… HEREis what another shop says be behind the price action overnight…

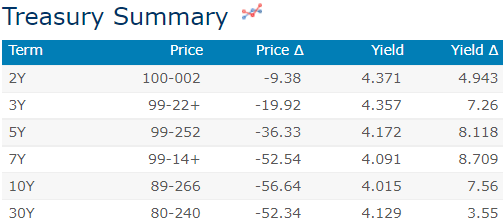

… WHILE YOU SLEPT Treasuries are lower with Bunds leading (10's +16bp) after record or near record inflation prints seen in France, Italy and within Germany (NRW). DXY is higher (+0.3%) while front WTI futures are lower (-0.75%). Asian stocks were mostly lower and down hard in China (SHCOMP -2.25%, HS China Ent -4.1%), EU and UK share markets are all in the red (roughly -0.5%) while ES futures are showing -0.7% here at 7:10am. Our overnight US rates flows saw listless flows into the German NRW inflation data when Asian real$ bought that dip (intermediates mostly). During London's AM session we saw decent selling out of Asia but good buying from EU real$. Overnight Treasury volume was solid at ~145% of average overall with 3yrs (206%) again seeing the highest relative average turnover overnight.

… UST 5yrs, daily: Bear trend broken and 5yr yields falling out of an Ascending Wedge pattern- the latter event a reliable trend reversal signal. Daily momentum still aims to lower yields while weekly momentum (as with SFRZ3 above) looking on the cusp of a new bull signal too- if ECI plays along today.

… and for some MORE of the news you can use » IGMs Press Picks for today (28 Oct) to help weed thru the noise (some of which can be found over here at Finviz).

I’ll add TO those press links something likely overlooked for good reason … iBONDS all the rage given the 9.62% buy with liquidity in govy market an issue and now, even RETAIL feelin it … Evidence this from WSJ yesterdy,

… The government’s TreasuryDirect site, the only place investors can directly purchase securities such as I Bonds and Treasury bills, this week became one of the most visited federal sites on the web, officials said, and has experienced intermittent outages. The interest rate on I Bonds is expected to drop to about 6.47% beginning Nov. 1…

… The interest rate on I Bonds is recalculated every six months. The I Bond interest rate is based on a calculation tied to the consumer-price index. The overall CPI increased 8.2% in September from the same month a year ago, according to the Bureau of Labor Statistics. There is a $10,000 annual limit per person for I Bonds, yet there are certain strategies to exceed that ceiling.

Investors must complete purchases and receive a confirmation email by Oct. 28 to ensure they will get the 9.62% rate, according to the TreasuryDirect website…

Consolation prize for those unable to secure 9.62%, this ‘stack’ comes completely free of charge? Ok, hardly making it worth 9.62% but … here are a few bullets from Global Wall Streets inbox…

First up ahead of this evenings big game,

WFC: The Economics of the 2022 World Series … The Federal Reserve is aggressively raising interest rates to tamp down inflation, which we expect to lead to a mild recession in 2023. The Houston and Philadelphia economies will not be immune to the adverse effects from a contraction in national growth.

… The 2022 World Series will kick off on Friday night with the upstart Philadelphia Phillies taking on the powerhouse Houston Astros. Both teams are entering the final leg of the playoffs with momentum. So far, the Astros have yet to lose this post-season. The Phillies have punched far above their weight with convincing wins over competition who ended the season with much better records. While clouds of uncertainty are beginning to form around both metro economies, one thing is certain: The World Series is sure to be a competitive one.

A NYY point of view down below.

BNP offers an FOMC preview: Downshift in focus, December too soon? … Ultimately, we think near-term inflation data will preclude a downshift in the pace of hikes until next year. We see the Fed raising rates by 75bp again in December, and by 50bp more in Q1 next year to hit a terminal fed funds upper bound of 5.25%.

AND a chart (or two) from CSFBs tech analyst … on 10yy, “… We would turn tactically bullish on a clear and closing break below 3.94%, looking for a move to resistance at 3.505/50%.” and they HAVE already bought 5yy, “We turn tactically bullish following the break of the uptrend from August, with scope for a move to 3.685% initially”

… Gilts had been a key source of volatility across global bonds but greater stability there wasn’t the only driver of the rally. While US central bank officials were quiet ahead of the Federal Reserve meeting next week, it undoubtedly helped they signed off with talk of slowing the pace of hikes at some stage. Traders responded by positioning for lower yields, aided by growing talk from other world policymakers of a pivot toward a rates plateau.

New Zealand’s central bank has been a key hawk, but its chief economist expressed hopes inflation has peaked. Another of the more aggressive actors, the Bank of Canada, surprised by downshifting the pace of hikes citing recession fears. That’s a break from the global mantra of quashing inflation first and worrying about the economic damage later — and one that could come back to haunt Governor Tiff Macklem…

… Central bankers are also wrestling ever harder with the conundrum of how they handle the rapidly depreciating government bonds they bought so much of over the past decade or so. The Fed is facing billions in losses on its Treasuries holdings, while the ECB is reluctant to announce a start date for the planned reduction in its portfolio.