The story sets up and defends what is know as the steepening yield curve trade where one sells longer maturities and channels those funds TO the front-end.

… The Federal Reserve’s recent pivot towards a more aggressive strategy to fight elevated inflation has flattened the so-called yield curve, a signal that some investors anticipate that the US central bank’s policy tightening could eventually crimp longer-term economic growth.

The yield curve shows the different interest rates that investors demand for holding shorter and longer-dated government debt.

But traders and strategists say that some hedge funds are wagering that the yield curve will not flatten much more. Instead, they are once again betting that yields on long-term US government bonds will eventually rise, and rise more than yields on shorter-term debt.

YESTERDAY I offered a look at what I view as an increasing short-base but one that’s far from compelling (ie they’ve gone TOO far and short covering BUYING is the more clear and present danger). The FT STORY offers a look and guess as to the other side of the coin, noting

… Hedge funds have been making this bet on a steeper curve on and off for months, expecting that as economies emerge from coronavirus lockdowns inflation will accelerate and longer-term bonds will sell off, pushing yields higher.

But while it worked in the first few months of this year, the bet proved painful during the spring and early summer, and again in the autumn as the market moved to price in the likelihood that central banks would act to curb inflation.

“It has been very, very difficult to make money from steepeners this year,” said Andrew Beer, managing member at the investment firm Dynamic Beta Investments.

… Leveraged funds for the past two weeks have held net bullish bets on two-year Treasuries futures at just below the seven-year high hit in November, CFTC data showed. While the trend weakened slightly in the seven-day period ending December 21, it is notable that it did not soften even more following a strong hawkish signal from the Fed, which lifted yields on the two-year while sinking prices.

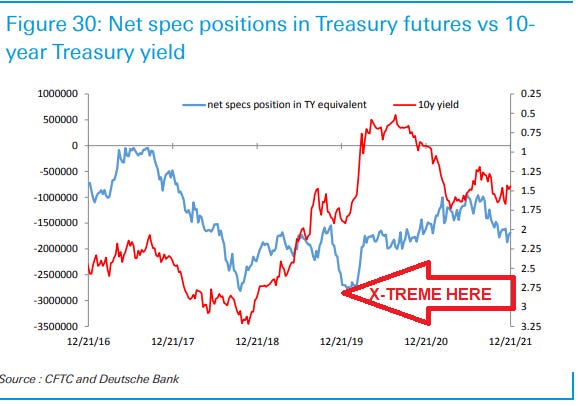

At the same time, funds have been increasing their short positions and trimming their long positions in 10-year futures — a bet that prices will fall and yields rise — pushing their net position to the lowest level since March.

“Levered funds were increasing their steepener positions going into the Fed meeting,” said Gennadiy Goldberg, senior US rates strategist at TD Securities. That the positioning has broadly held since the Fed meeting indicates that some hedge funds are moving against the grain.

Decio Nascimento, chief investment officer at the hedge fund firm Norbury Partners, said he had recently put on US steepeners as his fund’s biggest position as the curve had flattened. He highlighted how long-term interest rates on swaps, tools that let investors protect against bond market fluctuations, briefly fell below shorter-term ones, which he said “makes little economic sense”.

Speculators and levered funds activities are fun to watch and I too used to look towards this crowd for any sort of ‘tell’.

At the moment, though, based on what I can see, there simply doesn’t seem to be any ACTUAL risk of pain here. Not yet. Somethings will have to continue to develop (shorts of 10s will need to grow MORE THAN THIS and longs in front-end — pricing in the END OF HIKES? will have to increase, too).

For now, though, it would seem to ME that writers of these stories are simply trying to please editors with word salad and truth is, nobody here to read this increased word count …

Those who ARE ‘important’ will show up for todays liquidity event — 7yr auction (1p) — make a brief appearance on the bid / offered side in rates — and then head right back beneath the rock from which they came.

showing leveraged funds’ net positions in two-year Treasury futures")

showing leveraged funds’ net positions in 10-year Treasury futures")