(a FEW)sellside observations, listen TO a bond BEAR - Bianco and a bull Gurevich, WATCH Lacy Hunt and consider ReSale Tales this way; weekly econ indicators and SIFMA SAYS...

Due to the geo-politics of this moment in markets history, I’ve really no choice but to step aside, allow the facts and story lines to play themselves out in the fullness of time.

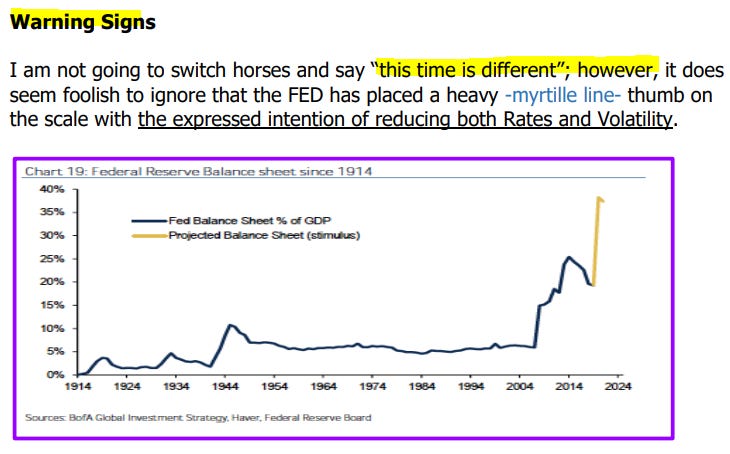

To say the coming few hours/days/weeks and months will be nothing short of stunning would likely be an understatement.

The rate hike and QT guessing game isn’t the only game on the boardwalk folks are playing. World leaders still meeting in effort to circumvent the aggressions of Russian leadership. Perhaps these increased geo-political tensions will impact the Fed’s decisions. I’ll say as of now, unlikely, until the point at which we’re ALL feeling much MORE pain (ie stocks, real-estate, crypto ‘investments’, incomes, etc…).

We’re mostly ALL feeling the pain at the pump.

I cannot help but think that ‘Earl will be up near the top of short list of driving rates and other global markets, inflation expectations and to a degree.

The PERCEPTIONS which ’degenerate rates market gamblers’ which will drive front end (EDZs, OIS) or even impact those with a more calm and cool approach to INVESTMENTS and, who are likely to BUY 2s, 5s and 7s in the holiday shortened week ahead, are constantly changing.

As are the probabilities of whether or not the Fed likely to do 50bps hike or a somewhat more benign series (5, 7, 9 or perhaps they’ll turn the dial up to 11?).

With this in mind, I’m going to limit my regular weekend update of sellside observations and guess-A-thons and offer to you a couple choice quotes (links) and visuals from those who I’ve identified over the years as THE best in the biz.

First off, then, I would have to be Ian Lyngen of BMO who has carried the torch from the days when he worked with David Ader and year in and out, won the II poll for strategy and tech analysis. His weekly is titled Explanation or Excuse and he sticks the landing with his opening sentence,

In the week ahead, there will be two key influences driving the overall direction of US rates; geopolitics and supply…

Specifically TO supply, the note suggests supply / demand backdrop lends itself to continued core flattening bias and that it works in both bullish and bearish environments. A single excerpt and visual from his weekly which speaks TO the curvature as well as buying HIGHER PRICES (if there is a break), caught my attention

… The current resteepening momentum evident in 5s/30s may have further to run given that, unlike 2s, the broader risk off sentiment has contributed to the belly bid – in addition to moderating expectations for a 50 bp liftoff. It’s with this backdrop that we’re focused on the 10-year sector and the potential for a further rally as the 1.906% resistance quickly approaches. An in-range consolidation in 10s between 1.906% and 2.063% has been the path of least resistance after the double-top was established when 2.063% failed to break on the second attempt (February 16). Now that stochasticshavereversedfromoversold territory and there remains a solid bid for the benchmark, we’d favor going with any break of 10-year yields below 1.90%.

NOTED. For somewhat MORE, I’d strongly encourage one find latest podcast on your favorite platforms (I prefer GOOG) but one may also locate his sage words — Flight of the Hawks — directly HERE.

Next up are a few thoughts from Morgan Stanley’s rates group who’s weekly notes ALWAYS have a catchy title and some meaningful content. Sometimes I agree and others I don’t. Currently maintaining a flattening bias — as BMO above — doesn’t seem to go too far out the strategy limb,

Bearing With Geopolitics Investors, grappling with geopolitical uncertainty in the 2nd half of February will then have to grapple with central bank uncertainty over the 1st half of March. Risks skew toward higher inflation, stronger growth, and more hawkish central banks. Stay bearish bonds while bearing with geopolitics…

… In global rates markets, we maintain 2s30s flatteners, short 5y TIPS outright, and short 5y TIPS vs long EDZ3 (DV01 ratio of 0.8:1). We continue to recommend UST 5s30s flatteners, short 12m T-bills vs OIS, and paid positions in H3 SOFR/FF basis. In US rates vol, we continue to recommend 6m5s30s conditional bull steepeners, long 6m1y1y forward vol positions, and 1x1 1y30y payer spreads…

… we think that selling volatility outright is a risky endeavour when the Fed might be looking to tighten FCI.

Exhibit 22 shows the relationship between Chicago Fed FCI and 3m10y volatility over the last two decades. Higher volatility and tighter financial conditions have gone hand in hand over the years, suggesting that if the Fed wants to tighten financial conditions, it is likely going to be accompanied by higher volatility. Thus, we caution against exposures that primarily depend on realizing lower volatility.

Importantly, as volatility increases, it also opens the door to additional relative value opportunities as evidenced by our Morgan Stanley Treasury Relative Value Index (see MSTVI index on Bloomberg). The index rose sharply this week, in line with the rise in rate volatility (see Exhibit 23), and is currently approaching peak levels we have seen in the last ten years.

Financial conditions and relative value! NOTED. Onwards and upwards, then and I’ll admit that a weekend of sellside observations and guessing as to WHAT will / won’t be important in the week ahead, well, would be incomplete with some reference TO a note / thoughts from Goldilocks and so, for all us former and current MUPPETS,

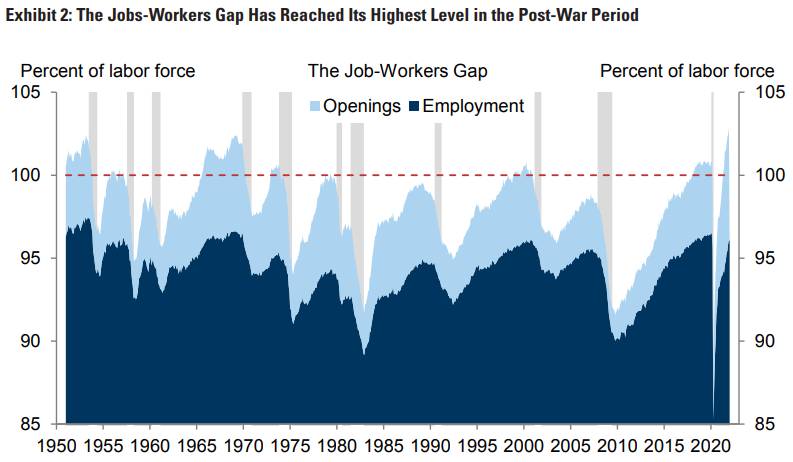

We propose measuring labor market tightness as the difference between the total number of jobs (i.e. employment plus job openings) and the number of workers (i.e. the labor force). The jobs-workers gap currently stands at +4.6mn workers or +2.8% of the labor force, the most overheated level in postwar US history. This is because employment relative to the labor force is fairly high—i.e. the unemployment rate is fairly low—and job openings are extremely high.

Statistically, the jobs-workers gap explains wage growth somewhat better than other tightness measures, such as the gap between the unemployment rate and its (estimated) natural rate, the prime-age employment/population ratio, or the ratio of unemployed workers to job openings. At present, it points to +4½% yoy nominal wage growth, which is ½-1pp above predictions from other measures.

Once we allow for the strong momentum in the latest sequential wage numbers, the signal from the jobs-workers gap looks consistent with our wage growth forecast of 5% year-on-year by the end of 2022. Assuming 1½-2% productivity growth, this implies unit labor cost inflation of 3-3½%. If sustained, such a pace would make it hard, if not impossible, for PCE inflation to return to the Fed’s 2% target.

In principle, the jobs-workers gap may start to ease even while other tightness measures (such as the unemployment gap or the prime-age E/P ratio) are still catching up. Job openings have moved sideways since mid-2021, and there are signs in business surveys and alternative data that they may have started to edge down in the last couple of months. Additionally, some workers should return to the labor force as Covid fears recede and excess savings are exhausted.

However, eliminating the jobs-workers gap—and thereby restoring balance to the labor market—will likely require a significantly larger deceleration in output and employment growth than predicted by the consensus of forecasters, let alone the FOMC. And even our below-consensus forecast that real GDP will grow 2¼% on a Q4/Q4 basis in 2022 would probably keep the labor market out of balance well into 2023. The jobs-workers gap therefore reinforces our hawkish forecast of seven 25bp funds rate hikes in 2022 and a terminal funds rate of 2½-2¾%, and it suggests that the risks to the latter call are tilted to the upside.

…There are several takeaways from Exhibit 2. For most of the postwar period, total workers have exceeded total jobs. Currently, however, the jobs-workers gap stands at +2.8pp, the highest level in the postwar US history. The current overshoot of jobs relative to workers is therefore a leading candidate to explain the recent surge in wage growth.

When all else fails, propose a NEW WAY in which to measure the statistics ensuring one thing — your very own JOB SECURITY — at the expense of … everyone in the sample size AND at the same time, proving there’s simply NO WAY you could be wrong…Read the entire note and enjoy!

In today’s Dispatch we’ll distill and amplify the Volcker moment theme that we wrote about on Wednesday (see here). To remind, the context here is how to “curb inflation without a recession, in a socially just manner where the politicalgoalis redistribution through preserving wage growth at the bottom and the monetary goal is curbing services inflation by deflating asset prices at the topend of the income distribution”. The themes that this new and complicated “socially just” dual mandate (as opposed to plain dual mandate) brings up are these:

Same operation (1stBOS) and different author out with a good note for the long weekend, talking of SUPPLY PRESSURE GAUGE COOLING and from their technical analysis department, you may be interested in latest,

Market Spotlight: US Equity topping threat grows One of our “Key Themes for 2022” has been for US equity markets to have a more challenging year with some likely aggressive swings, both up and down. We are now though seeing growing evidence of a more negative backdrop given geopolitical tensions, with the risk growing that we are now seeing the formation of more important tops.

We maintain our negative outlook for the S&P 500 to retest the 4223/4199 key support cluster but whilst we had previously looked for this to hold again to define the lower end of a broader range, we now see the risk that this key support will be removed as elevated.

Below 4199 would in our view mark a (slightly messy) “head & shoulders” top to warn of a more significant decline warning of further weakness with the next major support seen at the 38.2% retracement of the 2020/2021 bull market at 3855/15…

In effort to wrap this up, and having had the pleasure of a long drive this weekend to pick up Thing 1 who did NOT travel with his peers to Thailand to complete a project, and having the benefit of time to listen TO a couple MACRO VOICES podcasts … well, something from couple FI ‘gurus’ (not one mention of BMO … but whatever),

Alex Gurevich (BULLISH BONDS, very interesting MATH — must listen to the interview as HE interprets PRICE ACTION — before you simply write him / me off as village idiots): The Trades of March 2020

And finally, a couple things from THE Convexity Maven - Harley Bassman. First off he dropped this email into inboxes last week,

The Yield Curve is the single best predictor of the economy. Like clockwork, a curve inversion (where short-term rates rise above long-term rates) precedes a recession by about 16 months.

While I will not claim I predicted Covid, I did highlight in a November 2018 Commentary that a recession in early 2020 was being signaled.

Presently, the Yield Curve is again flashing yellow - should we take notice ?

Today's Commentary, "Dangerous Curves Ahead", explores this concept and why it may be different this time. (Did I just say that ?)

With this — his latest commentary in mind, I’d feel guilty not to mention two final things. FIRST, the Lacy Hunt's guest appearance on the Keeping It Simple webinar is here and was just AFTER CPI which made it all the more fun-ter-taining.

Harley Bassman — THE convexity MAVEN (@ConvexityMaven): I challenge Dr. Hunt and @profplum99 to explain why inflation will recede and the economy will soon turn South

Who do you believe, me or your lying eyes ?

NEXT from someone who’s process of thought is nearly unmatched and who’s ability to think outside the sellside box is very much appreciated, Eric Basmajian of EPBMacro, sent a note addressing what happened this past week with ReSale TALES. As most / many were quick to jump TO conclusions that omicron didn’t impeded growth and it’s ONLY FULL STEAM AHEAD, well, you may not like what follows BUT … as with Lacy Hunt and Alex Gurevich above, I'd BEG you to read / listen to and then, tell me how or why you disagree.

This week two important coincident data points were released for the January reporting period. The Census Bureau released the Retail Sales report which showed a surprising jump relative to December and the Federal Reserve published their Industrial Production Index, also showing a larger than expected gain.

Retail sales are reported in nominal dollars so we have to adjust the time series for the Consumer Price Index in order to arrive at a figure that measures "real consumption." Furthermore, the month-to-month data comparisons are extremely noisy and hold no cyclical value. As with all data we measure at EPB Macro Research, the trending direction of the growth rate is where we find the most important cyclical information.

In real terms, retail sales growth jumped in January to 2.3% when measured via a smoothed six-month annualized growth rate. The trending direction of real retail sales growth remains sharply lower and the 2.3% reading was the second-lowest growth rate since May 2020.

January certainly held stronger growth relative to December but from a cyclical vantage point, the trending direction of real consumption growth was unchanged.

Moving from consumption to production, the Federal Reserve's IP index showed a jump in January to a 6.2% annualized growth rate relative to 4.0% for December when plotted on a smoothed cyclical basis. This increase in growth, however, was due to a 9.9% monthly surge in utility production, accounting for more than 75% of the total index's monthly gain…

Clearly I’m most sympathetic TO Gurevich — even MORE confident now than EVER — perhaps time to start thinking about reducing durational shorts — and with Lacy Hunt and EPBMacro just above. Things may APPEAR ok on the surface but when you think these things thru, well, there’s always more than meets the eye.

And with great respect of The Convexity Maven, perhaps it IS different this time, as HE concludes,

… While my memory is indeed growing cobwebs, I cannot quickly recall a flattening of the Yield Curve BEFORE the first interest rate hike by the FED. Usually, the FED starts hiking until something breaks and then long-term interest rates decline in anticipation of a recession and resulting reversal of FED policy.

Even more strange is that Yield Curve flattening usually arrives with short-term rates rising a lot, and long-term rates rising less. So, for example, the two-year rate may rise by 100bps while long-term rates rise by only 50bps; thus, compressing the Yield Curve.

This time, despite a raging increase in CPI inflation, in contrast to asset inflation, the Yield Curve has rotated with short-term rates rising and long-term rates declining.

Curve rotation is a late-stage event that should not occur before the first hike.

You’ve got some time before CA$H markets open (Monday evening) and only a few hours ahead of FUTURES this evening, 6p. A few highlights:

And finally, a friendly reminder,

… that’s all for now. Enjoy rest of your long weekend!!