Given the flurry of central planning news and DOTS SHOCKS still rippling through global markets AND with GILTS BID impacting USTs here / now (I’m told), I thought I’d leave the day-to-day of markets to the pros.

I DID want to pass along something of a longer-term visual and thought from a large German bank from a stratEgerist who wins the EZ Inst Inv popularity contest year in and out. The following is to be the last CoTD for 2021 and a good one, indeed …

Interesting visual and one that speaks a thousand words, in and of itself. Here are another 240 to help make the point

It seems fitting that we end the year looking at inflation and bonds. Today's first chart looks at the real return of our 10yr US Treasury series by year over the last century. Since the start of 2021, 10 year Treasuries have “only” risen by around 55bps so far but the real return will likely be around -10% assuming things stay broadly stable into year-end. If we end worse than -10.2% it will be the 6th worst year in 100 years. The three weakest years have been 1946 (-17.8%), 1980 (-13.6%) and 2009 (-12.5%) so 2021 might not be too far away from the top three.

Talking of 1946 this started the last sustained serious period of phenomenally negative real returns in global government bonds. The second chart shows that for a selection of major government bond markets, the total real returns over the 35 years to 1980 were between -40% to -90% for the vast majority.

So massive financial repression and awful real returns. I can’t help think we’re in the early stages of a repeat of this period given the huge global debt pile. If defaults are not an option to de-lever the financial system, a long period of financial repression and negative real returns are likely in order.

So don’t buy DM government bonds as a present to your loved ones this Xmas if you want long-term returns that keep pace with inflation.

TINA. FOMO. It’s everywhere and why not?? Financial repression and negative REALZ then are a design feature NOT a flaw and **SHOULD** keep equity markets afloat?

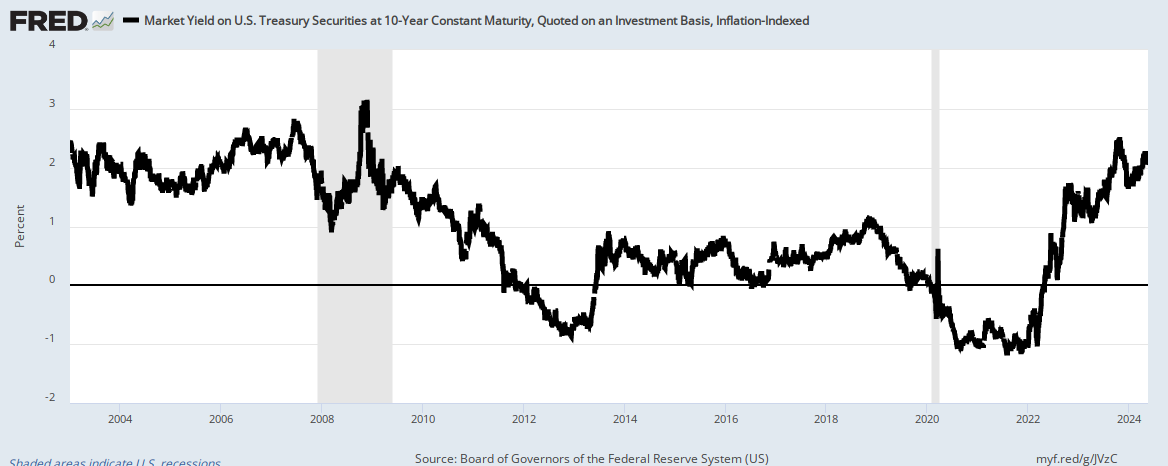

I don’t know him personally but I understand the fascination with the analysis. It’s good, thought-provoking stuff, for sure BUT … I still cannot buy into the idea bonds (10yr USTs in this case) offer NOTHING any longer, in the form of portfolio insurance. Even WITH a current (ie short-term) negative REAL (inflation adjusted) yield. Above, HERE.

I’ll be keeping all of this in mind as we enter that time of year … when friends and (former) clients are doing last minute, year-ending BOND ‘holiday shopping’ and portfolio adjusting for clients / fiduciaries in TO 2022.

Thinking along the lines of YTD performance of various asset classes and yes, the fabled stories of rebalancing of the 60/40 (now 70/30) — NOT dead yet, IMO — and while not LONG term considerations laid out above, annual returns and the like, certainly considerations for all the cheaper / steeper and generally HIGHER rates calls we’ve all come to know, love and read about from THE Sellside.

More from them in due course AND as time / weather permits…Back to the day job!

{kind=link}