Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this note … Sending off a quick few quick thoughts and a visual as I will be outta pocket tomorrow and regular spammation of this ‘stack and yer inbox should resume on Thursday.

… Boy, that was a rough start to the day and Team Rate Cut as …

ZH: Stocks & Bonds Slammed After Unionized & Govt Workers Send Employment Costs Soaring In Q1

… it then got worse for those without financial assets (as far as they know) but ‘only’ a hope and a dream to someday buy a home …

ZH: 'Affordabiity Crisis' Worsens As US Home Prices Soar Near Record High In Feb

… and then, wait, there was even more and let us not forget, bad = good right …

ZH: Fastest Drop Since 'Lehman': Chicago PMI Puke Screams Stagflation

ZH: 'Expectations' Plunge To 11-Year-Lows As Conference Board Confidence Craters

… and just like that, Team Rate CUT was right back in this thing watching equities melt all. day. long…

… so nobody anywhere was safe haven other than gold? in my priors, didn’t really talk with those booking gold so as to have on the books for months end … guessing price action witnessed today NOT going to make folks happy and MAY, just may have folks stop and pause as S&Ps had first down month since October?

Hmmm … what else has been going on at same time? Oh right, RATES have been pricing OUT rate cuts … (premature to think HIKES — see BBG story below and think interest costs / burden // and while never ZERO chance of hikes, certainly going to be very funTERtaining few months just ahead for the Fed) …

What next? Perhaps JPOW offers some clues tomorrow? How to trade it? I’ve NO idea (but DBs Ruskin below does — see just below…) but for now, a best guess …

Bloomberg: Fed to Signal Delay of Interest-Rate Cuts

Officials may tweak policy statement amid stickier inflation

Central bank will likely announce slower balance-sheet unwind

… and so I’ll quit while I’m behind, hit send and wish you all very best of luck tomorrow as you turn the page in the calendar and start all over!

Before I hit SEND, some of THE VIEWS you might be able to use … here’s SOME of what Global Wall St is sayin’ about the day which just was …

The Employment Cost Index for civilian workers rose 1.2% 3m in March, accelerating from 0.9% in the preceding three-month period. This will further undermine confidence that inflation is set for a sustained slowing to 2% as the FOMC meets this week, amplifying risks of delayed rate cuts.

… With the incoming ECI estimate, our state-space model now infers that disinflationary pressures on underlying wages have stalled since late 2023…The updated trajectory of underlying wage growth now looks flat since October 2023 (Figure 2), with the monthly pace still quite elevated relative to the 0.20-0.25% m/m range that prevailed in the years leading into the pandemic…

BARCAP: February house prices post surprisingly strong gains

The FHFA and S&P CoreLogic CS 20-City indexes both posted surprisingly strong increases in February, growing 1.2% and 0.61% m/m, respectively. Both indexes deviated from their recent downward trends with today's strong prints.

The world of fixed income is undergoing rapid and profound changes. New technologies are transforming the landscape of trading, at a time when record issuance of US Treasuries is posing new risks to financial stability. We take stock of the shifts, and the possible shocks, in this 2024 edition of the Equity Gilt Study.

US Treasuries Treasury tsunami Investors are faced with persistently wide deficits as far as the eye can see. We argue that the tsunami of Treasuries will affect several key assumptions underpinning the fixed income markets, from returns in holding cash to compensation for taking duration risks to how investors view the role of USTs in a portfolio.

… We think that high returns for holding cash are here to stay as persistently wide deficits shift the saving-investment imbalance away from saving, at a time when investment demand from the green energy and AI transition is already competing for the low household saving rate, arguing for a higher equilibrium rate than pre-COVID. In addition, active fiscal policy should raise the through-the-cycle average policy rate as it reduces the likelihood of deep recessions.

Scope for the Fed’s reaction function to shift more hawkish given the strength in data alters the market regimes outlook.

Through the lens of our BERT regime analyser, we had previously argued that fluctuation between the buying assets (‘B’) and expansion (‘E’) regimes as most likely, but now flag the risk of a tightening regime ('T’) has increased.

According to our analysis, which also includes MarFA™ valuations, some assets can perform across multiple regimes. In E and T regimes, USDJPY can rise above 160, and long rates forward vol can perform. Long equities can perform in E and B, and commodity carry in T and R.

While a recession (R) regime is a tail risk, it could result in lower equities, a duration rally, weaker USDJPY and higher USDMXN. We favour defensive liquid alternative strategies: commodity carry, FX STEER™ strategy, the quality factor and intraday trend.

… Rates: Short duration via US 30y – as with USDJPY, this is currently not as appealing from a valuation perspective, but projections of further moves higher in real yields and inflation expectations suggest that the 30y could rise to 65bp.

… Rates: US yields appear too high according to our MarFA-Cyclical and the shorter-term MarFA™ Macro models. This is particularly the case at the 5y points of the curve. Our framework favours receive positions in a B regime.

The US 2y note has rallied on all of the last four FOMC days, and eight of the last 10 final FOMC days of meetings since February '23. The 10y Treasury note reaction has been even more pronounced, rallying on nine of the last ten final FOMC days. Not surprisingly the associated skew for median US equities performance has been positive. The USD has also tended to weaken consistently, but only moderately - the average absolute change on final FOMC days is just 0.5% for EUR/USD, which is indicative of low FX vol relative to the rates market.

Over the last 2 years there have tended to be bigger bullish short-end reactions on FOMC meetings when 'the dots' are not provided, which is at least some evidence that when the dots and Fed forecasts do not do the talking/distracting, Powell has helped prompt the bullish reaction. In the past, any fear of Fed "hawkishness" preceding the FOMC meetings, has then had a strong tendency to be quickly reversed, but will the Fed correct the market's recent more hawkish predilections this time around? Probably not, and here is why…

Goldilocks: Employment Cost Index Above Expectations in Q1

BOTTOM LINE: The employment cost index rose 1.2% in 2024Q1 (not annualized), above expectations. Compensation growth was once again disproportionately strong among unionized workers, which we see as a lagging indicator because union workers' contracts adjust less frequently. Our wage tracker now stands at 4.5% on a quarterly annualized basis in Q1 (vs. 4.1% in Q4) and 4.3% on a year-over-year basis (vs. 4.7% in Q4).

Wells Fargo: Q1 ECI Delivers Another Setback for the Fed's Inflation Fight

Summary The Q1 reading for the Employment Cost Index (ECI) was yet another data point suggesting that progress on inflation is stalling out. The ECI is the Fed's preferred measure of labor cost growth, and the 1.2% quarter-over-quarter increase was stronger than consensus expectations for a 1.0% gain. An equally-high reading one year ago kept the year-over-year gain stuck at 4.2%. Seasonal factors may not quite be fully capturing the wage and benefits dynamics at the start of the year, but otherwise the details were not suggestive of many one-off quirks. Private sector employment costs jumped sequentially, and excluding sometimes volatile incentive paid occupations did nothing to dampen the gain.

On balance, today's ECI reading is not the end of the world for the FOMC, but it is yet another data point that suggests the inflation slowdown that began this time last year stalled out in the first quarter of 2024. We expect the FOMC to hold the federal funds rate steady at its next few meetings, leaving plenty of time to ascertain whether the Q1 data is a bump in the road or a canary in the coal mine. Signs of faltering labor demand, declining labor market turnover and still solid labor supply suggest to us that employment costs will decelerate further as the year progresses. But, it will take time to see that in the data, and this is why we think the FOMC will keep rates unchanged through at least the summer.

Wells Fargo: Slipping Confidence Hard to Square with Resilient Spending

Summary Confidence is slipping among consumers amid concern about the current labor market situation as well as future business conditions and whether income can keep up.

… And from Global Wall Street inbox TO the WWW,

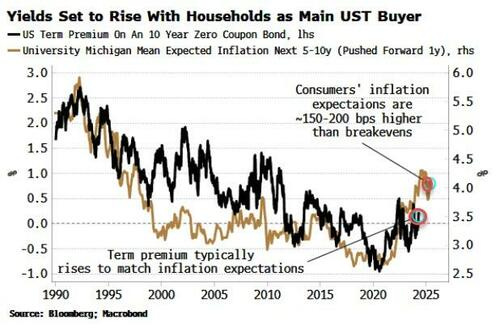

Bloomberg: Don't Buy Rate-Hike Hype, Next Fed Move Is A Cut (thinkISSUANCE)

… Households have become the de facto buyer of last resort for Treasuries. But there’s nothing to suppose they’ll be happy to continue to do so at any price. As the chart below shows, consumers’ long-term inflation expectations typically lead term premium. The market’s view of longer-term inflation, i.e. breakevens, is about 150-200 basis points lower than households’ outlook. As the UST buyer of last resort, households will increasingly set the price, one that’s likely to be lower than it is now.

Higher long-term yields will lead to the government having to borrow yet more to pay its spiraling interest-bill on its outstanding debt. But that points to fewer reserves and falling reserve velocity – effectively undoing the work of the Yellen pivot and leaving the stock market in a precarious spot.

The Fed is thus likely to cut rates in a quid pro quo with the Treasury. This would not only help the government fulfill its borrowing requirements at a non-usurious cost, it also helps the Fed with its responsibility for financial stability by taking the pressure off risk assets and reducing the likelihood of a funding squeeze.

MarketWatch: Why T-bill and chill is here to stay, these strategists say

… The U.K. bank also provides a barrage of interesting investment commentary accompanying this data, and the latest edition focused on the rapid and what it called profound changes in the world of fixed income. A report from its U.S. rates team led by Anshul Pradhan says the worsening fiscal profile should affect several key assumptions underpinning the fixed income markets.

Among their conclusions — high returns for cash are here to stay.

That’s a function not just of the massive deficits that neither major political party wants to tackle, but a low personal savings rate and the need for major green energy-related investments. “Hence, in the context of structurally wide deficits, the steady state nominal policy rate could be 3.5% assuming 2% inflation. If inflation settles at a higher level — at say 2.5% — the steady state nominal rate would be 4%,” they say. The Fed, by contrast, expects the longer-run federal funds rate to range from 2.5% to 3.1%.

Barclays analysts also note a smaller tolerance by authorities to accept recessions. “While there is a possibility that policymakers could feel constrained in using fiscal policy to the extent needed in the next downturn given the fiscal profile, the same argument could have been made during COVID as debt projections were equally bleak but fiscal measures were still deployed,” they say. So that means not just that the neutral rate is higher, but also the through-the-cycle average won’t be as far below the neutral rate.

Furthermore, the demand base is moving from price insensitive buyers — think the Fed executing monetary policy or banks meeting domestic capital requirements — to sensitive ones, like hedge funds. That means there will be a headwind for Treasury valuations going forward.

And now we get to the T-bill and chill discussion. “Barring a downturn that creates attractive prospects for total returns in owning government funds, it is unclear why investors would buy 10y Treasuries at 4.6% when 3m T-bills are yielding 5.3%. Even if the Fed cuts to, say, 3.5% over the medium term, history suggests that a healthy term premium would be demanded over the expected returning in rolling T-bills, keeping long-end Treasuries elevated,” they say.

A worrying fiscal profile also has implications for the role of bonds in a broad multi-asset portfolio. While high inflation is usually blamed for the falling correlation between equity prices and Treasury yields, a world in which investors are worried about the fiscal profile is “unlikely to be kind to [U.S. Treasurys’] role as a diversifier,” they say…

Forget 2 Minutes to Midnight, Bill Bonner says the 130% Debt to GDP ratio, which will tripwire during the next administration, is the real Doomsday Clock. He likes a Dow-Gold ratio of 5 for the Dow's future 'bottom'. I'm looking for a 2-1 ratio or better, but who really knows....

Yes, sir !!!

I think we are seeing the answer to the

Question: Does Big Government Spending lead to Stagflation??

35 Trillion in Debt, 1.5-2.0 T. in deficits

1 Trillion in Interest Expense.

843 Billion in Q3 Estimated Treasury

Borrowings.

3.5- 4.0 % Inflation rate, after 3 years

of 20 % Cumulative Inflation.

Must be almost time for some

Politically Rigged BLS Payroll

Numbers to cover over all the CRAP

with a big fat headline for their

favorite Democrat Communist,

President Moron.

Forget 2 Minutes to Midnight, Bill Bonner says the 130% Debt to GDP ratio, which will tripwire during the next administration, is the real Doomsday Clock. He likes a Dow-Gold ratio of 5 for the Dow's future 'bottom'. I'm looking for a 2-1 ratio or better, but who really knows....