When all else fails, toss in a RISK PARITY reference and BOOM! You’ve once again got my attention because, you know … RISK PARITY,

… DAILY RECAP

USTs and US equities idly recouped some risk-parity gains lost yesterday in the penultimate session of 2021. All manners of franchise volume and engagement remained dreadfully light, while macro news was challenging to source. Only the comments from ECB’s Holzmann, who hopes to “gradually phase out negative interest rates and unconventional monetary policy in 2022”, were market relevant amid subtle EGB under-performance (US 10s -3.4bps to Germany, Gilts out-performing). There were some sparks in the Asia EM-complex however, MES futures +1.2%, and beaten-down China ADRs saw hefty gains (KWEB +9%). This gathered some sympathy in FX-space, thought decent moves seen in Latam (BRL +2.3%, COP new 18-month high) were poo-poo’d by traders as seasonal noise (last session of the year for many local markets). USTs generally bull-flattened through the US morning, cash flow exceedingly light, somewhat offset by better futures activity after yesterday’s selling pressure after the pit-open. Open-interest data from yesterday’s session shows that the volume profile from the selloff was led by new short risk; FVH2 OI + 57k contracts (>198k added in last 5-sessions), with a general steepening bias (-13k TU, +61k TY added yesterday). Today’s retracement was more than likely a nod to tomorrow's barren calendar and abbreviated 1pm month-end session close (the BBG UST Index extensions is +0.07yrs, adjusted up from +0.06yrs yday).

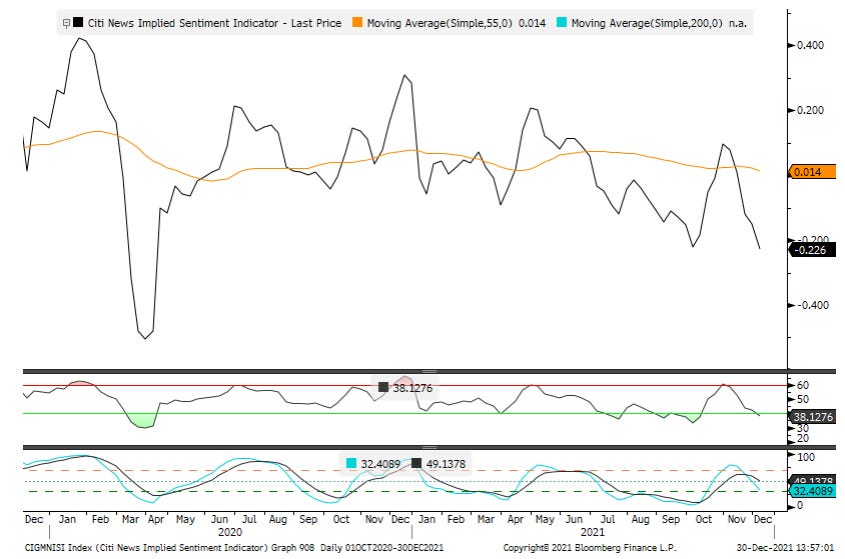

IF mere mention of RISK PARITY wasn’t enough to simply wow ya, well, lets just let some QUANT charts sink in with this attachment,

Quant - News Implied Sentiment Indicator: Threatening the ‘Delta-wave’ lows from late-September, with only the initial Covid wave lows from March-April still lower.