Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends SECOND (outta character) note…This, I promise you, will NOT take long.

I’m cleaning up ‘the inbox’ and continuing to read through some of the funTERtainment out there on Global Wall and theme continues to read as a modestly more bullish (rates) one.

For better (inflation reaching target for all right reasons) or worse (more uncertainty leading to less desirable economic outcomes), most seem to have similar bets …

This is what brings me in (along with there being grapefruit league baseball, some college hoops and weather still bit too chilly to be out playing little bit of ‘wheat hockey’ — Bay Hill final round up soon!

So it’s on THAT note …

…AND ANOTHER THING … here’s some MORE of what Global Wall St is sayin’ …

Moving of longs out the curve so, in a way, bookin’ profits and getting / stayin longer’er …

In the US, markets are still understating the risk that well below trend growth will require a Fed response, even if lagged. We recommend moving longs from 2y to 5y USTs. In Europe, Germany's fiscal regime shift made headlines this week. In Japan, investor trends around FY turn are in focus.

… Move longs from 2s to 5s: Spillover from Europe should be limited We have been recommending positioning for slowing growth via being long 2y USTs (entry: 4.31%, exit 4.0%). In light of the market having priced almost 70bp cuts this year but very little further out, we are exiting this position and instead recommend going long 5y USTs (entry 4.10%).

Figure 9 shows that the markets are pricing in a trough of about a 3.6% policy rate and Figure 10 shows that corresponds to about 70bp in cuts this year and 10bp next year. We believe the terminal rate looks high in light of the above developments. Figure 11 show that the markets are pricing in inflation to revert to about 2% in 1yf space; still, Figure 12 shows that the real rates are priced to average 1.7%. If the economy grows below trend over the next two years, labor markets will become cooler and with inflation at target, the Fed is more likely eventually to undershoot neutral than stay above it…

… this next shop expressing a similar bias but far less direct and willing to commit — and I can relate. I’ve got a fear of commitment — mostly to the WRONG idea …

…Rates: US exceptionalism fades, US rates outperform US: Hold soft long rate bias or at worst be neutral benchmark given US growth risks. We still like nominal 5s30s steepeners & conditional bullish front & belly trades…

…Stagflation calculation: hard for Fed to pivot dovish A key client question over recent weeks has been: “how does Fed respond to stagflation risks”. We have long believed stagflation shifts Fed focus to inflation expectations. Recent Fed comments agree, especially from St. Louis Fed Pres Musalem. The Fed broadly judges that inflation expectations are well anchored but there has been an uptick in some measures such as U Mich, Conference Board, ISM prices paid, etc.

If inflation expectation measures continue to rise, it limits the Fed’s ability to turn dovish when facing stagflation. The Fed will not be as easily able to look through higher inflation & focus on growth. A Fed that does not appear sufficiently responsive to shifting downside growth risks will create a more challenging market for risk assets. We see echoes of sharp equity drop post Dec ’18 FOMC meeting in market set up today.

If downside risks continue to build today & the Fed is unable pivot away from inflation, we worry about further headwinds for risk assets. Headwinds for risk assets are likely to mean lower rates & a further front loading of Fed cuts. Clients willing to position for this might consider outright SOFR Z5 or J5Z5 flatteners (see Closing SOFR M5Z6 flattener).

…Duration guidance today: at worst be neutral We believe clients should at worst be neutral their benchmark. We believe this is a hard market to be short & continue to believe clients should lean slightly long. Our core logic = (1) soft data may propagate to hard data & support lower yields, (2) negative feedback between risk assets & bond yields could increase, especially if insufficiently dovish Fed.

Our models currently suggest fair value for 10Y is 4.15-4.4% (see Monthly rates models). Slowing data + elevated economic uncertainty = recoupling of 10yT yields to fundamentals. Market biased towards interpreting fading macro data more as noise rather than signal. Vol dynamic seems to corroborate this view. We continue to see asymmetric risks and favor holding conditional bullish structures in the belly and front end. For more detail see US vol.

Bottom line: we continue to recommend clients trade duration with a soft long duration bias or at worst be neutral given downside US growth risks & elevated economic policy uncertainty. We continue to like 5s30s nominal steepeners & positioning for a further front loading of Fed cuts if hard data starts to turn. We continue to see asymmetric risks and favor holding conditional bullish structures in the belly and front end.

…Technicals: Raise stop on US 5s30s steepener In Nov-2024 we recommended a medium-term US 5s30s steepener entering at 30bp, targeting 60 and 85bps. 5s30s has reached 55bps. We raise our stop to 35bps.

In November 2024 we recommended a medium-term US 5s30s steepener trade entering at 30bps while targeting 60bps and 85bps. This week 5s30s reached 55bps. We raised our stop to 35bps and remain convicted while it's above the rising trend line and 200- day SMA. Please see this report for more detail: Chart alpha: Raise stop on US 5s30s steepener 06 March 2025.

Eurozone’s fiscal reforms mark a watershed moment and with that a structural shift for European assets.

The market has failed to react much to new US tariffs being implemented, but we see scope for this to change the longer tariffs stay in effect. This implies MXN, CAD and CNH weakness, lower US real yields, higher US inflation expectations and a flatter UST curve.

We think the US payrolls report validates the ‘on hold’ stance from Fed officials as they assess the trade-off between upside risks to inflation and a possible activity slowdown.

… The household survey was a soft spot. Employment on this measure fell 588k, though volatility is typical in these numbers. The unemployment rate rose 0.1pp (4.1% versus 4.0% prior), a move that would have been larger had the participation rate remained steady. In a big picture sense, though, the current level of the jobless rate is still below the Fed’s estimate of longer-run neutral (see below), while inflation has not yet converged to 2% (see US February jobs report: Good enough, dated 7 March).

Here’s another Sunday morning offering …

MS: Sunday Start | What's Next in Global Macro: Credit's Low-Beta Opportunity

…From a credit perspective, we would highlight that our economists are not calling for a recession. Their growth expectations still leave us in territory that we would deem credit friendly, although edging towards the bottom of our comfort zone. Cooling growth may also temper animal spirits and continue to constrain corporate debt supply, keeping market technicals supportive as they have been in the last few months. Fund flows into credit have been very strong, and while Treasury yields have rallied, overall yields are still at levels that sustain demand from yield-motivated buyers.

That said, if growth concerns intensify from these levels, with weakness in 'soft' data spreading notably to 'hard' data, the probability of markets assigning above-average recession probabilities rises. This could challenge credit’s low beta, and credit beta could increase on further drawdowns in risk assets.

That credit spreads have not budged much provides an opportunity to position for the risk of incremental deterioration in incoming data through liquid credit hedges. As Vishwas Patkar, our head of US credit strategy, highlights, hedging remains quite cheap, especially via credit derivatives and macro products. He notes that CDX spreads screen very tight relative to cash and equity volatility and recommends CDX hedges, both in index shorts and out-of-the-money puts.

… then there’s this one — missed earlier in the week just passed BUT from one other of the popular kids on Global Wall … Albert Edwards … written before NFP hit …

SocGEN: Global Strategy Weekly | 6 March 2025 Still thinking the unthinkable

In my working lifetime, many economic dogmas have come and gone. Things that had been unambiguously true to any right-thinking market practitioner suddenly were no longer true. And institutions that acted as enforcers of firmly held ideologies rose in stature, but then, as the world changed, they lost their power and credibility. But up to the point when such ideas were eventually discredited, woe betide anyone in the markets that dare speak out against the overwhelming consensus – they would have been pilloried or even worse, simply ignored.

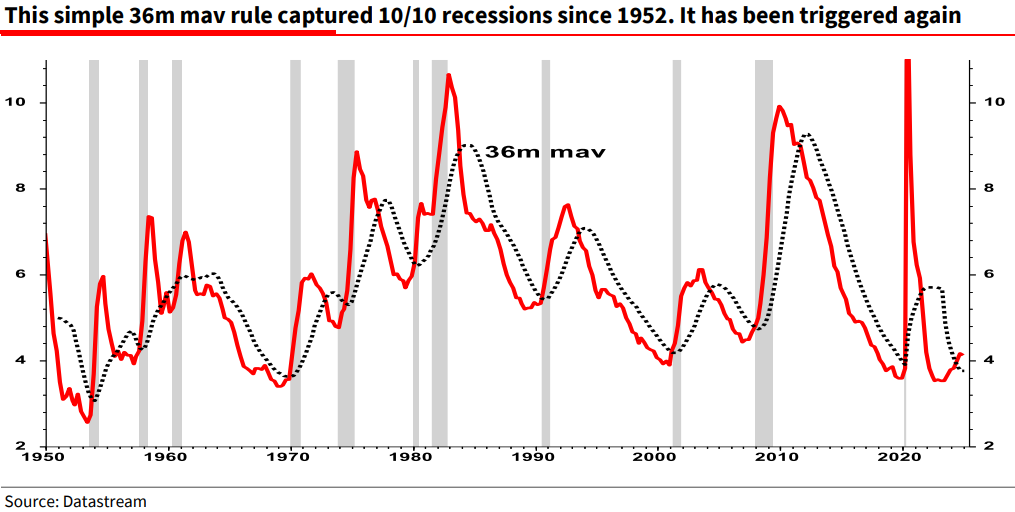

… Despite all the debate and analysis of whether that long awaited recession is finally coming, one simple rule convinces me – namely without exception when the monthly US unemployment rate rises above the (still declining) 3 year moving average, a recession is never very far away.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

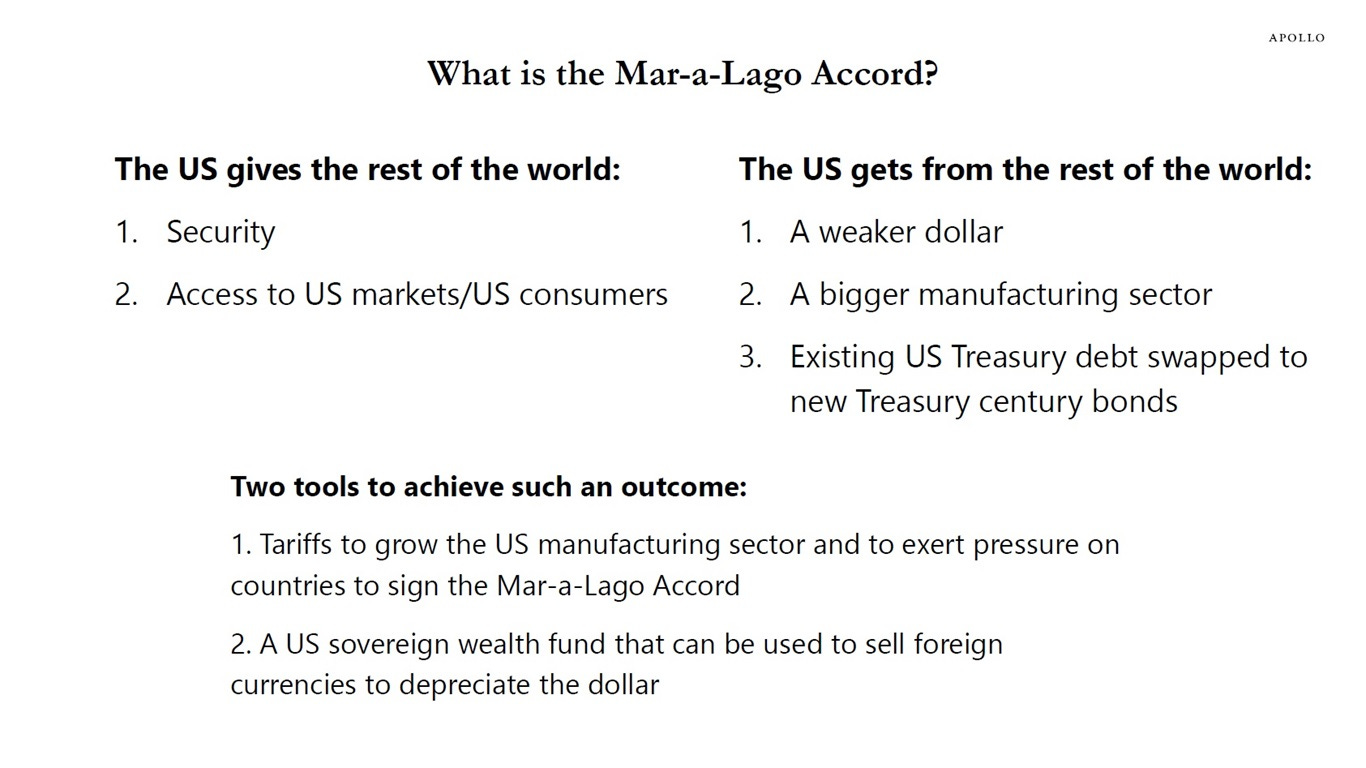

Lots of folks talkin’ bout it — Mar-a-Lago Accord as if they were there, in the room and so, here’s a note from Slok on what it even all is …

… In short, the idea is that the US provides the world with security, and in return, the rest of the world helps push the dollar down in order to grow the US manufacturing sector…

From Mar-a-Lago TO … the bond market Trump trade …

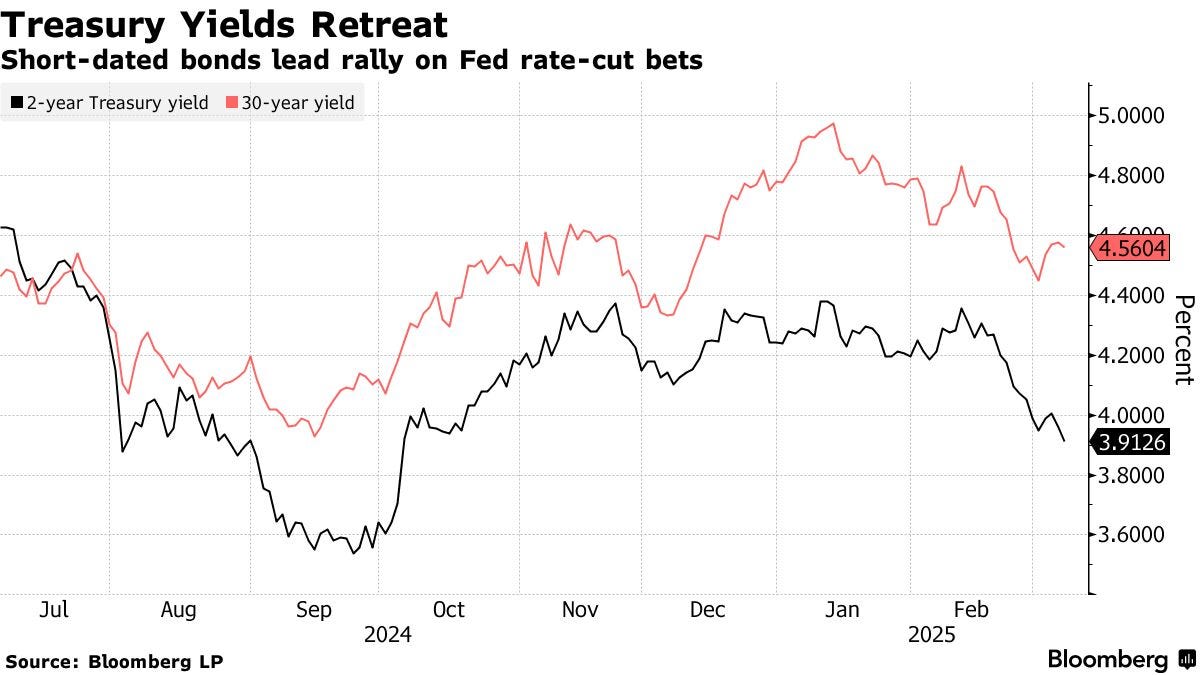

Bloomberg: The Bond Market’s Trump Trade Is Looking Like a Recession Trade

Yield curve steepens as traders see rate cuts as soon as May

US bond moves diverge from global market on slowdown concerns

Bond traders are signaling an increasing risk that the US economy will stall as President Donald Trump’s chaotic tariff rollouts and federal-workforce cuts threaten to further restrain the pace of growth…

…Since mid-February, though, Treasury yields have come down as the new administration’s policies cast significant uncertainty over the outlook. The decline has been lead by shorter-dated securities, steepening the yield curve, as typically happens when investors position for the Fed to start easing monetary policy to jumpstart growth.

A key driver has been Trump’s brewing trade war, which is likely to deliver another inflation shock and roil global supply chains. That fueled a stock-market selloff last week that continued even after he again delayed tariff hikes on Mexico and Canada. The administration’s efforts to withhold federal funding and fire tens of thousands of government workers are also taking a toll…

Uncertainty isn’t ever a good thing (unless, of course, yer long bonds …?)

TKer by Sam Ro: When uncertainty becomes unambiguously high

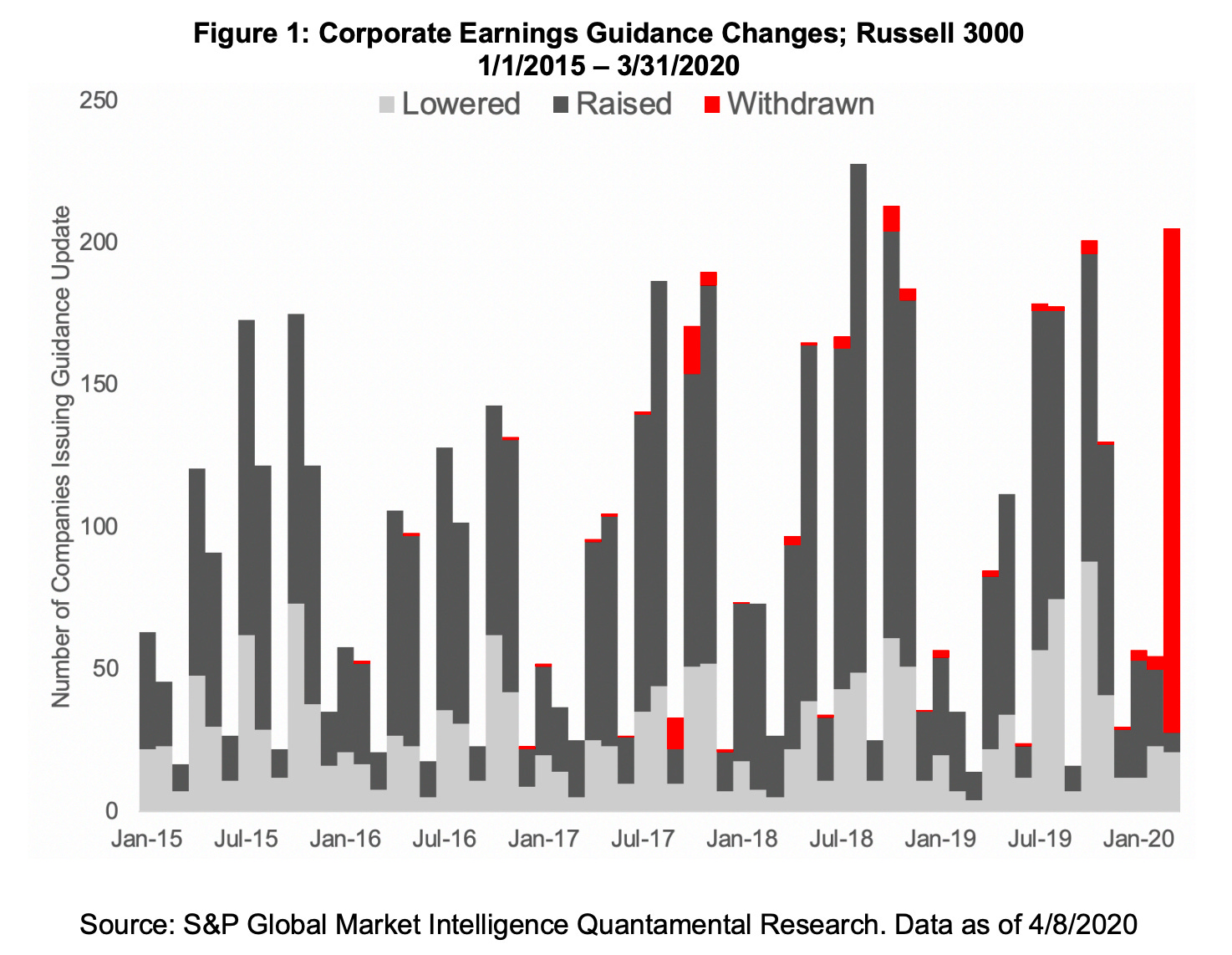

…Zooming out a bit, 173 Russell 3000 companies withdrew guidance during the first quarter, according to S&P Global. The chart below shows how unusual that was.

In Q1 2020, 173 Russell 3000 companies withdrew guidance. (Source: S&P Global)

“The question for managers is: Do they know about future performance substantially more than investors do?” NYU Professor Baruch Lev told me at the time. “My guess is that in most cases managers aren’t now better informed than investors. We are all in the dark. In that case, guidance is futile.”

It’s one thing for a company to revise guidance lower. It’s another much scarier thing for a company to admit they just don’t know where things are headed.

That’s real uncertainty.

This speaks to TKer Stock Market Truth No. 8: “The most destabilizing risks are the ones people aren’t talking about.”

Pandemic risk was effectively on no one’s radar going into 2020. Companies didn’t have plans for addressing it, and it wasn’t priced into the market. It’s why the S&P 500 was able to rally to its then record high of 3,393 on February 19 before tumbling 35% to its low of 2,191 on March 23…

… THAT is all for now. Off to the day job… Enjoy what’s left of the weekend …

good headline.....