while WE slept: USTs weak, another 'Adult Swim'; happy "Day The Fed Nationalized The Bond Market" -A-versary ... fitting timing, given current day events ...

Good morning … unless, of course, yer a ‘basis trader’ …

April 9, 2025 at 10:07 AM UTC Bloomberg: Treasury-Bond Slump Has Traders Pointing to Hedge Fund Strategy So-called basis trade seen as a cause for selloff

… The basis trade is a strategy hedge funds use to wager on the minuscule gaps between prices of cash Treasuries and futures. They typically borrow to multiply their bets, up to 50 or 100 times the capital invested. Recent estimates put the amount of existing wagers at about $1 trillion, roughly double what is was five years ago.

Problems can arise when market turmoil upends the economics of the trade and forces investors to rapidly unwind their positions to repay their loans. It can create a cascading effect that causes yields to surge, or even worse, the Treasury market to seize up, much like what occurred in 2020…

… more on basis trade defined YESTERDAY (courtesy of Apollo) …

Good morning … unless yer a 3yr up for sale …

ZH: Dismal, 3Y Auction Has 3rd Biggest Tail On Record, Only Covid, SVB Worse

…and heaven forbid IF you have to help Uncle Sam finance national debt with today’s installment of $39bb 10yr USTs … let us hope that was is not a precursor to the far more important 10yr auction later on today which continues to … respect … 4.00% (like kryptonite to superman) …

10yy: 4.315% (TLINE, broken earlier today) seems to be of significance…

… as momentum flipped from overBOUGHT (down beneath 4%) to nearly OVERSOLD … all sorta makes sense to ME if yer askin (which I realize, yer not) … concession straight ahead perhaps to be utilized as location to cover shorts OR consider very short-term rental …

… AND before I hit send, let me be very first (I hope) to wish you a happy train-WRECK-A-versary …

Thu, 04/09/2020 - 18:20 ZH: The Day The Fed Nationalized The Bond Market (ZH, BBG)

… Until we wait here is a complete summary of everything the Fed announced this morning, when it released the details of the $2.3 trillion in loans and purchases to "support the billionaires economy", which will consist of:

Main Street Lending Program,

Paycheck Protection Program Lending Facility,

New Municipal Liquidity Facility,

Expansion of existing primary and secondary corporate bond buying facilities.

These Fed's loans and facilities are based on the additional capital the Treasury has made available under the CARES Act (see below). Of the total $454bn that Congress appropriated to backstop Fed facilities, this morning’s announcements commits $195bn, leaving the majority of funds available for other purposes - like stocks - or to expand these programs if necessary. That said, the programs the Fed announced this morning cover essentially all of the areas in which we have expected the Fed to act, so we do not expect the Fed to announce any further facilities for the time being…

April 9, 2020, 10:46 AM EDT Bloomberg: Fed Is Seizing Control of the Entire U.S. Bond Market In a dramatic move, the central bank extends its reach into munis, fallen angels and more

… I’ll quit while I’m behind … here is a snapshot OF USTs as of 711a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures mixed, DXY lower as China refrains from immediate retaliation for now … Overnight action saw USTs slump to a 110-01 trough with downside of over a full point at worst. The pullback in USTs began after a weak 3yr note auction, the results showed a slump in direct bidders, a soft cover and an elevated tail. Also driving the move was the ramping up of trade tensions, as Trump made clear that the reciprocal tariffs would (and since have) be coming into effect. The European session has seen US paper clamber off lows, as the risk tone improves a touch - potentially as China avoided announcing any fresh retaliatory measures to the latest Trump tariffs. Given all this, the next litmus test for the market in the absence of a tariff/trade driver will be tonight’s 10yr Note auction; an auction which intersects Fed’s Barkin (2027 Voter) and the Minutes from March’s meeting.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

A few techAmental thoughts / visuals to consider ahead of this afternoons 10yr auction (and I’ll come back to this well ahead of tomorrows BOND auction) …

Apr 08, 2025, 23:39 CitiFX US rates: Higher yields after term premia shock

A rethink around term premia has driven US yields higher this week after testing strong support levels at last week's close. In the process we have posted some reversal indicators. Techs suggest the move higher in yields could continue in the short term and we flag levels to watch in this update…

…10y yields 10y yields have bounced higher from 3.88% support (76.4% Fibonacci) that we tested on last week's close. Weekly slow stochastics have now crossed higher after touching 'oversold' territory.

At the moment, signs still continue to point towards bearishness in US 10s (higher yields). We are already edging past short term resistance at 4.36-4.40% (55d MA, March high). IF we close above that, next resistance is only at 4.50% (psychological level and November high). Short term support is likely at 4.22% (200d MA).

Comments here by very popular stratEgerists specifically on morphing into a ‘financial war’ are why i’m passing along this next one from Germany …

9 April 2025 DB: The end of an era George Saravelos

We have been warning about a confidence crisis in the dollar for more than a month now. Events over the last few days are in our view validating those fears. We are witnessing a simultaneous collapse in the price of all US assets including equities, the dollar versus alternative reserve FX and the bond market. We are entering unchartered territory in the global financial system. It is very hard to foresee market dynamics in coming days but we would make the following observations:

1. Dollar plumbing dynamics are being transformed…

2. The US administration is encouraging the sell-off in US Treasuries. The first order effect of current policy is of course the generation of a large negative supplyside shock that raises inflation and makes it harder for the Fed to cut rates. There is of course the bond basis trade that is being unwound. But there is something larger at play as well: a policy objective of reducing bilateral trade imbalances is functionally equivalent to lowering demand for US assets as well. This is not a theoretical consideration: the US has this week initiated trade negotiations with Japan and South Korea, with a specific reference to currency valuations. It should not be overlooked that Japan is the largest official holder of US treasuries. An implicit negotiating objective of lowering JPY valuations entails the possibility of the sale of US treasuries from the Japanese Ministry of finance. We argued two weeks ago that the whole Mar-A-Lago accord framework was flawed because it imposed fundamental inconsistencies in the desired economic objectives of the administration. We are now seeing those inconsistencies exposed in broad daylight.

3. Beware a trade war shift to a financial war. At the epicenter of the last few days' escalation is the trade war with China. As our colleagues have highlighted China appears to be maintaining the optionality on weaponizing the currency while signalling a far more supportive domestic economic stance. With a 100%+ tariff on China, there is little room now left for an escalation on the trade front. The next phase risks being an outright financial war involving Chinese ownership of US assets, both on the official and private sector front. It is important to note there can be no winner to such a war: it will damage both the owner (China) and the producer (US) of those assets. The loser will be the global economy…

Wait, what? I thought we were to NEVER sell ‘Merica short …

8 April 2025 ING Rates Spark: Is sell America Inc. now a thing?

US Treasuries are not behaving as a safe haven. They have cheapened versus the risk free rate, in a significant manner. The 3yr auction was a mess. There is now heightened nervousness ahead of the 10yr auction. This seemingly 'sell America' trade, is one that's now dominating the rising recession risk theme that typically would have pushed yields down …

… Moreover, the US 10yr swap spread has shot out to 60bp. That's a material cheapening in Treasuries versus the SOFR risk free rate curve. This is something that we had feared could have happened. That, plus the fiscal deficit plus elevation inflation expectations was the combination that we initially suggested could drive the 10yr to 5%. We never took that off the table completely, but had reverted to a more bullish tactical call for Treasuries as the recession risk became elevated. See more here ….

What's going on with inflation breakevens? Tariffs are supposed to push up prices, but breakevens have fallen. Not great as it points to macro malaise. Equities down too points to lower earnings. Lower bond yields gel with that, and we likely get more. But as we likely hit 4% inflation again in the months ahead, longer rates will be pressured back up again

Term premium discussed …

8 Apr 2025 NWM: Fed credibility and the term premium

The Fed, in assessing the market's reaction to tariff policy, will not look kindly on bear steepening. Intuitively, higher inflation risk should be consistent with a higher term premium. We illustrate an empirical model that captures 90% of the variance of our term premium proxy, and then show that the model attributes most of the recent increase in term premium to increases in the long-term U. of Michigan inflation survey variable. This mapping runs contrary to Chairman Powell’s characterization of the U. of Michigan survey as an “outlier”. Moreover, higher risk-free term premia put upward pressure on the risk premia of other assets. In this way, an overly dovish Fed can negatively impact asset valuation just as surely as can an overly hawkish Fed.

Fiscal theory suggests that the price level evolves to prevent “hard” defaults by the public sector. If debt is to be repaid, the market expects the Treasury will run surpluses to service its debt, and if it is not to be repaid, the price level will evolve so that the real present value of the debt goes to zero. In this model world, a second consecutive failure to control upside inflation looks less like an error and more like a conscious decision by an effectively consolidated Fed / Treasury balance sheet. The present situation is an acid test for the Fed’s reaction function and will materially impact Fed inflation fighting credibility, in our view.

This is def NOT our Tea Party of old …

09 Apr 2025 UBS: Tea parties become more expensive

US President Trump implemented an extraordinary tax increase on US consumers overnight. If the 104% tax increase on goods from China is not reversed, it is likely to push the US into recession more rapidly. China’s economy is negatively impacted—but the larger each round of tariffs, the less their marginal impact on foreign growth. USD 55 million of tea imported from China is subject to the 104% tax (in 1773 the UK cut tea taxes).

For years the US persuaded foreigners to exchange US government promises for valuable goods and services. That exchange is threatened—despite equities falling yesterday, bond yields rose sharply. The Federal Reserve would intervene if the bond market became disorderly (if China dumped Treasury bonds, for instance)—as the Bank of England did in the Truss debacle. A weak but orderly market does not merit intervention.

The US further increased the tax on de minimis goods from 2 May. This means that US consumers will pay taxes on small parcels. Politically a “Temu tax” visibly tells voters that tariffs raise prices, and domestic consumers pay.

Public disagreements between the people around Trump increase uncertainty about trade policy—and also about the prospect for trade deals; disagreements make it unclear what the administration’s objectives are.

‘Merica runs on small biz (and Dunkin’) …

April 8, 2025 Wells Fargo: Small Business Optimism Dims in March Economic Outlooks Unsteady Amid Tariff Uncertainty

Summary Three Makes a Trend The NFIB Small Business Optimism Index declined for the third consecutive month in March, dipping 3.3 points to 97.4. Although optimism remains above its level preceding the 2024 election, the index is now back below its historical average. Small firms’ economic outlooks continue to deteriorate, with dimming economic perceptions and worsening sales expectations as the driving force behind March’s decline. Labor quality remained small firms’ top reported problem as the worsening macroeconomic backdrop spurred a retrenchment in hiring plans. There was little evidence that tariff policy produced an increase in prices in March. However, the percent of firms planning to raise prices over the next few months reached the highest share in 12 months.

Same shop with a STAGFLATIONARY monthly outlook …

April 8, 2025 Wells Fargo: U.S. Economic Outlook: April 2025 Tariffs Throw a Spanner in the Works

Tariffs Likely Will Cause a Modest Stagflationary Shock to the U.S. Economy

The import levies that President Trump announced on April 2 will cause the effective tariff rate to jump from about 2% last year to more than 20% this year, the highest rate in more than a century.

If tariffs were to remain at their current levels, then our model simulation shows that inflation would shoot higher in the coming months, leading to a downturn in the U.S. economy.

Assuming that tariffs rates remain at current levels strikes us as a bit extreme. The Trump administration very well could reduce tariffs, at least partially, if it is able to strike deals with other countries. But the 10% minimum tariff that the president has put into effect leads us to believe that a return to the 2.3% effective tariff rate of last year in not in the cards, at least not in the foreseeable future.

We assume the effective tariff rate will recede to about 15% and remain there through the end of our forecast period in Q4-2026. This assumed 15% effective tariff rate strikes us as a reasonable balance between the current lofty level of levies and a return to pre-April 2 rates.

We look for inflation to move higher in the coming months, eroding real income growth and causing growth in real consumer spending and overall real GDP growth to dip into negative territory beginning in Q3-2025.

As growth weakens and the unemployment rate moves higher, we look for the FOMC to restart its easing cycle. Specifically, we forecast 125 bps of rate cuts between the June FOMC meeting and the end of 2025.

We readily acknowledge that uncertainty around our economic outlook remains greater than normal. We expect the Fed to "look through" the price level increase caused by tariffs as long-term measures of inflation expectations remain anchored. However, if inflation were to show signs of becoming more entrenched, then the FOMC likely will not cut rates as much as we currently envision, if at all.

Finally, THE question which needs to be addressed … and the good news IS the Fed Put likely to come back into play (?) and / or DJT starts DEALIN’ …

Apr 8, 2025 Yardeni: Is Something About To Blow Up In The Credit Markets?

The S&P 500 is now down almost 19%. It closed at 4982.77 (chart). If it falls another 1.35% down to 4915.32, it will be in a bear market. The index was up sharply at the start of trading today, but closed down 1.6% during regular trading hours after the magnitude and imminence of the Trump administration’s tariffs on US imports hit home. After midnight tonight, the US is slapping a 104% tariff on imports from China. S&P 500 companies have lost $5.8 trillion in stock market value since Trump's tariff announcement last Wednesday, the deepest four-day loss since the benchmark was created in the 1950s. Tomorrow, the drop could make the history books as the second fastest bear market since the Covid selloff.

Trump administration officials have claimed that the plunge in stock prices caused by their tariffs only really hurts the wealthy. That's not true given that 62% of Americans have money invested in the stock market (chart). At the barber shop I went to on Sunday, everyone was complaining about how much money they lost recently in the stock market, including the barber. The guy who turned on my sprinkler system this afternoon was following the market on his cell phone and getting upset that the morning's rally fizzled…

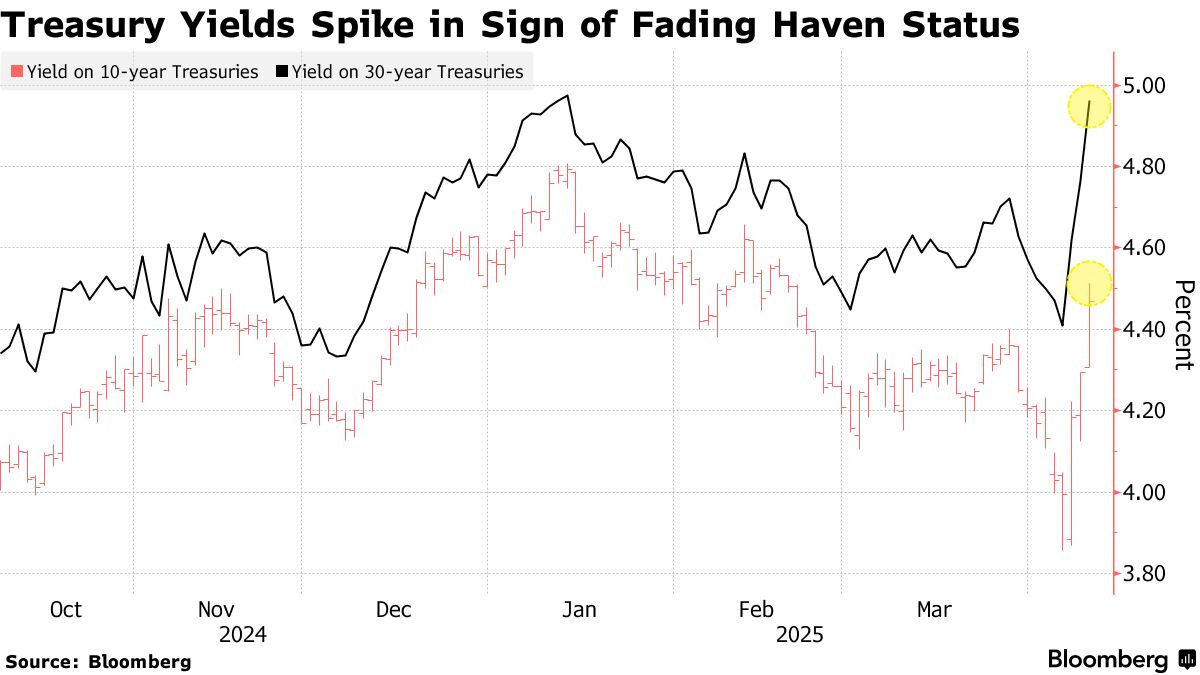

… Trump administration officials have been taking credit for the recent drop in bond yields and mortgage interest rates (chart). Unfortunately, the 10-year Treasury bond yield is up from a recent low of 3.87% on April 4 (two days after Liberation Day) to 4.36% this evening! Mortgage rates hit their highest level in over a month this week, reversing course after a period of improvement.

Why is this happening? Fixed-income investors may be starting to worry that the Chinese and other foreigners might start selling their US Treasuries.

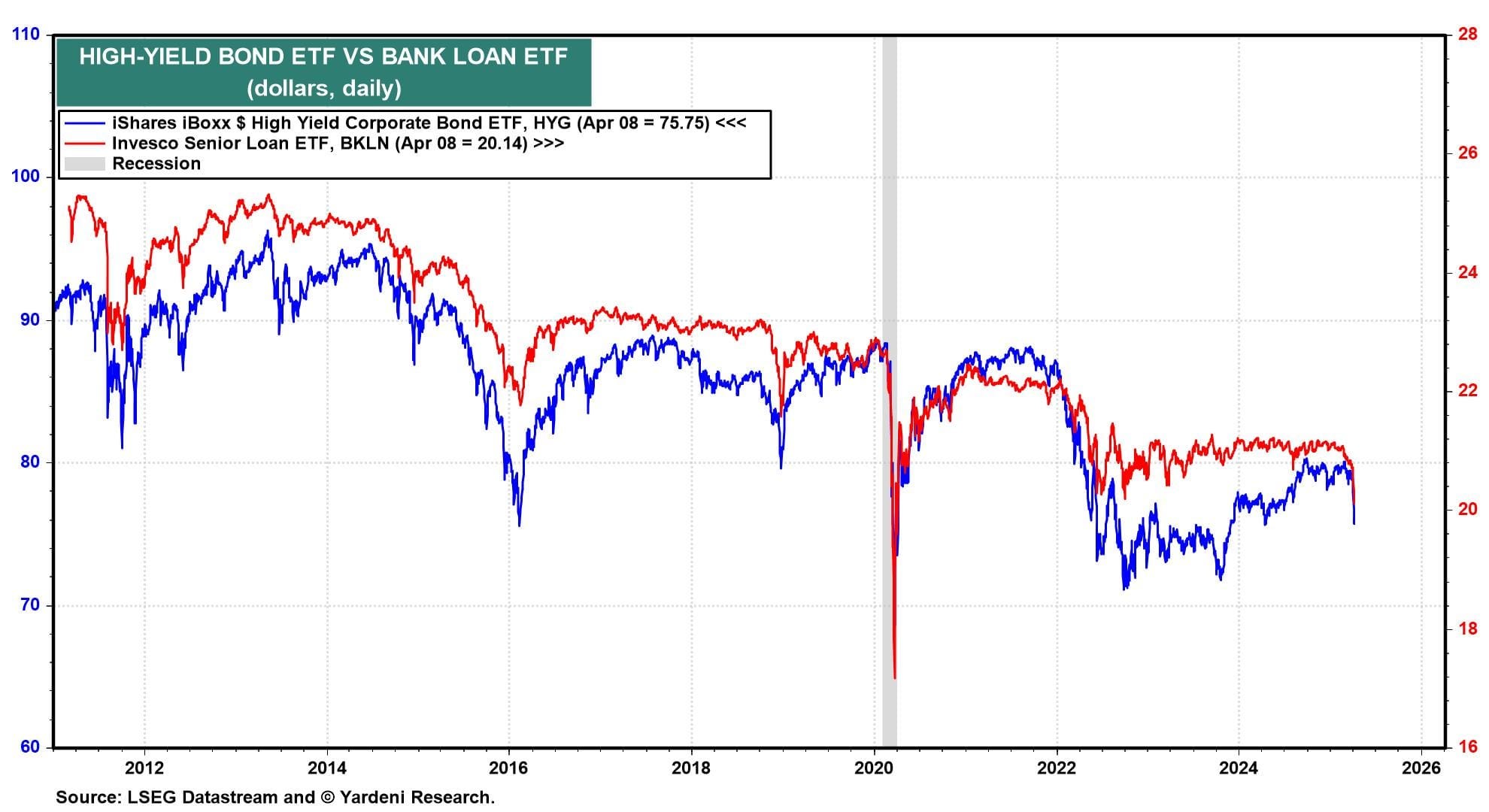

The credit markets are also starting to show signs of stress. The yield spread between the high-yield corporate bond composite and the 10-year Treasury bond is widening rapidly at the same time as the S&P 500 VIX is soaring (chart).

ETFs that invest in high-yield corporate bonds and in senior bank loans are starting to plunge (chart).

The Stock and Bond Vigilantes are signaling that the Trump administration may be playing with liquid nitro. Something may be about to blow up in the capital markets as a result of the stress created by the administration's trade war. If so, then the S&P 500 will fall into a bear market for sure.

That's the bad news. The good news is that the Fed Put will probably make a quick comeback if this happens. However, the financial markets might not recover unless the Trump administration moves quickly to negotiate trade deals. It might have to postpone the tariffs for 90 days while it is doing so.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Bonds. LONG bonds …

Bart's Charts: Long Bond – April 8, 2025 This looks like BIG TIME support for bonds. What a level.

Well, would you look at that …! Certainly looks like this long term level is going to get tested and boy does it look like some VERY STRONG support …

I’m telling you folks … sounds crazy, but just seems like Mid-May is going to be very interesting. Right …?

Anyhoo, I’m going to close my TBT position and go long TLT … no other reason than why not?

… AND from Terminal Dot Com …

April 9, 2025 at 4:00 AM UTC Bloomberg: There Isn't a Practical Alternative to US Treasuries US government debt is the world’s benchmark for a reason — and that hasn’t changed…

… Liquidity may be an ephemeral concept and impossible to measure, but it's best defined as the ability to buy or sell an asset with relative ease without meaningfully altering the price. A huge amount of volume has traded and there are few reports of inability to exit normally liquid securities. This is the key benefit of the largest financial market the world has ever seen - no other comparison exists. It's akin to the debate about whether BRICS nations could ever create a liquid alternative to the dollar.

The US may well be a dirtier shirt as the tariff debacle plays out, but we're no closer to an alternative either. The US may not be as exceptional as we once thought, but it's still way more attractive than anywhere else as an investment conduit for the rest of the world.

April 9, 2025 at 5:24 AM UTC Bloomberg: Treasuries ‘Fire Sale’ Sends Long-Term Yields Soaring Worldwide

… A vicious sell-off in what are supposed to be the world’s safest assets has investors grasping for reasons behind the steep declines in Treasuries which accelerated Wednesday…

… But there were other reasons cited for why investors were turning their back on US sovereign debt. Dislocations in a popular hedge fund trade, speculation of foreign selling of US debt and investors just ditching whatever they could in favor of cash-like shorter-dated securities as risk-assets swooned were also cited as reasons behind the bond declines.

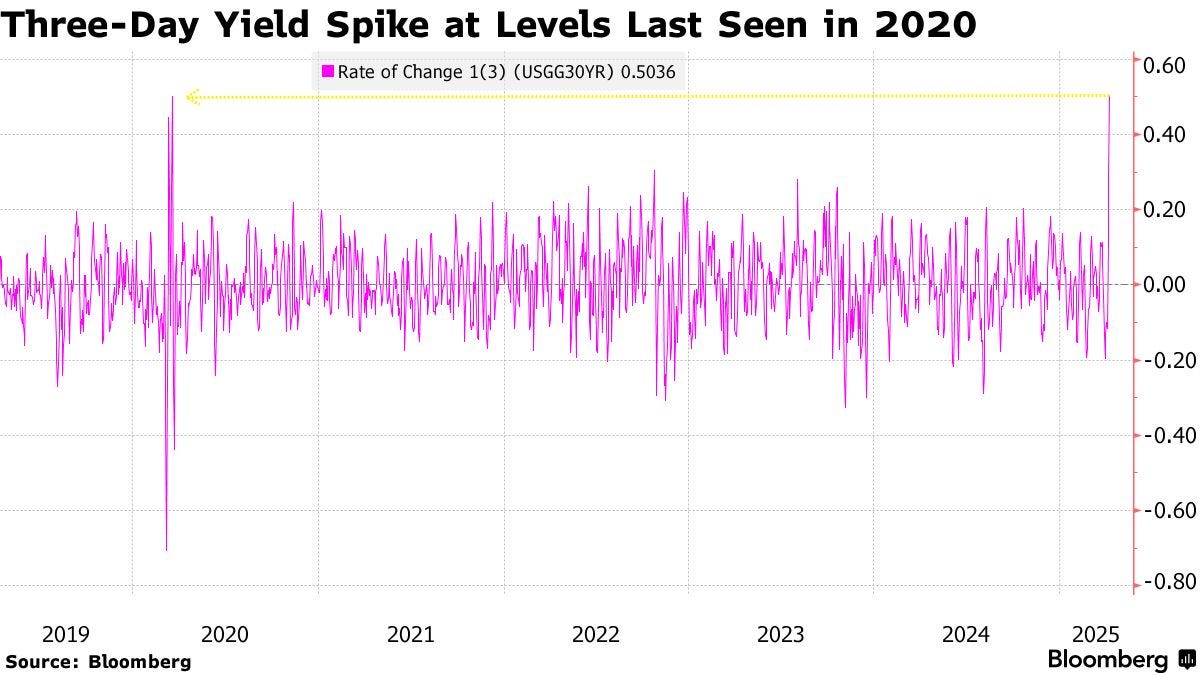

The magnitude of this week’s yield surge was reminiscent of one almost three years ago, when it became clearer to traders that a decades-long bond bull market was ending. It matched levels last seen during the market turmoil at the height of fears about the pandemic…

The yield on 30-year Treasuries surged as much as 25 basis points to a level unseen since November 2023, bringing the three day rise in yields at one point to the largest since 2020, according to data compiled by Bloomberg…

…Basis Trade Blowup Others are voicing concerns over the risks of a spike in Treasury yields of such a magnitude. The selloff was reminiscent of when a highly leveraged hedge-fund wager called the basis trade, which exploits gaps between cash Treasury prices and futures, was unwound in 2020. That caused the world’s largest debt market to seize up then.

The rise in longer-dated yields came alongside smaller gains in their shorter-term peers after a disappointing auction of three-year notes on Tuesday. That’s a sign traders are moving funds into cash-like positions.

A gauge of Treasuries’ implied volatility has soared to its most extreme level since October 2023. Currency fluctuations are the highest in two years, and the VIX index of equity volatility reached an eight-month high…

… For more on BASIS TRADE, see Apollo thoughts yesterday / HERE … back TO one more VIEW from The Terminal …

April 9, 2025 at 5:07 AM UTC Bloomberg: 104% is doubling down on dumb

… The remarkable V-shape that the 10-year Treasury yield has sketched out since Liberation Day, illustrated in this terminal chart, does lend some credence to the notion that someone is trying to push up yields deliberately (and the selloff continued in Asian trading, with the 30-year now up a remarkable 70 basis points for the week so far, and the first time it’s reached 5% since 2023):

Could China be firing a warning shot this way? Probably not. Joe Lavorgna, economist at SMBC Nikko, who served in the first Trump administration, argues that the share of US Treasury securities owned by China has been declining ever since data became available in late 2011, to 12% from 30% of total foreign holdings — and that in any case, yields are no higher than they were last week. The reduction has been very stable:

The Asian investor base has been significantly diversifying away from the US bond market for the past 14 years. Therefore, current tariff policy is not a factor.

He’s probably right about this. China is one of many factors moving the Treasury yield, and shouldn’t be singled out in the way Miran did. For China, the best response is to boost domestic consumption, as it has been trying to do for years. That will likely mean a fiscal expansion before long — which the trade war only makes more urgent…

Finally, ending on a high (or low, depending) note … POSITIONS matter …

April 8, 2025 at 8:34 PM UTC Bloomberg: Tariffs Turbocharge Collapse of Favored Hedge-Fund Rates Bet

… The upheaval from President Donald Trump’s tariffs is accelerating the collapse of a popular hedge-fund bet that Treasuries would perform better than interest-rate swaps.

The trade had been losing momentum since February, in part on waning expectations for an imminent move by the Trump administration to loosen bank regulations and allow lenders to keep more Treasuries on their balance sheets. Signs of such a policy shift would have boosted Treasuries relative to rate swaps, which are derivative contracts through which two sides agree to exchange interest payments.

But the unraveling picked up abruptly in recent days as the intensifying trade war darkened the outlook for Corporate America, leading banks to sell Treasury holdings to raise cash to meet clients’ liquidity needs, traders say. At the same time, the lenders have been adding swaps contracts to maintain exposure to interest rates in the event of a bond rally.

The result is that swaps have massively outperformed Treasuries, pushing swap rates far below Treasury yields. In the 30-year maturity, that spread reached a record low on Tuesday.

“The most violent move in the last six weeks has been that swap-spread trade coming to a violent conclusion,” said Ed Al-Hussainy, a rates strategist at Columbia Threadneedle. “This tells us that banks are now looking to raise and looking to preserve cash.”

Rate swaps are usually an exchange of fixed for floating rates. The side that receives the fixed makes money when interest rates fall, so the position acts as a way for banks to add so-called duration without owning cash Treasuries on their balance sheets…

… before signing off, SKED UPDATE — NOTHING TO BE SENT TOMORROW, Thursday 4/10th due to travels. My apologies for any inconvenience and if you require a rebate, well … have your gal call mine (where they’ll discuss how you get what you pay for and how it is that Freedom may not be free, but this ‘stack shall be!!) ….

Upon further reflection BTC is today's Tulip Bubble, and cryptos are the South Sea Bubble 300+ yrs later. IMHO! This Bond-Meltdown is ur thing safe travels mate!

https://www.zerohedge.com/news/2025-04-09/spike-yields-isnt-china-dumping-treasuries

Upon further reflection BTC is today's Tulip Bubble, and cryptos are the South Sea Bubble 300+ yrs later. IMHO! This Bond-Meltdown is ur thing safe travels mate!