Waterfall of information being created and spammed out to our collective inboxes over the past several days and I’ll spare you a run through of all the accelerated taper / tightening timeframes … Trying to get through to the highlights and somewhat bigger picture things being said … here goes.

Links provided are publicly available to the best of my knowledge. Otherwise, excerpts to consider (reach out for more specifics and context). In no particular order

ABNAmrowith reminder of how important financial conditions are …

Does Omicron change the monetary policy outlook?

… Our unchanged outlook for central banks reflects that the starting point compared to Covid I is different in terms of the supply side and inflation, and Omicron could prove to be at least as much a supply shock as a demand shock (see our previous note here). However, we do argue that a very sharp tightening of financial conditions would be the game changer for central banks, though we are currently nowhere near close to that.

Fed still heading for faster taper and 2022 rate hikes

In his testimony to Congress yesterday, Fed Chair Powell confirmed the hawkish pivot of the Fed we recently flagged with our change in rate hike expectations. Powell followed up on comments from a range of FOMC members recently – doves and hawks alike – suggesting an imminent speeding up of tapering is on the cards. On this Powell said that the need for asset purchases has ‘clearly diminished’ and that it was appropriate to consider wrapping up purchases ‘a few months sooner’. The headline grabber was Powell’s remark that it was ‘probably a good time to retire that word’ in reference to the ‘transitory’ description of recent inflation developments. Indeed, the remarks were generally hawkish, with Powell now clearly prioritising bringing inflation under control over returning the labour market to pre-pandemic employment levels. On this, Powell said “To get back to the great labor market we had before the pandemic we’re going to need a long expansion. To get that, we’re going to need price stability,” adding that the Fed “must ensure higher inflation doesn’t become entrenched.” Powell’s comments were all the more notable considering they came after the news of the Omicron variant that has injected fresh uncertainty into the outlook. On Omicron, Powell acknowledged the downside risks this posed to the growth outlook, but he also said it meant ‘increased uncertainty for inflation’ – consistent with our view that Omicron could, if anything, put additional upward pressure on inflation. All told, the comments were consistent with our view that the Fed will announce a speeding up in tapering at its 14-15 December meeting, with purchases ending entirely by March rather than June. Thereafter, we expect the first 25bp rate hike to come in June, with an additional two hikes in September and December, and three more hikes in 2023.

ECB unlikely to extend the PEPP, but could maintain optionality

It might seem that the PEPP would be extended on the back of the eurozone’s struggle to contain the Delta strain and the new threat of the Omicron strain. After all, the function of the programme is clear from its name (Pandemic Emergency Purchase Programme). However, we do not expect a quick U-turn on the PEPP. First, there is limited information about the impact of the new strain. Second, even if Omicron leads to new global restrictions/lockdowns for a longer period, it is unclear at this stage what that would mean for the medium term outlook for inflation. The ECB reduced its medium term forecasts for inflation when the pandemic first broke, but over recent quarters it has been raising them and we are currently back in line with its pre-Covid outlook. Third, the ECB can maintain policy accommodation via its forward guidance on policy rates and by extending net purchases under the APP. There is a possibility that the ECB may delay a decision on the PEPP until early next year, but given the above considerations we think the central bank will push on and signal that the programme will likely end in March as planned. It could however maintain some optionality, by stressing that this scenario is dependent on developments, which it is monitoring carefully…

Moving on TO … STOCKS because, you know, as a RATES guy inundated with TINA and FOMO, well … STOCKS and 60/40 really 70/30 and the 30 should prolly ALSO be in stocks … so, Barclays on 2022

U.S. Equity Strategy: Outlook 2022 - Proceed with caution

We see limited upside for equities next year with a 2022 SPX price target of 4800. Household and corporate cash hoards should support modest earnings growth but persistent supply chain woes, reversal of goods consumption to trend and China hard-landing are key tail risks. We downgrade Cons. Disc. ex FANMAG to UW.

We see five tailwinds: 1) Earnings surprises continue, driven by persistent, above-trend Goods consumption fueled by a $2.5T cash hoard on the Household balance sheet. 2) $500B corporate war chest supports Buybacks and Capex. 3) With no corporate tax hikes, fiscal policy is less of a headwind. 4) Equities take measured monetary tightening in stride. 5) Positioning is extended for some investors, but they have coupled it with strong downside protection that should limit downside.

But also five tail risks: 1) Supply chain bottlenecks persist. 2) Goods consumption reverts to pre-pandemic trends. 3) Omicron variant situation worsens. 4) China's economy slows further than anticipated. 5) COVID or China-driven slowdown with persistent inflation complicates Fed's decision-making, which leads to a faster normalization of elevated P/E multiples.

Index view: Our modestly positive baseline scenario but non-trivial tail risks leads us to expect modest upside for the SPX with a 2022 year-end price target of 4800 with upside in CY 2022 EPS of $235 (+12% YoY, IBES consensus -$222) being offset by a modest decline in the P/E multiple from the current level of 23x to 20.5x.

Sector views: We downgrade Cons. Disc. ex FANMAG to UW from MW due to high valuations and the risk of a significant slowdown in Goods consumption. However, we are still cyclically oriented and remain OW Financials, FANMAG, and Healthcare; MW other Cyclical; and UW the other Defensive sectors.

Style factor views: Value should perform in line with Growth, but the near-term risks are high due to Omicron. Quality is currently the best positioned factor going into 2022, while LowVol is the worst. Momentum is well positioned in the near-term due to Covid-19 resiliency, but has the most to lose if Omicron concerns fade.

… SPX EPS Growth driven by changes in Inflation but not level of Inflation

Note that in our Top-Down inflation model, the level of inflation (measured as CPI YoY and/or PCE Deflator YoY) does not enter as a variable because we have found that earnings are not dependent on it. Instead the change in inflation does enter but it contributes positively to earnings growth. Intuitively, both companies and consumers adapt to a particular level of inflation and it is only changes in inflation which causes a change in profitability.

Our Top-Down model is based on analysis from 1994 - present (when analyst adjusted EPS is available and EM ) and thus omits the crucial period from 1965 - 1994 when inflation reached peak levels. However, even during the period of extended high inflation in the 1970s earnings were not negatively impacted Figure 27 shows that the average annual earnings growth for the top 500 companies by Sales Growth (our SPX proxy, the top 500 US companies in the Compustat database by annual sales) in the 1970s was 11.7%, which was higher than in the 1960s or 1980s. The higher level of earnings growth was driven by strong Sales Growth (average of 12.7% in the 1970s), which surpassed levels in the 1960s and the 1980s. Really the only time EPS growth turned negative during the periods of high inflation was during recessions, which is as expected. This is mainly because earnings are also a nominal variable.

Never fear, EARNINGS are merely a nominal variable … speaking of nominal and variability … 60/40 as it relates TO states and local coffers overflowing, Wells Fargo:

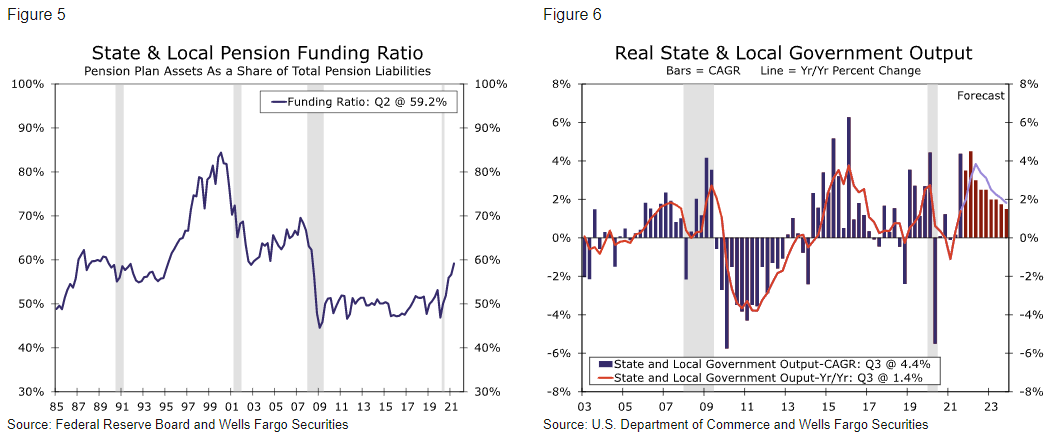

Wells: State and Local Governments Find Funds Plentiful, but Labor Scarce

… Even S&L public pension funds have seen their fortunes improve amid robust asset price returns and increased contributions from governments and their employees. In the aggregate, S&L pension funding ratios are at the highest levels since the 2008-2009 financial crisis (Figure 5), and a recent analysis by the Pew Charitable Trusts found that the nation's state retirement systems have improved significantly across a wide variety of metrics.1 As we look to 2022 and beyond, we believe S&L governments are positioned for much stronger output growth in this expansion compared to the 2010s. S&L output increased at a solid 4.4% annualized rate in Q3-2021, and we look for a similar pace of growth over the next few quarters as the education sector continues to normalize and S&L governments put their windfalls to work (Figure 6).

EMPHASIS mine. FULLY FUNDED certainly makes the 60/40 (which is now 70/30 for intents and purposes) rebalancing question become incrementally MORE interesting as 2021 comes to a close, no?

In the flurry of Fed regime change this week where JPOW retired transitory, MSs ZENTER pointed out

December 1, 2021

US Economics: A Sea Change At The Fed

A rethink of the Fed's policy stance is coming, starting with a faster taper and hawkish shift in the dot plot at its December 14-15 meeting. If inflation then cools sequentially, as we expect, a pressure valve will open and allow for a clearer separation between tapering and rate hikes.

… At the December FOMC, we expect to see a sea change in the SEP dot plot alongside an accelerated taper announcement. We think that makes a firm median of one hike in 2022 as a likely minimum of what we will see, with good reason to believe that the dot plot could show a median of two hikes in 2022. The deciding factor will be how inflation evolves as we go into next year. If inflation cools sequentially as we expect, that will take some pressure off of Fed policymakers, allowing for a clearer separation between tapering and rate hikes. But as always policy remains data dependent and if supply (both of goods and labor) remains constrained for longer and inflation remains elevated at the same time, we see hawkish risks to the policy path, putting our call for liftoff in 1Q23 at risk of earlier delivery.

Clearly here Zenter & Co wearing Team Transitory jersey despite phrase being retired.

Moving right along … DBs Francis Yared asks / answers

Why is the Fed hawkish?

The short answer. Because the Fed should "theoretically" already be above neutral.

The long answer. Inflation is above target and the Fed expects it to remain so for the next two years. The labour market is behaving as if it was through full employment. The economy is growing above potential. These are textbook conditions that require policy tightening. Fiscal policy may do the job post midterm elections. But in the meantime, the Fed has to play its part.

The timing of the announcement is unfortunate given Omicron. But the economic rationale pre-Omicron was reasonably clear. Moreover, the various Fed announcements had failed to dent financial conditions pre-Omicron. As to the impact of Omicron, it is too early to tell. But even if it turns out to be severe, there is a decent probability that it would exacerbate rather than dampen the inflationary pressures and constrain labour supply more than labour demand. Finally, higher inflation is currently a bigger problem for households than finding a job. Thus, the administration is more likely to welcome rather than oppose a more hawkish Fed. Taken together, despite the non trivial tail risks created by Omicron, it is not unreasonable for the Fed to consider accelerating taper to have some optionality from Q2 onward.

Now with the Fed’s more hawkish reasoning explained and not necessarily fully digested (or agreed with hawkish as bearish or bullish?), DB also offered a warning of sorts …

Beware the global investment gap

Markets have obsessed over the consumer in the last year, tracking household consumption as the key to recovery. And, on most metrics global consumption has returned to the pre-pandemic trend. Although expectations of 'gangbusters' consumption fuelled by excess savings have been dashed, the pandemic has made less of a dent on global consumption than the Great Recession.

The recovery looks even more impressive when it comes to investment. The Great Recession left a massive and persistent global investment gap. Investment returned to the pre-crisis trend growth rate by 2010, like consumption, but never made up for the sharp slump in 2009-10 in level terms. This time, by contrast, global investment closed the gap even before consumption did. It has bounced back to levels it would have been at on pre-pandemic trends.

Perhaps this is why markets have paid little attention to investment. But that, we think, is a mistake. In our view, one of the most important ramifications of the pandemic is a massive shortfall in productive investment. Just as the composition of global consumption has shifted from services to goods, the composition of investment has shifted from machines, equipment and intellectual property to housing.

To be sure, to the extent that residential investment is reflected in construction activity, it is more helpful for global demand than households ploughing excess savings into cash or cryptocurrency. Still, investment in machines, equipment, structures and indeed intellectual property would be far better for potential growth. If this shortfall in productive investment persists, it may thus drag on potential growth in coming years and accelerate the decline in neutral and thus terminal rates that we have been writing about all year.

Global investment has shifted from productive assets--machines, equipment, intellectual property--to real estate and consumer durables

SO a more hawkish Fed is going to eventually have to confront this global investment gap…Is a more hawkish stance going to lead us right back TO Q4 2018?

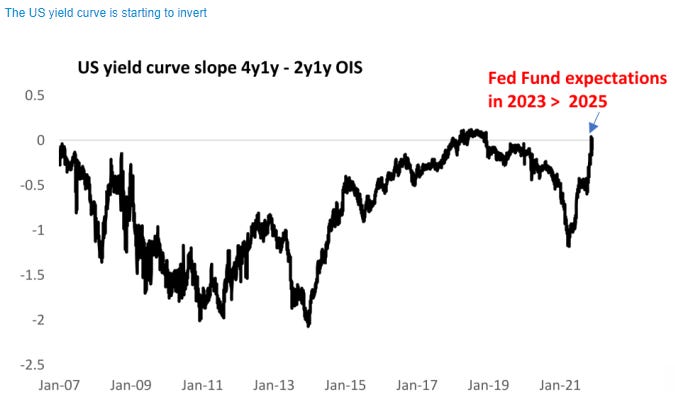

DB — on a roll — notes US yield curve starting to invert

Join the club

With Fed Chair Powell all but confirming an earlier end to the Fed’s taper program yesterday, parts of the US yield curve inverted. We are now starting to price some risk of rate cuts in a few years. In doing so the US curve joined the UK, Europe and especially many Emerging Markets where yield curves have already inverted aggressively. Yesterday we argued that the omicron variant – irrespective of the precise immunological properties – would just help reinforce existing trends, not change them. It is a fallacy that the market has been “looking through” COVID. Weak US labour supply, strong inflationary pressure in the goods sector, high excess saving, very low terminal rate pricing, a stronger dollar and very negative real rates are all because of persistent COVID forces this year not despite of them. It’s the new “COVID normal”, very different from the “old”. Is the market right to price such late-cycle dynamics? If the whole point of the Fed turning hawkish is to slow the economy down and take the unemployment rate back above the “new” NAIRU, the answer is yes.

Imagine THAT … a tighter fed policy designed to SLOW THE ECONOMY DOWN and take URATE BACK UP …

Leaving DB aside for a bit and focusing on some of the blocking and tackling in UST market … supply and demand in 2022 as per JPMs Flows & Liquidity which seems designed to support a narrative … see if you can spot what I’m referring to:

Goal seeking secured? On TO HOLIDAY SHOPPING. A SALES UPDATE via Goldilocks …

High Hopes, Higher Hurdle

■ After strong spending growth in October and early November, the pace of holiday purchasing now appears to be slowing. In Adobe’s panel of online retailers, spending over Black Friday weekend and Cyber Monday declined 1% year-on-year, its weakest pace in over a decade. This datapoint is a useful indicator of the November retail sales report (correlation +0.64 since 2012). And while firmer early-month spending or a rebound in brick and mortar purchases could offset the online slowdown, we are tentatively assuming a 0.3% decline in November retail control (mom sa). Credit card data from Fiserv/BEA and 1010data will provide additional clarity when released the week of December 6.

■ Our sector analysts are observing lower-than-usual promotional activity, and we continue to expect higher core goods prices in November and December. Our analysts also found some items out of stock—including 7% of items surveyed at Walmart and 19% of items surveyed at Target—though these shortages were restricted to consumer electronics, cosmetics, and apparel.

■ Looking ahead, vessel-tracking information from our Dataworks team indicates some sequential improvement in port congestion in the second half of November. However, the amount of stranded tonnage is still historically elevated, and these incremental imports likely arrived too late to reverse upward price pressures over the holidays.

Where we find nuggets of info graphics like this …

Exhibit 1: Online Spending Growth Slowed During Black Friday Weekend and Cyber Monday

And this

Exhibit 3: Despite Some Sequential Improvement, Supply Chain Bottlenecks Are Likely Boosting Prices and Constraining Holiday Sales in Some Categories

Back TO DB and a visual from Ruskin with some reflection,

Cross market thoughts on a big Fed day …

The bond market reaction remains remarkable, and while oil certainly helped on the day, this is plainly the most surprising story of 2021 to date. Witness Q4/Q4 US nominal GDP growth tracking at a ‘gangbusters’ 11%, while inflation far exceeds target, and yet the 10y languishes below 1.5%. Since WW2 there has never been anything close to this kind of gap (see Figure 1) between nominal yields and nominal growth! Since back-end yields are a component of, and a key driver of, other components of financial conditions (FCI) notably equities, the USD, and credit spreads, it stands to reason that the less yields back up, the more heavy lifting the Fed will have to do at the front-end. In short, something has to give – either longterm rates move higher, or, the terminal rate (priced generously off the Eurodollar curve at below 1.75% in the next 5 years) has to move higher, or both!The alternative view is that i) the recovery is so mature or fragile the momentum fades without any policy push; and/or ii) the massive helicopter liquidity drop fades and so does nominal GDP, now that special quantitative measures are reeled back. Asset prices tell the story of a mature cycle, but even then, surely more than 150bs of tightening are needed to slow 11% nominal GDP growth down to a more sustainable 4%.This is especially so in an environment where asset prices are inflated by the helicopter drop and have much less private sector leverage behind it, and are therefore less vulnerable to rate increases, than a traditional asset bubble.