Good afternoon. I may be alone here in NOT posting / offering a view of FRA/OIS and of stress (more below and/or ZH HERE) and I’ll only say that a couple weeks ago we weren’t talking of this.

Perhaps it too can / will be TRANSITORY but for now, how one directs / uses this terminology may govern how one trades / invests and I’m not able to predict (guess) what can happen by days end let alone the turn of events with which the Fed will meet and consider in just about 10d, 2hrs (CME FedWatch Tool below).

‘Posting’ of updates has been and will continue to be lighter than normal due to a few ‘circumstances’ beyond my control. Truth is, we’re all better off as war on the ground heating up, truce talks falling apart before they even take place, and trading this sort of war game in real-time, is (and truthfully has always been) beyond my paygrade.

The late, great economist John Maynard Keynes always said, "When the facts change, I change my mind." Cramer has adopted the quote as his personal mantra. After all, he said one of the easiest mistakes to make is refusing to change your mind when the facts are in and you've been proven wrong. It's one of the most difficult things for the most emotional investors and traders to do, but also crucial to be a good investor.

"Swallowing your pride is never easy, but the more time you spend digging in your heels, the less you have to take advantage of the new situation and profit from it," Cramer explained…

You KNOW it’s real when I’m leaning on Cramer quotes … based on these moments in financial markets history and given known unknowns, your time best left to you to prepare and stay in the moment without ME trying to slow you down for macro musings.

That in mind, and data mining any / all messages from the yield curve (financial — 3m10y — or a more standard look at 2s10s) may be missing the mark BUT still worth absorbing **IF** you have a moment. THIS from McClellan Financial

Perhaps, then, it’s simply too soon to climb that Wall-O-Worry — here’s one of the better detailed visuals for some context (from Scott Grannis),

Watching VIX and even the MOVE and putting that aside for a moment, as it may, it’s hard NOT to think of the great stagflationary (and tax on consumption) impact on US economy with headlines like this (also from CNBC),

I’ll not bore you with an overused 08 analog but simply say that I don’t envy the Fed. And I believe in their (JPOWs) own words, he’s looking to avoid replay of that 70s analog (Swonk below) …

Hiking rates and ending QT, ultimately winding down balance sheet quick enough so they’ve got ‘ammunition’ to fight the next recessionary war, well, NEVER seems like a good idea to me.

Hiking to have room to cut.

Feel free to disagree (that is what markets are for) but in short, USTs seem to me to be pricing in these forward looking outcomes and unwilling to trade HOPE for a speedy resolution in Russia.

I’m going to quit while I’m behind, bring forward two visuals from investing.com (2s10s and 30yy — both WEEKLY) and then a few choice excerpts and links to some of the sharpest tools in the sellside shed.

2s10s WEEKLY — momentum seems to me to be in ‘no-mans’ land (inflecting towards further flattening — still have 25bps cushion),

And speaking of INFLECTING LOWER, a weekly look at 30yy suggests more of the same until / unless we hold above 2.10 (I know, you knew that level would be significant, well, it appears to ME to be coming right back into focus),

For somewhat MORE (and for those into ‘hindsight trading’, I’d also see LAST WEEKENDS update re 2s5s RED ALERT and also mentioning as it was just a week ago, we look at the visual above — 30yy which closed @ 2.285 — where I said,

With the above WEEKLY visual in mind, it DOES appear that momentum about to turn in favor OF the bond market and this will be disturbing to ALL the haters who are simply always gonna hate.

THAT is quite a bit of scratch, in the land of the BIG 01s but again, this isn’t a time for victory laps and I told ya so’s — for THAT, I’d simply point you to your inbox and/or FINTWIT for all the armchair QBs selling you whatever it is they are selling.

Rising above them all — just a few that I’ll now make time to read so as to stay on top of things — are the following, which may be of interest to you as well.

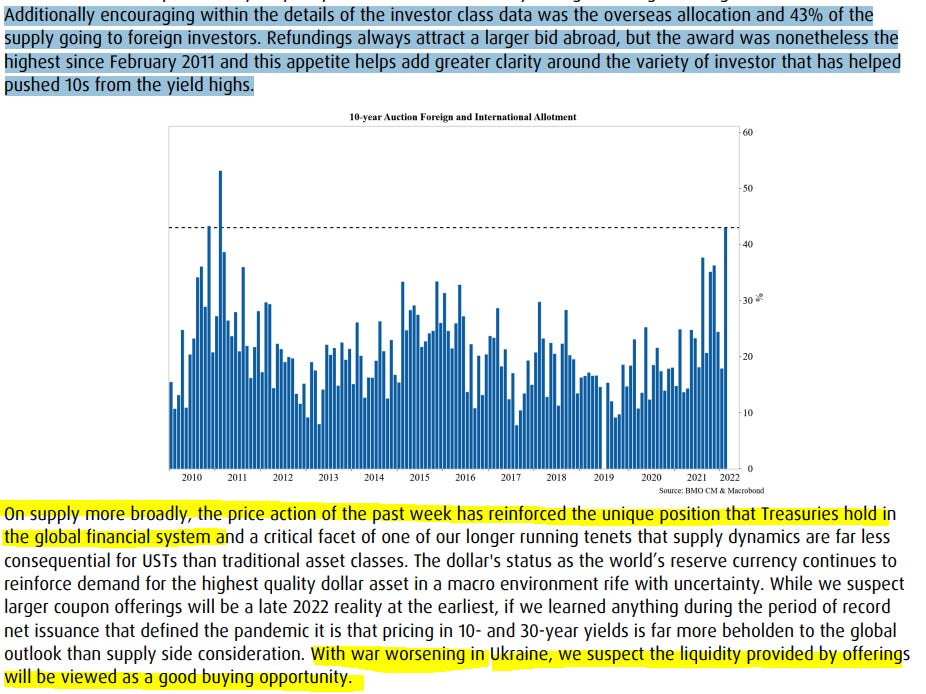

First from a large Canadian outfit which is home to THE best in the (stratEgery)biz year after year … Think FLATTENER, WATCH 10yy vs 168 (break and become a seller at 150), stagflation, curve inversion, Fed hiking into recession and/ or until something breaks … EZ risks are heightened and will impact global econ — GOT #USD and then UST?? (see/ listen TO BMOs latest — Bonds in the Time of War — and note foreigners took most 10yy in Feb (reFUNding) since 2011 via breakdown of investor class data recently released

AND so, with 10s and 30s in the week ahead there is now a lowered DIP BUYING bar and interest,

Back TO some CHARTS as there is typically some price in truth and from the shop that offered us 2s5s RED ALERT just last weekend, are this past weeks 12 charts of winter.

You’ll find word and visual salad of WTI, Brent, EZ natty, US natty, GAS (XB1), GRAINS, Lumberrrrrrrrrrr!, Industrial // HEAVY metals, Dr Copper, Gold and … Hi Ho SILVER … ?

… This bearishness has pushed the current speculator standing to the most negative level in the past one hundred and seventy-two weeks, dating back to November of 2018.

SPECS are all in and perhaps providing some of the fuel to the short-covering bid / FIRE we’ve seen … The world (and specs) are watching every move by the Fed and the CMEs got THIS HANDY DANDY COUNTDOWN CLOCK in the case you’ve forgotten

Moving along and back TO RATES and going from the great white north of Canada TO a large German shop offering an updated and yes, still quite BEARISH VIEW (initiating bearish trades 2 March 2022) including a discussion of FRA/OIS (with some very good visual CONTEXT)

… Households also have significant balance sheet buffers which can be used to cover the increased costs of living and maintain discretionary spending.

Admittedly, not all households have the benefit of higher wages and excess savings. But we believe that most households will have the benefit of at least one of the two offsets.

Households at the low-end the bottom of the income distribution are enjoying robust wage growth which, in many cases, is exceeding inflation. While total wage growth slowed in February to just 5.1%, non-supervisory (i.e. blue collar) wages were up 6.7% y/y and have largely kept up with inflation…

In other words, don’t worry, Fed sees NO reason to deter them from their current path forward … don’t worry. WORRY?

Speaking of NOT worrying and things NOT being so bad, a couple items from MS — a global markets weekly as well as the firms Sunday Start.

Global Macro Strategist | Hoping For De-escalation While we hope for de-escalation in Ukraine, we maintain a neutral investment strategy vis-à-vis government bond duration and the USD, EUR. Yield curve flatteners in the US, long inflation protection in Europe, and long USD/JPY seem the best risk-reward propositions amid heightened uncertainty.

… Interest Rate Strategy We add 2s10s and 2s30s UST curve flatteners…

MS details inflation impact on recession, this tidbit

Full stop. While HOPE generally NOT a strategy, it is what we’ve got at the moment. Furthermore, I’m typically NOT a fan of group think, having read and listened TO BMO (above), I’m going to be honest with you in that I’m having a hard time seeing a different outcome … A reasonable steepening (dip) into this weeks supply — even IF inspired by some peace breaking out — might be a DIPportunity — and there’s much more room for the (financial / 3mo10yr)curve to flatten before seriously considering recession.

Moving along TO what the firm had to offer this morning from the muni strat (Zezas) succinctly reminds us of this old Russian quote,

Weeks Where Decades Happen "There are decades where nothing happens, and there are weeks where decades happen."

– Vladimir Lenin

While I certainly don’t count myself a fan of Lenin, I have to admit that he grasped the way that changes in geopolitics can shift from a crawl to a sprint in the twinkling of an eye. He’d likely identify the actions of his native Russia over the past two weeks as one of those catalyzing moments. And while focus is rightfully on their terrible humanitarian toll, investors would also do well to understand something else this offensive may bring about: an acceleration of ‘slowbalization’, with clear implications for how global governments, corporates, and consumers allocate resources going forward.

Consider some of the apparent results of the invasion of Ukraine: A more unified ‘West’ than we’ve seen in nearly a generation… An incomplete China-Russia partnership … A potential acceleration of ‘slowbalization’ … For investors trying to look beyond the short term, that last point is crucial – we may see a rapid rewiring of the global economy consistent with slowbalization: The preferences revealed by the world’s reaction to the Ukraine crisis are compatible with the creation of economic spheres where supply and tech chains are insulated from geopolitical concerns. While this has myriad potential market implications, we see the following most clearly: Amped-up investment in defense and cybersecurity… Elevated commodity costs for a time… Elevated supply chain costs for a time…

Moving along back TO the idea of STAGFLATION and from a large British banks weekly economicreport,

The economic consequences of war … Soaring commodity prices and increased risk aversion caused by the Russia-Ukraine war imply a stagflationary shock for the global economy. We have revised our forecasts down for growth and up for inflation. While Europe looks more vulnerable than the US, and the UK is somewhere in between, China seems least exposed.

So, I’m NOT crazy and neither are YOU for thinking and uttering the STAGflationary words and expressing these fears. We’re all not alone here and Swonk of GrantThornton reiterates,

The Fed is watching and we’ve got little over 10d for further developments which is an eternity (as we know given Q4 2018).

In that I’ve now turned TO economics and fun-duh-mentals, here are a couple calendars to keep in mind as the week ahead progresses. First up is this calendar,