Good morning … due to holidays, friends, family and TIME being the most precious of all commodities, I’ll be brief. In fact, since I cannot say it any better …

I’m not doing content today, because I figure nobody is bored at the office reading newsletters while they pretend to work.

But I did want to thank all of you for reading and subscribing … The whole point of Thanksgiving, beyond the food, is to express gratitude, and I am really just incredibly grateful to have such an amazing audience…

Now as the parade has been watched and football is underway, what follows IS for any NYG fans who will be looking for something to do / read inbetween turkey / games …

WEDNESDAY defined … before the deluge of data Wednesday, some news which brought me back to the EZ debt crisis (PIIGSB)

ZH: Frexit Fears Reignite As Market "Storm" Drives Core EU Spreads To Crisis Highs

… and in as far as that deluge of data goes …

ZH: Q3 GDP Unchanged At 2.8% In Second Estimate ZH: Continuing Jobless Claims Top 1.9 Million Americans - Highest In 3 Years ZH: US Durable Goods OrdersDisappoint In October, Stagnant For 19 Months

… these were all the appetizer while the main course of the deluge, then was …

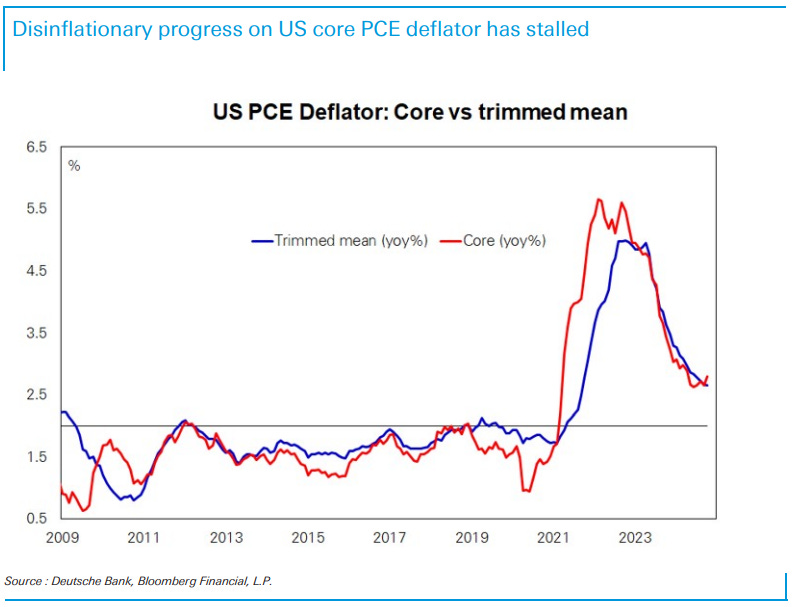

WolfST: Inflation Re-Accelerates Despite Plunging Gasoline Prices as “Core Services” PCE Price Index Hits 7-Month High

…The Fed has already been talking down the pace of future rate cuts recently, including in the meeting minutes yesterday and in speeches by Fed governors.

… Year-over-year, core services PCE price index accelerated to 3.9%, the fastest increase since May. There has essentially been no progress since May:

ZH: Savings-Rate Revisions Erase $140BN In American's Wealth As Fed's Favorite Inflation Indicator Jumps To 6-Month High

… The Fed's favorite (when it's going down) inflation indicator - Core PCE - ticked up noticeably in October to +2.8%, the highest since April...

… and this all part in parcel helped combine to create a powerful BID for 7yr …

ZH: Yields At Session Low After Solid 7Y Auction Stops Through

Moving along to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … First up, an economic recap / victory lap …

BARCAP: Second Q3 GDP estimate unchanged and consumer on solid footing for Q4

The second Q3 GDP estimate was unchanged at 2.8% q/q saar amid mixed revisions to its components. Real PCE growth slowed in October, but appears on still-solid footing for Q4. Equipment investment, though, looks to be soft in Q4, contributing to slower GDP growth.

BARCAP: October PCE inflation stays firm, as expected

Core PCE prices rose 0.27% m/m in October, raising the annual rate to 2.8%, while the September print was revised marginally higher (+1bp). With the data largely in line with our expectation, our Q4/Q4 core PCE estimate for 2024 is unchanged, at 2.9%.

…While our baseline expectation is for a 25bp cut at the December FOMC meeting, we think it is likely to be a close call. Recent elevated inflation prints, while not worrisome, are also not ideal for the FOMC. In addition, data on activity continue to look reasonably strong. This puts the spotlight on the upcoming November payroll report, which is likely to provide a cleaner read of the underlying labor market momentum following a hurricane- and strike-disrupted October report. The CPI and PPI data just before the December FOMC meeting will also factor in to the policy deliberations.

BARCAP: Federal Reserve Commentary: November FOMC minutes: Confident, for now

The November minutes indicate that the FOMC saw balanced risks to its dual mandate objectives and viewed gradual adjustments as most appropriate. Although there was no mention of Trump policy shocks, apprehension about the durability of favorable supply conditions foreshadow tensions ahead.

… next up, best in show … stopped OUT 2s10s steepener, remaining LONG FF and continues to like fading any 'post-NFP selloff in 2s as long as UNR retains 4-handle’ …

… The broader tone of consolidation in the Treasury market remains in place and as 10-year yields slip back down to 4.25%, we have taken solace from the conspicuous absence of bearish follow-through after the benchmark momentarily touched 4.50%. From here, we view a move back toward 4.0% as more likely than a meaningful break above 4.50%. However, our base case outlook is for the 10-year to hold the prevailing range of 4.00% to 4.50%, with a bias toward the lower bound as the balance of the trading year unfolds. The Fed remains on its normalization track even as the uncertainties regarding the cadence of cuts will only be resolved by the realized economic data …

… Here’s a note from France … ‘bout France …

BNP: France: What to watch out for in the coming days

KEY MESSAGES

Risk events are accumulating in the next few days – we draw a list of what to watch out for and our views.

Caution will still be warranted, particularly ahead of next week when the risk of a no-confidence vote is intensifying.

However, we maintain our base case that there is a greater chance that the government passes the budget and survives a no-confidence vote. Hence, we see room for some opportunities arising next week but prefer to wait before stepping in.

… here’s a chart from best techAmentalists out there and one that might help continue to spread little joy esp for those travelling by car …

…WTI futures (CL1) A similar picture in WTI futures, with a bearish outside day on Nov 25. This adds onto the trend lower that we have seen. Momentum also remains weak, as evidenced by weekly slow stochastics ticking lower.

The next support level is at 65.27-66.33 (2024 low and October 2024 low). Below that, we see support at 62.43 (Dec 2023 low).

… next up a German bank Chart of the Day caught my eye …

Cross Sector We look for a mild downshift in growth to 2% and continued deceleration in core inflation, allowing the Fed to ease an additional 100bp by YE25. Look for lower yields, led by the front end, with higher term premium leaving curves steeper. Expect QT to conclude by 1Q25, leaving front end swap spreads wider. We project HG corporate spreads can reach all-time tights and think corporates can outperform mortgages. We expect fixed income net issuance to step down modestly while demand should firm across the board.

Governments We see more room for the front end to outperform as the Fed eases through 3Q25. We forecast 10-year yields to fall to a low of 4.10% in 3Q25 and to rebound to 4.25% by YE25. Stay long 2-year Treasuries and maintain 10s/30s steepeners. We recommend 64:11 weighted 3s/10s/30s belly-cheapening butterflies to position for higher term premium. We discuss the supply/demand backdrop, which should keep yields anchored at higher levels. Slow progress on inflation, policy uncertainty, and an asymmetric easing bias from the Fed should keep TIPS breakevens trading near the rich end of the range through 1H25. We target 10Y breakevens at 235bp at midyear and narrowing modestly over 2H25. We see slightly positive Agency issuance, driven by rising home prices. Agency spreads are tight and privatization concerns present a bearish risk…

…Treasuries How I learned to stop worrying and love higher yields

We project 100bp of further easing by 3Q25 with the Fed funds rate target range troughing at 3.5-3.75%. OIS forwards are pricing in a more hawkish path than our forecast and look cheap after controlling for Fed speak and growth expectations...

... Meanwhile, historical precedents show yields tend to decline through shallow cutting cycles. Coupled with the Fed’s asymmetrically dovish bias, we think this favors lower front-end yields in 1H25. Stay long 2-year Treasuries.

Longer-dated Treasuries have diverged sharply from their fundamental drivers recently, but we think there’s limited room for yields to decline...

...This cheapening reflects higher term premium, supported by the shift in demand toward price sensitive investors. Over time, we expect this shift to continue, and recommend positioning for higher term premium via 64:11 weighted 3s/10s/30s belly-cheapening butterflies.

The long end should steepen as front-end yields decline, but we recommend avoiding wider steepeners which could be exposed to expanding term premium: maintain 10s/30s steepeners.

We expect Treasury market liquidity to improve further as volatility declines, supporting less liquid sectors like Coups vs. Ps. The main risk is further tightening in funding conditions…

Technical Analysis We believe Treasury yields will remain in the broad two-year ranges through the first half of 2025 with a bias that the front end eventually trends back toward the lower end of its range, and the longer-duration sectors trade relatively stickier in the middle of those ranges. We are closely monitoring 10-year TIPS breakevens that have rebounded from near 200bp to key resistance levels at 242-252bp in the fall. Market differentiation between reflation and inflation expectations is critical not only to our Treasury outlook, but to all our global market views. We believe a material push through 250bp would mark a watershed event and likely drive a dramatic shift in monetary policy expectations that will resonate across equities, FX, and commodity markets…

…Figure 86: The bullish momentum divergence buy signals on the 5-year note yield monthly time frame that triggered as the market set the cycle cheap in 4Q23 left us looking for further bullish base building and an eventual impulse back through 3.00%. While the 2022-2024 range still marks a potential bullish head and shoulders yield top, the fourth quarter price action and response to robust data and the US election outcome favor a continuation of the same yield range through the first half of 2025... 5-year note yield, monthly bars with momentum divergence signals

… finally, the covered wagon folks had this to offer …

United States: Data Came in Like a Butterball Anyone who has ever gobbled until they wobbled can tell you it can be challenging to digest too much at one time. In the financial world, you know it's Thanksgiving when you get a full slate of economic data stuffed into one day. Nobody is relegated to the kids table as we break down what all this data mean for the outlook.

Gas prices at the pump continue to decline, which is another tailwind to consumer spending, see chart below. The decline in oil prices is driven by significant supply and production in the US and lower growth in China.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

I now return you to your regularly scheduled programming, whatever that may be … Not sure WHEN next post will be and I hope you find whatever it may be you are looking for and my HOPE is some / all of this may help as YOU plan your very own holiday / year ending trades and trade your holiday / year ending plans …

Happy Thanksgiving !!!!

Thank you for your excellent work........

Hey Buddy 😁