while WE slept: USTs incrementally firmer; 5s to 'break or hold?' (BAML); "ADP the new NFP?" (BMO); (equity)valuations matter (DB); JPM clients #GetSHORT

Normally I’d attemp to find / craft and lean on a chart of some substance with some relevance but … no need today as below you’ll note one of the more skilled TAs on Global Wall asking a question ‘bout The Belly …

…Yield tests 200wk SMA and trend line at 3.69-3.65% → Break or hold? Chart 6: US 5Y yield declined in August breaking below a short-term trend line (dashed green) and declined to test another line and 200wk SMA at about 3.69-3.65%. A break below this should usher in a decline to 3.38% / 3.16%, or wave (C) down in yield. However a reversal higher from here could lead to 4.05% / 4.35% and within the longer-term triangle pattern (black converging lines). Candle chart, 50-wk SMA, 200-wk SMA, RSI, MACD

And as YOU choose your own adventure < BREAK OR HOLD > I’m asking WHO said SELL?

If you had friends like this ‘Stack you might not need enemies?

Another reason why this ‘Stack is and should always / ONLY be ‘free’ … and a reminder that you get what you pay for? Sheesh!!

Data jolted this seemingly benign view …

ZH: US Factory Orders Dropped Again In July As Tariff Front-Running Hangover Lingers

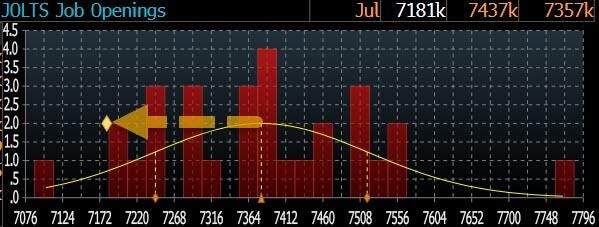

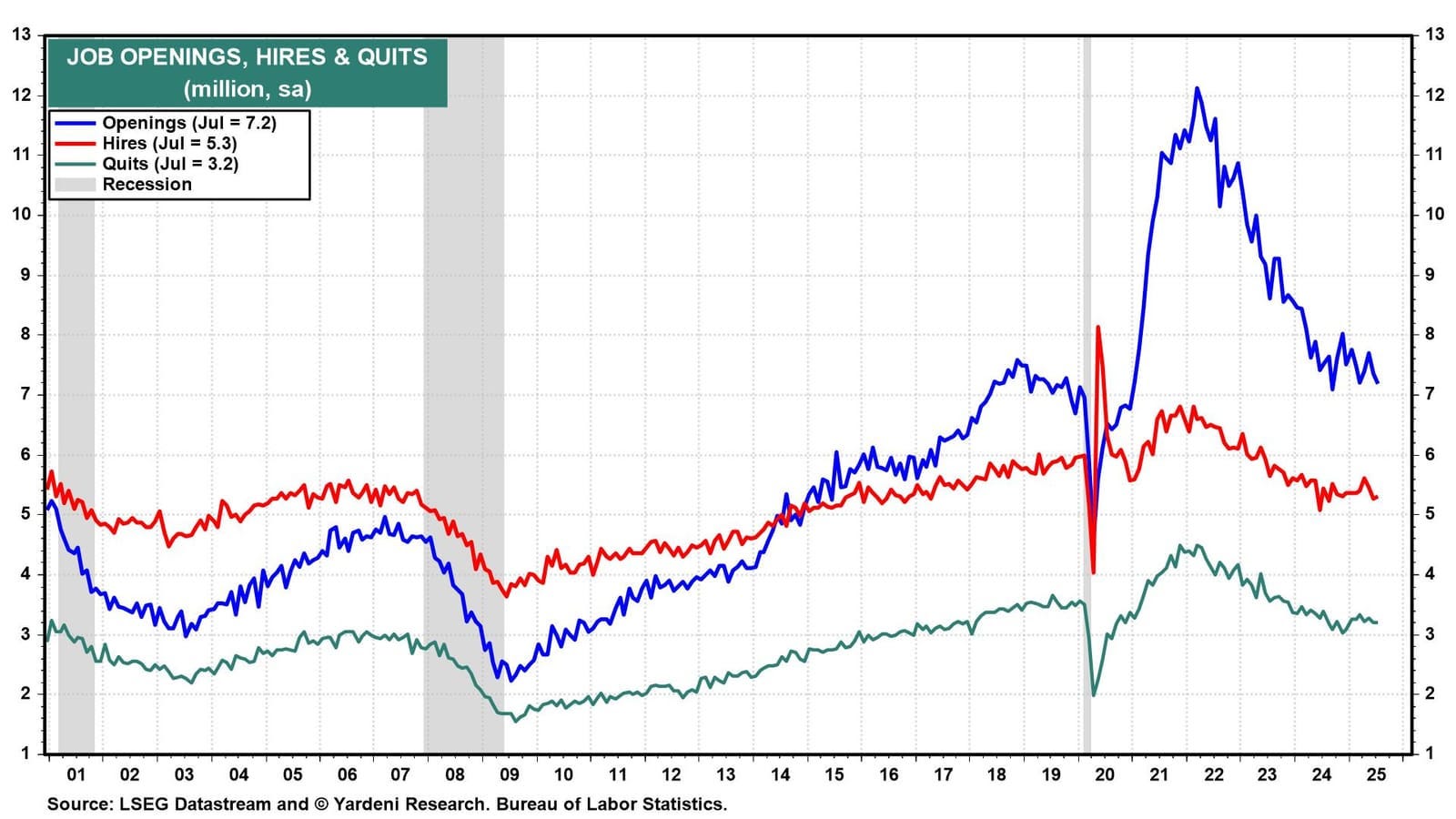

ZH: Labor Market Crosses Critical Threshold: For First Time Since 2021 There Are More Unemployed Than Job Openings

… Well, moments ago the BLS reported that in July the number of job openings tumbled by another 176K from a downward revised 7.357MM(originally 7.437MM), to 7.181MM, which not only came in far below the median consensus estimate of 7.380MM and below 28 estimates from the 29 economists polled by Bloomberg...

... but was also the second lowest going back to the covid crash, with just Sept 24 lower.

…How to make sense of this ongoing deterioration in the labor market?

It likely has to do with the DOL - which recently lost its previous commissioner after Trump fired her last month - starting to factor in the collapse in the shadow labor market, the one dominated by illegal aliens, and the replacement of illegals with legal, domestic workers which in turn is pushing the labor market into a demand-constrain imbalance. The question is how long until this appears in much weaker than expected payrolls prints - we may find out as soon as this Friday when we get the full jobs report for August, and more importantly, the full year revisions on Sept 9 just days later, which if we are correct will show another 600K-900K in jobs that were never there and were simply imagined by the Biden DOL, in the process greenlighting not only a 25bps rate cut, but potentially a jumbo 50bps... just like exactly one year ago.

Just. Like. Exactly. One. Year. Ago … UGH … onward then TO BEIGE …

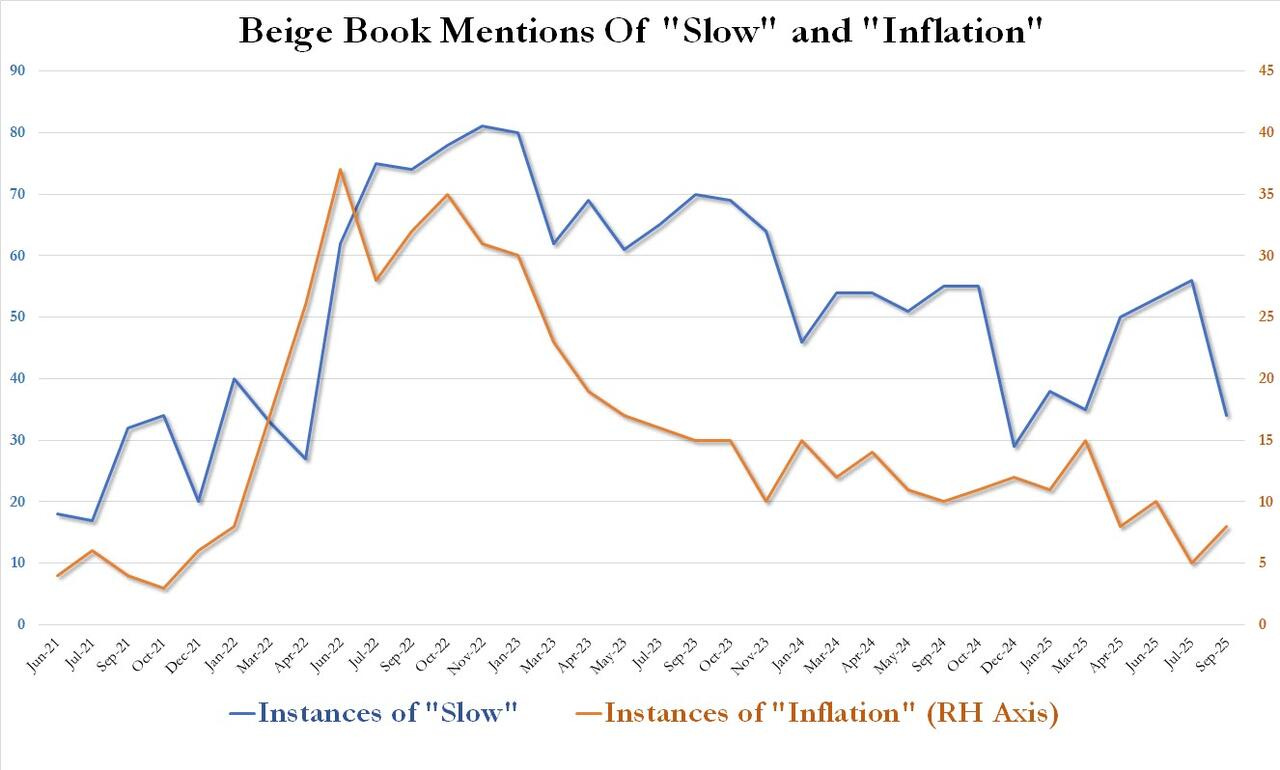

ZH: Beige Book Sees "Little Change" In Econ Activity: Notes Rising Wages As Immigrant Labor Shrinks While "Inflation" Mentions Tumble

… And finally, confirming that contrary to conventional wisdom the economic picture appears to have improved notably April, the latest Beige Book found that despite media narratives to the contrary, mentions of inflation remained near a 4 year lows, at just 8 in September, and up from the cycle low of 5 in July (effectively before the Biden inflationary explosion period) while mentions of "slow" tumbled from a two year high of 56 in July to just 34, indicating that according to the Fed respondents, neither inflation nor an economic are major concerns any more.

All of which suggests that the US economy - while hardly on fire as it was during the hyperinflationary period of Biden's admin - continues to chug along and is hardly collapsing as so many Trump foes would like to see; and it certainly is not seeing prices explode higher.

Hmmm so we’ll call it a draw? By days end, well, you know how it went …

… Worse still, construction industry quits have collapsed (because there's no better offers... or because you are an illegal and they are doing background checks)... not a good looking forward indicator for the economy...

That ugly print prompted the market to shift dovishly, now pricing in a 95% chance that The Fed cuts at the September meeting...

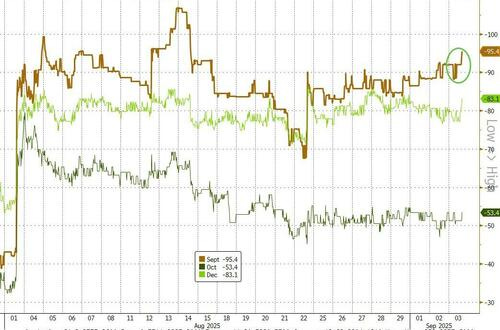

… and this is why I should have QUITs while I was behind. I’ll move on but first … here is a snapshot OF USTs as of 700a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures move higher, DXY/USTs await key US data & Fed Chair nominee Miran's hearing … USTS are flat/incrementally firmer. In a very thin 112-16 to 112-22 bound. Numerous updates on the trade and Fed front overnight, but nothing that has fundamentally shifted the narrative as we await the Senate hearing on Miran’s appointment to the Fed and then numerous US data prints, which include ADP National Employment, Jobless Claims, ISM Services PMI.

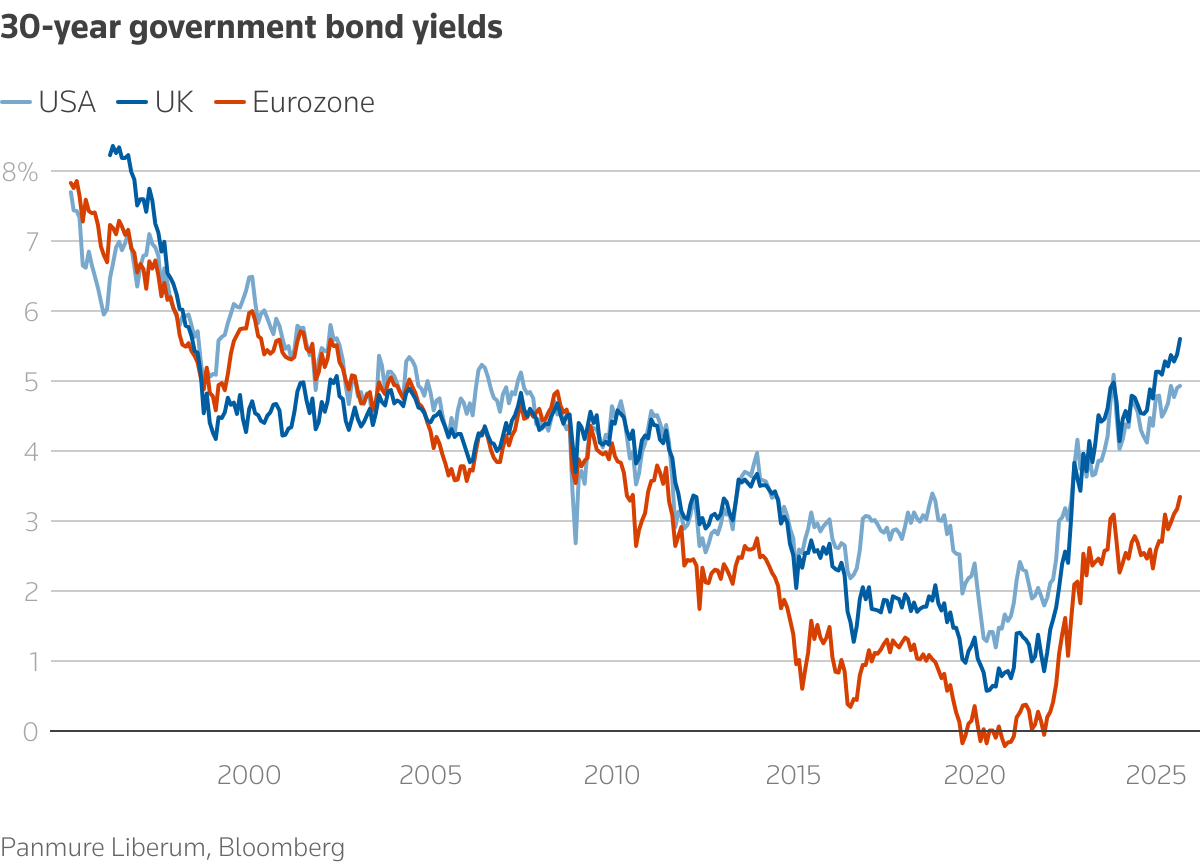

… The epicenter of market anxiety right now is spiking long-term government borrowing rates, and rescuing that market will be far more complicated than steadying an equities wobble.

Tighter monetary and fiscal policy would typically be the solution to worries about aggravated inflation and mounting public debt, but that prescription can also depress growth and potentially exaggerate a tax revenue problem.

Deftness is required. What's not required is easy money.

For decades, equity investors have talked about the so-called central bank "put" - options market parlance for a policy safety net that limits sharp stock losses with restorative interest rate cuts and liquidity injections.

Popularized during the tenure of former Federal Reserve Chair Alan Greenspan in the 1990s, the "Fed put" essentially worked as advertised. Authorities could justify easing policy with the need to tamp down excess volatility and business uncertainty or the argument that the "negative wealth effect" could harm the wider economy.

Many economists and market observers worried back then that encouraging this belief would encourage undue risk-taking, which largely proved correct in the lead-up to the 2007-2008 banking crash and global recession.

But central banks' decade-long response to that credit shock took the form of balance sheet expansion and money printing, resuscitating the idea that a policy put existed.

Not only have these actions skewed markets by essentially making Wall Street equities "risk-free" over the past decade, including during the COVID-19 pandemic, but they have also allowed the U.S. government - like many of its peers - to stack up ever more debt, not least because the central bank has been hoovering up many of the bonds.

One glance at the performance of long-term government bonds this year - and particularly this week - suggests markets are calling time on that debt buildup.

Graphics are produced by Reuters.

If so, perhaps it's time to activate the central bank put to keep debt affordable and governments solvent?

Not so fast, and not so easy.

NO IFS OR PUTS

Rising debt is only part of the problem. If it was the only issue, then lower policy rates might well work to resolve debt sustainability math.

The real worry is that unlike during much of the past two decades, we may now be approaching a "crisis" the Fed can't easily resolve.

Yield Hunting Daily Note | September 3, 2025 | EMO Rights/Sell, Distribution Changes, Out Of Nuveen, Bond Sells, Buffers

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

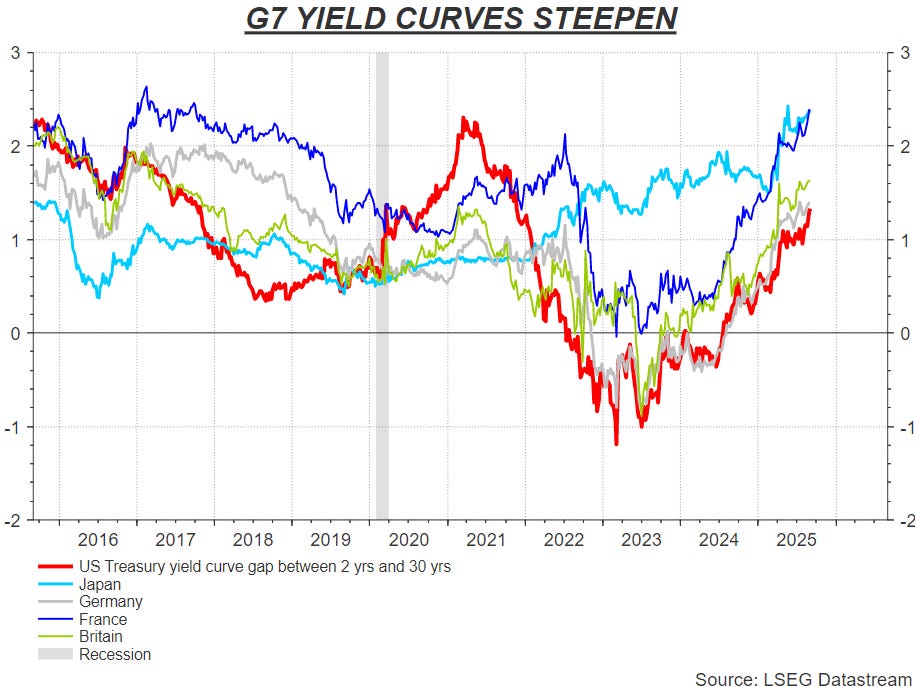

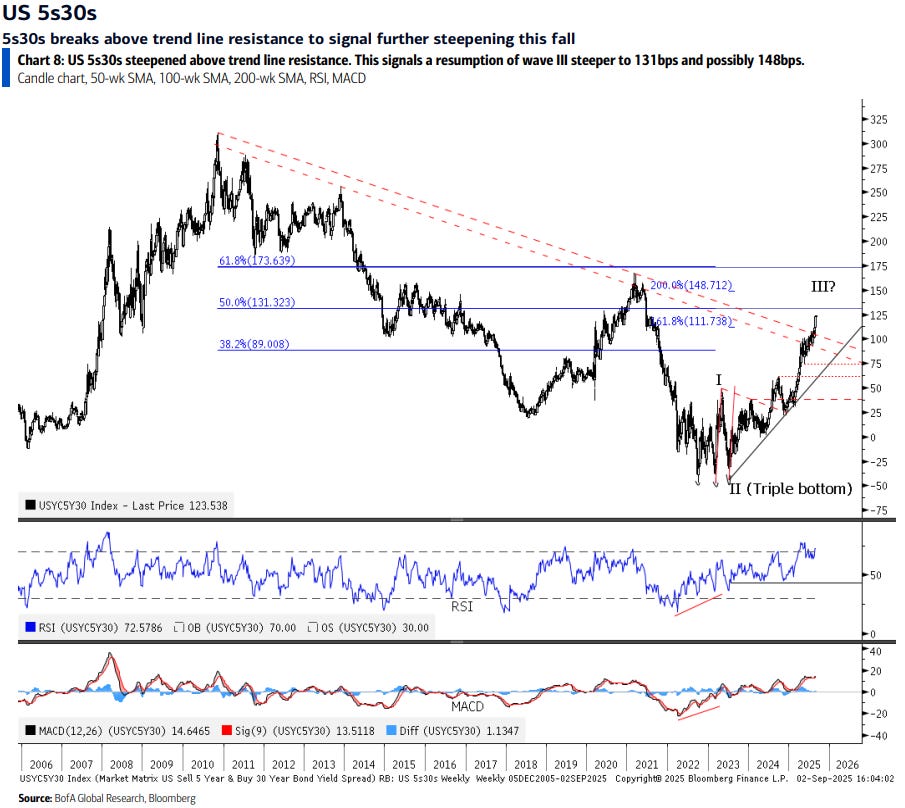

…Yields: US 5Y & 30Y test key levels, Gilts breaking higher? US 5Y yield: The August decline broke below tactical yield support, a medium-term yield support line and the 200wk SMA remain at about 3.69-3.65%. US 30Y yield: Stuck in a narrowing range of 4.82-5.01% with a breakout worth chasing coming due in SeptOct. US 5s30s: Steeper curves resumed in August and caused long term trend line resistance to break, 131bp & 148bp may be seen in 2025. Gilt 10Y Yield: September began with an upside breakout > 4.80% as upside risks are rising.

US 5Y yield: The August decline broke tactical yield support, but medium-term yield support from a trend line and the 200wk SMA remains at about 3.69-3.65%.

US 30Y yield: Stuck in a narrowing range of 4.82-5.01% with a breakout worth chasing and coming due in September-October.

US 5s30s: Steeper curves resumed in August and caused long term trend line resistance that began in 2011 to break. 131bp & 148bp may be seen in 2025…

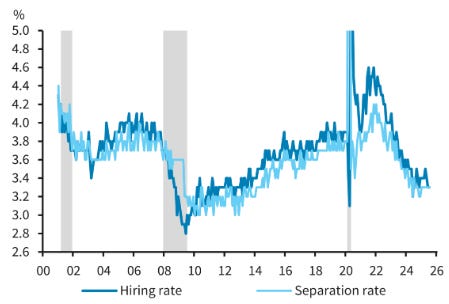

Job openings declined to 7.2mn in July from 7.4mn in June, a second straight drop. This came alongside constant labor market turnover relative to June, represented by constant hiring and separation rates. Today's data will not have any material impact on the Fed going into the September meeting.

…July's JOLTS release does little to change the FOMC picture Today's JOLTS readings did not alter the picture for the labor market, which remains on a gradual slowing trend, and little change in turnover. This release is also somewhat backward-looking, as it refers to the labor market situation at the end of July. For these reasons, we doubt that the latest JOLTS estimates will have a significant effect on the Fed's overall policy outlook. The August employment report, due this Friday, offers a more up-to-date view on the state of the labor market. At present, we expect the FOMC to gradually cut rates, with two 25bp cuts this year, in September and December. The committee will likely be keeping an eye on upcoming prints to detect any signs of deterioration in labor market conditions.

According to the Beveridge curve, a drop in labor demand (as measured by the job opening rate) would likely come at the cost of larger increases in the unemployment rate than occurred earlier in the expansion. However, reductions in immigration flows are likely also to moderate labor supply growth, muting the effect on the unemployment rate. These risks will keep the Fed attentive to labor market developments.

Figure 3. The gap between the hiring rate and the separation rate closed in July after running at around 0.1pp or greater in prior months

We may know whether Governor Cook can stay in her job (at least for now) as soon as Friday and likely no later than next week, in advance of the September FOMC meeting on Sep 16-17…

…If Cook is sidelined and market reaction remains muted, we wonder if it could embolden the president to find cause to remove other Fed governors. In that scenario, we see the threshold Senate confirmation as the ultimate check to the president's ability to replace governors, absent intervention by the courts.

…Treasuries are holding the range in what we’ll characterize as an all-too-familiar setup for the upcoming employment data. The one nuance worth highlighting that is unique to this particular data cycle is that the official data has been deemphasized by the recent criticisms levied against the quality of the monthly BLS payrolls figures and their tendency to be revised. Of course, revisions are not a new facet of the marquee employment report, instead it is the magnitude of the recent updates that has brought into question the methodology at the BLS. It isn’t a new criticism of the BLS and the falling response rate, although the President’s decision to release the head of the group has been accompanied by greater focus on the issue. Friday’s data won’t be any more or less reliable (i.e. revision prone) than usual; the real wildcard is how willing investors will be to trade the headlines with the normal level of conviction. Will the market quickly reverse any outsized reaction to a higher print based on the assumption that it will eventually be revised lower? We think yes.

As a litmus test for this operating assumption, we’ll be especially attuned to the market’s reaction to the ADP release for the month of August. In the past, we’ve been quick to downplay the series as it doesn’t have the strongest correlation with the corresponding private-NFP print. In the current environment, what had been ADP’s weakness has just become its strength – primarily because the recent BLS revisions brought the official data more in line with ADP. We anticipate that the resulting tone change implies that investors will respond to ADP with greater conviction; in effect, making ADP the new NFP – at least for a few months until there is further clarity, and investors see the next several months of BLS revisions. From the perspective of BLS credibility, revisions will ideally decrease in magnitude during the balance of the year and restore the market’s confidence in trading based on the official employment report…

A large German bank’s early morning markets reid-thru …

… The listening experience will be more pleasant if you're a bondholder this morning as the global selloff finally paused for breath yesterday, as weak US data meant investors ramped up their expectations for Fed rate cuts this year. The main catalyst was the JOLTS report for July, which showed that job openings fell to a 10-month low and exacerbated fears about a labour market slowdown. So that pushed the 2yr Treasury yield (-2.2bps) to 3.62%, whilst the 30yr yield (-6.5bps) saw an even bigger decline to 4.90%. Moreover, any fall in yields is going to ease some concern about the fiscal situation, which gave risk assets a lift as well on both sides of the Atlantic. So equities put in a decent performance, with the S&P 500 (+0.51%) moving back within 1% of its record high from last Thursday…

… Back to yesterday, and it had been quite a different story at the start of the day, as right after the European open, the US 30yr yield moved within a whisker of 5% again, reaching an intraday peak of 4.9997%, a full 10bps above its closing level. But those moves then unwound, as several data releases started to come in more softly than expected. That began in Europe, where the final services and composite PMIs for August mostly saw downward revisions. For instance, the German services PMI was revised down to 49.3 (vs. flash 50.1), putting it back in contractionary territory, whilst the Euro Area services PMI came down as well to 50.5 (vs. flash at 50.7).

Those moves then got further momentum during the US session, where weak data and somewhat dovish Fed commentary pushed the rally on. Most dovish was Governor Waller, who voted for a rate cut at the most recent meeting. He reiterated his expectation that the Fed should cut at the next meeting and favoured multiple cuts over the next few months. In addition to the JOLTS release, his labour market concerns got some support from the Fed’s latest Beige Book which saw seven of the twelve Fed districts report that “firms were hesitant to hire workers because of weaker demand or uncertainty”. Separately, St Louis Fed President Musalem said he expected the labour market “to gradually cool and remain near full employment with risks tilted to the downside”. And Atlanta Fed President Bostic said that he still only favoured one cut this year, but suggested that September could be in play if economic data weakened from here…

… Otherwise, the bond rally got its main push from that JOLTS report yesterday, which showed the US labour market was a bit softer than expected. Notably, the number of job openings fell to a 10-month low of 7.181m (vs. 7.380m expected). So that confirmed the message from the underwhelming July jobs report, and it added to fears that the labour market was softening more significantly. Indeed, it backed up the message from Fed Chair Powell’s Jackson Hole speech that the “downside risks to employment are rising”. That meant investors moved to price in more Fed rate cuts for the months ahead, with a 25bps September rate cut now 100% priced as I type. And in turn, yields moved lower across the Treasury curve yesterday, with the 2yr down -2.2bps to 3.62%, whilst the 10yr was down -4.4bps to 4.22%, a level it's settling at in overnight trading.

NO tariff ‘flation (yet?) …

03 September 2025 DB: Data DBrief: Not just tariff inflation

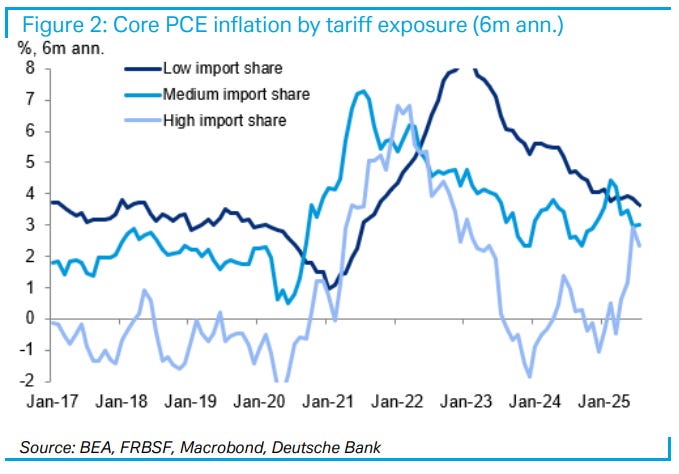

In this piece, we split up the PCE basket into those goods and services with low, medium and high import share to isolate the part of inflation that can be attributed to tariffs.

While the inflation rate for low import exposure categories is still elevated, this category is mostly comprised of rents which should continue to disinflate given the recent behavior of leading indicators. Conversely, high import exposure goods have seen inflation surge, with the largest six-month price gains since 2009 (excluding the post-pandemic experience).

For those goods and services with moderate tariff exposure, inflation remains stubbornly elevated, about a percentage point above its 2017-2019 average. While much of the upward pressure on prices does appear to be tariff related, this decomposition suggests that some of the elevated inflation may be in part due to other factors.

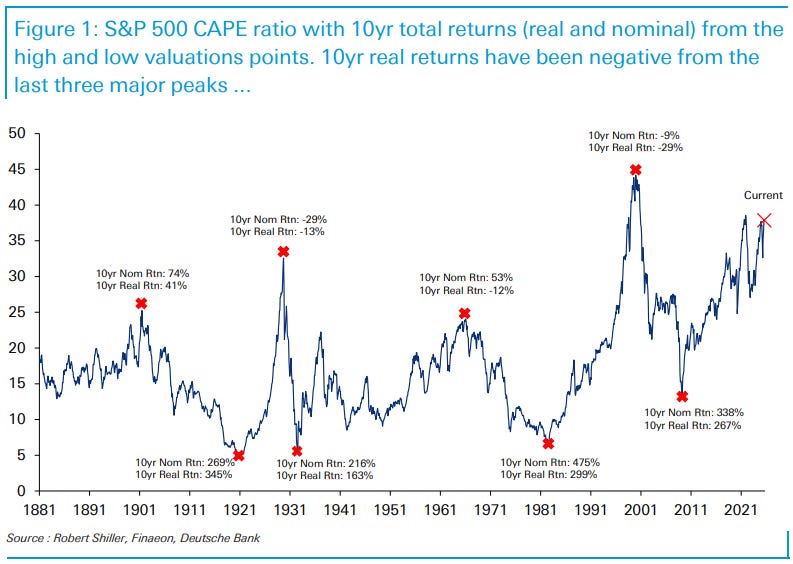

… AND same shop with a chart showing ‘valuations’ having mattered … at least as far as RETURNS go …

3 September 2025 DB CoTD: Valuations have mattered for returns...

…Looking back over 150 years, the contrast is stark: when valuations are high, forward returns are consistently weak. From the last three major valuation peaks, 10-year real total returns were all negative—a striking outcome given that US equities have historically delivered around 7% annualised real returns. Conversely, when valuations have been low, the subsequent decade’s returns have been extraordinary.

While many market participants today are less focused on 10-year horizons, the current setup underscores how central AI has become to the US equity story. The Mag-7 are driving much of today’s elevated valuations. If one believes we’re entering a genuine paradigm shift—beyond anything seen in the past century and a half—then the outlook for long-term returns could still be constructive. But you are taking a big position beyond what has already been 150 years of US equity market dominance.

A key distinction versus the 2000 bubble is that today’s valuation extremes are largely concentrated in the US. Other G7 equity markets sit at more moderate valuation levels. However, they lack the same AI exposure that makes the US narrative so compelling to many…

3 September 2025 ING Rates Spark: A Beige Book that smells a tariff stutter

In the US, the Beige Book is quite the sobering read - littered with tariff risk talk and at best flattish activity. Shaping up to be quite the week, with the pivotal upcoming payrolls to cap it off. In the eurozone, back end euro rates could come down a notch if US jobs data were to harm global risk sentiment, but the front end has a much higher hurdle to move …

… ok ok so maybe NOT a great Apocalypse Now related note but still … great clip.

September 3, 2025 MS: September 2019? Not So Fast, My Friend | US Rates Strategy

Repo market concerns have resurfaced, but fears of a '19-style funding squeeze are overblown given still-abundant reserves and foreign bank cash waiting to be deployed. With funding already priced for stress, we think staying long SERFFV5 offers compelling value amid downside risks to September tax receipts.

Key takeaways

Recent firmness in repo rates has led some to ponder whether funding conditions in September will resemble those from six years ago, when repo markets ceased to function.

We think market expectations for funding over the months ahead are overly pessimistic, especially when compared to where funding realized in 2018-2019.

Reserves are abundant; elevated FBO cash implies a portion of reserves will eventually be deployed, when repo rates are more attractive relative to IORB.

Tariff cost impacts on margins and R&D expensing/bonus depreciation included in the OBBBA pose meaningful downside risk to September corporate tax receipts.

With markets priced for '18-19 conditions, we suggest investors stay long SERFFV5; current levels offer an attractive risk-reward for lower implied funding, in our view.

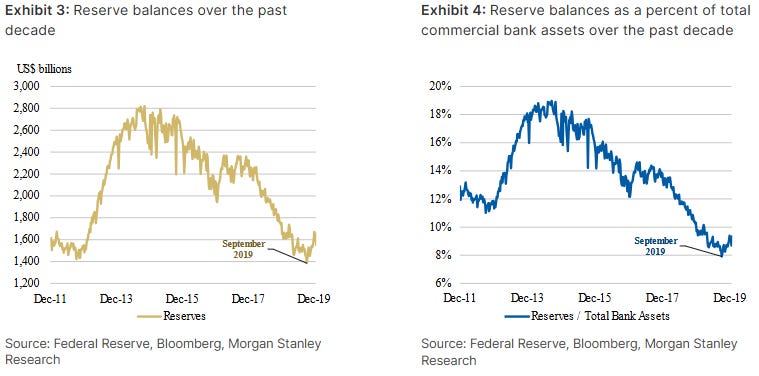

… A driving factor behind the volatility in money market rates was that this large cash drain occurred at a historically low level of aggregate bank reserve balances on an absolute basis and in relation to total commercial bank assets (see Exhibit 3 and Exhibit 4).

…Both the 2018-2019 period and the present are also representative of an environment that had a functionally depleted ON RRP facility. On September 2, the ON RRP facility had $21bn in balances, while in 2018, the ON RRP depleted in 1Q18 (see Exhibit 7).

Exhibit 7: ON RRP balances over the past decade

… AND an NFP precap …

September 3, 2025 MS US Economics: Employment Report Preview: Slowed hiring, but no slower than last month

Payroll growth has slowed, but our 70k forecast for headline payrolls and 80k for private payrolls represents no further slowing in August. We expect no change in the unemployment rate, average hourly earnings +0.3%, and an unchanged workweek.

…Exhibit 2: We project payrolls rose 70k

did you say CHARTS? I love charts …

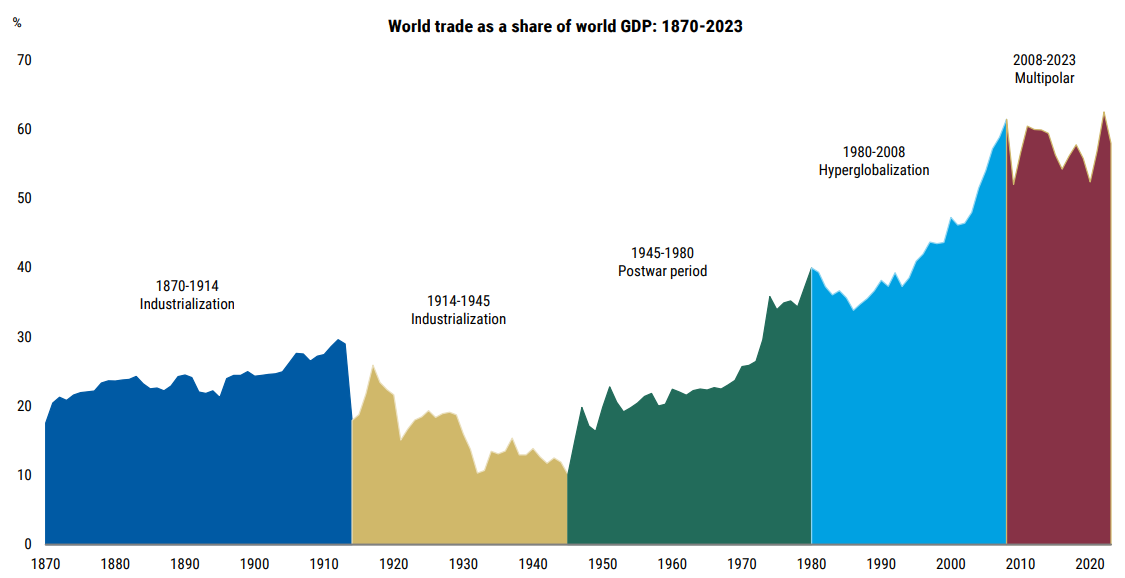

September 3, 2025 MS US Economics: US Economics Chartbook: Slow Growth, Firm Inflation, and Risk Management Rate Cuts

…From a post-WWII world order and globalization to a multipolar world

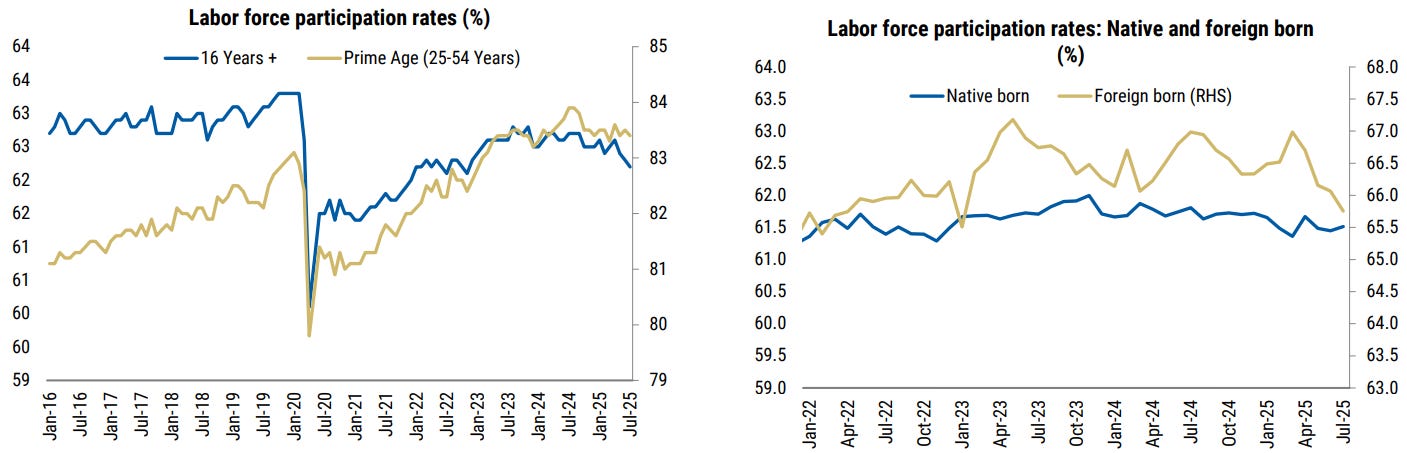

…Labor market: Chilling effect weighs on LFPR The labor force participation rate has declined 0.4pp over the past four months. This has been led by a decline in participation rates for foreign-born workers, which we believe could be a chilling effect from stricter immigration policies. A lower labor force participation rate helps keep the unemployment rate low, even as labor demand slows.

The Federal Reserve has to decide policy based on how far it believes labor markets will weaken, how high inflation will go, and whether higher inflation will persist. (There is also the question of whether rate changes will change any of those issues). On balance, yesterday’s information points to rate cuts.

The poor quality of the job openings data reduces its importance. Nonetheless, the persistence of weak hiring was evident. Smaller businesses, with less supply chain flexibility, reduced externally advertised job vacancies. The Federal Reserve’s Beige Book highlighted uncertainty (mentioned 47 times) as something hindering hiring. The summary section noted “nearly all Districts reported tariff-related price increases” (generally for input prices). There was some suggestion of profit-led inflation, but that does not appear to be widespread.

Bank of England Governor Bailey dampened expectations for a November rate cut. The UK does have higher inflation than its peers, although that should start to move lower. The remarks were not a particular surprise, and the UK government bond market is still generally outperforming European bonds.

US trade data is distorted, and has more political than economic significance. The initial and continuing jobless claims data has no bearing on tomorrow’s employment report, but does keep the focus on US labor market direction.

Steady or softening conditions in the Beige Book In the latest Beige Book, see here, pulling together anecdata and surveys of regional business contacts, the majority of districts reported little or no change in economic activity since the prior reporting period, with only four districts reporting modest growth. This is somewhat downbeat versus the prior survey, in which five districts reported gains. In the survey period, which extended through August 25, four districts (Philadelphia, Richmond, Chicago and Dallas) reported modest growth. Four districts (Boston, Cleveland, St. Louis and Kansas City) reported little change in economic activity over the period. The remaining four districts (New York, Atlanta, Minneapolis and San Francisco) reported slight declines.

Of those reporting flat or declining activity, this was driven by softening consumer spending with the report stating that "for many households, wages were failing to keep up with rising prices" and in New York specifically, "consumers were being squeezed by rising costs of insurance, utilities, and other expenses." On prices there was a shift in the characterization versus the prior report with 10 districts noting moderate or modest growth (versus seven in the prior report) and the other two reporting "strong input price growth that outpaced moderate or modest selling price growth." This shift towards higher prices is consistent with the tariff related pass-through we are starting to see building in the inflation data. In fact in the Beige Book today, "Nearly all Districts noted tariff-related price increases, with contacts from many Districts reporting that tariffs were especially impactful on the prices of inputs," and also that "Most Districts reported that their firms were expecting price increases to continue in the months ahead, with three of those Districts noting that the pace of price increases was expected to rise further." …

September 3, 2025 Wells Fargo: July JOLTS: Labor Market Balance Remains Fraught

Summary The "curious" balance in the labor market Chair Powell highlighted in Jackson Hole looks more delicate following the July JOLTS report. The job opening rate fell back to its cycle low of 4.3% in July. There is now less than one job opening per unemployed worker— the first time this ratio has dropped below 1.0 since 2021. Workers and employers alike remain in a freeze, evident in the hiring and layoff rates holding steady at low levels.

Finally, Dr. Bond Vigilante noting an interesting and all too familiar new normal …

Sep 3, 2025 Yardeni: Stock Market Oblivious To Weak Economic Data

The S&P 500 rose today despite a batch of weak economic indicators over the past two days. Investors perceive that bad news is good news if it increases the chances of a Fed rate cut on September 17. Indeed, the odds of that happening are now 97.6%, according to the CME FedWatch Tool. That's a sure thing. We've been at 40% and are now raising that to a still skeptical 60%. We might have to join the consensus if Friday's employment report doesn't surprise to the upside, as we expect.

Today's JOLTS report for July showed a downtick in job openings, but this series remains relatively high (chart). The ratio of job openings to the number of unemployed workers was 1.0 during July. The paces of both hirings and quits haven't changed much over the past year, suggesting that the labor market hasn't changed much either.

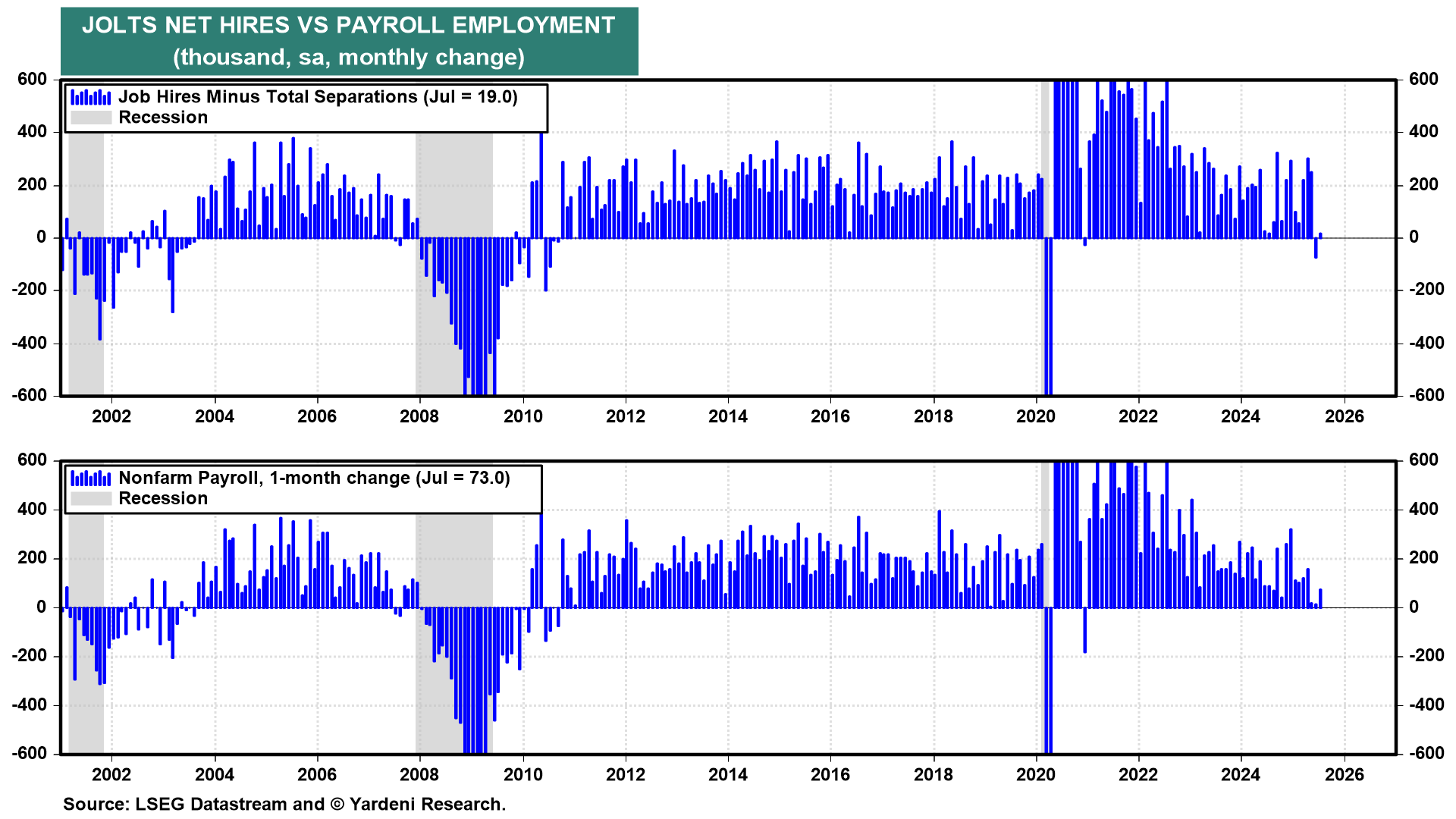

On the other hand, net hirings (i.e., hirings minus separations) rose just 19,000 during July, following a drop of 74,000 during June (chart). These are even weaker readings than shown by payroll employment. We still believe that the weakness in the latter from May through July reflected employers' caution due to uncertainty about tariffs. We expect employers to expand their payrolls in the coming months, as their sales and earnings remain strong despite the uncertainty.

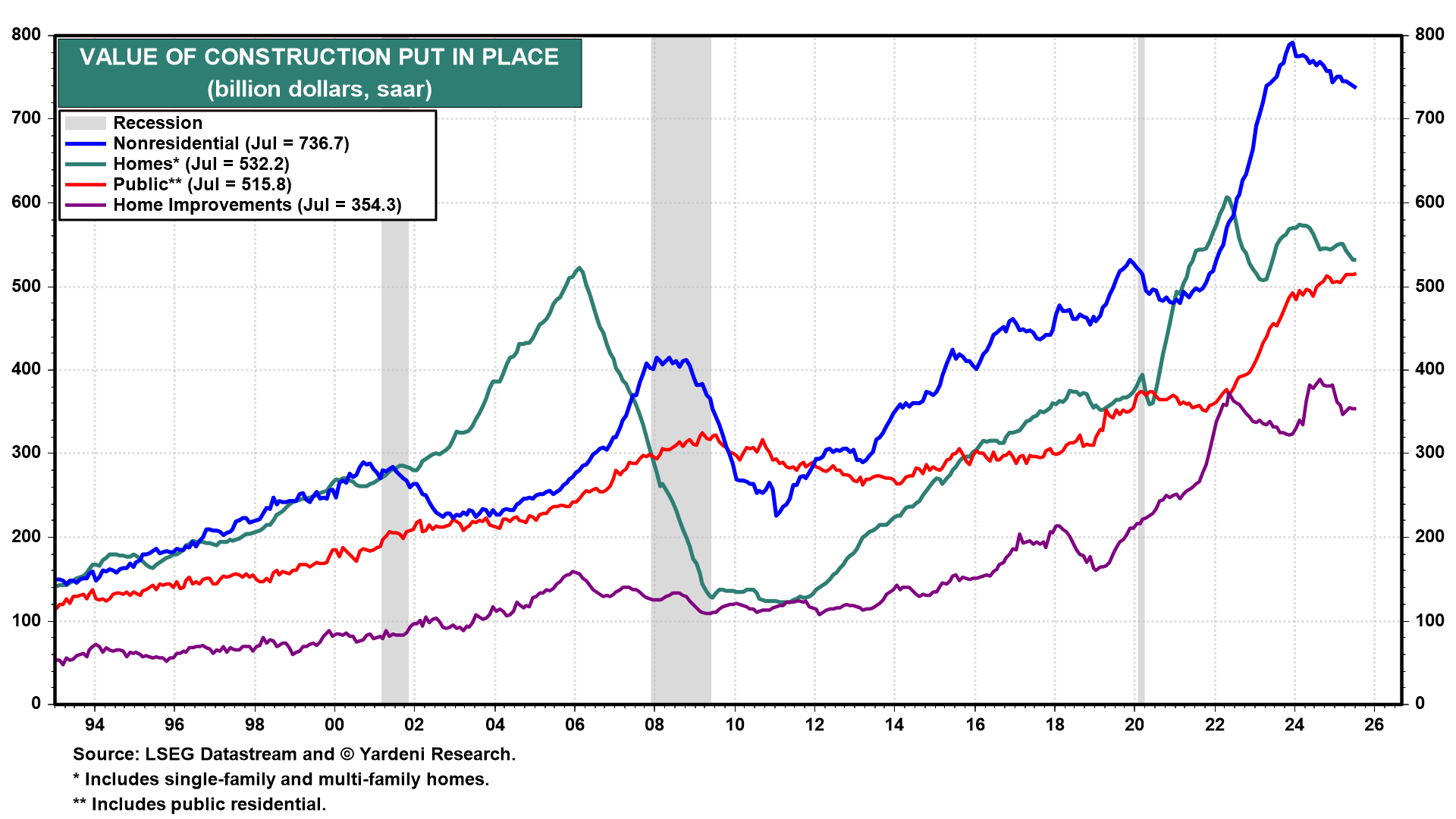

Another set of weak indicators came out yesterday for July's construction spending (chart). Total spending reached a record high of $2.22 trillion in May 2024. It is down only 3.6% since then through July. On the weak side have been nonresidential and residential construction. Public construction spending and spending on home improvements have been relatively stronger.

Another weak report was yesterday's manufacturing purchasing managers survey for August (chart). The M-PMI edged up but remained below 50.0. It has been below this level almost every month since November 2022. New orders rose above 50.0, but both production and employment were below that level…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

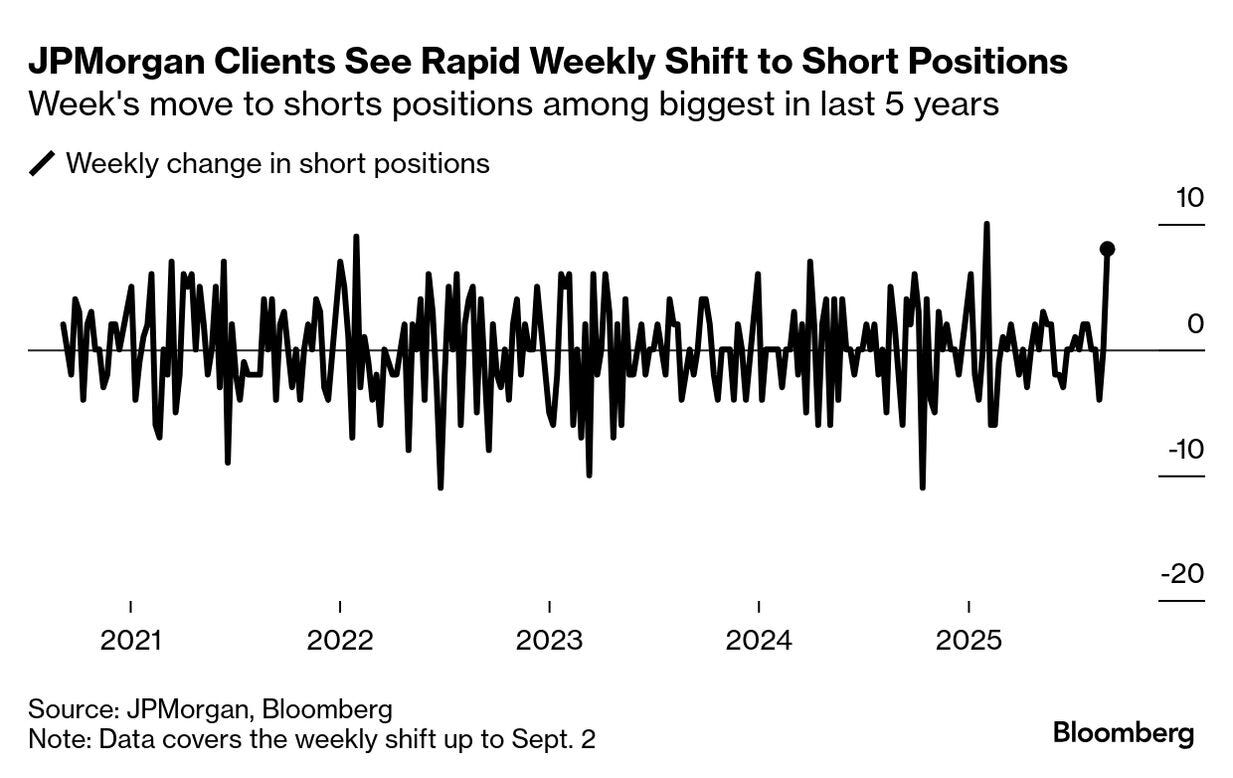

Positions matter and none better than EBB to discuss how clients of Jamie Dimon’s shop all #GotSHORTY …

September 3, 2025 at 8:35 PM UTC Bloomberg: Bearish Treasuries Bets Grow as Traders Brace for Key Jobs Data

Bearish bets are proliferating in US Treasuries and raising the stakes around Friday’s employment report, which may cement views on how aggressively the Federal Reserve will cut interest rates at its September meeting.

The pessimistic mood was captured in the latest JPMorgan Treasury client survey, showing one of the largest weekly shifts to bearish positioning seen over the last five years taking place in the period to Sept. 2. With fiscal worries pushing 30-year yields to just shy of 5%, short wagers stand at their highest level since February.

Those bets — a departure from a previous view that leaned towards a dovish Fed and lower yields after a series of weaker-than-expected economic data — will be tested when the US releases its employment report. A number that is significantly weaker than the 75,000 jobs economists are expecting would bolster the case for more rate cuts and ramp up pressure on bearish investors to recalibrate their positioning.

“If we get enough bad data to tip the scales we could have a break out in yields lower for the short end,” said Kathryn Kaminski, chief strategist and portfolio manager at AlphaSimplex Group. That “could be sort of a catalyst to signal that things in the labor market are a little bit worse than we thought.”

Steepening Curve

The gap between shorter term yields and those on longer-term Treasuries has grown in recent weeks, as investors weigh data suggesting a slowing economy against fiscal worries.

Two-year yields, which tend to more closely track Fed policy expectations, on Wednesday hit the lowest level since May after a weaker-than-expected report on hiring and firing by US employers caused traders to almost fully price in a 25 basis-point cut this month.

While the possibility of a 50 basis-point cut in September is seen as slim, traders in the SOFR options market have nevertheless resumed hedging against such an outcome over the last week.

The recent bearish positioning, however, suggests that some traders believe that recent evidence of cooling growth is an anomaly, according to Sean Simko, head of fixed income investment management at SEI Investments Corp.

“A strong number will move yields higher, faster than a weak number will push yields lower, unless the number is very weak,” he said.

Meanwhile, longer-term yields have headed higher in recent weeks as investors demand increased compensation for financing government deficits. The Trump administration’s spending and tax cut plans are projected to worsen the country’s fiscal position unless tariff revenue growth is sustained, an outcome that a federal court ruling jeopardized last week.

A faster pace of rate cuts could allay some of those concerns, at least temporarily, if falling yields make it easier for the US to service its debt.

It’s Friday’s number, however, that will likely dictate the trajectory for yields over the next few weeks.

Steven Englander, head of global G-10 FX research at Standard Chartered, said in a note that any number below 40,000 jobs would move markets toward a 50 basis point cut.

“To take a cut off the table completely, we think NFP would have to rise to 130k or more, with positive revisions,” he said…

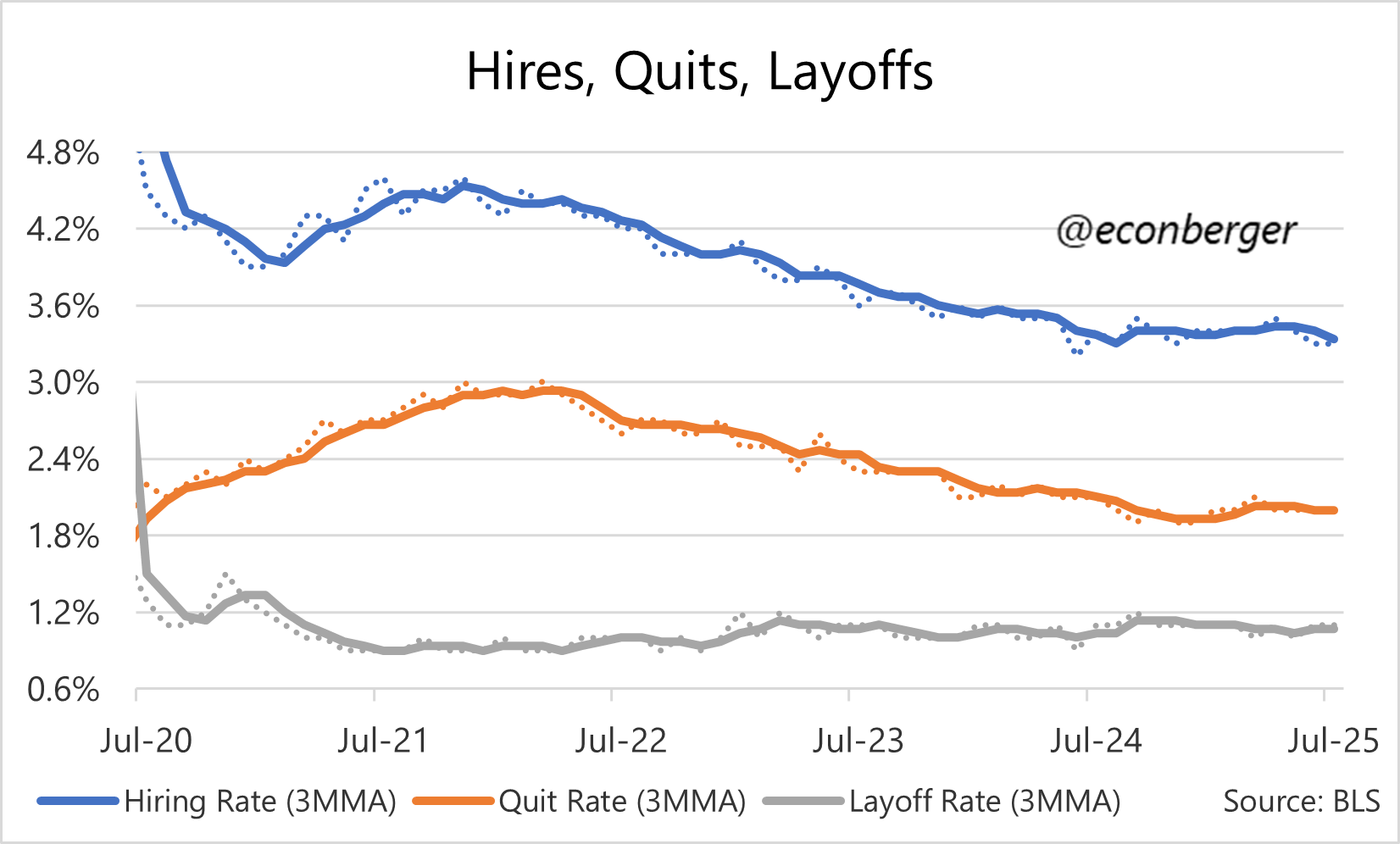

There’s a ‘nuthin burger’ and then there’s an ECON nuthin berger …

TL;DR: JOLTS data remains relatively stable, without clear signs of renewed labor market cooling…

1. The Big Picture

Hiring bottomed in the summer of 2024; quits followed a few months later. If you’re wondering why folks characterize the labor market as stable, the JOLTS data provides a lot of the evidence (and the household survey in the jobs report bears the rest of the load1).

I didn’t see anything in today’s report that seriously challenged that thesis. Hires have been down a little in June and July, and if that intensifies it will be worrisome - as my friend Conor Sen suggested, I could be overlooking a turning point. But it could also easily be noise.

Underpinning this stability is something I’ve been talking about a lot in my posts: policy is taking big whacks at both labor demand and labor supply, and so far has harmed both in roughly equal measure. That seems like an unstable equilibrium, and it could easily tip one way or the other in the coming months. (Weakly held belief: labor market cooling is more likely than labor market reheating.)

But these forces aren’t necessarily in balance across the economy. Even in normal circumstances, we’d expect some industries to be doing better than others, which in a stable environment means expansion and contraction co-existing. In the current environment, where policy is providing strong pushes in various directions, you’d be sure to see it! And later in this post, I’ll discuss a few of these sectors…

AND …

… follow me for more travel tips but … THAT is all for now. Off to the day job…