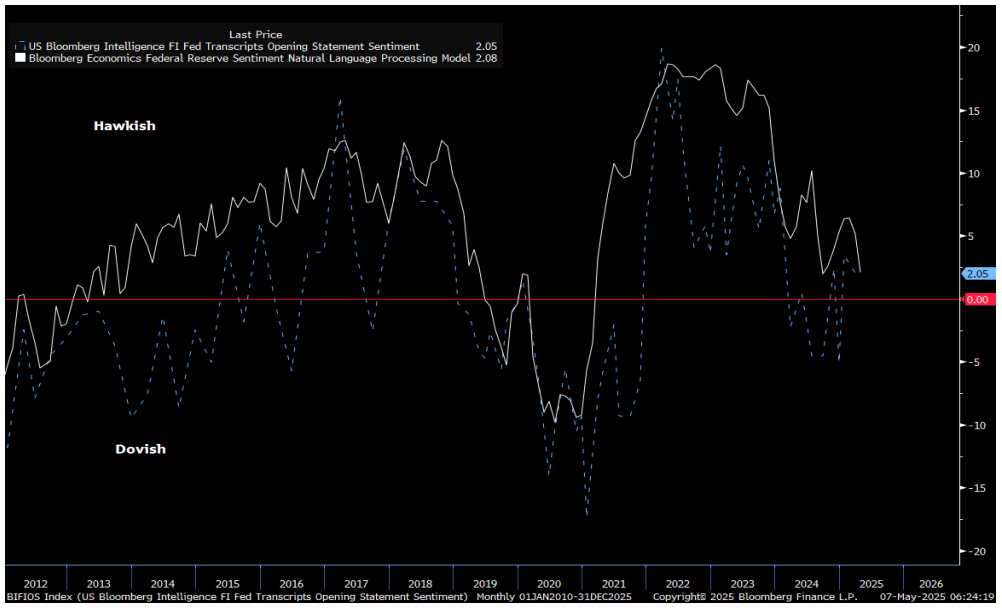

while WE slept: "USTs traded without direction overnight but...", a twist flatter; "The Taiwan effect" -Saravelos; BBG’s NLP Fed Sentiment scoring model suggests ...

Good morning … just after 6p, some good news (needed as India / Pakistan heats up) …

ZH: US, Chinese Delegations To Meet In Switzerland To Launch Trade Talks; S&P Futures Surge

… which is funny ‘cuz just a couple hours earlier, as the dust settled on the day that was, well …

ZH: Bullion, Bonds, & Black Gold Bid, But Stocks Skid As Bessent Bats Down Beijing Deal Bets

… be that as it may, some good news on TRADE was then followed by rate CUTS …

ZH: China Cuts Rates To Stimulate Struggling Economy, Just Hours After Agreeing To Tariff Talks

… AND we continue, then, to live in HOPE (and die in fear) but for now, lets focus on HOPE, as yesterday’s 10yr auction was, well, ‘stellar’ …

ZH: So Much For "Not A Safe Asset": Yields Tumble After Stellar 10Y Treasury Auction Stops Through On Soaring Direct Demand

… also of some funTERtainment value after noting ‘support’ HERE at (recently redrawn) TLINE …

Anyways, a good sign where a concession put rates up to / near TLINE support and that appeared to be ‘nuff.

That said, the 30yr auction will not happen today as Bessent makes way for JPOW so in that I missed offering a look at the 3yr ahead of auction AND as it relates closely to the official policy rate …

3yy DAILY: middle of range, ‘bout where we ‘should’ be ahead of the Fed …

… momentum more overSOLD than overbought but not an extreme, suggesting one should fade current move higher (up nearer 4%, though, gets much more interesting)

… AND, ahead of the Fed, some inputs to be considered … transitory trade deficit and a recap …

ZH:Tariff-Frontrunning Sparks Record Trade Deficit In March

ZH: Stocks Spike As Bessent Says Trade Deals Coming As Soon As This Week, Teases 'Substantial Reduction' In Tariffs

US Treasury Secretary Scott Bessent on Tuesday said during testimony before the House Appropriations Committee that trade deals may come 'as soon a this week,' and that while 'many partners have good offers,' there have been no discussions with China yet.

… Turns out, once again, they are NOT very good at the art of SURPRISE and told us early on, what to expect …?

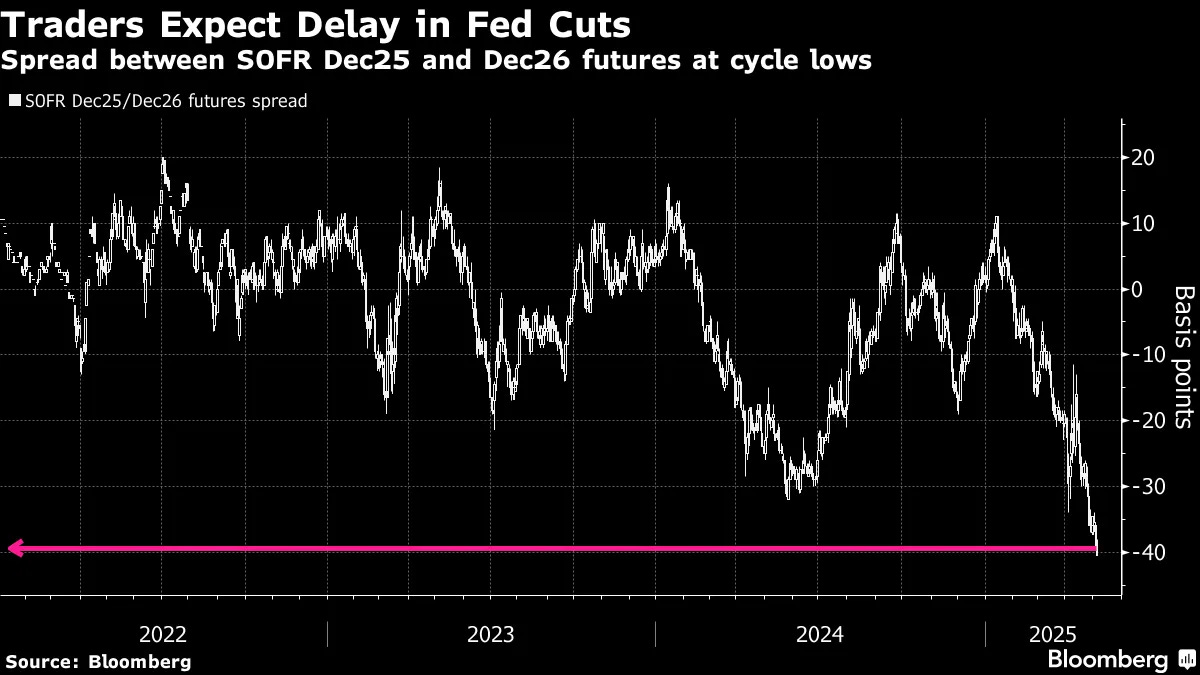

With that in mind, and still more questions than answers — FOMC will NOT be cutting rates today — see story below on TRADERS PUSHIN’ OUT CUTS — but at some point, will have to contend with rate CUT expectations (CME FedWatch Tool HERE) and I’ll simply quit while I’m behind but first … here is a snapshot OF USTs as of 701a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are twist-flattening on the US-China trade meeting announcement overnight as well as positive reception for yesterday's 10yr supply. The desk saw early front end demand from real$ and systematic accounts in 2s and 3s. 5s have noticeably cheapened up with 2s5s10s cheapening 1bp in London, before seeing some retracement into the US session. Overall price action has been characterized as orderly on a modest bearish drift in the FOMC decision, where a pause is very much expected. Volumes are in line with recent averages. S&P futures are +0.6%, DXY +0.3%, Gold -1.2%, Crude Oil +1%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US-China to start trade talks this week & PBoC announced rate cuts; FOMC due … USTs traded without direction overnight but as traders digest the latest US-China trade talk updates and China's latest monetary policy package, US paper has been coming under some modest pressure. USTs are at the bottom end of a relatively narrow 111-04 to 111-11+ band. Focus for today will be on the FOMC (expected to keep rates steady).

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Trade deficits expanding …

6 May 2025 Barclays: March trade deficit expands to another record level

The US trade deficit expanded $17.3bn to $140.5bn in March, as imports grew faster than exports. Tariff front-running effects in the advance goods balance were the main impetus for the historically large deficit today, taking over from prior gold arbitrage effects.

… Resilient Hard Data, Easier Choice - With Fed implied pricing at zilch for today’s meeting, and sharply reduced from ~38bps of easing for June (at the height of the April VaR shock) to ~8bps, the sense of urgency for Fed forward guidance has greatly reduced. Two-sided risks remain in the form of mandate sensitivity, but resilient labor market data in the form of April NFP should leave the reactive (not proactive) Fed committee tilted towards handwringing over the state of their inflation dashboard. As BBG’s NLP Fed Sentiment scoring model suggests, while the transcript of the FOMC Statement flirted with ‘dovish’ overtones in Q3-Q4 2024, Federal Reserve sentiment hasn’t fully adopted a dovish bias despite the emergency cut last year. This should give Chair Powell some wiggle room to emphasize how the FOMC’s reaction function will have to take into consideration how far each mandate is from being achieved, with the focus perhaps a bit more keen on the rise in inflation expectations (as U-Mich, Conference Board and ATL Fed time-series have turned sharply to the upside). Still, with US Financial Conditions still at levels commensurate with the ‘restrictiveness’ of late-2022 / early-2023 (as shown), Chair Powell may allude to the narrative that softening underlying services-derived inflation (as well as lower energy prices and wage pressures) may contribute to a more ‘transitory’ inflation picture…

Best in show with a look back on strong auction, bull flattening …

May 6, 2025 BMO Close: Trump's Tariffs, Powell's Pause

… Tuesday’s early choppiness ultimately gave way to a more durable bull flattening as the market took solace in the strong reception to the 10-year refunding auction. The offering cleared 1.2 bp below the WI yield at the bidding deadline and end-users took their largest share of a 10-year new-issue in over two years (91.1%). Aggressive bidding was evident among both direct and indirect participants, with each group of buyers awarded above-average shares of the issue at 19.9% and 71.2%, respectively. While the extent of domestic and overseas participation won’t be known for certain until the investor class data is released on May 22nd, the preliminary auction statistics show ongoing investor demand for US Treasuries and no clear indication of flagging foreign sponsorship at this stage. From Deputy Treasury Secretary Faulkender’s perspective, the auction “went fantastic… we are not seeing any issues in Treasury markets, and our auctions continue to go very strongly.”

With this week’s marquee supply event in the rearview mirror, investor attention has shifted to Wednesday’s Fed meeting. No change to the policy rate is all but guaranteed and with no updated SEP on offer, the most tradable information is poised to come from Powell’s press conference. We’ll look for the Chair to retain the messaging from his latest appearance on April 16th, pushing back on the prospects for a rate cut in the near-term. With the futures market ascribing 1-in-3 odds to a 25 bp cut in June and a reduction fully priced by July 30th, the Fed’s messaging will offer a key litmus test for the market’s baseline assumption that a rate cut will be delivered within the next three months. Powell expressed no urgency to cut three weeks ago, and we suspect the Chair will stay on message given the interim performance of the real economy. With the backing of a solid labor market and consumer on stable footing, Powell has sufficient cover to hold the line and retain the wait-and-see messaging.

The strong reception to the 10-year auction reinforced our assumption that there is a bullish underpinning to the Treasury market, and we continue to favor coming out of this week’s refunding process with a long-duration bias. After all, a steady Fed combined with strong auction results for 10s and 30s is a compelling environment to add duration exposure – especially in the wake of a classic pre-auction concession. The leading indicators have left us wary of a more significant slowdown in the real economy in the coming months and quarters. On the labor market specifically, the surge in year-ahead unemployment expectations within the U-Mich/NY Fed surveys combined with the gloomier outlook for hiring conditions via Conference Board Consumer Confidence are just a few details that underlie our bullish bias from here.

France on China rate CUTS …

07 May 2025 BNP China: Monetary easing to support financial stability

The monetary easing announced by China today is a follow-up of the guidelines from the Politburo meeting on 25 April, we think, and in line with our expectations.

Despite the relatively modest policy package, we view the announcement as a strong ‘policy put’ for the stock market, with funding support from the People’s Bank of China to act as a stabilization force for equities.

We think other ministries might hold similar press conferences to elaborate on specific fiscal and industrial policy measures to stabilize the economy.

We still expect a 20bp cut in the policy rate in H2, and now see another 50bp RRR cut for the rest of 2025.

FX & rates: The PBoC still prefers a relatively stable RMB against the USD. Despite the PBoC reaffirming a loose monetary stance, we expect near-term rates to stay range-bound due to the modest extent of the easing measures and profit-taking interest upon policy implementation.

The US–China trade talks will be our next key focus to see at what level tariffs will settle and the follow-up policies from China.

… an early morning Reid as well as some of the Flows to knows …

… As we hit another FOMC day, market sentiment has seen another round trip (unlike my defunct tumble dryer) over the past 24 hours, with the S&P 500 (-0.77%) falling back for a second day as concerns about the economic outlook resurfaced but with futures erasing most of these losses overnight on news that US and China will this week begin talks to de-escalate the tariff standoff. The sides announced talks in Switzerland on Saturday and Sunday, led by Treasury Secretary Bessent and Trade Representative Greer on the US side and Vice Premier Lifeng on China’s. This would mark the first substantive talks between the world’s two largest economies since the prohibitive 125% tariffs were introduced a month ago. Bessent suggested last night that the talks would focus on de-escalation rather than a big trade deal “but we’ve got to de-escalate before we move forward”. China’s Commerce Ministry called on the US to “show sincerity” in the talks. Markets have advanced on the news, with futures on the S&P 500 and NASDAQ +0.60% and +0.66% higher respectively as I type …

… There was a brief pop higher just after Europe went home that nearly took back flat for the day on Trump's quotes over an announcement that will be "as big as it gets" between Thursday and Monday. It's not clear whether this is the overnight China talks news or whether something else is in the wings. However intriguing this was, the pop soon faded. On top of that, there was more news on the retaliation front too, as Bloomberg reported that the EU were planning to hit around €100bn of US goods with tariffs if the trade talks failed.

This concern was evident across multiple asset classes. For instance, investors priced in more rate cuts from the Fed this year, with the amount expected by December up +5.1bps on the day to 81bps. In turn, that led front-end yields to fall back too, with the 2yr Treasury yield down -4.9bps to 3.78%. The 10yr yield (-4.8bps) was steady until a decent auction helped it rally and close at 4.30%. Lower yields added to a renewed decline in the US dollar, which lost ground against all G10 currencies, though this morning the dollar index (+0.30%) is on course to erase about half of yesterday’s -0.59% decline.

Even as investors were pricing in more rate cuts, inflation concerns again mounted, with the 1yr US inflation swap up +4.9bps on the day to 3.32%. That came as oil prices staged a recovery, with Brent crude up +3.19% on the day to $62.15/bbl, picking up from their 4-year low on Monday, after a major independent US oil producer predicted that US shale production will drop in the coming months. And gold prices (+2.93%) rose to a new record close of $3,432/oz, though they are -1.42% lower overnight following the news of the US-China talks…

… What is our tracker showing over the last few days? On the positive side, some modest recovery in foreign buying of US equities (figure 1). On the negative side, a continued absence of foreign purchasing of US fixed income (figure 2). What is stark in our most recent dataset is the "Taiwan effect". Many of our ETFs did not report data for Monday due to the UK bank holiday. But of those that did, those domiciled in Taiwan reported very large Taiwanese selling of US fixed income ETFs. The proceeds have been presumably repatriated onshore and coincided with the record-breaking rally in TWD of the last few days (figure 3). This fits in with similar work from our EM colleagues who have documented early signs of a repatriation of USD-based assets from Asian currencies …

In all, we agree with the view expressed in the market that the extremely volatile markets seen in Taiwan FX over the last few days are a warning shot to the self-fulfilling moves that could happen to other currencies where the institutional investor industry is left with a large overhang of unhedged USD asset positions. The JPY immediately comes to mind.

China talkin’ and cuttin’ …

7 May 2025 ING: China unveils fresh monetary policy easing package ahead of this week's trade talks

The People’s Bank of China cut its benchmark rate by 10bp and the reserve-requirement ratio by 50bp, while unveiling a series of additional measures to support the economy. The moves come ahead of China-US trade talks set to begin in Switzerland later this week

When you get to the fork in the road, TRADE it. Trade ideas …

6 May 2025 NatWEST: Trades for the Fed’s Fork in the Road This piece was originally published on Friday, May 2nd. We are republishing with a pricing update.

The Fed must triage simultaneous adverse shocks to growth and inflation. Markets now price roughly 80 bp of cuts by year end. Our view remains that the Fed will be more inclined to do nothing whilst assessing the final form of tariffs implemented and the impact on the economy. We suspect in the end the Fed will attempt to look through both shocks and allow passive tightening to return inflation the rest of the way to target.

The first implication is that the Fed will not be willing or able to deliver the rate cuts currently priced in the near-term forwards. We favor payer spreads on short tails to capture the roll up available if these forwards are not met.

We think a Fed pivot to growth would unleash a torrent of higher expected inflation potentially exacerbated by the likelihood of fiscal expansion and concerns about Fed independence. We favor buying 1y10y high strike payers as a hedge to our core view that the Fed will defend the inflation mandate before turning to growth.

India v Pakistan — couple nuclear powers — apparently one man’s view is NOT an issue …

India conducted military strikes against Pakistan, and Pakistan’s defense minister has pledged retaliation. Investors appear to be expecting a relatively contained situation. It is unlikely that global risk appetite will be affected by these events…

…US Treasury Secretary Bessent may not have blinked at China in the trade standoff, but they have definitely winked. Meetings with China are due this weekend to talk about de-escalating current tensions. It is unlikely that China will rush to deal with the US. It is in the interests of most US trading partners to wait until more of the economic damage from tariffs is apparent, thus strengthening their bargaining power.

A total of 94 out of 94 surveyed economists expect the Federal Reserve to do nothing on rates today. Erratic government policy leaves the Fed as uncertain as everyone else about the best course of action, but that will not stop the press conference being a market focus.

‘bout that there trade gap …

May 6, 2025 Wells Fargo: Trade Gap Widens to Record Amid Import Surge

Summary Businesses pulled forward needed industrial supplies and retailers stocked their shelves with consumer goods in March ahead of tariffs. April may bring a last ditch effort of firms front running tariffs, but after that net exports are set to reverse dramatically.

Dr. Bond Vigilante on the FOMC …

May 6, 2025 Yardeni: FOMC Day Minus One: Waiting For Nothing

The federal funds rate (FFR) futures market has consistently been predicting several cuts in the FFR since March 2023 (chart). The Fed did deliver three rate cuts totaling 100bps from September 18 through December 18, 2024. Since then, Fed officials have said that they are in no hurry to lower the FFR again. Nevertheless, the FFR futures market is currently anticipating two rate cuts over the next six months and four rate cuts over the next 12 months. We've been in the none-and-done-in-2025 camp since the last rate cut. We remain in that camp.

We reckoned that the economy would remain resilient. We still think so, but Trump's Tariff Turmoil (TTT) is stress-testing the resilience of the economy. It will probably slow economic growth and boost inflation. A short bout of stagflation is likely.

In the past, Fed tightening cycles caused recessions, which forced the Fed to lower the FFR (chart). So far, there has been no recession following the latest tightening cycle. Yesterday, we lowered our subjective odds of a recession from 45% to 35%, as TTT concerns are ebbing somewhat and the labor market remains robust. A recession is still possible. More likely is slower growth with higher inflation over the rest of this year. Given that likelihood, the Fed should remain on hold.

In the past, rising unemployment and falling inflation caused the Fed to lower the FFR (chart). This time, the unemployment rate remains low, and so does inflation. The former is likely to rise less rapidly than the latter in coming months. Given that likelihood, the Fed should remain on hold.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Watch what they say as well as what they are DOING …

May 6, 2025 at 8:32 PM UTC Bloomberg: Traders Bet It Will Take Longer for Fed to Start Cutting Rates By Edward Bolingbroke

Traders are betting on a slower pace of interest-rate cuts from the Federal Reserve this year, with economic resilience forcing policymakers to remain on hold for longer before easing more sharply in 2026.

Just a day ahead of the US central bank’s latest policy decision, money markets are pricing three quarter-point reductions this year, one less than at the start of April. About a half point of additional cuts are expected next year, the most priced in for 2026 at any point in the current easing cycle.

Traders will be scrutinizing comments by Fed Chair Jerome Powell on Wednesday — when the central bank is expected to keep its benchmark rate steady at 4.25%-4.50% — for clues on whether President Donald Trump’s economic policies are prompting any change in policymakers’ view on the timing for further rate cuts. Prior to the customary, pre-decision blackout period, officials urged patience, particularly with higher US tariffs set to fan near-term inflationary pressures.

Market expectations for a cut at the June policy meeting have also faded since Friday, when employment data came in stronger than economists predicted. Monday’s April ISM services data also hinted at economic strength, adding to pressures for front-end yields which are particularly sensitive to monetary policy.

“Unless something bad happens between now and June, it means the Fed doesn’t need to go,” said Kevin Flanagan, head of fixed income strategy at Wisdom Tree. Short-term yields are vulnerable given that the Fed in March had forecast two rate reductions this year, he added.

Traders are also positioning for later rate cuts in options markets. For example, the maturity date of one particular position hedging against deep cuts was just extended for the second time in a couple weeks.

Open interest data from the CME showed a considerable amount of de-leveraging and position unwinds in the front end of the curve after the April payrolls, consistent with liquidation of long positions.

In the cash market, conviction remains light as investors grapple with Trump’s trade policies and their potential impact on central bank policy. Tuesday’s JPMorgan Treasury client survey showed neutral positions remain elevated and close to yearly highs…

Finally, and for no reason at all … Little known fact …

I’ll show myself out … THAT is all for now. Off to the day job…

: r/starwarsmemes")