The ongoing waterfall of information creation produced in effort to sway the buy side view and curry favor (and business, transaction flow) continues to fill up the inboxe … I thought the following few items are worth NOT letting slip underneath the radar screen …

Barclays on 2 Dec, US Econobytes: Supply Chains

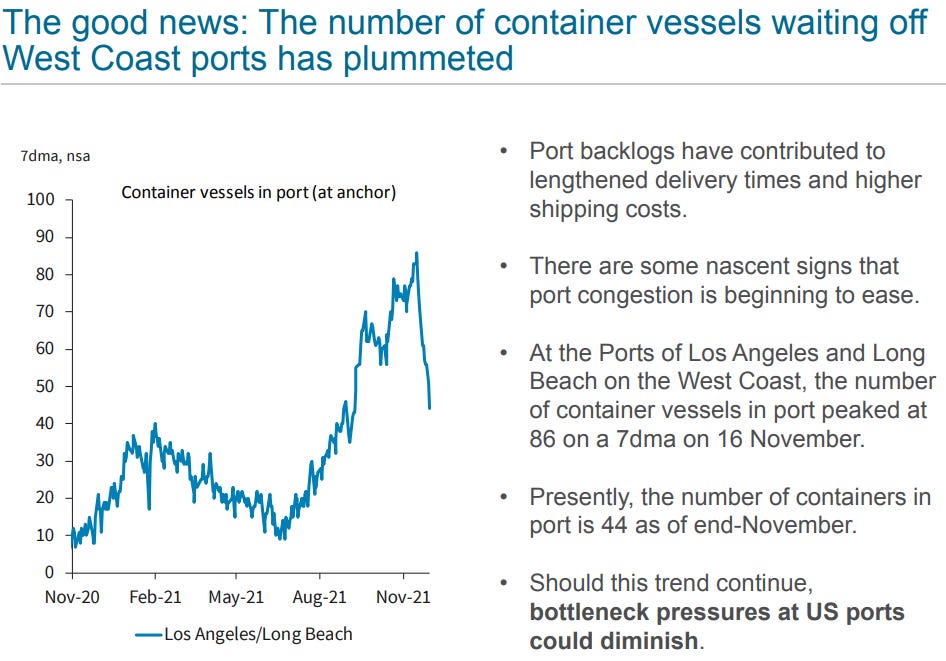

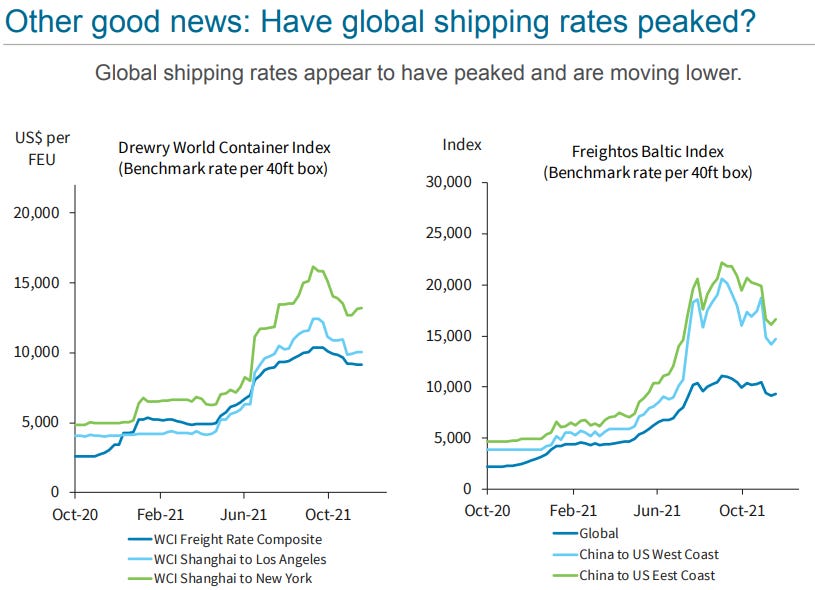

We find good news in high frequency data on container traffic and global shipping costs. We see the rapid decline in container vessels waiting to unload and falling global shipping prices as possibly leading to some easing in supply bottlenecks.

Then there’s THIS from First Boston on 2 Dec, US Economy Notes: Almost tight

The labor market is not tight yet, but it’s getting there. Nominal wage growth is strong, but concentrated in a few sectors disrupted by the pandemic, and is otherwise an unreliable indicator of slack in the first place.

The labor market puzzle is that worker shortages are widespread while employment is running far below pre-pandemic levels. In this note we try to solve this puzzle and explain how the forces that drive wages are likely to unfold in the next year or two. Counterintuitive outcomes are possible, such as decelerating inflation and wage growth just as the labor market gets tight.

Investors who extrapolate the odd extremes of short term data during the pandemic are likely to find themselves lost. Recently, inflation has shot up, jobs growth numbers have been strong, and global industrial production is finally gathering pace, while US retail sales is coming off perhaps its most phenomenal period ever. Much of this may reverse by late 2022. Wages might follow a similar pattern. At the same time, the not-tight labor market might be tight within a year.

The world will look different in six months. The question of whether the Fed will hike next summer is not as clear cut as market pricing and policymaker chatter seem to indicate.

This from Goldilocks latest Global Views: Tightening Despite Omicron, has this excerpt on the ‘flation

…The inflation news, by contrast, has turned more mixed. On the one hand, prices of durable goods such as used cars have continued to surge and we expect another outsized 0.6% increase in the core CPI this week. Moreover, Omicron raises the specter of further supply chain disruptions in the manufacturing sector, especially in Asia where Covid risk aversion remains much greater than elsewhere. On the other hand, oil prices have plunged, transport costs and shipping disruptions are starting to normalize, and the slower-than-expected 0.3% increase in average hourly earnings in November may be an early sign that wage growth is converging to the 4% pace incorporated in our 2022 forecast, not the 5-6% sequential annualized pace seen over the summer. We continue to believe that the pace over the summer was temporarily inflated by the availability of extended unemployment benefits with replacement ratios of 100% or more for low-paid workers. As a case in point, note the sharp recent slowdown in wage growth for production and nonsupervisory workers in leisure and hospitality, the lowest-paid major industry group.

Yes … NOTE the recent SHARP DECELERATION which everyone keeps talking about as IF it’s an acceleration … wage - push ‘flation which would make everyone’s re-election campaign plans much easier? GSs latest view then ends with this topical summary

… Our market views are mostly constructive, especially after the recent risk and commodity selloff. We expect the DM rate hike cycle that is now getting underway to extend for longer than discounted in the bond market, and therefore see upward pressure on intermediate and longer-term rates. We remain fairly positive on global equities because of continued above-trend growth despite Omicron, but have more neutral views on credit and broad US dollar direction. Our strongest view remains on commodities, where our strategists see the recent oil selloff as an attractive entry point into their long-standing “revenge of the old economy” theme.

Emphasis mine. All told, seems benign enough to have slid beneath radar screens. More to follow…