Good morning … Catching up and heading through the inbox best I can a couple / few items which stood out are noted below but first, I see I cannot trust y’all to manage a long bond with a bid in my absense?

AND … the range persists as it appears to my now unprofessional eyes, the (declining)50dMA was RESISTANCE and we’re approaching TLINE support as we continue ‘triangulating’ and as bonds move higher, momentum does appear to be gently into oversold territory — not quite ridiculously so OR on verge of bullish cross and so … patience, grasshopper? In as far as WHY yields leaking back up?

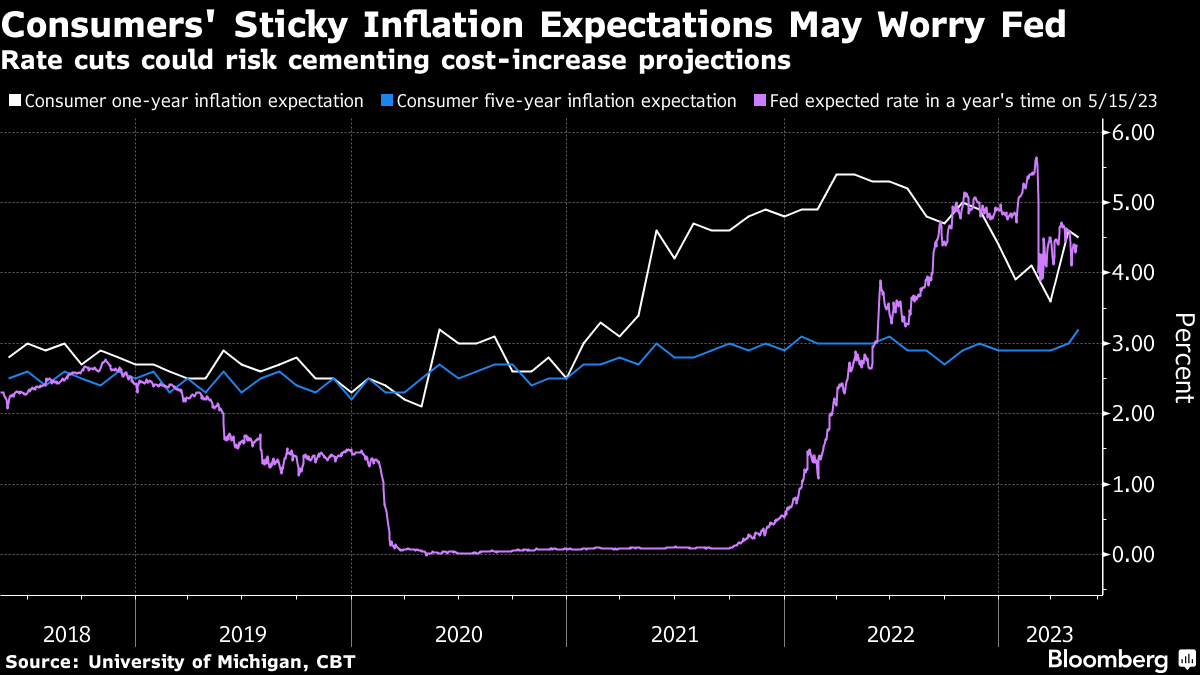

ZH: UMich Inflation Expectations Haven't Been Higher Since 2008; Headline Sentiment Slumped In May

After last month's massive jump in 12-month inflation expectations, analysts are hoping the this morning's preliminary May data from UMich's consumer sentiment survey shows some pullback in that fear. While inflation expectations for the next year dipped very modestly, expectations for the next 5-10 years jumped to +3.2% - it hasn't been higher since 2008 (tied for its highest since 2011)...

… here is a snapshot OF USTs as of 706a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower and the belly is leading to the downside after the Eu commission upped their growth and inflation forecasts (link above). DXY is modestly lower (-0.1%) while front WTI futures are modestly higher (+0.25%). Asian stocks were mostly higher, EU and UK share markets are modestly higher (SX5E +0.3%) while ES futures are showing +0.4% here at 6:40am. Our overnight US rates flows saw a leak lower in Treasuries during the Asian session with no flow themes a standout amid the parallel shift to weaker prices. Overnight Treasury volume through 6:45am was ~80% of average overall with 5yrs (138%) seeing some relatively elevated average turnover to start the week…

… the Treasury 2s5s10s 'fly appears to be respecting its range support (around -60bp) derived by January's low print in the time series-- looking locally 'oversold' now which is a hint that the tactical crowd in the belly may be a little excessive at the moment.

… and for some MORE of the news you can use » IGMs Press Picks for today (15 MAY) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ … Given I have been outta pocket past few days, I’ve not yet READ through and given what follows,the necessary ‘once over’, so please forgive me if I miss the messages.

That disclaimer in mind, a few things which stood OUT …

BMO note on week ahead, “Anything but Average” » looking at 2s10s for a steepener, details within BNPs Sunday TEA: Short stories KEY MESSAGES

We expect the US debt ceiling to become an increasingly important theme for markets, and see asymmetric upside risk to the USD vs. high beta and FX vol into the debt ceiling.

Choppy but ultimately range-bound markets have created a challenging backdrop for global macro investors.

We see pockets of opportunity in idiosyncratic stories in the UK, Norway and EM.

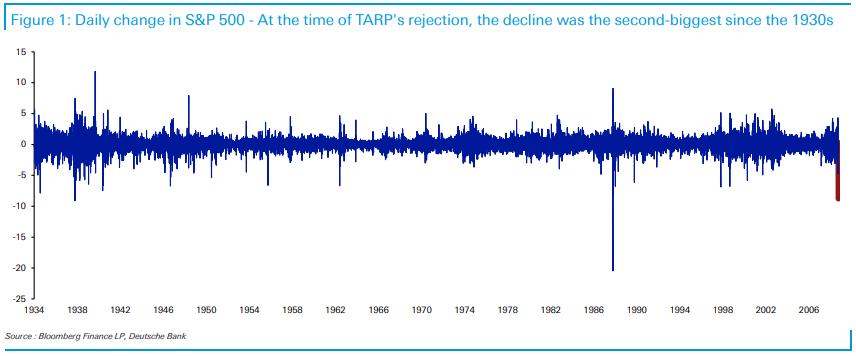

Brean’s econ weekly, “Slowly Subsiding Inflation Shows the Fed’s Job is Not Done” DB effort to MAP mkts in the week ahead, “How market turmoil can lead to policy reversals” NOTING, “….on Monday September 29, the House of Representatives rejected the bailout by a 228-205 margin. This triggered chaos in markets, and the S&P 500 saw its biggest decline since Black Monday 1987, with a single-day loss of -8.79%. Looking even further back, it was the second-biggest decline since the 1930s (Figure 1).”

GS: UMichigan Sentiment Falls and Long-Term Inflation Expectations Rise in Preliminary May Report

MS on global macro (and rates), “It's All Happening … We maintain UST 2s30s steepeners, 5s30s steepeners, and long 5y UST outright…” MSs weekly stock jockey report, “Thoughts from the Road”

MSs weekly WORLD(econO)view, “Breaking Into Pieces … We consider growth and inflation implications of a structural disentanglement of global supply chains.”

AND there’s more sitting and waiting to be discovered in the ‘global wall st inbox’ but for now … well … you get what you pay for!! Sorry

…While debt-ceiling drama and bank sector woes have taken up much of the focus across markets, Friday’s US consumer survey results from the University of Michigan may matter more than either of those themes. The burst of optimism that the Federal Reserve’s hiking cycle has reached its peak looks premature after Americans’ five-year inflation expectations jumped to a 12-year high. Chairman Jerome Powell has repeatedly insisted that avoiding a scenario where elevated projections for inflation become entrenched is a key reason for setting restrictive policy.

There are at least 19 appearances from Fed speakers scheduled before markets close for this week, culminating in Powell speaking on a policy panel alongside former chairman Ben Bernanke. With traders still betting on a rapid pivot toward easing policy and at least two rate cuts this year, bonds and equities look vulnerable should those bets unwind. That could come from any straight expressions of alarm about inflation, as well as the potential that policymakers push back once more against the idea that banking turmoil requires them to put away the interest-rate tool.

In as far as how the more things change, the more they stay the same, DataTREK on FedFunds,

… Topic #3: How the odds for Fed Funds rate cuts later this year have changed over the last week. We have annotated the CME FedWatch Tool chart below with the change in odds for various December 2023 rate scenarios over the last 7 days. Also noted is the current Fed Funds rate of 5.00 – 5.25 percent.

Two points on this data:

While Fed Funds Futures still expect three 25 basis point rate cuts this year, the odds of 4 such cuts fell materially last week (from 23 to 15 percent).

The odds of just 2 rate cuts increased by an almost equivalent amount, to 32 percent from 24 percent.

Takeaway: Even with last week’s tweaks to the Fed Funds probability data, this market remains entirely convinced the Fed will reduce interest rates this year.

For MORE, feel free to economically workbench all the data via CME FedWatch Tool and while I may have begun the mornings catchup note with a look at BONDS, here is a couple looks at 2yy via Raoul PaL (and his STACK),

… To conclude: inflation is yesterday’s news, and the bond market is starting to pick up on this. We also think that all the noise around the debt ceiling accelerates the move lower in bond yields. In fact, 2-Year Bond Yields are trading much as they did in the early 2000s, where the final move higher in yields was the ultimate bull trap just before the BIG move lower – we think it plays out similarly this time around...

... and literally no one is prepared for this – positioning in 2-year USTs is the shortest since May 2007...

The key takeaway? The pain trade in bond yields is clearly lower from here, not higher…

In as far as the GOLDILOCKS updated global views - climbing a wall of worry - here’s what they DIDN’T share in the note,

An oldy but a goody — sorry NOT sorry!!

AND what a weekend!! I’m still letting it all sink in — one down and 2 ‘things’ to go! That’s all I can say ‘bout that for now and so … THAT is all for now. Off to the day job…

No "climate change" within that Wall o' Worry....Beautiful!