A few EQUITY related observations given the risk on / off again nature and strength of the force on rates trading.

Barclays (2 Dec) latest U.S. Equity Strategy: Impact of Global Supply Chain Disruption - A Deep Dive

Lower production and deliveries have already negatively affected earnings of Autos & Consumer Electronics while Apparel & Leisure Goods face the prospect of a weak holiday season. Energy & Materials and Tech Hardware are benefiting from positive pricing trends but easing of final demand could cause a reversal.

DB on (equity) POSITIONS (3 Dec),

Fastest Cut In Equity Positioning Since The Pandemic Began

…Steep cut in equity positioning back to neutral

The equity selloff since last Friday remains modest so far, in keeping with regular 3-5% pullbacks that have occurred every 2-3 months historically. However, this was accompanied by the sharpest weekly decline in equity positioning since the collapse back in March 2020 at the beginning of the pandemic. Over the week our consolidated measure of equity positioning fell from near the top of its historical range to neutral (50th percentile), the lowest this year. Overall positioning is now well below levels implied by the historically robust relationship with indicators of macro growth, which have remained elevated. The decline has been driven by discretionary investors (94th to 62nd percentile) as well as systematic strategies (66th to 40th percentile). While positioning overall is down sharply, that in large-cap US equities specifically has remained more resilient and is still within the elevated range of this year.

AND from MSs stock-jockey in chief this past weekend (6 Dec),

US Equity Strategy: Weekly Warm-up: We Didn't Start the "Fire"

A new COVID variant started the ruckus for markets, but we view that as secondary to the real culprit—the Fed's more aggressive response to the "on Fire" data. Lower valuations is our call for 2022, and the Fed's accelerated taper just brings it forward. Favor Large Cap Defensive Quality.

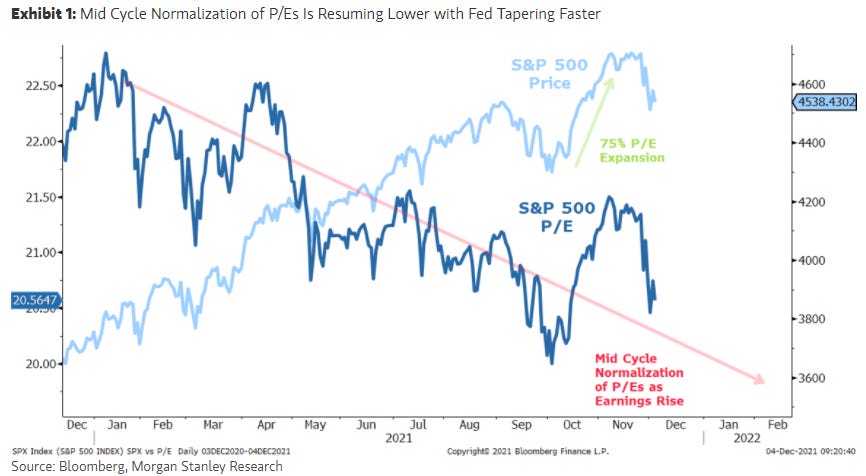

…Over the past week, markets faced 2 new curve balls—Omicron and a faster taper of asset purchases by the Fed. With respect to the new variant, we remain hopeful that this will prove to be just another wave of COVID that potentially leads to even greater immunity via vaccines and/or natural recovery from the disease. Furthermore, it appears unlikely that any new widespread lockdowns will be imposed on US soil which is the real risk to economic and business activity. While many are referring to the slowdown last summer from the Delta variant for comparison, we still believe most of that slowdown was attributable to the natural ebb of the cycle post the peak rate of change in the Spring. Finally, the recent spike in cases appears to be mainly the Delta variant and looks more like it could be a seasonal increase such as many were expecting. In other words, the severity of the sell off in equity markets the day after Thanksgiving was not necessarily due to Omicron. Instead, we think the new variant served as the trigger to end a speculative seasonal rally that was ignoring this seasonal wave along with a lot of other visible risks. Importantly, the decline over the past few weeks still leaves P/Es higher than they were 2 months ago with unfinished business, and we think this has more to do with the mid cycle transition than anything else (Exhibit 1).

…As seen in Exhibit 1, valuations began to de-rate at a more accelerated rate in early September in anticipation of the official announcement later that month—i.e. tapering is tightening for markets even if it isn't for the economy. Then, P/Es rose during October as the seasonal year end rally began as we anticipated. However, we viewed that rise as temporary before the P/E normalization would resume, likely sometime after Thanksgiving (Riding the Wave into the Holidays).

…Bottom line, the Fed is preparing to remove policy accommodation faster than what many investors were expecting due to higher inflation and a labor market that is rapidly approaching full employment—i.e., "Fire". Under such circumstances, it doesn't seem to make sense for the Fed to be buying assets any longer, especially at a pace of $1.5T per year. And while many bond market participants had started to price this accelerated taper in the past few weeks, the fact that Powell was not deterred by the growth risk from Omicron may have surprised some, leading to the sharp fall in risky assets.

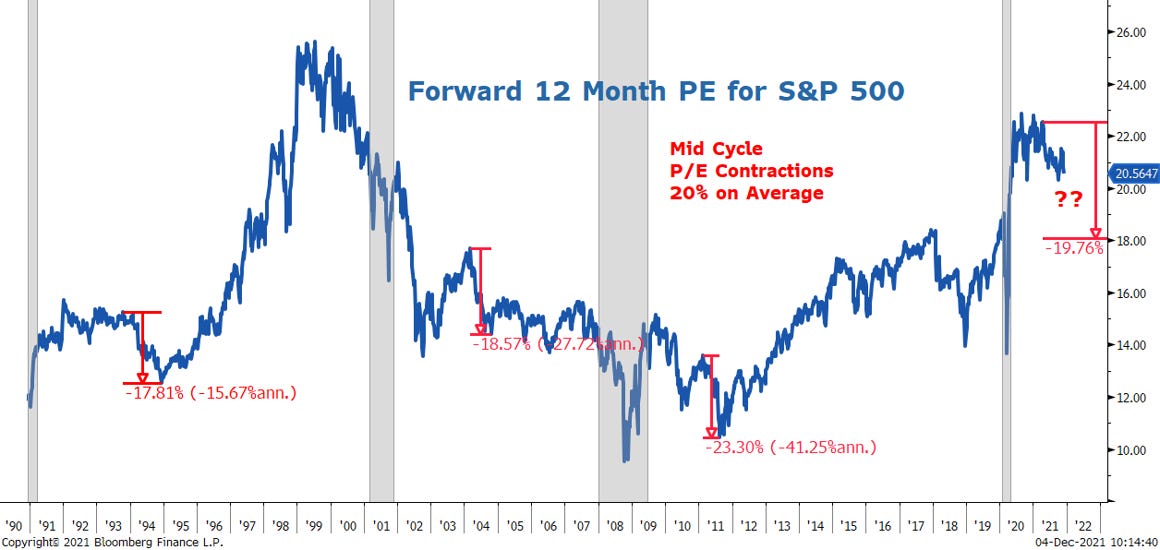

In our view, the Fed seems determined to remove accommodation more aggressively so they can be in position to raise rates if inflation rates remains higher than desired. This is exactly our "Fire" narrative which suggests valuations remain vulnerable, the key call in our well established Mid Cycle Transition narrative and year ahead outlook. In essence, the Fed's faster taper simply brings this risk forward and it's no coincidence the most highly valued stocks have seen the biggest hit over the past few weeks, a process that really began as far back as February when back end rates moved materially higher. We reiterate our view that tapering is tightening for the markets and it will lead to lower valuations like it always does at this stage of any recovery. How much lower? We forecast S&P 500 forward P/Es to fall to 18x, or approximately 12% below current levels (Exhibit 4). Obviously, for the more expensive parts of the market, that decline will be larger (Exhibit 5).

Exhibit 4: SPX P/E Still Has 12% to Fall, We Think…

…Friday's action in the equity market makes sense in the context of a very robust jobs report, factory orders report and services PMI—supportive of a more aggressive Fed path on tapering. However, a more aggressive Fed path did not translate to the Treasury market. Instead, bonds ripped with yields completely breaking down with the yield curve now down more than 80bps from its high back in March. That peak coincided with the peak rate of change in growth and the beginning of the mid cycle transition. The fact that the yield curve isn't showing any signs of bottoming yet tells us the mid cycle transition isn't over which means the de-rating isn't finished yet either (Exhibit 6).

Exhibit 6: Yield Curve Leading P/Es by One Month; So Don't Expect a Valuation Led Rally into Year End

If back end rates are falling, why are valuations falling at all with the longest duration stocks getting hit the hardest? We think the explanation lies in a few factors we have discussed in previous research, including our year ahead outlook. First, the bond market does seem to be more concerned with Omicron as a real threat to the recovery. In that context, a more aggressive Fed could be viewed as a policy mistake, hence the flattening of the curve. Also, the 10-year Treasury yield is a policy-influenced rate. As such, using it to make long term investment decisions will likely lead to over paying if you are holding the asset for long periods rather than trading it.This risk increases if inflation turns out to be higher than expected. Until recently, inflation has been an after thought, and quite frankly, something investors haven't had to worry about for 30 years. But, that risk is materially increasing now. The combination of record fiscal stimulus has led to record demand at time when the pandemic has exposed the fragility of outsourcing manufacturing and just in time inventory management systems. An aging China has also removed a source of cheap labor while asset inflation and the pandemic have led many older employees to choose early retirement. These are not easy to fix problems and suggest inflation may have finally turned the corner. That means longer duration rates could be materially mis-priced even if they don't reflect that risk today because they are policy-influenced. This would make other long duration assets mis-priced as well. With the Fed no longer able to turn a blind eye to these risks, can investors really count on unlimited support for long duration asset prices? Financial repression works wonderfully until we reach a turning point, and then it reverses quickly. This past week may be that moment of recognition for equity investors and could mean equity risk premiums (ERPs) are headed higher, and perhaps materially so, until the rates market reflects the risks of higher inflation and Peak Fed.

…Bottom line, 10-year yields don’t need to rise for P/Es to fall. The adjustment will simply happen via the ERP channel as equity investors get ahead of the inevitable rise in the discount rate they now expect over the longer term investment horizon.

Exhibit 7: The Equity Risk Premium Is Headed Higher If Investors Realize It's Peak Fed

We think our 1940s analogy may provide some insight on how markets may discount this changing dynamic…

On THAT — remember the good ole 1940s days analog, I’ll quit while I’m behind …

adding John Authers VIEW (12/8/21 here: https://archive.ph/hhGMW) with these levels from strategists who 'pretend to see the future' -- guesses compiled on 12/3rd when S&P was 4,538.

adding John Authers VIEW (12/8/21 here: https://archive.ph/hhGMW) with these levels from strategists who 'pretend to see the future' -- guesses compiled on 12/3rd when S&P was 4,538.