The link above offers a few (3)TLINES that author believes will matter in Q2 … We’ll only know in the fullness of time and these are some levels to watch, to be sure. I’ll attempt to help flesh some of them out over the weekend.

I’ll ALSO attempt to keep current it is not ALL who see rates going from here up TO ‘the moon’. Just the other day, 1stBOS noted 10yy look ‘increasingly close to a peak’.

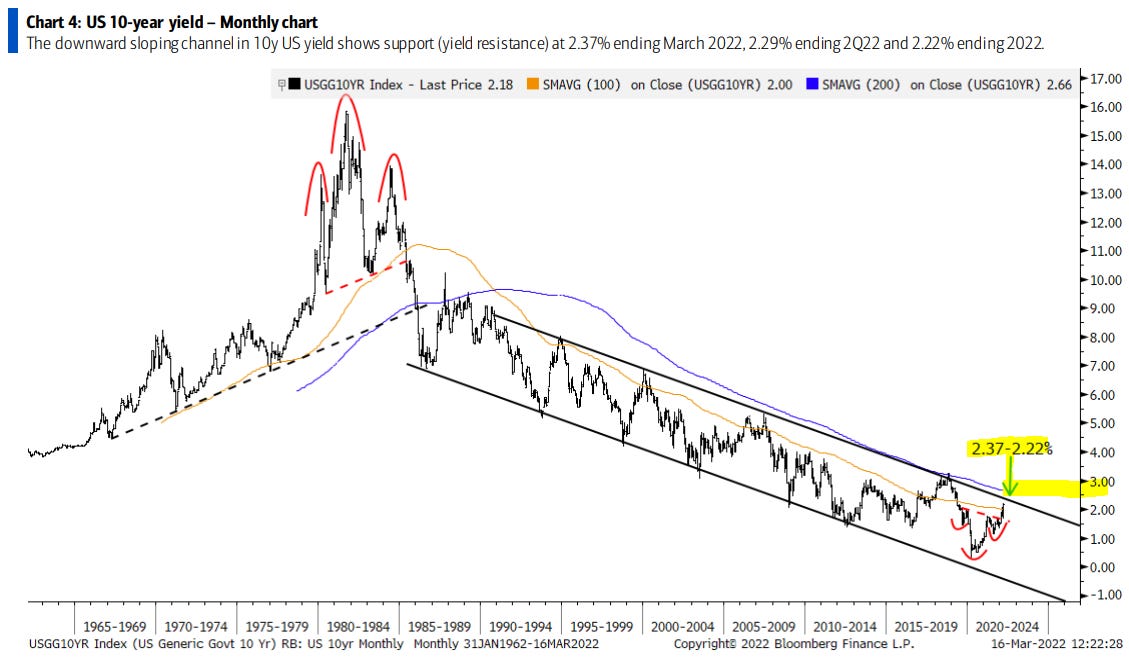

Keeping this MONTHLY them alive and well and looking further out the curve, from Twitter (so it must be true)

@AndrewThrasher Long-term look at the 30-year Treasury yield and how well the 100-month moving average has defined the over 3-decade trend.

It is now 4pm (which is the new 3pm from an index marking point of view) and that may / may NOT be significant now but back in the day, when the change was made (January 2021 and was even MORE prescient after a terrible 7yr auction in Feb followed by monster BID into month-end), HEREfor how it was noted then when I was in a different seat — daily 2pg note for Jan 26 2021 where you’d click through to what was on MY MIND and have seen this:

The RBC note (linked) reminds,

… The majority of Fixed Income AUM (>60%) continues to be in non-passive mandates which may be “index huggers” but aren’t mechanically required to shift to 4pm to reduce tracking error . The gradual shift to fixed income factor investing, alt-beta type strategies may eventually push more trading in that direction, however that isn’t a day 1 concern…

OR perhaps we should just get back to our curve obsession which could not be detailed better by this visual (h/t @fullcarry),

Food for thought and THAT is all for now — until it is we learn whatever it is happened overnight, while we slept … back TO the day job…