BUY 20s (vs 10s30s)

I missed this over the weekend when creating and posting THIS UPDATE with a few sellside observations (of this upcoming FOMC and more than a few 2022 outlooks) and I’m always FOR a good idea. The only way to know one is to read ALL ideas … good and bad … and decide for yourself. That in mind, one of global Wall Street’s favorites, Mike Cloherty (currently of UBS) suggests a new idea this past week.

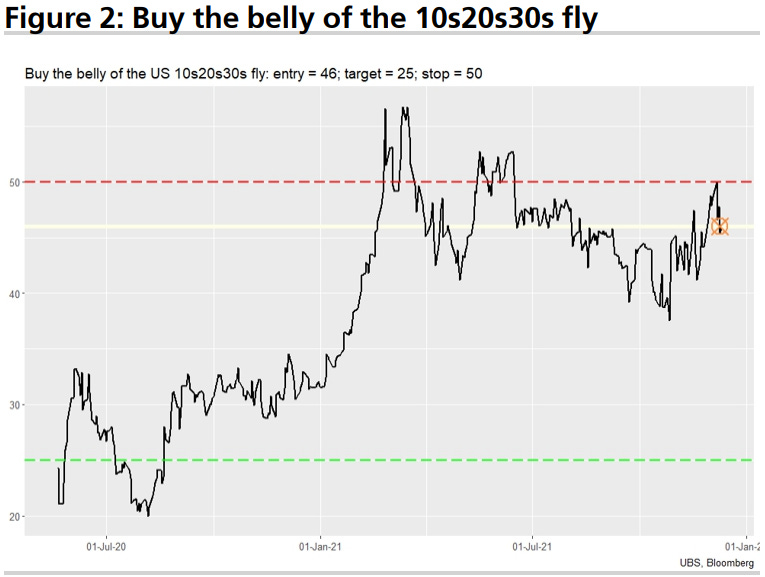

Buy the belly of the 10s20s30s fly (enter ~46bps on 9th Dec w/target of 25bps and stop @ 50bps … notes carry / roll of -0.1bps/3m). From the horses mouth:

Being long 20s has been one of the pain trades in recent months, but the fact that 20s have outperformed the last two days despite 20yr supply coming next week makes us think the bad position overhang is eroding.

The main driver of this trade is that the Treasury was issuing too many 20s, which created a large supply/demand imbalance that caused a hump in the bond curve. The Treasury was aggressive in cutting 20yr issuance with a $5bn cut in November. Unfortunately this was not enough of a cut to clear up the supply/demand imbalance, so we would expect the Treasury to follow up with $5bn cuts in Feb and May. By that time, supply and demand should be much more balanced causing the hump to fade.

This means we see two legs to the outperformance of 20s. First, the recent cheapening caused by stop-outs of long 20yr positions should be reversed, with help from additional risk capacity coming into the market in the new year. Second, continued auction cuts should balance supply and demand by mid-year.

The main risk to the trade is that it means being long a less liquid point and short two more liquid points, leaving a short liquidity profile that creates risk in a flight-to-quality.

EMPHASIS mine. Food (and a UST trade idea) for thought as day and week gets underway … keeping in mind this time of the year is among THE worst in as far as bond / other markets liquidity goes …