Treasuries have been led lower by intermediates overnight with the UK/EU markets following along amid locally 'overbought' conditions here and historically elevated tactical longs (see 2nd bullet above). DXY is little changed (see attachments) while front WTI futures are higher (+1.7%). Asian stocks were generally higher, EU and UK share markets are all modestly higher while ES futures are showing -0.2% here at 6:45am. Our overnight US rates flows saw a heavy trade in Treasuries after Tokyo CPI surprised on the upside, pressuring long-end JGB's. We saw better net selling in intermediates and the long-end with the curve bear steepening. The London session was a bit subdued but fast$ was a pretty consistent seller of 5's and 7's this morning. As the desk noted today, real$ has been buying on the real rate story while HF's have been selling on the valuation story. Hmmm... We discuss this kind of tension below. Overnight Treasury volume was about average overall with 7yrs (179% of ave) a turnover standout among peers, matching our flows.

With this past weeks liquidity events (aka US Treasury auctions) going 3 for 3 so, batting 1000% (only 17d 17hrs ‘til spring training), thought I’d pass THIS ONE from Bloomberg along

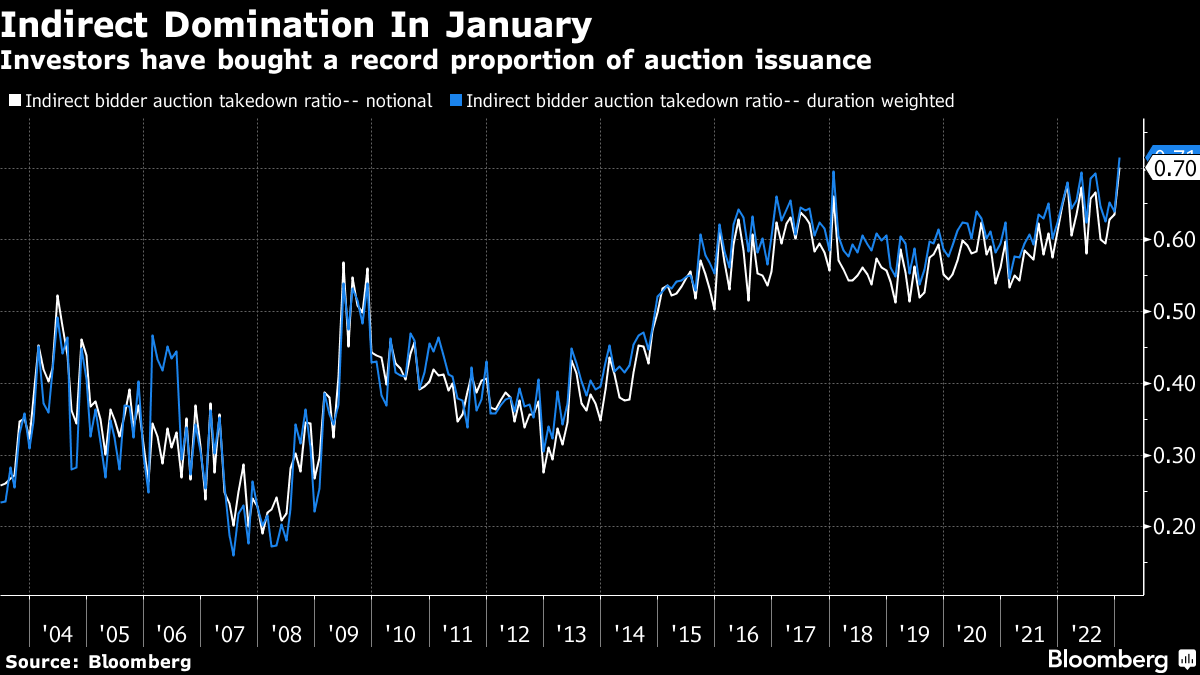

The Weekly Fix: Overseas Bond Buyers Are Buying the Fed’s Pivot

Big in Japan (And Likely Other Countries As Well)

It’s well-documented that bonds are back in vogue. It appears that’s especially true for overseas investors.

Each of the Treasury auctions this month were awarded at a yield lower than expected based on pre-sale trading, known as “stopping through” — meaning that demand was strong. Primary dealers (who are obligated to bid) in Thursday’s $35 billion offering of seven-year notes picked up just 6.1% of the securities, the smallest in any Treasury note or bond auction in data going back to 2003.

There’s a common undercurrent powering the demand: international buyers.

“Every single Treasury auction so far this year has gone incredibly well and the interest is coming from foreign buyers,” JPMorgan Asset Management fixed-income portfolio manager Kelsey Berro said on Bloomberg Television. “So for those that think that the debt ceiling is scaring away that foreign interest, we’re not at all seeing that yet.”

Indirect bidders — a category which includes international investors and global central banks — have been showing up in force in Treasury auctions this year after a rather subdued showing in 2022. Indirect bidders accounted for 75.7% of Wednesday’s $43 billion sale of 5-year notes — a record share. They snapped up 77.1% of Thursday’s seven-year auction versus a six-month average of 67%.

The reignited appetite suggests that overseas investors are buying into the idea that the Federal Reserve will pivot in the not-too-distant future, according to Ian Lyngen of BMO Capital Markets.

“Investors can see the end of Fed hikes and with the new year have been suffering from some yield FOMO,” Lyngen said. “They are positioning for two to three years, not two to three weeks. In the next 24 months, the Fed will have to cut rates by at least 100 basis points, if you believe the Fed’s own projections.”

One Hand Will Break What The Other Hand Builds

Just a few short days until the Fed’s February rate decision, and the overwhelming consensus is that Jerome Powell and company will downshift once again and hike by just 25 basis points. Mohamed El-Erian — a man of many titles, including Bloomberg Opinion columnist — made a persuasive case on Thursday that the central bank should eschew market prescriptions and fire off another half-point increase instead.

El-Erian arrived at that conclusion via several well-articulated arguments, but I want to focus on just one:

Financial conditions have loosened significantly in recent months and, by some measures, are around levels that prevailed last March when the Fed initiated this hiking cycle.

‘By some measures’ is a key phrase. As described by Powell in the past, financial conditions — a measure of strain across asset classes — are the mechanism through which monetary policy impacts the real economy. A Bloomberg gauge shows that conditions are at looser levels than before the Fed’s liftoff last March.

While the Bloomberg measure and others like it can be brushed off as giving too much weight to the equity market, other measures paint a similar picture. Take the Chicago Fed’s National Financial Conditions Index, which provides a comprehensive weekly update on financial conditions in money markets, debt and equity markets.” While still tighter than prior to March’s liftoff, the gauge shows that conditions have loosened significantly since the start of 2023.

“The Chicago Fed tells you that financial conditions have eased a lot more than market-based measures,” said Priya Misra, TD Securities’ global head of rates strategy. “It’s tricky for the Fed. As they are likely to downshift again, financial conditions have eased. So the market is undoing some of the tightening the Fed wants to put in the system to slow inflation.”

THE NOTEcontinues talking of differences between Libor and SOFR and credit. Worth a CLICK.

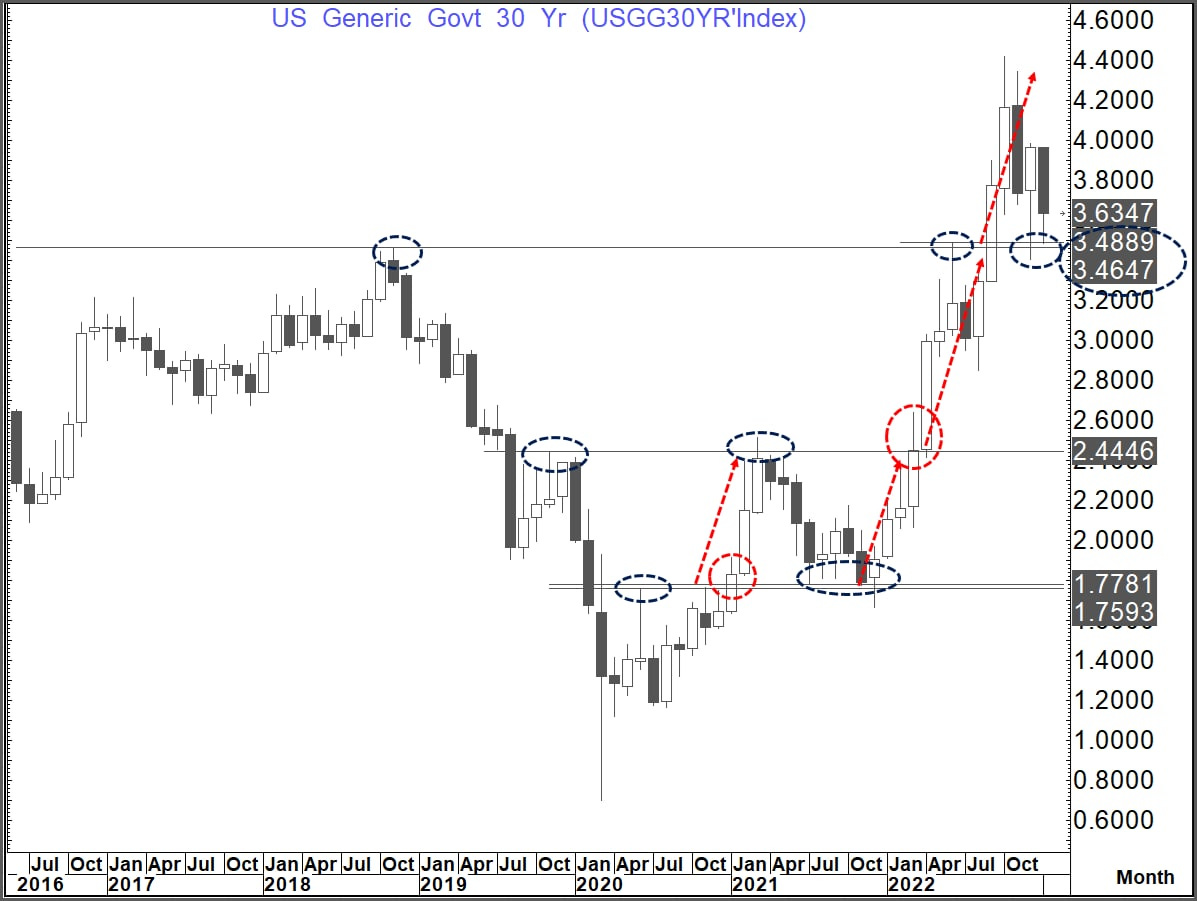

I would ALSO note a couple ‘dinosaurs’ sittin’ around and talking bonds (the best techAmentalsists out there) recently making some observations which I thought might be of interest.

… we remain very focused on the T-Bond/ US 30 year yield as in this cycle we feel it has had excellent directional bias around important levels.

That does not mean that we think the US 30 year yield will necessarily be the “biggest mover” in town but rather that it could be a major signaling indicator as it has been in most of this cycle

US 30 year yield has been an important directional indicator around pivot points

1. The first notable rally in the 30-year yield hit a peak at 1.76% in June 2020

2. In Jan 2021 it broke through that level accelerating up to major resistance at 2.44% in March which held on a monthly close basis.

3. A correction ensued taking the yield back down to the 1.76-1.78% area again but despite a 6 month period of testing it could not establish a monthly close below this range (prior resistance now support)

4. In December 2021, the low was posted and became the platform for the next move higher

5. In March 2022 we got a monthly close above the 2.44% level and accelerated higher to good resistance at 3.46% by June (Major Nov 2018 trend high)

6. We then saw a fall for 2 months before the yield rose again, had a monthly close above the 3.46% level in September and accelerated to the trend peak at 4.42% in October

7. It then fell yet gain and tested the 3.46% to 3.49% range in December and again this month (major high in November 2018 and failed break high in June 2022). Sop far this range is holding on a monthly close basis.

This is, in our view, a hugely important range as it was both the acceleration point of the surge to the trend highs as well as the cycle high in 2018.

RANGEZILLA in mind they discuss some other pertinent levels to watch in coming days/weeks/months noting a longer-term visual of 30yy,

… IF, however, this level was to continue to hold we would look for it to be the platform for the next move higher to likely new highs.

How high would that suggest?

On the long term chart that is pretty clear

A break would suggest the potential for a new high in the region of 4.80-4.85%

If we made that break, then the most obvious target would be back to the 2008-2011 highs posted between 4.80 and 4.85% …

John Boehner made famous the saying, “IF ‘ifs and and buts’ were candy and nuts every day would be Christmas'“ and this is NOT to be definitive stance simply an update which shows bond buyers buyin and daily, weekly, and MONTHLY closes of importance which should also be kept in mind…

Sorry for lack of daily updates past week or so. Been outta pocket — LIFE happening — and hope to get back soon … THAT is all for now. Off to the day job …