Is hawkish bearish?

Is hawkish bearish?

It seems to me we’ve forgotten June FOMC risk where a hawkish sounding JPOW led TO a significant bond bullish flattening reprice. Perhaps its different this time as THEN was more about trial balloons and signal flares and now reality and gravity of the moment is setting in.

I HAD thought BRAINard (incorrectly perceived IMO to be more dovish) would have been a BEARISH event while a JPOW (relatively more hawkish) top ticket to be less bearish.

Citigroup:

…In terms of the next calendar risk apparent, the FOMC Minutes due Wednesday provide limited hope for bond bulls after the duo of Clarida/Waller noted preference for speeding up the balance-sheet taper (the latter also endorsing outright BS contraction if his forecasts come to fruition). As our Citi Economists note in their (linked) preview, their may be some natural extension of the “hawkish optionality” theme in the Minutes, with “at least some hawkish Fed officials (who presumably pushed for this type of language) possibly explicitly arguing that a faster pace of tapering might be preferable to create options to raise rates earlier should inflation prove stronger than expected.” An even more hawkish risk would be if a sizable contingent (e.g. “many”) expressed a similar view. As this translates to our view on real rates and their ‘sell by date’ in Q1 2022 (when global CB liquidity deltas turn negative), a broadening endorsement of a faster-taper could easily accelerate that time-line…

FAIR. Keeping in mind, too, the core / inner circle AT the Fed is about to change and whether it’s to change for the more or less dovish (bearish/bullish … please choose one) remains to be seen.

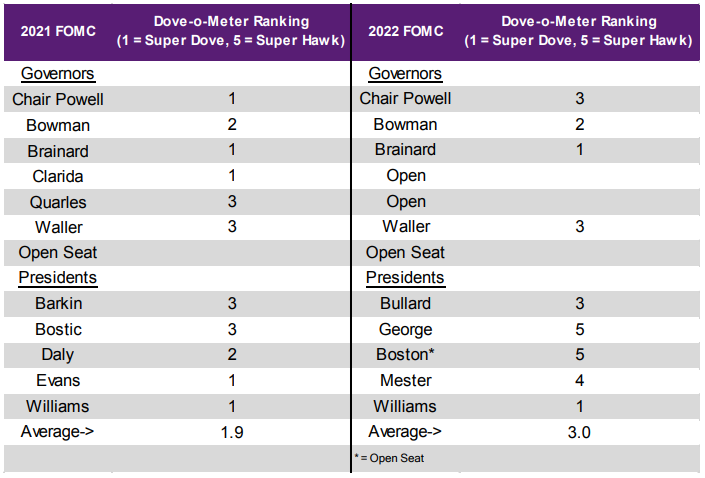

There are NO shortage of VIEWS and opinions. This from Natixis (LaVorgna) note titled, When Doves Fly:

The Administration announced its intention to reappoint Jay Powell as Fed Chair. There are two takeaways from his renomination. One, the Administration is more confident in the probability the Build Back Better plan (BBB) will be passed. Recall the House passed its version of BBB late last Thursday. The Powell renomination was a bargaining chip in the case BBB faltered. Two, the probability of more aggressive Fed policy next year—i.e., accelerated tapering and more tightening than the two and half 25 bp rate hikes currently in the curve—is much higher now than if Brainard took over…Powell may be less dovish next year now that he is reappointed. Ranking him a 3 pushes the average to 3.0. While still moderate, next year’s ranking still represents a big relative shift away from dovishness. The upshot is that the Administration may be incentivized to fill the governorships with super doves to minimize the chance the Fed aggressively hikes rates next year.

What this will do to the curve, nominals and REALZ remains to be seen BUT a better than 10bps move UP in 10yr TIPS yields (ie REALZ)

(pinch / zoom on bottom RIGHT)