With news making rounds of a Russian striking Ukranian base near the Polish border (ie striking closer TO NATO member — ‘likely a MESSAGE’ -ZH), seems to me that news is of more expansion OF offensive as opposed to whatever red-headline drove risk / yields Friday.

This makes ME think more about a risk OFF (and bond BID) reflex at this evenings open but then, ZH now offering some more HOPE from the Guardian and BBG

… The peace process is also getting a fresh kick start after Bloomberg reported that the U.S. and China will hold the first high-level, in-person talks since Russia’s full invasion of Ukraine, as the Biden administration continues to try to enlist Beijing to exert influence on its neighbor to end the crisis.

National Security Adviser Jake Sullivan will meet in Rome on Monday with China’s top diplomat, Communist Party Politburo member Yang Jiechi, according to a person familiar with the details of the plan.

President Joe Biden’s top advisers have been working to increase pressure on China to enforce sanctions on Russia’s economy imposed by the U.S. and its European and Asian allies. So far, U.S. officials have said they haven’t seen evidence that Beijing has tried to circumvent them, although that just means that they haven't looked hard enough.

In any case, if China does agree to mediate talks, it would be seen as a significant development toward peace. Then again, since the Biden admin has little to gain from an accelerated return to normalcy ahead of the midterms - after all the inflationary impulse will be here to stay well into 2023 - especially if the president can no longer blame Putin for everything that is wrong in the US domestically, we expect that this glimmer of hope will be promptly dashed over the next 24-48 hours.

I read this and would LIKE to think / HOPE there’s some truth, can’t help but feel

There’s been all sorts of ink spilled (before the weekend strike near Polish border) and while that, in and of itself, never ceases to amaze me, I will defer TO these few comments from those still in a seat of trying offer some sort of markets guidance in a world where any new or old normal, is quite a distance away.

Jumping right in and from a large Canadian bank (home of the best RATES strategist in the biz)

A Fed Day Like No Other (2s10s flattening view persists and remaining tactically LONG outta 10yr auction)

AND they go thru several OTHER conflicts as well … Finally from one of German banks fan favs (early morning guy) is latest MONTHLY CHARTS, “Dislocations”

Next on MY list of things to read before weekend is over and not one I ALWAYS agree with but respect a great deal — Hornbach & Co of MS

New shorts (at $10m) across the curve into cheapening => net short positioning become extended to $70m / 95th percentile and increasingly one-sided, with profits at the front end (large) and building across the curve.

Short profits in eurodollar - Eurodollar white but extended in legacy (short/profits) => short momentum 98.64 in ED Sept 22

10y shorts / balanced risk - one-side short (at $21m / 90th percentile) and now 10bps in profit below 126-24 => short profits squeezed at 126-05 vs 125-16 (extreme profit)

Large shorts in 30y (at $15m / 90th percentile) => large one-sided short in profit below 185-13 => support / resistance at 181-06 / 178-08 (extreme profit)

Curves: 2/10s flattening momentum in profits below 80bps, 10/30s neutral in futures but extended flatteners in cash at 35bps

Cross Market: Long TY/Short RX and in profit below 177bps (moving back into profit)

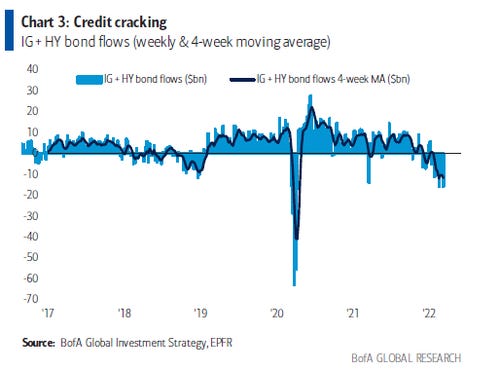

Liquidity: Liquidity stressed concentrated in Europe but remains challenging in US.

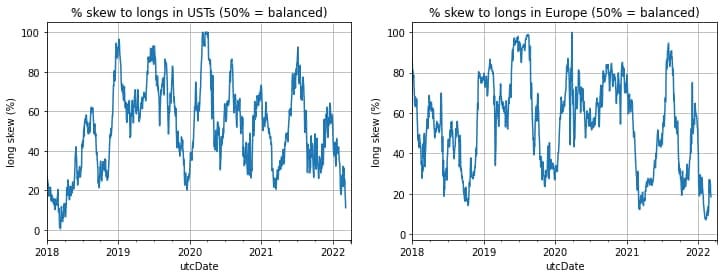

… How has deleveraging impacted the positioning landscape? One-sided short! Over the last few weeks into rising rates volatility we have seen both short covering and long liquidation. However over the last few sessions long liquidation has been the major driver of recent cheapening driving positioning to become highly skewed to shorts (90% in UST and 80% in EGBs). This is the largest it has been since early 2018 which ultimated ended in a short squeeze to lower in rates!

LPL asks: Are Long-Term Rates Setting Up for a Huge Move (higher, of course)?

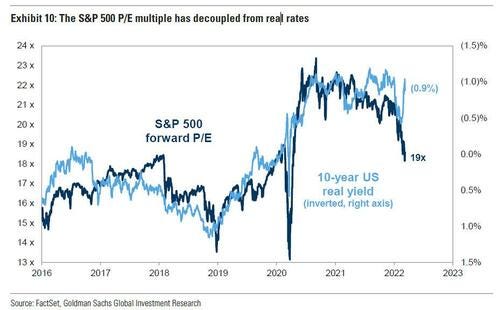

ZH: GS CUTS S&P target TO 4700, warns of ‘recession downside’ TO 3600

(SIDE NOTE — QUESTION for one / all — how’s THIS possible and allowed. Asking for a friend — “The full Goldman report is available to pro subs in the usual place.”)

In closing, as we look forward TO the week ahead with HOPE for some sort of peace to break out AS rate hikes / QT plans (and war) rolls on, for those wanting / needing more fundamental input, WELLS

Wrong or right, agree or not — kindly check yer politics at the door and reaquaint with common sense and tell me why this isn’t … appropriate if not all too accurate (and depressing)?

Hopefully you’ve set your clocks ahead and we’ll ALL enjoy some extended sunlight in the days/weeks and months just ahead.