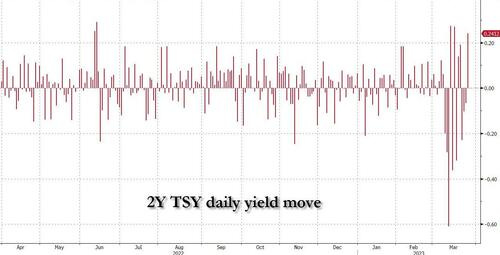

Good morning … in my haste to talk about SVB being fixed yesterday, I neglected to lead with visual of the front ends clubbing — turns OUT wasn’t even enough of a concession,

ZH: Dismal 2Y Auction Sees Record Tail As Demand Crumbles Amid Bone-Crushing Daily Swings

Furthermore, as the dust settles out on whatever what was YESTERDAY, it shall be yet ANOTHER for the history books, as detailed just below by Liz Ann

Momentum BEARISH and we’re just now approaching 200dMA (blue line @ 3.657 …

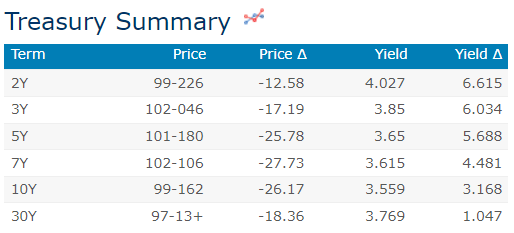

… here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are moderately cheaper led by the 5-year point (2s5s10s +5bps, due to 2y roll), cross-asset px-action indicative of consolidation and a modicum of calm. With fiscal year end in sight, JGBs saw a twist flatter (solid JGB 40y reopening with -4bp stop-thru), while the PBoC’s ¥278bn 7-day reverse repo adding new ¥96bn in new liquidity saw markets shrug (NKY +0.2%, SHCOMP -0.2%). In Europe, banking and broader risk-indices are very close to UNCH, the EURUSD +0.3% in early-trade on a day of limited catalysts. S&P futures are -4pts here at 7am, real yields leading the bear-flattening move, commodities and precious metals all waffling around UNCH levels. The SOFR strip is steepening (M3-Z3 +9bps), and 3m ESTR-SOFR basis is looking a bit improved (to -19.5 from -35 Friday). Flow-wise, most of our franchise action has been <5yr with real$ selling of 2s and shorter maturity bonds.

… Fundamentally, today’s Conference Board data should be educational as to the extent/speed at which recent banking ructions have impacted sentiment, the ‘present situation’ in particular. The theme in 2023 has been consistent softening in headline confidence almost entirely driven by a weaker ‘expectations’ component. As we show in one of our favorite charts of all-time (2s10s curve vs CB Expectations - Present Situation), a sustainable weakening in the latter vs expectations would increase our confidence in a durably steeper curves over time

… and for some MORE of the news you can use » IGMs Press Picks for today (28 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

Given the inclement weather here yesterday afternoon timed almost perfectly with walking of the dog, I thought economist (goldilocks) turned weatherman might be of some funTERtainment value,

It is still too early to have a confident view on the implications of the current banking turmoil for the US economy. Our baseline expectation is that reduced credit availability will prove to be a headwind that helps the Fed keep growth below potential despite the support from rising real income and better global growth, not a hurricane that pushes the economy into recession and forces the Fed to ease aggressively. The risks are clearly skewed toward larger negative effects, and we have moved our subjective probability that the economy enters a recession in the next 12 months back up to 35% from 25%. However, this number remains well below the consensus of 60%.

In Response to Recent Banking Turmoil, We Have Raised Our 12-Month US Recession Odds to 35%

… An immediate source of downside risk is another deposit run. The most effective way to reduce this risk would be an unlimited deposit guarantee. But that probably requires an act of Congress, which is unlikely to materialize barring a more intense crisis. Instead, Treasury Secretary Yellen has signaled that the FDIC will continue to use the “systemic risk exception” aggressively to protect all depositors (insured and uninsured) in the event of additional bank failures. At least for now, this message seems to have helped, judging from both our “big data” indicators and the statements by both Yellen and Fed Chair Powell that outflows have declined in the past week.

A more subtle risk comes from upward pressure on deposit rates…

… This is a difficult environment, not only for policymakers but also for investors. It is hard to simultaneously explain the large rally at the front end of the yield curve and the resilience of the equity market in the face of what looks like a negative growth shock of uncertain magnitude. Part of the disconnect may reflect an expectation that the credit tightening will mostly hit sectors of the US economy that are less heavily represented in public markets but still matter for monetary policy, such as commercial property and small business. But we suspect that two less benign explanations—an overly dovish view of the Fed’s reaction function and a simple disagreement between equity and rates investors about the growth outlook—also play a role. If so, expected returns on both stocks and bonds are likely to be relatively low.

Feel better now? Well don’t … Perhaps financial market participants should have stuck with medical doctor analogies?

In any case, moving along to another hot topic of how much banking stress acts like rate hikes … a large German institution recently in the news (for other reasons) is out offering this update,

In recent months we have consistently argued that a more complete view on financial conditions requires accounting for bank lending standards (see “5.1% is likely to be necessary but is it "sufficiently restrictive"?"). That view was reinforced by Chair Powell’s press conference, which noted that the evolution of credit conditions – absent from most FCIs – is likely to be critical to the economic outlook. In this report we augment the San Francisco Fed’s proxy rate to assess the impact of recent events on the Fed's policy stance.

Our augmented version of the SF Fed proxy rate provides a more complete picture of the Fed's policy stance by including a broader array of financial conditions, including bank lending standards. We find that the DB proxy rate, which incorporates these broader signals, was 6.9% in February, roughly 45bps higher than the SF Fed version. From this we can conclude that the proxy rate is materially higher once we account for the tightening of bank lending conditions that has already occurred.

Updating proxy rates through March we arrive at several additional conclusions. First, lower interest rates have not been able to fully offset the tightening of financial conditions across other metrics. Second, a 10-point tightening of the SLOOS indicators is roughly equal to a 25bps rise in the proxy rate, which is consistent with Powell's recent comments.

However, this analysis takes an "all else equal" approach, and our recent work better captured the potential dynamic relationship between bank lending conditions and broader financial conditions (see “(Credit) Crunching the numbers: A bank lending shock and recession risks"). According to that analysis, a one-standard-deviation tightening of bank lending conditions could reduce growth by an amount roughly equivalent to between two and three 25bp rate increases.

So more tightening INCREASES the chance of recession. Clearly. So says Prof Siegel,

… I was further disturbed that Powell said the Fed did not, under this dire scenario, even discuss whether any rate cuts would occur by end of the year. The bond and Fed funds futures markets are saying the Fed will have to cut at least two to three times this year given the Fed’s prediction. This denial of the possibility of cuts in the face of predicting a recession harkens back to previous Powell comments in 2021 when inflation was rapidly accelerating, and Powell said the Fed was not even “thinking about thinking about” raising rates!

Furthermore, Powell admitted a tightening of financial conditions from bank stress is equivalent to a Fed rate hike. So the Fed went 25bps when it could have gone 50. But most economists believe the current situation is significantly more serious, and one suggested upcoming bank lending contraction is equivalent to 50 to 150bps of hikes. The Fed is being too sanguine about the current lending contraction and needs to be more forward looking and cautious here …

… Maybe the markets will knock sense into the Fed. And I do think the Fed will be lowering rates by the end of the year and perhaps easing very rapidly.

In the meantime, I am more cautious about equities. Equities will likely struggle with recession risk rising and an overly tight Federal Reserve. Cyclical and value equities often face more pressures in that environment. If the Fed gets it, we can avoid the worst-case scenarios. But conservative positioning makes sense at the moment.

With more tightening taking place without Fed lifting a finger, a large British operation notes how,

Central banks go back to basics With data still strong, central banks have stuck to fighting inflation. We see tentative positive signs in the banking system. Equities have been resilient, and we don’t see a catalyst for a decline this week. US short rates have overreacted; imminent Fed cuts are very unlikely.

… We now expect global GDP to grow 2.7% in 2023, from our previous 2.5% o This is despite downgrading US and Europe for H2 2023, given banking problems o The upgrade is driven mainly by upside data in China and India… o …as well as a stronger than expected start to 2023 in the West

…With central bank meetings out of the way, we don’t see a catalyst for de-risking next week

At this point, the equity market is ‘less wrong’ in our view than US short rates

As the cyclicality of expansions and recessions takes on historical patterns (in a broader sense), the individuality of each cycle within these expansions needs to be addressed. Rarely do the unique qualities of the previous recession rear its head in the next one…though patterns can be broadly interpreted as they do have commonalities. In the current economic state, it has very little to do with the synthetic recession that was induced from the pandemic, but the fallout has been exacerbated by that unprecedented stimulus unfurled into the economy and markets. Since that anemic recession did not fulfill what the function of a recession is supposed to do and only exaggerated the situation, we find ourselves in, we must consider that a truer form of a recession has not occurred since the Great Recession ended in the summer of 2009…

… We don’t see an environment that is akin to the 2008–2009 period, however, it is more in that the larger banks have bolstered equity ratios and balanced risk out of necessity and regulatory guidelines …

… The state of the yield curves and historic inversions across the curve have caused massive shifts into Treasuries and money market funds. We now see money market funds standing at its all-time highest level at over $5.1 trillion.

… In conclusion, we have seen this before, but it feels new which is why this is more “vuja de” and not déjà vu. Ultimately, patience is required as we work through process, much like the five stages of grief. You must go through each stage to ultimately get to the end. Easier said than done as the markets seem to be experiencing all five stages of grief daily.

From money funds TO Treasury yields, which WolfStreet details as being ‘a mess’ … an UPSDIE to it all,

… But this interest income stimulates consumer spending. So banks are paying more, their profit margins are getting squeezed, and they’re hating it, and a couple have collapsed because they got caught ignoring the rising rates.

But for consumers with trillions of dollars in savings, money-market accounts, and Treasury bills: they’re now seeing a real cash flow for the first time in 14 years. And even though it still doesn’t keep up with inflation, it’s still a cash flow, and some of it is getting spent and is getting recycled in the economy. This is particularly the case for retirees that are often spending every dime in income they get, and this additional income is turning into additional spending.

There is a light at the end of the tunnel and once again, it is the US CONSUMER, as always … THAT is all for now. Off to the day job…

")