(about avg volumes o/n) while WE slept...recession indicators benign (for now); close to a (bullish) turn (look at 10s/BUNDS); cars N crypto; the TAILOR rule

Good morning … This will be the last installment of spam for the week. My oldest is playing what is likely to be his final college football game and we’re travelling up to Boston area for the festivities. We are celebrating his achievements and coming graduation and are so thankful he’s got a job offer on the table. Now if we could add a few more tackles and a VICTORY over arch rivals of MIT (in what is defacto BRAIN BOWL), that would be nice…

This UPTREND remains firmly entrenched and in place. It’s been threatened numerous times and levels to watch are clear. Momentum (slow stochastics, bottom panel) are middling (ie sending NO clear / pressing signal)

… here is a snapshot OF USTs as of 720a:

… HERE is what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower and up from their earlier lows with the curve flattening slightly ahead of CPI and a brace of Fed speakers (see below). DXY is higher (+0.25%) while front WTI futures are lower (-0.8%), see attachment. Asian stocks were lower, following NY, EU and UK share markets are mixed while ES futures are showing +0.4% here at 6:45am. Our overnight flow color was unavailable at press time and overnight Treasury volume was about average overall with 20yrs (233%) seeing some high average turnover (off a low base, no doubt) and 3yrs (59%) seeing little.

… Our first attachment this morning offers an updated look at Treasury 2yr notes in a daily chart. The multi-month bear channel does remain in place and the still-dominant bear trendline (channel bottom) intersects at ~4.47% today- a presumed resistance for 2's if approached. That said, what intrigues us is the triple bullish divergence set-up where higher highs in yields September-October-this month have been concurrent with lower highs in momentum (lower panel) over the same period, as drawn in. This is a textbook sign that new sellers may be pushing on a string or, alternatively, that the crowd of shorts is becoming un-sustainably big. At yesterday's close, we did see a confirmed bull turn in daily momentum and it will be interesting to see if it's confirmed-confirmed at today's close. Either way, the skew of risks in 2's appear to be increasingly price favorable given this set-up.

… and for some MORE of the news you can use » IGMs Press Picks for today (10 NOV) to help weed thru the noise (some of which can be found over here at Finviz).

The conditions for a turning point in US rates are starting to fall into place: (1) rent inflation is likely to peak soon, (2) core goods inflation is slowing, (3) the quit rate has been declining for a few months in a row, (4) the Senior Loan Officer survey is consistent with well below potential growth, and (5) there are downside risks to fiscal policy following the midterm elections.

However, a number of factors suggest waiting for confirmation before changing our outright duration view on UST: (1) inflation is still significantly above the Fed's target, (2) the labour market is still tight, (3) the credit market environment remains benign, and (4) the Fed has conveyed a clear preference for erring on the side of over vs. under tightening.

Even so, entering a 10Y UST-Bund tightener is attractive, in our view. From a strategic perspective, the Fed should go through the three stages of pivot ahead of the ECB, as reflected in our current yield forecasts. From a tactical perspective, the Treasury/Bund spread is close to its cycle high, and lower market fixings for tomorrow's inflation print suggest a possible downside surprise in the CPI. Hence, we add to our macro portfolio a 10Y UST-Bund tightener with an indicative target of 150bp and an indicative stop of 210bp.

Interesting … Moving along then TO this from Barclays, which is thematically consistent

Recession indicators: Benign, for now... Usual recession probability metrics, which extract signals from employment growth and the slope of the yield curve, do not indicate that a recession is imminent. We think this is misleading, in part, because we, and markets, are anticipating scenarios that are shallower than typical historical recessions.

Our baseline economic outlook includes a shallow recession in the US next year, with GDP registering a cumulative decline of 0.7% from Q1 through Q3 2023. However, data on activity are sending mixed signals, at best, about recession risks, with GDP bouncing back in Q3 and the labor market looking very robust through October. This note assesses risks through the lens of indicators that have informed our prior research: employment growth and the yield curve slope.

Across a wide array of possible activity indicators, the US Economics team's preferred approach is our labor market tipping points model. This model uses information about payroll employment to draw inferences about the cyclical state of the economy, using a regime-switching approach that, among other things, identifies a stall phase where the economy becomes vulnerable to recession. In past research, we have shown that this approach provides useful advance signals about the economy's vulnerability to typical recession scenarios.

With gains in payroll employment remaining robust through October, this model sees limited vulnerability: the fitted probability of a stall in the current quarter is no more than 10%, and the probability of being in recession is less than 1%. In our view, this highlights scenarios where the Fed's hiking campaign does not culminate with a "typical" economic recession, consistent with the FOMC's baseline in the September SEPs. That said, signals from our labor market indicator could significantly understate recession risks, in part because the model does not account for the downdraft to activity from the Fed's extraordinarily aggressive tightening campaign.

Meanwhile, the 3m10y yield curve is nearing inversion and, historically, the economy has entered into a recession, on average, about 11 months from the date this occurs, with a range of 6 to 17 months. At flat levels, the 3m10y curve would signal a recession risk of about 30%, significantly above an unconditional probability of about 15%.

With the Fed widely expected to hike aggressively over the coming months, we think it may be more useful to look at the shape of the 3m10y curve on a forward basis. With this measure priced to be inverted by almost 100bp by March 2023, the probability of a recession 12 months forward rises from 30% to about 60%. This is well above typical levels ahead of recessions, but roughly in line with consensus forecasts.

Much as with the tipping points model, we think that the yield curve may be sending important information about the high likelihood that the market is placing on shallow recession or soft landing scenarios that differ from the historical experience. Indeed, with longer-term inflation expectations well anchored, markets have priced in scenarios where inflation comes down "on its own" due to easing supply chain pressures and other influences, so that the Fed does not need to weigh as heavily on aggregate demand.

Economists are once again transforming into used car dealers. In other words, it is US consumer price inflation day. Used car prices will slow the decline in inflation. There appears to be a growing gap between wholesale and retail prices as dealers try to expand profit margins (though some might have bought high and are now "hodling" on).

Pushing US inflation lower will be health-insurance-related costs. The overall story is the same as elsewhere. Durable goods prices have moved rapidly into disinflation and deflation. Commodity prices are beyond the reach of central banks (gasoline will add to today’s data). The question is whether slowing demand and a changing narrative can squeeze profit margins in other sectors.

The ECB publishes its economic bulletin, and there are no fewer than seven Federal Reserve speakers scheduled. It is perhaps possible to have too much of a good thing.

Sadly, events are forcing economists to talk crypto. Economically, recent plunges in price are mainly about resource allocation. Crypto transferred wealth from many buyers to a few sellers, but too few people hold it to cause a serious negative economic wealth effect. With less crypto activity, energy and labor might be transferred to economically productive sources (assuming labor has transferrable skills).

This holiday season is likely to be characterized by a bargain savvy consumer. Our survey revealed that 70% of shoppers are waiting for stores to offer discounts before they begin their holiday shopping and the majority of shoppers are waiting to see deals in excess of 20%. Consumers are largely planning to spend a similar amount on holiday goods this year versus last year. Stores offering the biggest discounts will be able to grab the largest wallet share but at a hit to margins.

The US Economics team sees persistently higher inflation, rising interest rates, and fading excess savings as the main headwinds the consumer holiday shopping this year. The labor market remains strong though providing a positive driver for consumer spending this holiday season.

Mirroring the pattern we have been seeing since pandemic restrictions were lifted, consumer demand for services are stronger while the outlook for goods is softening. Our US Airlines team is bullish on travel and they expect a strong holiday season. The team's leading indicator for air traffic (FLITE) is forecasting revenue passenger kilometers (RPKs) well above 2019 levels.

Department stores and specialty apparel retailers' profits are at risk this holiday season as these companies are over-stocked and retailers have a tendency to slash prices when consumers are hesitant to spend. Slowing discretionary spending is also likely to weigh on hardline/broadline retailers and retail sales appear to have already pulled back in recent weeks even with higher promotions.

The IT Hardware team is preparing for a challenging holiday shopping season as shoppers pull back on consumer electronics and PC spending (two categories where we saw demand pull forward during lockdown). E-Commerce retailers will not be immune to any consumer weakness seen this holiday season.

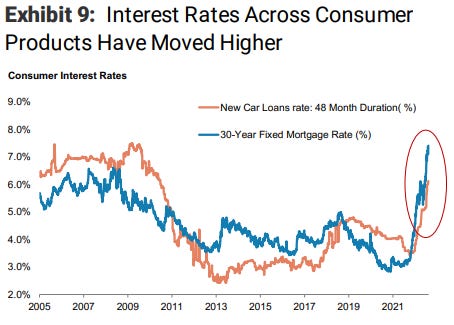

… Higher Interest Rates: The target federal funds rate Interest rates are 400bp higher than a year ago. As a result, financial conditions more broadly have tightened significantly as well. Mortgage rates are over 7%, causinghousing affordability to deteriorate faster than any point in our data history (Exhibit 9). In fact, since the start of the year, the monthly payment on the median priced home has increased 66%.For lower income households, who are less likely to own a home and are more affected by revolving credit card interest rates, they are facing average consumer credit interest rates of 16.3% (high since 1993).

Rates matter and WisdomTree’s (and former MS strat) Kevin Flanagan asks if

… The aforementioned UST yield levels are not meant to be an outright prediction. There is no doubt the Fed seems to be leaning toward a slower pace of rate hikes, but the terminal rate sure looks like it’s going to be headed in the 5% direction. Against this backdrop, history suggests 5% yield handles could be forthcoming for short-term Treasuries, at a minimum, with intermediate maturities such as the 5-Year note not too far behind. At this point, I’m not ready to make that assumption for the UST 10-Year yield (at least not yet), but it does appear as if some renewed elevation moving back into the 4.25%–4.5% trading range (if not a bit higher) is a reasonable scenario.

Finally, as I hit SEND, I’ll once again say thanks for your patience ahead of time. Travelling tomorrow as Thing 1 likely playing his final football game this weekend …Not sure I’ll be back in time to organize anything of a weekly update ahead of the markets opening Sunday evening …

And a live check in with how MODERN MONETARY THEORY IS GOING …

(where’s Steph Kelton these days? still on book tour? askin’ for a friend)

Finally, always knew there was some there there, to this one

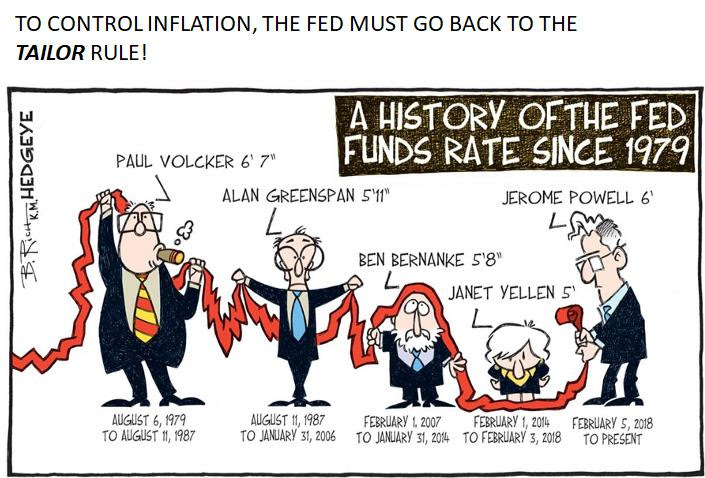

Based on the TAILOR rule — Vocker at 6’7” and JPOW @ 6’ … perhaps a stepdown of hikes IS closer than it appears in the mirror?