and another thing(s): 'More room to go' (BLK); Fed to remain on hold (BNP); investors buying (approaching 'the fence', ie NEUTRAL -DB); dollar down, 'flation UP

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends (additional) note…

Still undetermined IF I’ll be spamming the interwebs with anything tomorrow morning, Monday but I’m leaning on taking the day, sparing you all and so I wanted to chime in ahead of this weeks upcoming duration supply on offer — $58bb 3s, $38bb 10s and $22bb Bonds … in addition TO (bullish) weekly 30yr yields, some levels to watch Monday …

3yy DAILY: dipORtunity at / just above 4.00% (TLINE) …

… as momentum moving from (rate CUT optimism)overBOUGHT to now, nearly overSOLD …

10yy DAILY: just north 4.40 (TLINE) might be similar dipORtunity …

… with similar momentum setup (ie bearishly moving from overBOUGHT to nearly overSOLD) …

30yy DAILY: 5.00 on the radar screen as a ‘dipORtunity’ …

… as momentum adjusts and here my only hesitations are with regards to how the longer end of the curve TRADES the OBBBA …

… on on that last ‘fear’, a few words and a view …

“Big Beautiful Bill” (hashtag#BBB) could boost hashtag#equity sentiment and push up term premium - still low to historical comparables (chart) - through worsening hashtag#deficit. Congressional Budget Office puts it at an additional, front-loaded, $3.25T in borrowing over 2025-34. I continue to favour US equities over long Treasuries.

… that said, couple other links as weekend comes to a close and just ahead of futures opening, which one may want to consider …

Friday, Jul 04, 2025 - 05:40 PM ZH: Trump Sends Tariff Letters Threatening Up To 70% Levies, Sparking Fears Of Delayed Trade Deals

Updated on July 6, 2025 at 5:09 PM UTC Bloomberg: Nations Chase US Trade Deals as Bessent Hints at Longer Deadline

Moving on TO a few things I’ve stumbled upon since hitting send …

Breakfast with … a large French bank who’s tennis tournament is OVER (and so too are Feds rate CUT chances) but …

We continue to see the Fed staying on hold this year. Strong US labour data and a declining unemployment rate suggest revisions to FOMC forecasts, particularly for rate cuts during 2025. We still like 2s10s flatteners on the US curve.

Rising FX hedge ratios remain the key driver for the USD’s direction. We see falling FX-equity correlations leading to higher hedging needs, and we stay short USD.

With only a few days left until the 9 July tariff deadline, we expect initial framework agreements and/or extension of deadlines to continue negotiations. But early signs suggest potential nonlinear risks for markets with relatively little risk premium priced in.

Unchanged Fed in 2025: Last week’s US June NFP data surpassed market expectations, indicating the labour market's underlying resilience. Notably, the unemployment rate is key. Its drop from 4.2% to 4.1% reflected a lower participation rate. This likely stemmed in part from the impact of immigration policies, resulting in a lower breakeven level for monthly NFP numbers compared to the past. Consequently, the FOMC’s 4.5% median unemployment rate dot could decrease during H2 2025, potentially prompting committee members to revise their outlook for rate cuts. This aligns with our forecast of no Fed easing this year, even if at least two dissents are likely in the future meetings with policy on hold (see US Fed: All this happened before, and will happen again, dated 3 July). For more on the US employment report and our take on the passage of the US tax-cut bill, see US: One Big Beautiful Note, dated 3 July …

Investors positioning — buying BUT ONLY approaching the FENCE …

04 July 2025 DB: Investor Positioning and Flows - Just Approaching Neutral

Last week we had noted that equity positioning had been rising but was still underweight even as the market hit new highs. This week, positioning has continued to rise and is approaching neutral but is still a little shy of it (-0.14sd, 35th percentile). Discretionary investors have turned slightly overweight (0.04sd, 46th percentile) while systematic strategies remain a little underweight (-0.14sd, 35th percentile). Equity funds ($2.2bn) saw inflows this week but at a modest pace as robust inflows into global ($6.1bn) and broad-EM ($2.4b) funds were offset by outflows from China (-$3.7bn), US (-$1.9bn) and Japan (-$2.8bn) funds. Europe saw modest inflows ($0.6bn). Across sector-dedicated funds, there were notable inflows into Financials ($1.6bn), Industrials ($1.3bn) and Tech ($1.2bn). Inflows to bond funds ($20.bn) picked up to the highest in 6 weeks, with strength in most categories outside of government bond funds. The trend of booming buyback announcements has continued, with banks adding to the tally following favorable Fed stress test results.

A few thoughts on the soap opera that has become the tariff regime in DC …

July 6, 2025 MS IDEA: Sunday Start | What's Next in Global Macro: As the Tariffs Turn

…And this Wednesday, the 90-day pause on reciprocal tariffs – initiated on April 9 – expires. Our base case? Effective US tariff levels rise only modestly, but with some new noise. While many US trading partners could see a deadline extension for further negotiation, this may not be a uniform approach. The administration could relax some tariff levels given sufficient progress in bilateral talks, or conversely communicate that tariff increases are coming on other trading partners (per the president’s own comments earlier this week and the recently announced arrangement with Vietnam).

But it’s worth considering what happens if things don’t go according to plan. There’s been little publicly reported concrete progress on trade deals. There have also been some hawkish signals from the administration – consider that it has floated the idea of a tiered system for global trade partners, similar to the messaging we saw ahead of the April 2 'Liberation Day' announcements. And as our colleague Rajeev Sibal points out in recent work, we’re likely not yet seeing concrete effects of tariffs on inflation that could influence policymakers’ decision-making. And importantly for markets, consensus among the investors and companies we’ve been in dialogue with is clearly that further escalation is not in the cards. Said more simply, it’s prudent to consider multiple scenarios. ..

…given the variability of outcomes, tariffs are still a critical variable to our outlook. A more aggressive tariff path would reinforce our economists’ view that risks to the outlook are skewed to the downside. This is reflected in their forecast for ~1% 4Q/4Q GDP growth in 2025/2026 – not quite recessionary, but softer versus last year. This in turn reinforces a number of our key asset class outlooks, notably our preference for US Treasuries and short USD positions. Tariff relief, conversely, would cut against these key views.

Bottom line – tariffs are still a critical variable in the outlook for markets…so July 9 remains a critical date.

Steepener and / OR a flattener? Which is right? Which will win? Depends …

4 Jul 2025 NatWEST: US Weekly Economic and Strategy Brief

…Employment Report:

June fireworks: Nonfarm payrolls rose by 147,000, more than expected.

Government jobs added 73,000 jobs, led by state (40,000) and local (23,000) education jobs. Federal jobs fell 7,000.

Private payrolls slowed to 74,000, with cooling vs recent trends (notably healthcare).

Unemployment fell 0.127 pts to 4.1% (4.117% vs. 4.244% unrounded)

The latest jobs report should not alter the near-term policy outlook

Is bank balance sheet expansion a steepener or flattener?: We illustrate that general bank balance sheet growth and growth in the portfolio weight of Treasuries as a percentage of bank credit have opposite effects on the term premium.

The Treasury portfolio weight (Treasuries as percentage of bank credit) is positively related to the term premium. This squares with intuition that bank holdings of Treasuries are more heavily concentrated in the front end.

The total system balance sheet – bank credit – is negatively related to the term premium.

This is important because the proposed changes to SLR would, according to Fed Governor Barr, reduce bank capital system wide by $210 billion. If deployed at 4x leverage, balance sheet growth of $1 trillion would flatten the term premium by approximately 40 bp, in our view.

France weighing in and cautiously so …

03 July 2025 SocGEN: Fixed Income Weekly Cautious optimism

Risky assets have extended their run, while the US labour market has bucked the recent trend of downward surprises in economic data. As we approach the key 9 July tariff deadline, the markets seem somewhat more optimistic of a relatively benign outcome from the trade negotiations, certainly compared to the weeks following ‘Liberation Day’. However, we have learnt that one of Trump’s key negotiation tactics is his unpredictability. This delicate balance creates asymmetries in the likely market reaction from bonds this week…

…United States Looking good Passage of the One Big Beautiful Bill appears imminent. The resulting increase in the debt ceiling will likely be followed by around $500bn in net T-bill issuance before the end of September. The surge in supply could weigh on bill valuations vs SOFR and push repo rates higher. June’s non-farm payrolls exceeded expectations, allaying worries about the health of the labour market. A cut at the July FOMC meeting looks increasingly unlikely.

Recommendations Trade the range over the next quarter. A move in yields towards the high end of the recent range is a buying opportunity, in our view.

Over the longer term, we expect the 2s10s and 5s30s curves to steepen modestly.

Stay long front-end and intermediate swap spreads.

Swiss on NFP …

3 July 2025 UBS: US Economic Data Labor market slowing

…As we noted in our preview, we thought an employment increase near ours, in which we placed more emphasis on private over government, was probably good enough to keep the FOMC comfortable with waiting a little longer than July, and consistent with our expectation for the next rate cut at the September FOMC meeting…

… and on the <economic> week ahead …

3 July 2025 UBS: US Economics Weekly A big bill and big increase in tariffs

Economic Comment: One Big Beautiful Bill Act moving along We updated our estimates of the support to growth from fiscal policy under the assumption the Senate passed reconciliation bill is close to the final form of the bill, and that it gets passed into law. Compared to our prior assumptions, there is more near-term deficit widening and then more deficit narrowing in 2027. This led us to shift around the expected support to growth. Overall, the increments, on the base of a $30-plus trillion economy, were not far off our prior assumptions. Compared to our economic outlook last week, we added a tenth to real GDP growth in 2026 and removed a tenth from 2027. That masks a few other smaller adjustments, such as nudging down our Q2 tracking from 2.8% to 2.5% due to incoming data. Overall, we expect the OBBBA to support growth, but fall short of the boomy expectations that followed the Presidential election…

July 9 is only days away: more duties, deals or delay? As July 9 approaches little clarity has emerged on what will happen to the higher tariffs that are set to snap back into place for a number of US trading partners, including substantial trading partners like the European Union. Will the administration postpone them? Will some snap back into place? Will new rates be proposed? The outlook is highly uncertain despite being potentially consequential…

The Week Ahead: July 9 and FOMC minutes There is a great deal of uncertainty over how the administration will adjust tariffs at the July 9 deadline. We discuss this on page 6. The minutes of the June FOMC meeting will be published Wednesday. Participants likely discussed tariffs, and highlighted the uncertainty. The FOMC appeared divided but the voting members seemed tilted toward raising their inflation projections and still lowering rates 50 bps this year. Also, Vice Chair Bowman and Governor Waller put a July rate hike on the table soon after, citing concerns over the labor market. The Fedspeak calendar looks light so far and the data calendar will be light too. Small business confidence is expected to have improved further in June and is consumer credit growth to post a modest gain in May. Volatility in initial claims the week of the July 4 holiday is a risk…

The fireworks started early in the stock market last week. On Thursday, the day before Independence Day, both the S&P 500 and the Nasdaq rose to new record highs (chart). In addition, their 50-day moving averages rose above their 200-day moving averages. Those "golden crosses" tend to be bullish breakout patterns, indicating the possibility of a long-term bull market.

The unprecedentedly fast rebound in the stock market since April 8 is attributable to less uncertainty. The S&P 500 volatility index (VIX) peaked at 52.3 on April 8 (chart). On Thursday, it was back down to 17.5, below its average over time of 19.5. We wouldn’t be surprised to see it fall to 10.0 over the rest of the summer. That's because the rapidly rising uncertainties on a number of fronts that caused the stock market correction from February 19 through April 8 have been rapidly abating since then.

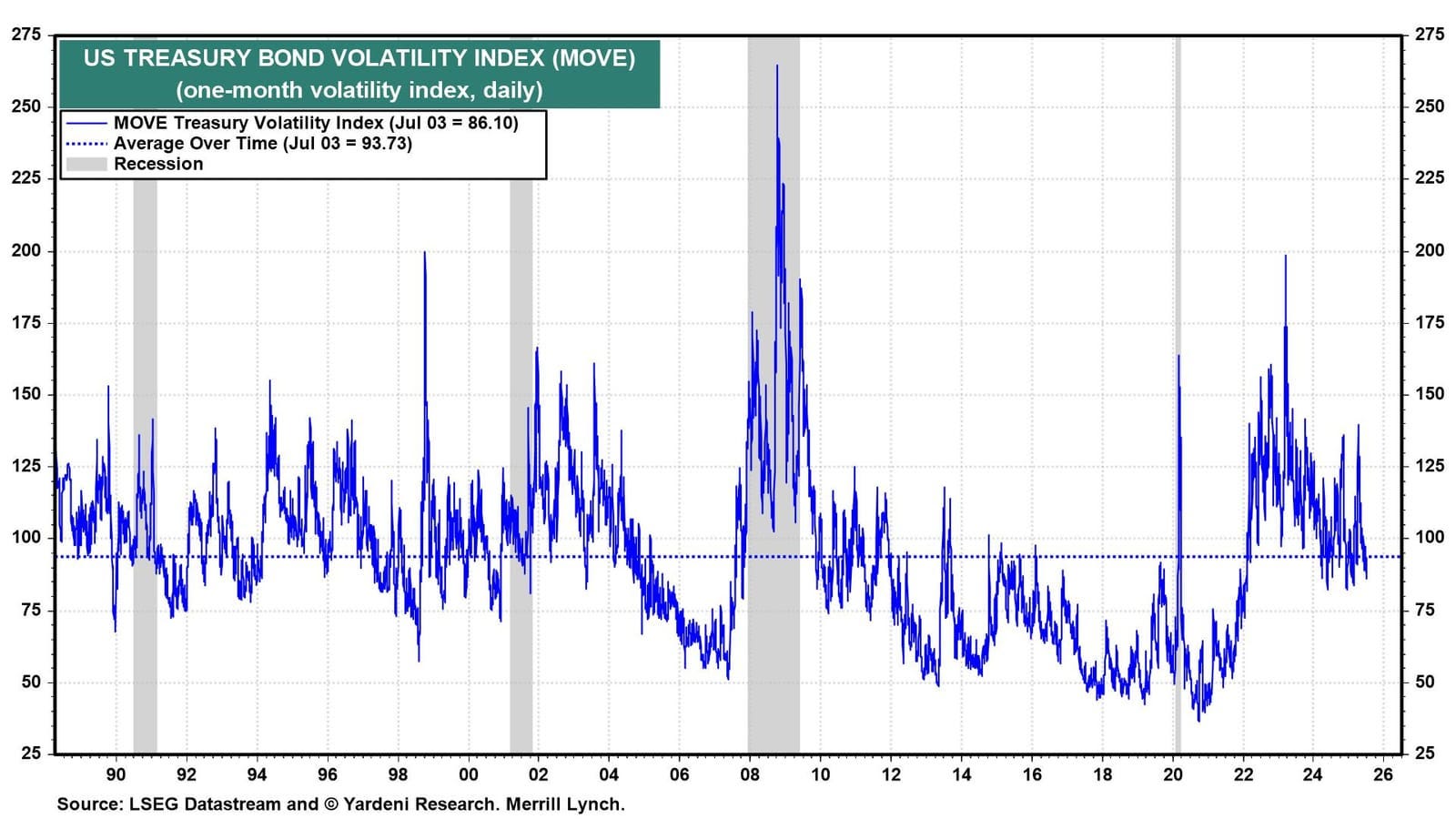

The US Treasury bond volatility index has dropped sharply as well, from 139.9 on April 8 to 86.10 on July 3 (chart).

Let's review the main sources of uncertainties so far this year and why they’ve dissipated:

(1) Tariffs. Stock prices soared on April 9 when President Donald Trump postponed the reciprocal tariffs he intended to impose on America's trading partners. The markets rightly concluded that these tariffs would be negotiable.

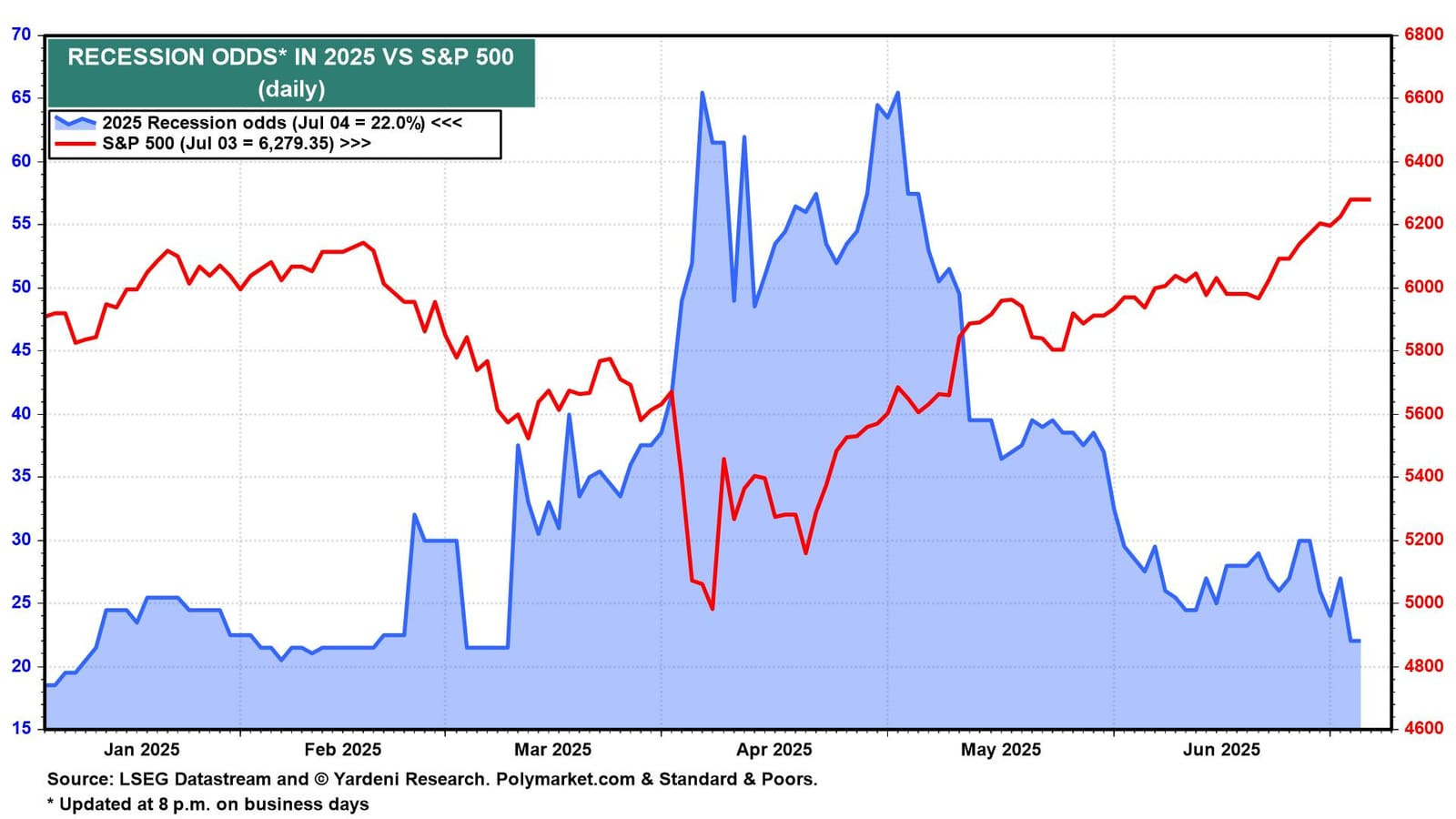

(2) Economy. The tariff issue hasn't gone away, but it hasn't weighed on economic growth or boosted inflation as was widely feared. According to Polymarket.com, the odds of a recession have declined from 65.5% on May 2 to 22.0% currently (chart).

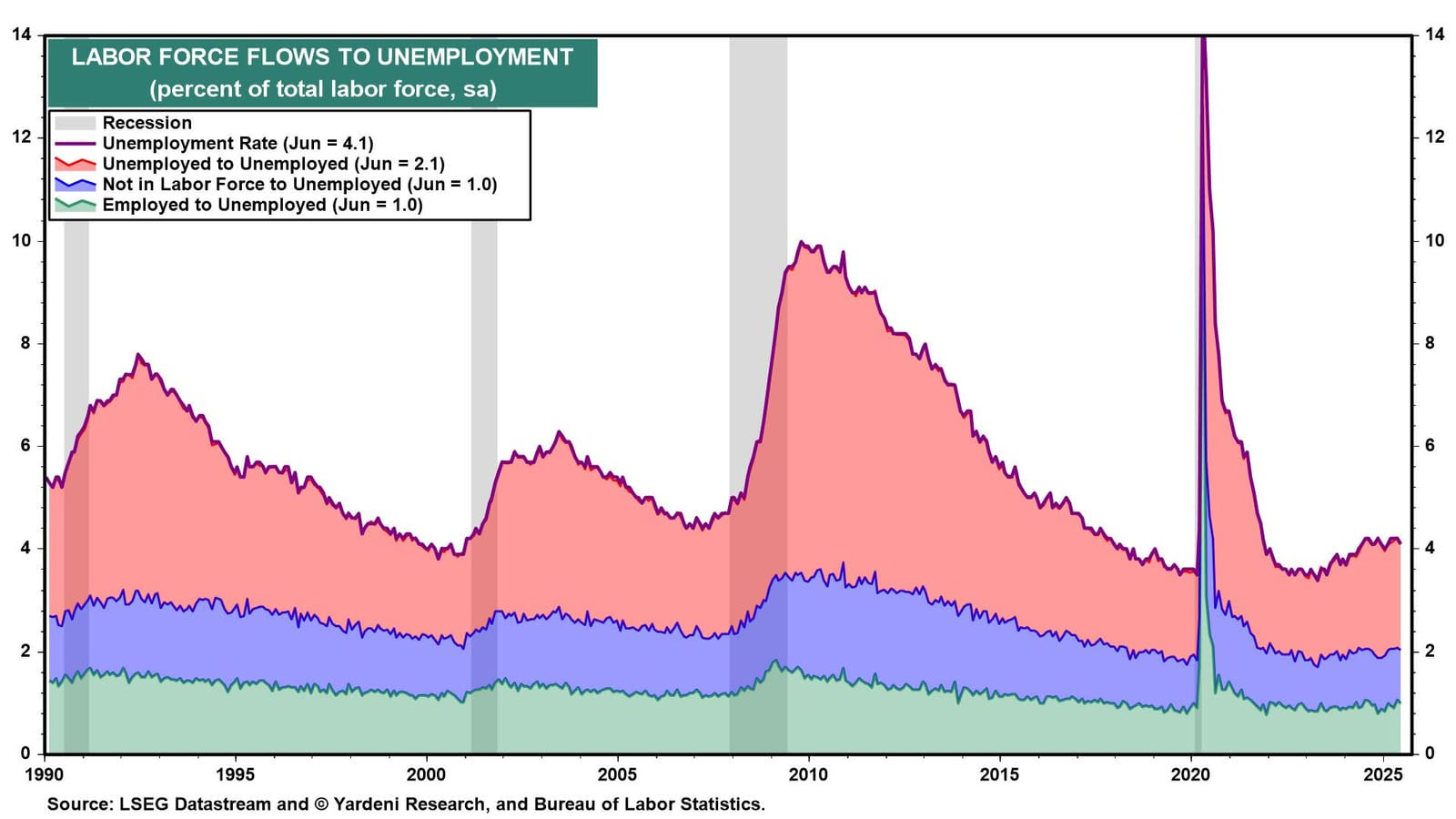

Thursday's reports for weekly unemployment claims and June's employment confirmed the resilience of the labor market. Payroll employment rose solidly by 147,000. The unemployment rate edged down from 4.2% to 4.1% because of a drop in the unemployment rate for those who were unemployed in May (chart). This implies that it isn't getting harder to find a job as rising continuing unemployment claims would suggest.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

‘bout that there decline in the USD so widely advertised …

July 6, 2025 Apollo: The 10% Depreciation in the Dollar Will Boost Inflation by 0.3 Percentage Points

There is already upward pressure on inflation from tariffs, oil prices, and immigration restrictions, and the chart below shows the impact on inflation of a 10% and a 20% depreciation in the dollar. The bottom line is that we should see inflation move higher over the coming months; that is what the consensus expects, what the Fed expects, and what we expect.

… and a couple from The Terminal …

July 5, 2025 at 9:00 AM UTC Bloomberg: Charting the Global Economy: US Jobs Data Eases Pressure on Fed

July 5, 2025 at 10:00 AM UTC Bloomberg: Ghost Factories Are a Warning Sign for Green Manufacturing’s Future Rollbacks of clean-energy credits in Trump’s tax bill add to the sector’s challenges as project cancellations rise.

… THAT is all for now … enjoy whats left of the weekend and I’ll be over here with Thing 3 as he learns to drive, having now completed his 6hrs with the driving school, like …