A nice recap of the week that was and including a few tidbits from BMOs Lyngen - the best in the biz of stratEgery, To believe in the specific excerpt which I’ve highlighted for you just below, well, one would have to believe ‘its different this time’. OR, if you prefer, one would have to ‘believe in Santa Claus’ and hey, I know grown men who still believe in the NY Giants (ahem …)so maybe this time, the Fed will get it right?

Not A Drill

Coming into this week, March was seen as a ‘live’ meeting for a potential Federal Reserve rate hike. Now it’s viewed as all but a lock. Swaps show March hike odds at about 82% as of Thursday evening in New York, up from about 66% at the start of the week.

Bets were recalibrated following the release of the Fed’s December meeting minutes, which showed that officials are prepared to move perhaps more quickly than thought on both rate liftoff and, potentially, balance sheet runoff -- a message that’s been taken as unequivocally hawkish across asset classes, and spurred a flurry of Fed-speak in the aftermath.

As a result, we’re suddenly staring at a 10-year Treasury yield north of 1.72%, after closing 2021 closer to 1.5%. What’s interesting about this selloff is that it’s been driven entirely by real rates, rather than rising inflation expectations. Yields on inflation-adjusted 10-year Treasuries have surged by 31 basis points so far -- the biggest weekly jump since March 2020! -- while 10-year breakeven rates have dropped nearly 10 basis points.

To Ian Lyngen at BMO Capital Markets, the dynamics speak to a renewed confidence that policymakers will be able to thread the needle between restraining inflation without crimping growth.

`Single Highest Conviction’

Even still, 22V Research’s Dennis DeBusschere says this week’s rise in real rates is just the start. In fact, higher real rates is the “ single highest conviction” call of 2022 for DeBusschere, who was voted as the No. 1 U.S. portfolio strategist in last year’s Institutional Investor survey.

That could make for an extremely interesting and volatile equity market in 2022. This week provided a preview of what that might look like -- the stock market’s most speculative corners were hammered, with the likes of profitless technology shares, recently public companies and Cathie Wood’s ARK Innovation ETF (ARKK) plunging.

It was less ugly on the index level -- the S&P 500 is roughly 1.5% lower, which would be its worst week since only mid-December. And even with rising real yields, DeBusschere sees the benchmark rising to 5,040 by-year end, from just below 4,700 at Thursday’s close.

That seems to be the consensus among Wall Street as well -- that generally, the broadly measured stock market should be fine. The average year-end S&P 500 forecast in a Bloomberg survey of strategists stands at 4,950, which isn’t amazing, but it’s still a gain (and already, targets are moving higher). However, the richly valued and hyper-growth stocks at the equity market’s riskiest fringes may be first in the firing line.

If You Insist...

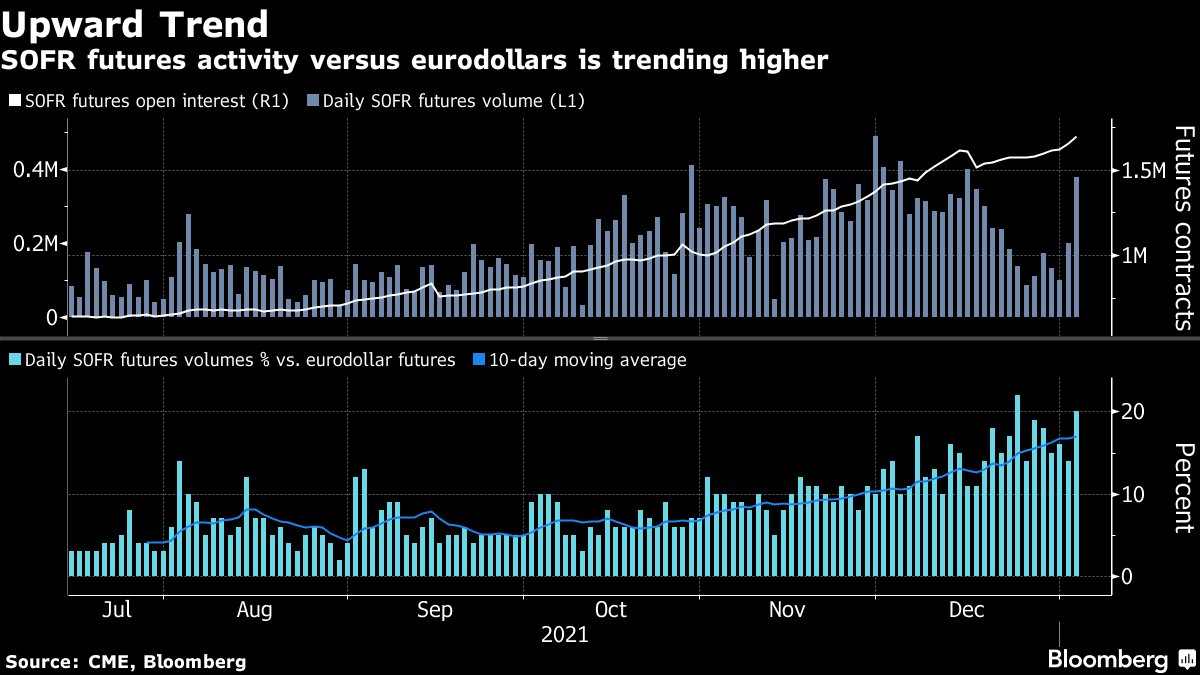

The London Interbank Offered Rate is finally dead -- kind of. Over the past two years, regulators have dragged U.S. traders kicking and screaming to take its anointed successor, the Secured Overnight Financing Rate, seriously. This week, signs emerged that they finally are -- kind of.

As chronicled by Bloomberg’s Edward Bolingbroke, a short call position in December three-month SOFR options hit the tape on Tuesday, days after most versions of Libor were published for the last time. The total trade size was just 5,000 contracts, which would barely register as a blip in most established options markets. For SOFR, it was gigantic -- that single trade more than doubled the outstanding positions held across all three-month SOFR options to a whopping 7,772 contracts as of Tuesday’s close.

So the good news is, SOFR futures activity is rising. The not-as-great news is how far activity still has to pick up before the options actually attach to the freshly adopted overnight rate. Comparing it to other futures contracts make that abundantly clear: average daily SOFR volumes clock in at around 17% of eurodollar futures. That’s up around about 5% at the start of October, but as Bolingbroke describes, the still-shallow market makes hedging tricky.

That’s the potentially bad news. After the Fed’s December meeting minutes dropped on Wednesday, a March rate hike is seen as more likely than not. Instead of leaning on SOFR-based options to hedge positions around the Fed’s expected liftoff path, traders will likely still have to tap eurodollars options to do so, rather than turning to Libor’s heir.

Drowning In Debt

The rush for corporations to borrow bonds turned into an all-out sprint. More than $59 billion of investment-grade debt has priced so far this week. Tuesday’s $23 billion tally was the largest single-day for U.S. high-grade credit since September, and competition was fierce enough that four borrowers stood down.

Fueling the frenzy is the ever-present fear that the ultra-easy window to lock in cheap financing -- one that was thrust open by the Fed -- may be closing soon. That fear was brought into sharper focus this week, with Treasury yields screaming higher in the lead-up to and the aftermath of the Fed minutes.

In some ways, the dynamics between the credit and government bond markets were self-fulfilling this week. Spooked by the prospects of rising yields, corporate issuers dove headfirst into primary markets. To make room for the deluge of incoming blue-chip bonds, investors offloaded Treasuries -- driving yields even higher.

In any case, a boatload of bonds were sold with seemingly little indigestion, and buyers were largely left holding the bag. A Bloomberg index of investment-grade returns sank 1.13% on Monday -- the lousiest one-day showing since March 2020. The gauge has dropped every day so far this week. Despite their relatively lower duration, junk bonds haven’t fared much better as stocks swoon -- the U.S. high-yield index has posted seven straight days of losses.

But even with the blip, junk issuers are also getting in on the action. After a slow start to 2022, the primary market kicked into gear on Wednesday, lead by the likes of ZipRecruiter Inc. and Golden Nugget Inc.. Meanwhile, investors shuttled money into high-yield funds for a third straight week, Refinitiv Lipper data show.

And while investment-grade and junk debt both buckle under the combined weight of Fed anxiety and equity turbulence, floating-rate debt is on a tear. A gauge of loan prices hit a more than seven-year high on Tuesday, riding a boom in demand for inflation protection. Relative scarcity is also a tailwind -- while the tally of U.S. loan sales was the highest since 2017 last year, the new issue market has had a sleepy start to 2022.

“This is consistent with the FOMC Minutes reinforcing the Committee’s hawkishness and reflects investors’ renewed faith in the Fed’s ability and willingness to combat the amount of inflation presently in the system,” Lyngen wrote in a note. “As a vote of confidence in the growth outlook, this combination of moves speaks to the degree of recovery optimism that has been brought into the new year.”

Of course, there’s one big question mark left this week: Friday’s U.S. jobs report. BMO’s informal pre-NFP survey found that 45% of respondents would buy into post-payrolls weakness, compared to the 38% average. Meanwhile, the $17 billion iShares 20+ Year Treasury Bond ETF (ticker TLT) is nearing oversold territory on its 14-day relative strength index, and 10-year yields are a few basis points away from last March’s 1.77% high-water mark -- so perhaps we’ll see bond dip-buyers emerge before too long.