s trading. The 10-year yield tumbled more than 20 basis points to 3.46%, inching closer to its low for the year. (The announcement from the Swiss National Bank has, at the time of writing, buttressed confidence a little, with the 10-year yield back to 3.5%.) Traders are now abandoning bets on additional rate hikes and have begun to price in rate cuts. Swaps traders now put roughly 50-50 odds on either a pause next week or a quarter-point increase.

The remarkable shift in narrative and sentiment has gone from how much the Fed will hike to whether it will hike at all. Economists at Nomura Securities are taking it a step further by predicting the Fed will cut its benchmark interest rate by a quarter-percentage point and stop reducing the size of its balance sheet…

AND so it goes … NARRATIVES always FOLLOW PRICE.

Happy JPM BUYS BEAR and / or C19 ALMOST broke markets A-Versary!!