while WE slept: USTs regain footing after poor 20y JGB auction; rent-to-own; "This downgrade is different" -DB; USTs extend 0.076y (slightly > May avg) -MS

Good morning … especially for any / all who might have taken the ‘bait’ (30yy up over 5.00% … a ‘rent-to-own’ situation?.

Looking at the 10yy to see how IT fared yesterday and what, if any, messages one might glean …

10yy DAILY: 4.50% psychologically important level nearby …

… and on the breach, there were buyers … I’d suggest a very similar (momentum rolling over from overSOLD levels, rent-to-own)approach and that we circle back and look to WEEKLY charts by weeks end … for now we’re romancing current bearish UPtrend line and if, for some reason, we close below it (4.43), one is likely to start looking more closely …

… GOOD morning. Yesterday …

ZH: What Downgrade? Stocks & Bonds Surge Into The Green After Moody's Cut

… or was it …

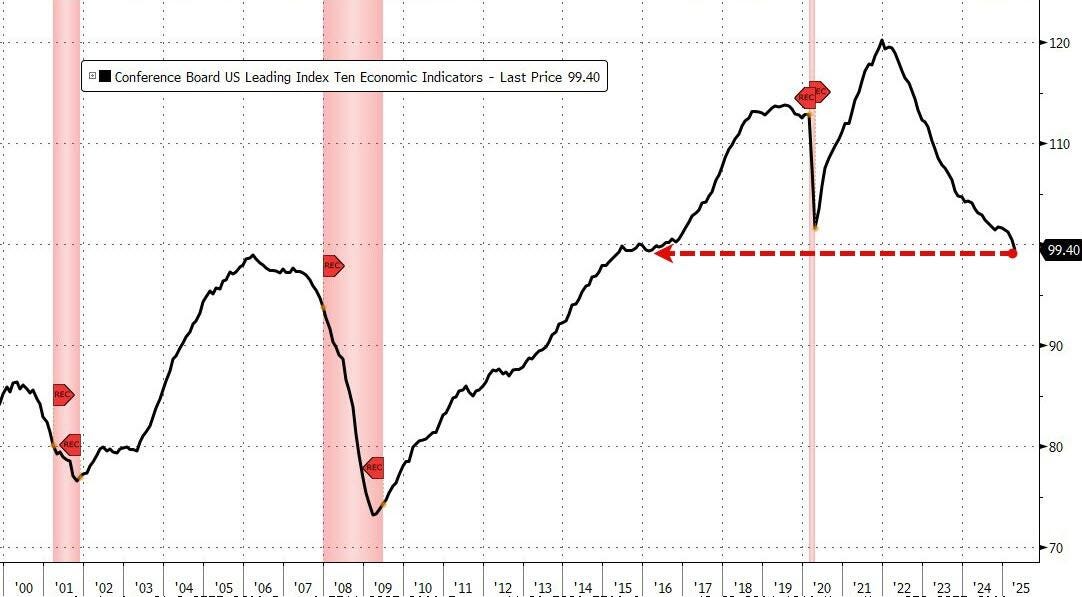

ZH: US Leading Economic Indicators Tumble Most In Over 2 Years

… That dragged the total index level down to its lowest since February 2016...

…So the economy is doomed (ish) because stocks and sentiment are down... because investors are pricing in a doomed economy...?

Perhaps the word 'leading' in this index is misleading...

… adding to uncertainty was activity in Japanese bond market overnight …

Tue, May 20, 2025 at 3:54 AM EDT Bloomberg: Japan Bonds Plunge as Weak Auction Adds to Fear Over BOJ Retreat

(Bloomberg) -- The slump in Japanese bonds worsened Tuesday after the weakest demand at a government debt auction in more than a decade highlighted worries over the central bank’s retreat from the market.

The rout drove up the 20-year yield by about 15 basis points to the highest since 2000, while the yield on 30-year bonds climbed to the most since that maturity was first sold in 1999. Yields on the 40-year tenor rose a record high in a sign of nervousness ahead of a sale of that debt next week…

…The bid-to-cover ratio at Tuesday’s 20-year bond sale — a key gauge of investor appetite — fell to the lowest since August 2012…

… watching in the case this latest ‘Truss moment’ something of an export headed to a theater near you and me, soon. More down below…

Good morning, from Jamie Dimon and CNBC …

Mon, May 19 20255:48 PM EDT CNBC:JPMorgan CEO Jamie Dimon says markets are too complacent on tariffs, expects S&P 500 earnings growth to collapse

Key Points

JPMorgan Chase CEO Jamie Dimon warned Monday about the risks of record U.S. deficits, tariffs and international tensions.

Dimon, the chairman of the biggest U.S. bank by assets, said stock markets aren’t properly representing the possibility of higher inflation and even stagflation.

Dimon also discussed his timeline to hand over the CEO reins to one of his deputies.

…“We have huge deficits; we have what I consider almost complacent central banks,” Dimon said. “You all think they can manage all this. I don’t think they can,” he said.

“My own view is people feel pretty good because you haven’t seen effective tariffs,” Dimon said. “The market came down 10%, [it’s] back up 10%. That’s an extraordinary amount of complacency.”

Dimon’s comments follow Moody’s rating agency downgrading the U.S. credit rating on Friday over concerns about the government’s growing debt burden. Markets have been whipsawed over the past few months over worries that President Donald Trump’s trade policies will raise inflation and slow the world’s largest economy…

…“I think earnings estimates will come down, which means PE will come down,” Dimon said, referring to the price to earnings ratio tracked closely by stock market analysts.

The odds of stagflation, “which is basically a recession with inflation,” are roughly double what the market thinks, Dimon added…

… AND once again, these comments help make the point that narratives FOLLOW price and not ever the other way ‘round … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures & DXY lower ahead of a slew of Fed speak, Crude choppy on Iran updates … JGBs were initially firmer, in-fitting with peers after Monday’s eventual intraday recovery from Moody’s-driven pressure. However, upside in Japan was limited into supply. But a poor 20yr outing caused JGBs to slip from 134.40 to a 138.78 base - pressure which has since pared. USTs experienced a slight bearish blip on the above auction. However, Monday’s intraday recovery remained intact for USTs overnight and the benchmark has since extended to a 110-14+ high, eyeing 110-21+ from last week as the next point of resistance. Today's speaker slate includes Fed's Bostic, Barkin, Collins, Musalem, Kugler, Daly & Hammack…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

As day came to a close, a few words from THE very best in the biz…

May 19, 2025 BMO Close: Unattended Downgrade Party

… Monday’s price action answered the question ‘what would happen if Moody’s threw a downgrade party, and nobody came?’ Stocks improved throughout the session and despite a softer open, the US rates market was effectively unchanged. As a referendum on the relevance of the rating agencies, investors are clearly siding with Bessent who commented that they are ‘lagging indicators.’ The front-end of the Treasury market outperformed with 2s rallying in outright terms – although it was a narrow range as the sector slipped back into 3-handle territory. The moves further out the curve tended toward weakness, or at least underperformance, and the curve initially steepened. That being said, the net moves were small enough and the nature of the price action subdued enough that we’re content with the characterization of the ratings downgrade as a non-event. Even as such, it was the most topical development of the session as the data calendar was noticeably blank…

…10-year yields have closed above the 200-day moving-average (4.410%) for six consecutive trading sessions, the longest stretch since February 24th. In fact, since bottoming at 4.120% on May 1st, 10-year notes have been in a bearish price channel. If the trend holds using the current parameters (using 4.120% from 5/1 and 4.386% from 5/16), 10-year yields would finish the week above 4.50%. In this context, we’ll be watchful of Friday’s close relative to 4.50% given all that might imply about the sustainability of the uptrend in yields since the beginning of the month. We see initial resistance at the 200-day moving-average of 4.410% and through there is the remnant of an opening gap from 4.386% to 4.379%. Overhead, support comes in at the post-downgrade high yield mark of 4.562% before an isolated yield peak at 4.586%.

German note recapping of yesterdays round trip in USTs and another on downgrade … this time is different and here’s why …

… We saw a large round trip in Treasuries around the news, with the 30yr yield briefly reaching its highest intraday level since 2023, at 5.035%, before paring back that move to close at 4.90%, -4.1bps lower on the day and virtually in line with where we were immediately before the news late on Friday. That recovery started shortly after the US open and continued as the session went on. It perhaps indicates the slow moving trend of overseas investors selling Treasuries but domestic investors increasing their holdings …

… In terms of that bond move in more detail, the selloff was initially very aggressive, with the 30yr yield reaching 5.035% and on track for its highest close since 2023 and actually higher for only six business days since 2007. However, that was then pared back, and it actually ended the day -4.1bps lower at 4.90%. Similarly, the 10yr yield hit an intraday high of 4.56%, but eventually closed -3.0bps lower at 4.45%. So the initial fears of the day ultimately didn’t materialise as US buyers stepped in, and at the front end, the 2yr yield fell -2.4bps to 3.98%. Overnight, yields are moving less than a basis point across the curve …

19 May 2025 DB: This downgrade is different Francis Yared

At the time, the US government was divided, with Republicans controlling the House and Democrats controlling the Senate and the White House. House Republicans forced a significant fiscal tightening on the Obama administration. Deficits declined from ~8% of GDP in 2011 to ~2.5% in 2015. Core PCE was below 2% in Q2 2011 and averaged ~1.3% over the preceding two years. Given the negative demand shock created by the fiscal tightening and low inflation, the Fed eased monetary policy and introduced Operation Twist. At the time, term premia were relatively elevated, with the ACM 10Y term premium around 200bp. This environment created the perfect storm for a UST10Y rally of more than 100bp.

This downgrade is different for several reasons.

Firstly, Republicans control all three branches of government, which should substantially reduce the probability of a forced fiscal tightening. Moreover, the US Administration has already spent substantial political capital by imposing tariffs, which should reduce the political space to implement the necessary spending cuts. In fact, our economists expect deficits to remain in a 6-6.5% range for the foreseeable future.

Secondly, core PCE is currently around 2.6%, has averaged 3.3% over the past two years and is likely to rise in the coming year on the back of tariffs. This is likely to constrain the Fed’s policy response.

Thirdly, despite its recent increase, the term premium is relatively low by historical standards as the ACM 10Y term premium is around 75bp.

From Germany to the Netherlands … narratives FOLLOW price …

The Moody’s move is more a reminder on the de-rating mood on Treasuries. Not directly impactful, but something that will linger as an issue in the coming months. In Europe, Bunds evaded the latest headwinds and we sense that ECB officials are paring back their dovishness. The Dutch parliament will vote on a controversial pension reform amendment

…Moody's acts as a reminder of risks not fully priced into Treasuries We remain bearish on Treasuries. The Moody’s move is more a reminder on the de-rating mood on Treasuries. Not directly impactful, but something that will linger as an issue in the coming months. On the tax bill, if it does get passed, it will be bearish for Treasuries, as in its current guise it has minimal fiscal deficit reducing capacity. The only silver lining is the extension of existing cuts, while optically the most expensive aspect of the bill, it in fact won’t add directly to Treasury issuance (as its already catered for in current issuance patterns). As it is some 23% of issuance is financed through bills, which is well above the preferred level of 15%. So far Treasury Secretary Bessent has decided not to push some of this out into coupon issuance, which helps to contain pressure on long dates.

A complicating factor to consider is the debt ceiling. This was automatically reinstated on 2 January 2025, and the biggest implication of this for liquidity circumstances comes from the requirement for the US Treasury to spend down its cash balances (as a cushion for the inability to engage in higher net issuance). Currently, the Treasury has a cash balance of around $600bn. As we progress towards late summer and into the autumn/fall season, the US Treasury will be in payout mode, and in that sense will tend to bolster bank reserves. But once the debt ceiling has been successfully negotiated, the Treasury will re-commence net issuance, rebuilding its cash balance and, in turn, depleting reserves from the banking system. It’s at this point that issuance pressure will really be felt by the market.

The prognosis remains for a steeper curve as the front end still has a rate cut bias to cling to US remain rates under upward pressure with the Moody’s downgrade probing 10y US Treasury yields beyond 4.5% again. The widening of Treasury yields versus SOFR swaps and the even more pronounced widening versus Bunds – in the 10y from 184bp to up to 193bp – underscore the domestic nature of the driver.

The downgrade last week turned the spotlight back on US fiscal dynamics and the question whether there is any serious intent by politicians to rein in the deficit. The US has now lost it last AAA rating, although it was not really a surprise. S&P had downgraded the US from its highest level already in 2011. Back then, however, the market reaction was quite different – the reaction was a flight to safety which ultimately benefitted Treasuries. But it was very different times.

This time bearish headwinds are more persistent and compounded inflationary concerns even if alleviated somewhat by the latest data. And away from the sentiment indicators, the overall economy and its labour market is still proving relatively resilient. Given the Fed’s “slightly restrictive” stance – as stated by Williams on Monday again – there is some room to cut rates. But there is a large degree of uncertainty around the impact of tariffs and the outlook in general. As Williams also again made clear, the Fed is in no hurry to cut rates and it may take months before the FOMC has the confidence to change its policy.

There is little data this week to change the narrative, so markets will likely look more closely at the take-up of the 20y UST auction later this week as a more timely gauge of investor appetite surrounding the US credit…

A quick recap and a note thinking way ahead to NEXT weeks month-end extension and so, in search of duration NEEDS (wants, to a lesser degree) …

US assets pare the overnight weakness on the back of the US credit rating downgrade; 30y UST yields breach 5.0% before rallying; Fed members emphasize patience; 20y JGBs underperform; UK and EU reach post-Brexit deal; mixed China activity data; DXY at 100.35 (-0.7%); US 10y at 4.447% (-3.0bp)

Following Moody's downgrade of the US credit rating on Friday, UST yields sell-off, the USD declines, and US equity futures fall overnight, but all retrace weakness during the NY session.

30y UST yields rise more than 9bp overnight, breaching 5.0%, following the credit rating downgrade and fiscal policy developments; UST yields retreat, and the curve ultimately bull-flattens (30y: -4bp).

Fed officials continue to urge patience, with Atlanta Fed President Bostic saying the Fed "will have to wait 3-6 months to see how uncertainty settles" and New York Fed President Williams saying June and July are too early to have a clear picture of the US economic outlook…

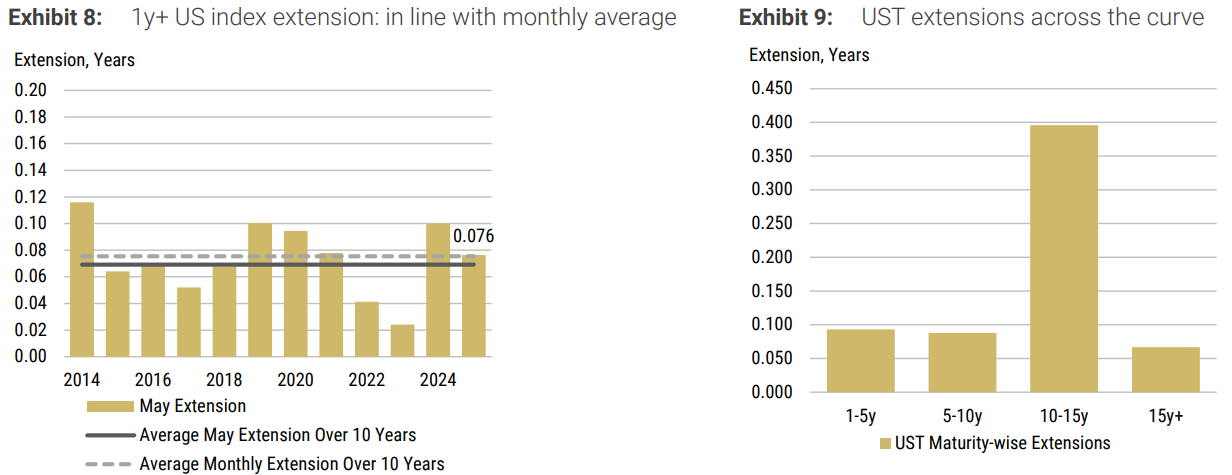

May 19, 2025 MS: Global Rates Strategy: May Index Extensions

Above-average extension in Eurogovies at 0.07y; USTs to extend 0.076y, marginally higher than historical avg in May; UKTs to extend by -0.032y, lower than monthly avg; Eurolinkers extend by 0.187y (avg 0.066y); TIPS to extend by 0.029y relative to May avg of 0.010y.

… We expect the 1y+ UST index to extend by 0.076y, compared to an average May (0.069y) and an average month (0.075y) – Exhibit 8 . A total of US$324 billion of supply (offered amount) will affect the extension and the monthly issuance of 2y, 3y, 5y, 7y, 10y, 20y, and 30y will affect the respective maturity-wise indices. No bond will be falling out of the index.

The key message from yesterday’s pontification of Federal Reserve speakers was “uncertainty”. Uncertainty about policy, uncertainty about how companies and consumers would react to that uncertainty, uncertainty about second-round effects from tariffs, and so on. The result is a wait-and-see approach from the Fed. The risk is that a reactive policy may come too late to correct any economic damage from all the uncertainty.

There are more Fed speakers today, but no reason to suppose the focus will shift. There is little economic data of note, with the Philly Fed non-manufacturing sentiment poll likely to be as subject to partisan bias as all the other sentiment indicators …

… US President Trump appeared to retreat from a position as mediator in the war in Ukraine, but suggested the two sides would start talking at once. Russian President Putin seemed less enthusiastic to talk. While a comprehensive peace would have economic consequences (via reconstruction), the global economic implications of moving towards a ceasefire are likely to be very limited.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Glass is, at best, half EMPTY? Some risks to consider…

May 20, 2025 Apollo: 10 Downside Risks to the US Economic Outlook

The trade war is making products more expensive at Walmart, student loan payments are restarting, and the Moody’s downgrade is pushing up borrowing costs for consumers and firms. The list of headwinds is growing, see below.

… and a(nother) VIEW which harkens back to and leans on Apollo view YEST (HERE) regarding overseas bidders for 30s …

May 20, 2025 at 5:00 AM UTC Bloomberg: Markets snap back, but Moody's was on to something The message to ratings agencies: You’re overrated. But the reality? Look deeper.

… The rally shows that the “End of the US” trade was overdone, but the fact remains that overvaluation got so extreme earlier this year that some adjustment was vital. US stocks have recouped only a little of the ground lost to the rest of the world:

This is in part due to the dollar…

…Slack foreign demand for Treasuries also weakens the dollar. Foreign bidders don’t participate directly in Treasury auctions, but have their bids placed by intermediaries — hence “indirect.” Apollo Group’s Torsten Slok points out that such participation in 30-year Treasury auctions has trended sharply down recently:

All else equal (it never is, but economists assume as much), higher bond yields would raise the dollar compared to other currencies…

… Finally, watching what happens over in the Far East in the case it’s bond market activity is yet another export headed here to a theater near you and I …

May 20, 2025 WolfST: Japan’s 30-Year and 40-Year Bonds Crater, Yields Spike, Huge Mess Coming Home to Roost. Yen Carry Trade at Risk

The BOJ’s QT, inflation that’s higher than in the US, an atrocious fiscal mess, a devalued yen, it all comes together.

… The 30-year JGB yield jumped 11 basis points to 3.09% at the moment, after a majestic spike, as market participants grapple with the prospect of continued and possibly hotter inflation – because hotter inflation is a way to deal with the fiscal mess at this late stage – and they’re grappling with the scary notion that the BOJ, now surrounded by inflation, will no longer be the relentless bid in the bond market that will push prices back up and yields back down. That era may be over.

Yen carry trade less attractive? Very long-term yields in this range are beginning to offer an alternative to the yen carry trade. Japanese investors can still borrow at low short-term rates in Japan but invest in long-term JGBs, instead of selling the yen for dollars and buying US securities with higher yields. Sticking to yen investments would avoid the risks and costs associated with foreign currency investments. If these high long-term yields progress, they would drain some buyers from foreign markets, such as the US Treasury market.

All these trades are risky, and a lot of things can go wrong, including sharp interest-rate moves and currency moves, but years of central bank yield repression leads to risky yield chasing…

Mr Dimon, enough pontificating, you have a phone call:

https://archive.is/TiJF3

Moody’s cuts ratings on major U.S. banks.