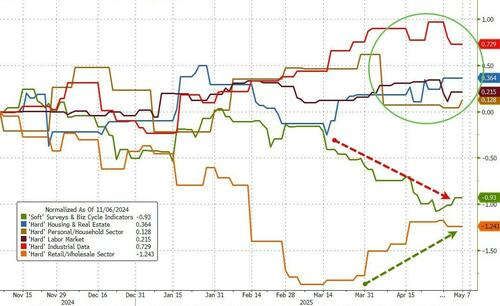

while WE slept: USTs currently a touch into the red (concession?); UK trade deal; FOMC recaps / victory laps (CONsensus around the wait N see); 100d of Trump in a chart (credit def swaps on USA)

Good morning … I’m sure that you’ve heard by now …

… right … This was the scene from FOMC board room located at The Eccles Building, 2051 Constitution Avenue NW. as the meeting came and went with NO rate cuts for us, yet … More …

ZH: Fed Rejects Trump Calls To Cut Rates: Warns Of "Increased" Stagflationary "Uncertainty"

ZH Watch Live: Fed Chair Powell Explains Why It's Different Now Vs September

… Recapping the statement, Goldman chief US economist David Mericle writes:

Very close to what we were expecting. Surveys have weakened a lot, hard data has not – we continue to think that they will want to see that before they make any changes.

Very little new info here - No policy change, highlighting that uncertainly has increased further.

Highlighting risk on both sides of the mandate - higher unemployment and inflation.

Very first paragraph acknowledges Q1 GDP (and other data) was weaker because of “swings in net exports”

In his prepared speech, Rabobank's Philip Marey notes how Powell stressed that despite the heightened uncertainty, the economy remains solid (a point he underscored during the subsequent press conference when he confirmed that there had been no weakness in the hard data)…

… More on the Fed and it’s conclave from Global Wall below but for now … AND as the day came to a close, I’ve not yet seen it put better so …

ZH: Stocks, Bonds, & Bitcoin Jump On China 'Hope', Powell 'Nope', & Trump 'Rope-a-Dope'

… Powell stood strongly in the room against a roomful of reporters who were desperate to hear that Trump's tariffs had wrecked the world but the Fed Chair said - all we see is 'concern' about the impact (driven by fearmongering we would suggest) of the impact of the tariffs, but none of the data is showing any effects... none (labor market is strong and inflation is slowing).

So maybe that 9% inflation expectation from UMich Democrats is exactly what Powell said - an outlier.

Paraphrasing the hour-long press conference:

"It's not the economy; it's the fearmongering, stupid!"

… It's Not a Situation Where We Can Cut Preemptively

*POWELL: INFLATIONARY EFFECTS OF POLICIES COULD BE SHORT-LIVED

*POWELL: UNCERTAINTY ABOUT PATH OF ECONOMY IS EXTREMELY ELEVATED

*POWELL: NOT SEEING SLOWDOWN SHOW UP IN ACTUAL ECONOMIC DATA YET

*POWELL: COSTS OF WAITING ARE FAIRLY LOW

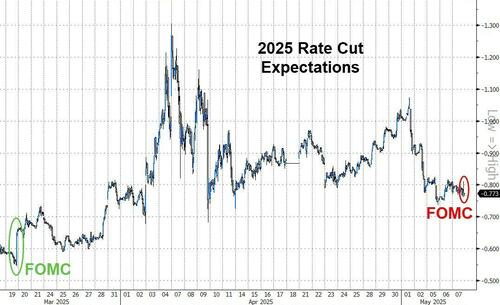

Which left the market pricing in just three cuts for the rest of 2025...

Before we leave The Fed commentary, Academy Securities' Peter Tchir pointed out the most salient aspect of today's meeting: The FOMC basically said the risk of stagflation rose.

Upside risk to inflation and unemployment. Normally that would be big news, but

The big question going into Powell’s press conference is whether the Fed will respond to unemployment faster than to inflation fears?

In his prepared remarks, he tried to make it clear that they would balance the two.

That they would compare and contrast how far they are from goals, and how they are moving. He made it seem like he was in no rush to do anything!

Nothing in the Q&A seemed to come out overwhelmingly hawkish or dovish.

Maybe neutral was a bit better than expected, but I’d watch out for negative headlines from the administration going forward, more than hoping for positive headlines.

Basically what I came into the week thinking, just a touch worse/more negative.

Obviously the headlines around US-China trade talks starting this weekend sparked the initial gains, sending US equity futures higher by over 1% shortly after the cash equity close.

… Treasury yields were lower across the curve with the long-end outperforming (and all yields lower on the week now)...

President Trump is expected to announce on Thursday that the United States will strike a trade agreement with Britain, according to three people familiar with the plans.

Mr. Trump teased a new trade agreement in a social media post on Wednesday night, though he did not specify which nation was part of the deal.

“Big News Conference tomorrow morning at 10:00 A.M., The Oval Office, concerning a MAJOR TRADE DEAL WITH REPRESENTATIVES OF A BIG, AND HIGHLY RESPECTED, COUNTRY. THE FIRST OF MANY!!!” he wrote.

A spokesman for the White House declined to comment beyond Mr. Trump’s post. A spokesman for the British Embassy in Washington did not respond to a request for comment…

… AND all this provides a bit of a risk ON reflex / response from bonds (ie a concession) ahead ofthis afternoons $25b upcoming auction … A look at yields …

30yy DAILY: watching trangulating range 4.95, 4.85 and 4.55 …

… momentum NOT suggesting much of any impulse, at least not to me

… I’ll be done, move on and first … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US Market Open: Stocks gain and DXY tops 100.00 ahead of Trump's UK-US trade announcement; BoE due … The Fed's decision to keep rates steady (as expected) and Powell stressing a wait-and-see approach to policy, sparked some two-way action in USTs - before then extending a little lower into the APAC session. As for today, US President Trump saying he will announce a trade deal (with the UK) today has managed to boost the risk tone. USTs currently a touch into the red but above yesterday’s low in a 111-11 to 111-19 band. Ahead, weekly jobless claims are due before the NY Fed SCE, in March it showed an increase in near-term inflation expectations and a slight moderation further out alongside an expected deterioration in the labour market. A 30yr auction is also scheduled…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

AND we begin … Global Wall reporting live from … the Fed’s conclave …

8 May 2025 ABN Amro: Fed Watch - No rate cut in sight

As expected, the Federal Reserve kept rates on hold today, maintaining the upper bound of the federal funds rate at 4.50%. The key update in the policy statement was that uncertainty about the outlook has increased further. Risks of higher unemployment and higher inflation have risen. Powell acknowledged that Trump's tariffs were higher than anticipated but noted that tariff talks are currently in a new phase of negotiations, which could change the picture materially, or not. Powell reiterated that the only response to this level of uncertainty is to wait and see, and that the Fed is well-positioned to react in a timely manner.

… Global Wall reporting from the Fed conclave …

8 May 2025 Barclays: Federal Reserve Commentary: May FOMC: Wait and see

The FOMC kept rates unchanged amid a further increase in uncertainty about the outlook. It viewed activity as growing solidly and judged that risks of higher unemployment and higher inflation have risen. Powell signaled that the FOMC is in no rush to adjust rates.

…We retain our baseline expectation that the FOMC will deliver two 25bp cuts this year, in July and September, and again two more cuts in 2026 (June and September). In doing so, we think the FOMC will maintain a policy stance that remains somewhat restrictive so that inflation ultimately returns to the target over time, but that would avoid becoming increasingly restrictive as the economy slows and the labor market deteriorates…

Absent a decisive turn in US economic data, the FOMC seems comfortable remaining on hold indefinitely. We continue to believe, as we have since December, that rates will stay unchanged through year-end.

If it were obvious that the next move is a cut, Chair Powell would have cut already. The problem is that this isn’t obvious at all.

… US rates strategy: With Powell discussing the “heightened uncertainty” that plagues both sides of the Fed’s mandate, we think US rates investors are unlikely to take much signal from the May FOMC meeting and will let the data do the talking. To that end, most investor conversations recently have revolved around two main scenarios – (i) where the data continues to stay resilient for some time at least, giving the Fed no reason to deliver cuts in 2025 and pushing out more aggressive easing to next year (our central case), or (ii) where the nonlinear risks of a labor market slowdown materialize and the Fed sharply lowers rates this year. We think there is value is staying positioned for a trade that targets 2026 rate levels, which can benefit in scenarios of sharp cuts in 2025 as well if easing is pushed out, and therefore we suggest trades on the 1y1y rate. We continue to suggest mis-weighted 1y1y receiver ladders to position for these non-linear risks, but with limited downside (Buy 1y1y A-50/A-125/A-150 receiver ladder (1.75 x -1 x -1)).

Best in show — an FOMC recap and a daily catch up…

May 7, 2025 BMO FOMC: Uncertainty Rising, Policy Rates Unchanged

It was unsurprising to see that the most relevant takeaway from the FOMC meeting was that uncertainty regarding the outlook has "increased further." That is certainly consistent with the price action since Liberation Day -- choppy with limited conviction. The statement began by downplaying the negative real GDP print for Q1 -- observing that, "Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace." The statement also added regarding the dual mandate that the Committee "judges that the risks of higher unemployment and higher inflation have risen." Indicating that monetary policymakers are also wary of a round of stagflation -- or at least what could optically appear as such. The vote was unanimous - with even Kashkari (who voted as an alternate) confirming the wait-and-see approach.

There wasn't anything within the statement that was particularly surprising, although the cautious tone has led to a round of buying in US Treasuries with the 5-year sector leading the move. 2s are the underperformer given that nothing within the statement suggested the Fed is readying to cut rates in June. Instead, we're viewing this as simply a placeholder of a statement and expect attention will quickly shift to the press conference -- where we see the risk as a more 'hawkish' tone from Powell as the objective appears to be continuing to delay cuts until there is less uncertainty on the outlook.

… Consistent with expectations, Powell held the line at the press conference by reiterating that the Fed is ‘well positioned’ to await greater clarity and doesn’t need to be in a hurry to lower policy rates. Notably, the Chair went as far as saying that the cost of waiting for greater clarity is ‘fairly low’ – hawkish, but a downgrade from ‘very low’ at the March FOMC. More relevant to how the Fed plans to address a situation in which its dual-mandate goals are in tension, Powell reiterated a familiar framework in that policymakers will consider 1) “how far the economy is from each goal” and 2) “the potentially different time horizons over which those respective gaps would be anticipated to close.” In Powell’s words, it’s a “very difficult balancing judgment” that the Fed may ultimately face. That said, the Fed Chief made the observation that “we may never face it” – even if the FOMC needs to keep the risk in its thinking.

Before the Fed, Bessent’s congressional testimony was in focus. While none of the Treasury Secretary’s comments on bank capital regulations were ‘new’ information, the simple re-emphasis that SLR reform is a “high priority” for financial regulators was enough to trigger a bid in swap spreads. The prospects for SLR relief have been on the market’s radar for some time and while it’s been made clear that it is a high line item for market officials, there isn’t a clear timeline for when any changes are likely to be implemented. Bessent also signaled that the US-China trade negotiations will begin on Saturday. If anything, we’ll be mindful of the potential flows associated with the event risk as the weekend comes into focus.

Wednesday afternoon’s release of the investor class data for the coupon auctions that settled on April 30th (2s, 5s, 7s, and 20s) reinforced Bessent’s comment that there is “broad investor support” for Treasuries in the primary market. Despite universally below-average indirect bidding at the front-end offerings, there was no evidence of flagging foreign demand. Foreign buyers took 9.6% at the 2-year offering, slightly below the 10.9% average but within the recent range. Overseas investors took 11.1% at the 5-year auction, above the 10.2% average and highest since October 2024. And lastly, foreign buyers were allotted 9.9% at the 7-year auction. Below the 6-month average of 10.8% but the first increase in seven months and a YTD high…

Germany weighin’ in on the Fed conclave …

07 May 2025 DB: May FOMC recap: Nothing much to say beyond stay

The May FOMC meeting offered no surprises, with the Fed keeping rates steady and Chair Powell providing limited guidance about the policy outlook. Elevated uncertainty was the key theme, with the statement noting uncertainty and two-sided risks have risen since the March meeting. Although Powell was pressed on how the Fed would lean if dual mandate tensions arise, he did not get into hypotheticals. Instead, he continued to emphasize the Fed was not in a hurry/can be patient with policy still "well positioned" to deal with risks.

Our base case remains that the next rate cut is in December, followed by two more 25bp cuts in Q1 2026 (see US outlook: Tariff-struck). These reductions will bring the fed funds rate into the 3.5-3.75% range, consistent with our view of neutral. Risks are tilted towards earlier cuts if unemployment rises more sharply.

…In a Trump 2.0 world it often seems like the news flow doesn't really get going until after the US market closes and today is another example of that as overnight Mr Trump has teased that a "major trade deal" will be announced today at 10am DC time (15:00 BST). This must be the very big announcement he flagged on Tuesday. The media are all lining up behind the deal being with the UK. Given that full trade deals take years to negotiate, this will likely be a framework and it will be interesting to see whether the 10% baseline tariff stays as that will provide an important template for negotiations with other countries and a good guide to the long-term tariff strategy of the US…

…This news has slightly overshadowed the Fed last night, where as widely expected, the FOMC kept the fed funds rate on hold for a third meeting running at 4.25-4.50%, while sticking to a patient tone amid heightened uncertainty. The prepared statement noted that uncertainty had “increased further” as risks of both “higher unemployment and higher inflation have risen”. In the press conference Chair Powell acknowledged opposing pressures on its dual mandate stemming from larger-than-expected tariffs announced so far and offered little guidance on the policy path ahead. Powell emphasized the elevated uncertainty but also noted that the economy remains resilient and repeated that policy is well positioned to respond, while pushing back on the idea of pre-emptive rate cuts. Our US economists continue to expect the next rate cut to come in December, with risks tilted towards earlier cuts if unemployment rises more sharply. See their full reaction here.

Rates initially saw a moderate rally following the Fed decision, but this then reversed as Powell emphasised a wait-and-see approach. The next rate cut is now 80% priced by the July meeting while the amount of Fed cuts priced by December declined by -3.1bps yesterday to 78bps, though this move had already played out pre-FOMC. 2yr Treasury yields were little changed (-0.6bps to 3.78%), while 10yr yields declined -2.6bps to 4.27%. This morning in Asia, Treasury yields have reversed higher again with 2yr (+2.3bps) and 10yr (+1.9bps) yields settling at around 3.80% and 4.29% respectively as we go to print…

… and on EARNINGS …

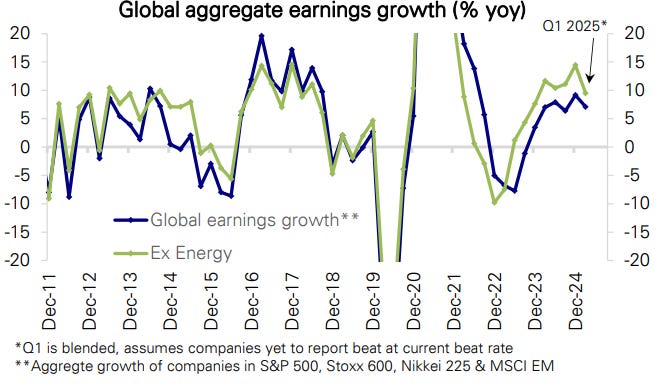

07 May 2025 DB: Asset Allocation - Q1 2025 Global Earnings Chart Pack

…A modest slowing in global earnings growth. Global earnings growth declined modestly from 9.2% in Q4 to 7.1% in Q1 but remained well within the 6.5%-9.5% range during 2024. Earnings growth for the Energy sector was negative in all four regions, excluding which Q1 earnings growth (10%) was in the double digits for a 6th straight quarter. Across regions, earnings growth in Japan, the US and EM continued to be robust, but that in Europe stayed near zero:

US growth slowed only modestly in Q1. S&P 500 earnings are on track to deliver robust 9.8% yoy growth in the quarter, only a little slower than the 13.5% seen in Q4. The slowing in earnings growth was broad based across sectors.

Is Europe turning the corner? Earnings growth in Europe has been weak for almost 2 years, being extremely negative for most of 2023 and then hovering near zero for most of 2024. Growth remained near zero again in Q1 2025. However, the level of earnings, which had declined for three straight quarters, rose sequentially in Q1 2025, albeit only slightly. It is notable that this sequential increase occurred even as US earnings saw a slight sequential decline.

Continued robust growth in Japan and EM. Earnings growth in Japan (10%) and EM (7.1%) rose slightly in Q1 and continued to be near the upper end of their typical ranges.

… Global Wall reporting from the Fed conclave …

7 May 2025 ING Fed’s wait and see stance could persist through to September

Another hold from the Federal Reserve with an acknowledgement that uncertainty has increased with more upside risk for both inflation and unemployment. This suggests little inclination to move until they are confident of the direction the data is heading, meaning rate cuts could be delayed, but risk being sharper when they come

7 May 2025 ING Rates Spark: The Fed is talking a lot but the BoE will deliver

The Fed was balanced but yields managed to edge lower on rate cut optimism; cuts still seen as inevitable, eventually. The Bank of England will likely cut rates but this won't come as a surprise to the market. Having said that, sterling rates remain sensitive to moves in US rates, which puts markets at risk of pricing in too many more cuts in the near term

… Global Wall reporting from the Fed conclave …

May 7, 2025 MS: Federal Reserve Monitor: FOMC Reaction: Awaiting Further Clarity

The Fed sees upside risk to inflation and unemployment. Powell was clear in saying monetary policy was "well positioned" and the Fed needs further clarity before making policy adjustments. We continue to think markets are putting too much weight on near-term cuts out of the Fed.

Key expectations

The Fed left its policy rate and balance sheet policies unchanged as expected.

A solid economy, tension in the dual mandate, and a modestly restrictive policy stance leave the Fed in wait-and-see mode.

We still expect no rate cuts in 2025, with back-loaded cuts in 2026 that bring the policy rate to 2.50-2.75%.

Our rates strategists suggest investors maintain positions for a steeper yield curve – UST 3s30s steepeners and term SOFR 1y1y vs. 5y5y steepeners – as we expect a lower market-implied trough rate.

We see room for the USD to decline driven by both factors of our post-April 2nd framework: yield differentials and negative policy premium.

The near-term path of least resistance for agency MBS is likely tighter, but if net issuance trends normalize, we're concerned that valuations are not attractive enough for money managers to add to overweights longer term.

The Fed leaves rates unchanged and are not in a hurry to move. With higher uncertainty at both sides of their mandate, they are waiting for more clarity.

… Global Wall reporting from the Fed conclave (with an I told ya so from our neighbors to the North)…

May 7, 2025 RBC: The Fed continues to wait and see

As was widely expected, the Fed continued to hold interest rates steady in its May meeting. While their messaging was little changed, there was a notable tweak to their statement, which emphasized the growing uncertainty surrounding both of their mandates – inflation risks are intensifying following the implementation of [higher than expected] tariffs and the risks to unemployment are climbing as the economy shows signs of slowing. Still, the Fed expressed confidence in its current policy stance as it awaits to see the impacts of trade policies on the economy in the months ahead.

“[…] as we noted in our statement, we have judged that the risks to higher employment and higher inflation have both risen and this, by the way, of course, is compared to March… I think there’s a great deal of uncertainty about, for example, where tariff policies are going to settle out and also when they do settle out, what will be the implications for the economy, for growth, and for employment… ultimately, we think our policy rate is in a good place to stay as we await further clarity on tariffs and ultimately their implications for the economy.”

AND …

08 May 2025 UBS: How far, how fast is the retreat?

Federal Reserve Chair Powell pointed out that uncertainty had risen, and that inflation and unemployment might rise. These are all eloquent statements of the obvious. leaving the Fed reacting to data. Central banks that react rather than pre-empt data tend to be late in changing policy. Economic data is also increasingly less reliable, making data dependency more dangerous.

US President Trump declared they will announce trade developments with a “big and highly respected” country. It could be the penguins of the Heard and MacDonald islands. It could be the UK (the UK does not always appear to have a trade surplus with the US). Markets only really care how far and how fast Trump retreats from tariffs.

A promise of some kind of trade deal is unlikely to affect the Bank of England policy decision. Global disinflation trends (ex-US) give the bank room to cut rates. Sweden’s Riksbank is expected to leave rates unchanged (its policy rate is already half that of the UK).

The data calendar offers limited information. US first quarter productivity and unit labor cost data relates to the before times, and it is trade taxes and profit-led inflation rather than labor markets that are likely to drive US prices in the near term.

… covered wagons after the Fed conclave …

May 7, 2025 Wells Fargo: FOMC's Holding Pattern Continues

Summary

The widely expected decision by the FOMC to keep rates on hold at today's policy meeting was universally supported by all 12 voting members of the Committee.

In its post-meeting statement, the FOMC noted that "uncertainty around the economic outlook has increased further" (emphasis ours). The statement included the previously used sentence that "the Committee is attentive to the risks to both sides of its dual mandate" but then added "and judges that the risks of higher unemployment and higher inflation have risen."

The sharp rise in the effective tariff rate likely will cause both inflation and the unemployment rate to rise in coming months. Hence, there may be some tension in terms of the Fed's dual mandate (i.e., "price stability" and "full employment") in coming months.

The best course of action for the FOMC may simply be to wait for more clarity about trade policy and its implications for the U.S. economy. Indeed, Chair Powell seemed to indicate as such during his post-meeting press conference.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Powell Post Fed stock mkt …

May 7, 2025, 1:04 PM BESPOKE: Stocks with Earnings Momentum; Powell Fed Day

… This afternoon, the Fed will announce its latest decision on interest rates, and Fed Chair Powell will take the podium around 2:30 PM ET to discuss policy with the world.

Regular readers of Bespoke should know that the market has typically done poorly in the afternoons on Powell Fed Days. Remarkably, the S&P 500 has declined in the final hour of trading on each of the last eight Fed Days! Below is an intraday composite chart showing the average path that the S&P has taken on the last eight Fed Days. Look at the sell-off we've seen in the last hour from 3-4 PM ET! We've gone from the highs of the day around 3 PM to closing at the lows of the day.

A view worth a look — agree or not …

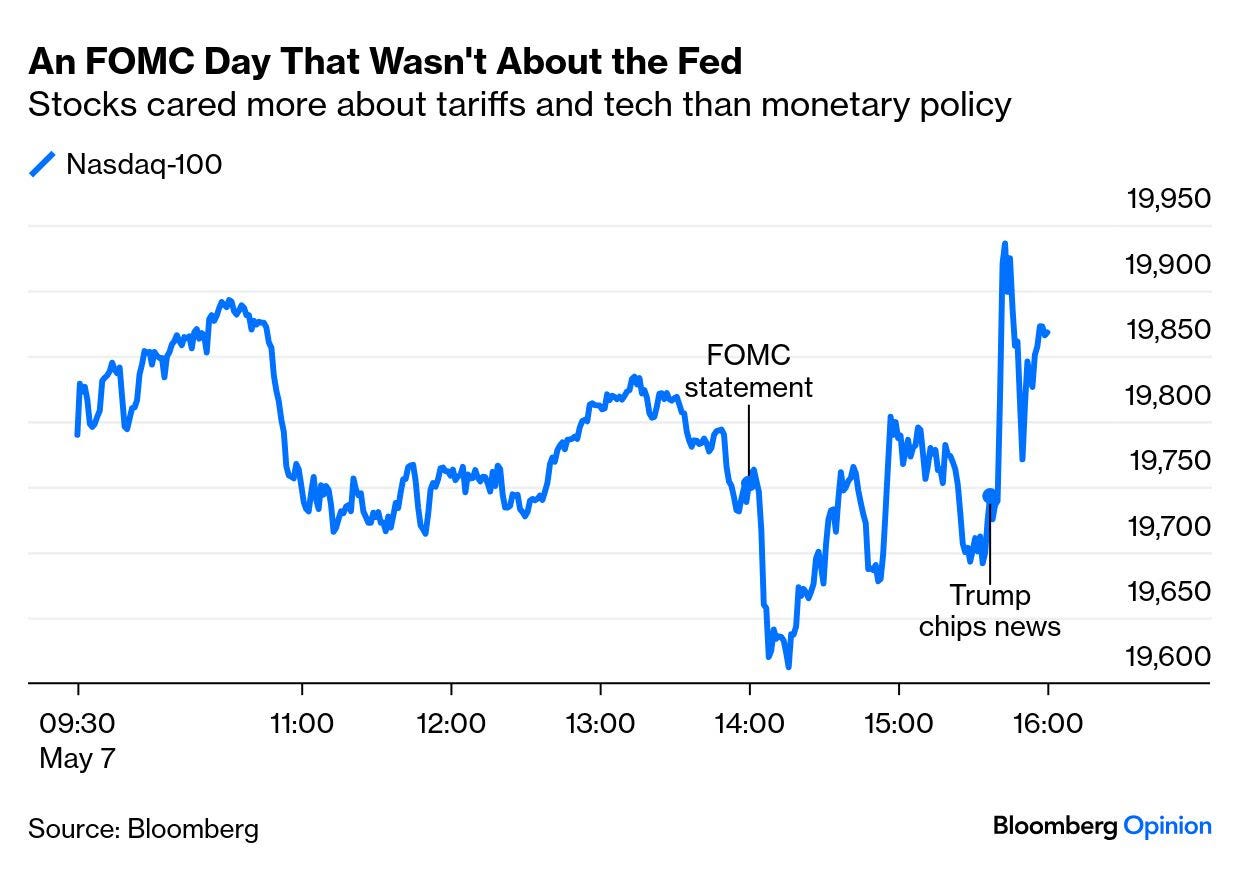

May 8, 2025 at 5:02 AM UTC Bloomberg: Stagflation, But That's Not Important Right Now The Fed falls flat: Tariffs are all anyone wants to know about until the 90-day pause expires.

…With the Fed predictably on hold, tech mattered more. Breaking news shortly before Wall Street’s close that the Trump administration was planning to lift restrictions on chips used for artificial intelligence had a much bigger impact on stocks than the Fed:

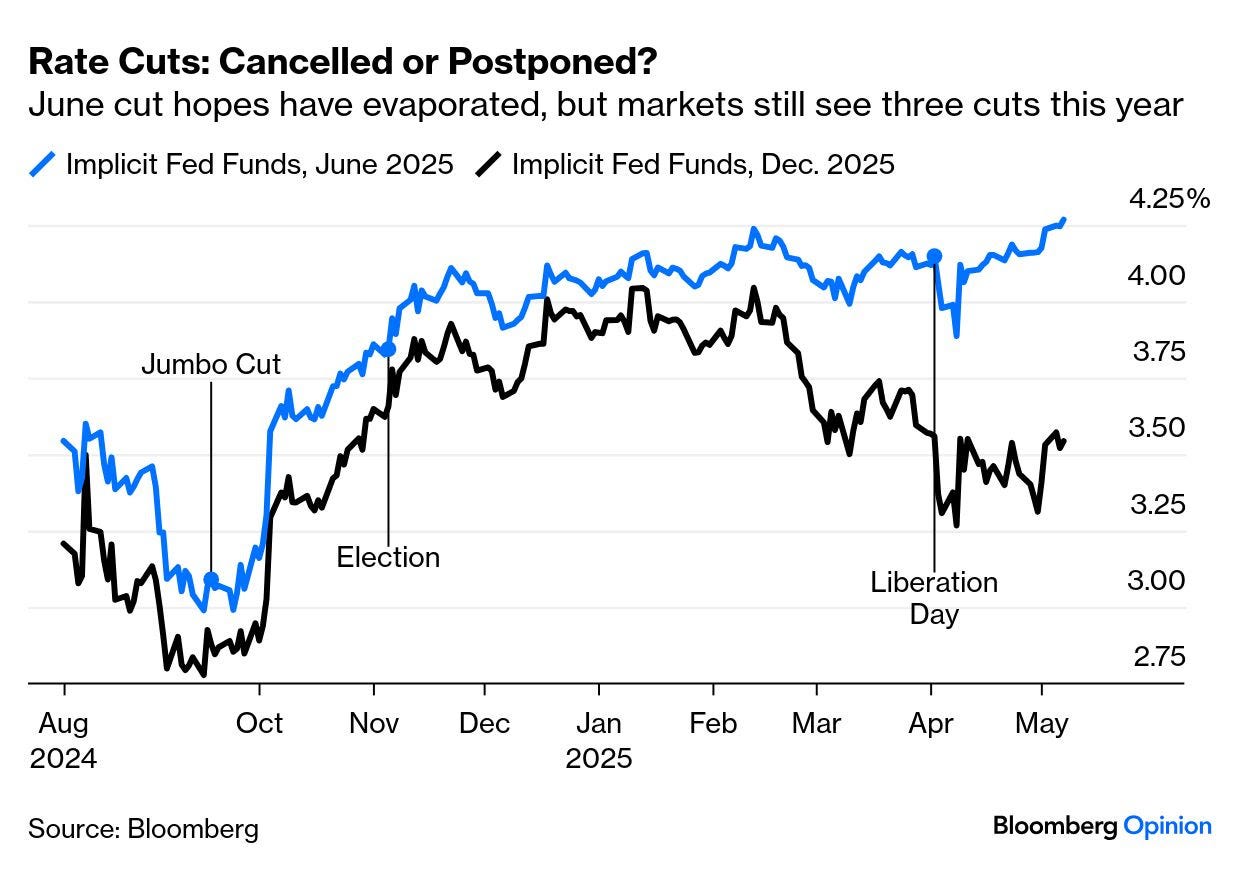

Oddly though, the Fed’s perception that risks have risen has had minimal impact on market expectations for future rate changes. Hopes for a cut next month have dwindled, with the odds now put at only 20%. Why would the Fed move before the tariffs pause ends on July 8? But confidence that three cuts are on the way this year remains strong. The market still expects the fed funds rate to be at 3.5% at year-end, substantially unchanged since Liberation Day:

The market evidently believes thatPowell will wait and see, and also appears to think that tariffs’ ultimate impact will be to limit growth without stoking inflation. Three cuts over the year’s last four meetings would imply a seriously slowing economy. Why the confidence?

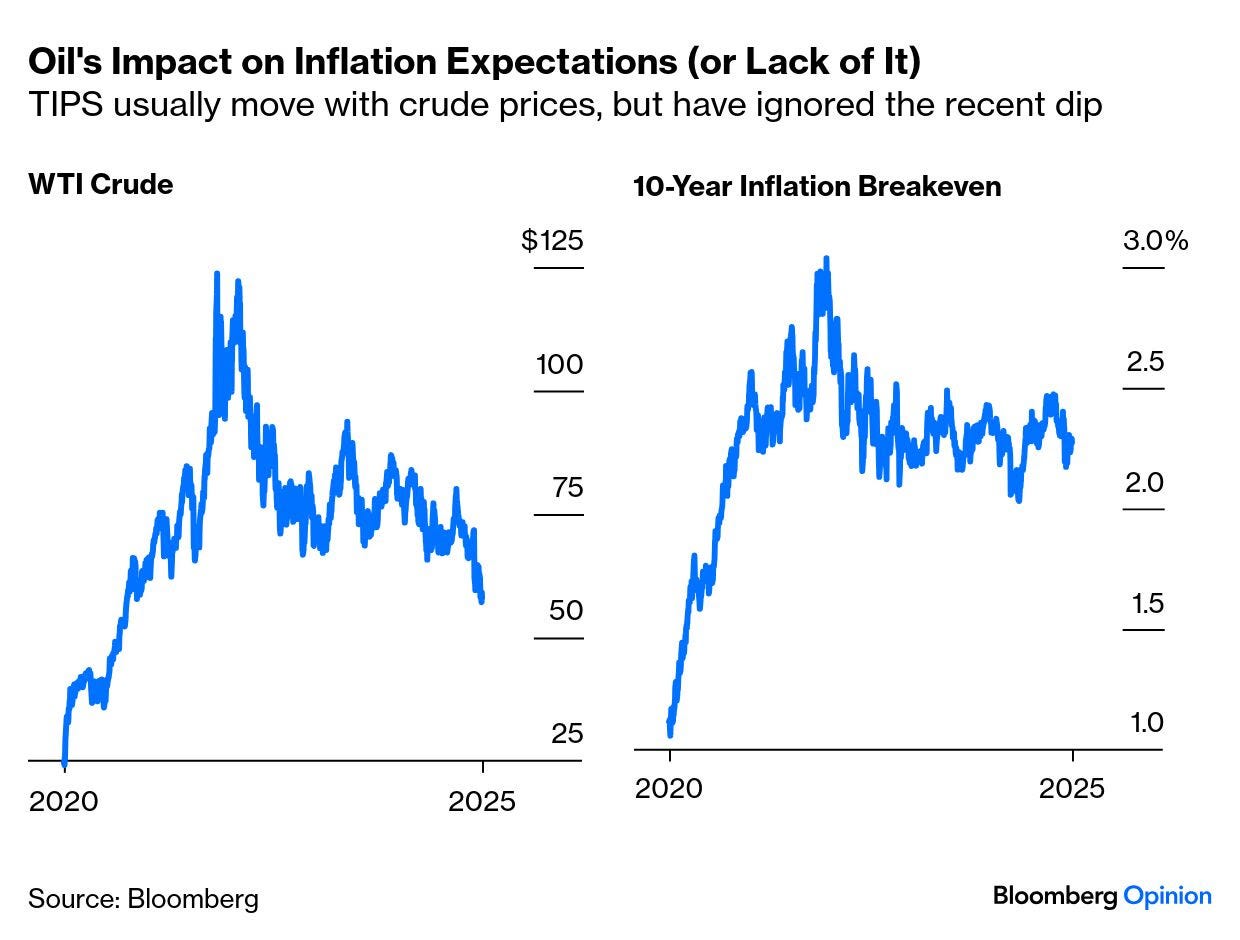

The single biggest reason comes from the oil price, which has recently collapsed to its lowest since early in 2021. That directly implies downward pressure on inflation, and crude prices usually translate directly into bond market inflation breakevens. That hasn’t happened thus far, with 10-year inflation forecasts barely changed as oil tumbles. (If you’re reading this on the terminal, press the “Open in GP” button so you can see the two series overlaid — normally the relationship is remarkably close):

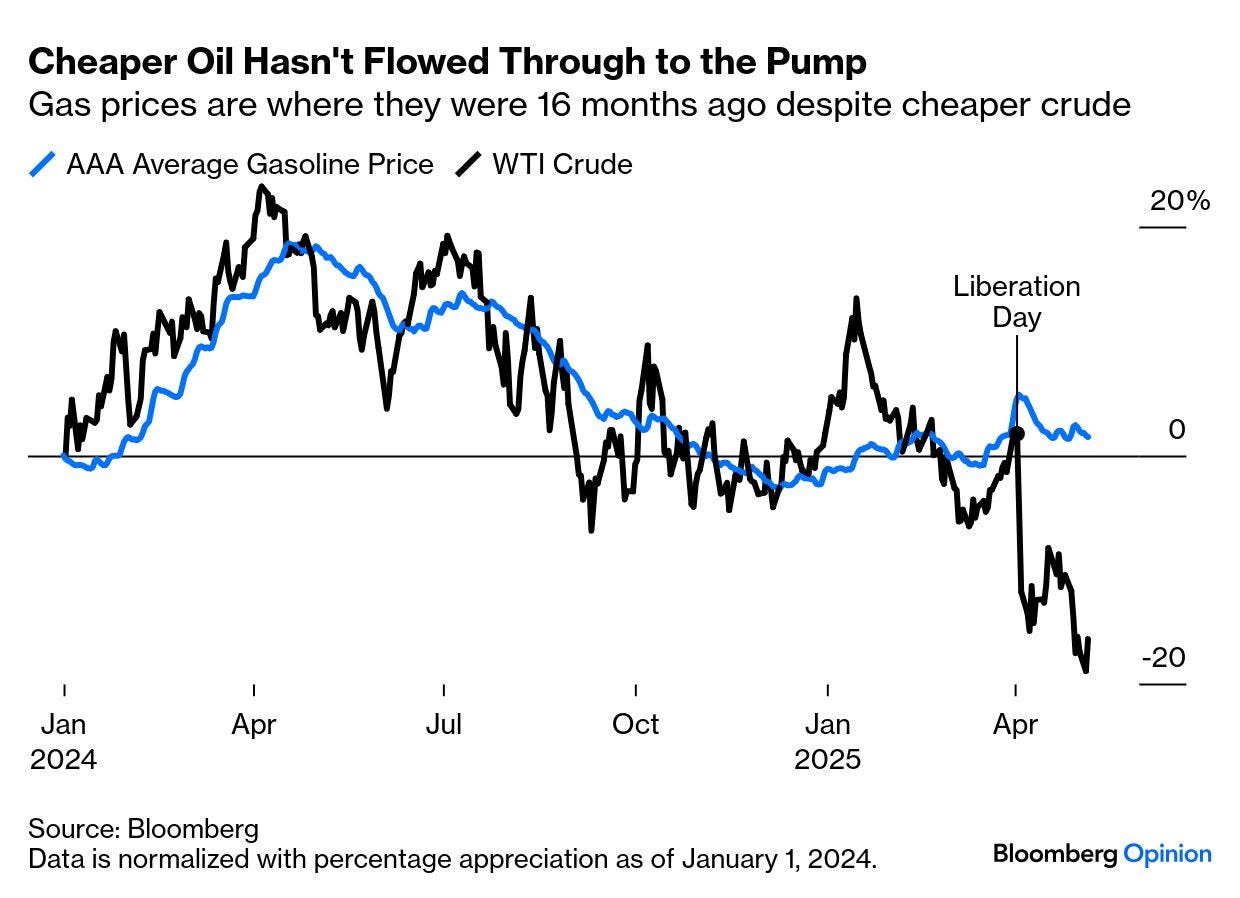

Cheaper oil isn’t necessarily a total boon. It reduces input prices for industrialists who might be facing a tariff bill for importing components — but it also eats into the incentives for producers to drill, baby, drill. That explains why OPEC+ has been happy to let the price fall, led by Saudi Arabia. It can also be a symptom of falling global demand. Oil took its first dramatic dive on Liberation Day, which was seen to be a hit to global economic strength. Unlike stocks, it hasn’t recovered in the slightest.

Another strange phenomenon is that the bear market in crude has had virtually no effect, as yet, on prices at the pump. This is very unusual:

If we assume that cheaper crude will, at the end of the long refining process, trickle through to cheaper prices for American motorists, that is reason to hope consumer confidence can be bolstered, and inflation can stay under control. So maybe that justifies the expectations of rate cuts. But a lot more will need to go into that calculation.

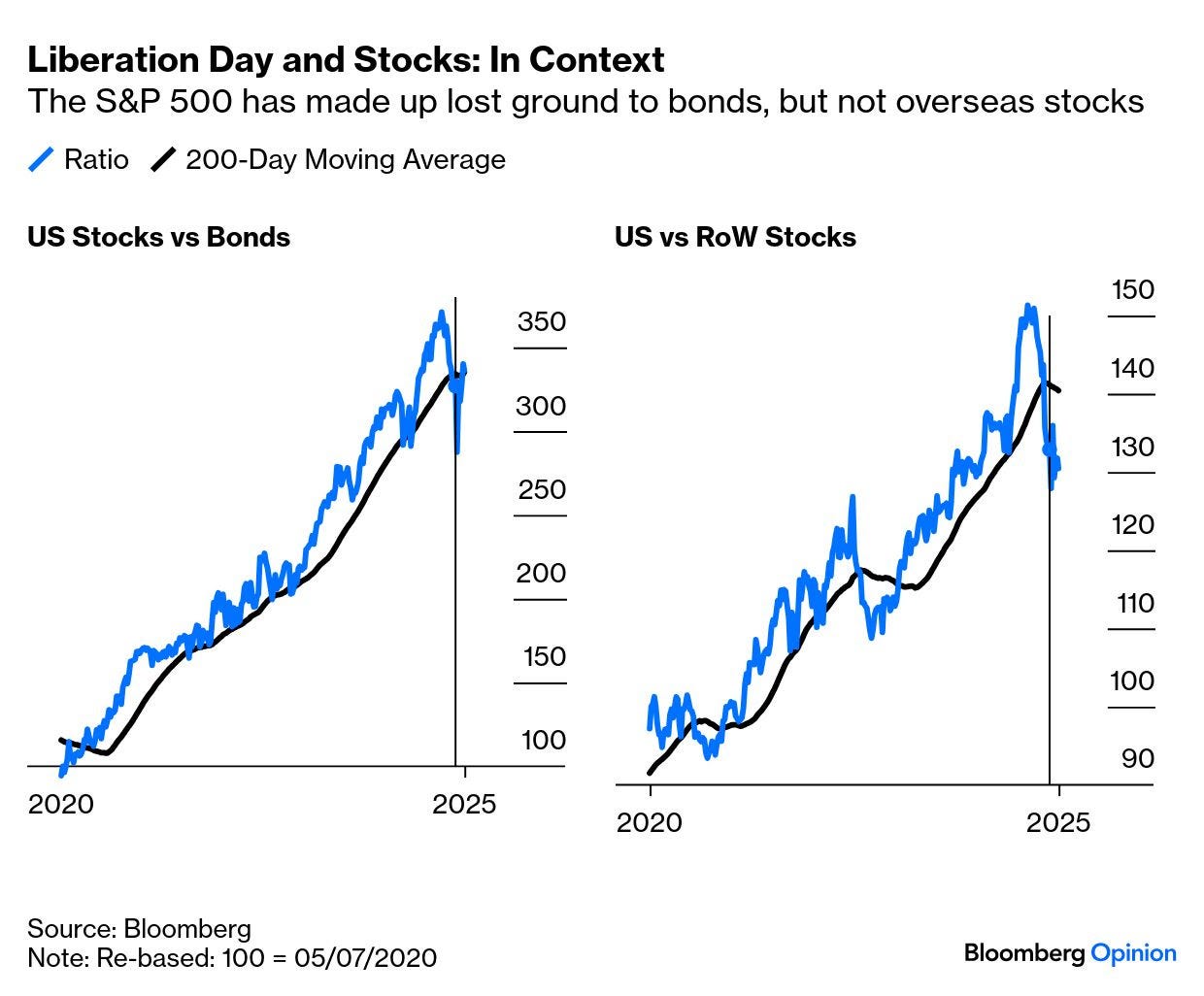

Where Next? Markets have now had five weeks to digest Liberation Day, and four weeks to adjust to President Donald Trump’s decision to pause the levies for 90 days for countries other than China. To date, there have been no concrete agreements to avert tariffs returning in full force, and 60 days or so remain to make them.

The behavior of key market gauges suggests an outcome in which growth continues (so stocks don’t fall behind bonds), but where equities elsewhere continue to outperform the US market. In this chart, US stocks and bonds are proxied by the SPY and TLT exchange-traded funds, and US versus rest-of-the-world stocks by the S&P 500 and FTSE All-World Excluding US indexes:

One explanation for this is that other central banks have much less of a tariff dilemma. For them, US tariffs are a purely deflationary shock (assuming they don’t retaliate by protecting against American imports). It diminishes their chances of economic growth, without having any upward impact on prices…

Never got invited TO Camp Kotok (not a fishin’ guy so that’s OK) but friends (Stu T) have and while I don’t know the guy … lots of respect for him and his informed view…

“I think the good parts are the Trump economy, and the bad parts are the Biden economy because he’s done a terrible job.” Donald Trump’s words, Meet the Press interview, May 4, 2025.

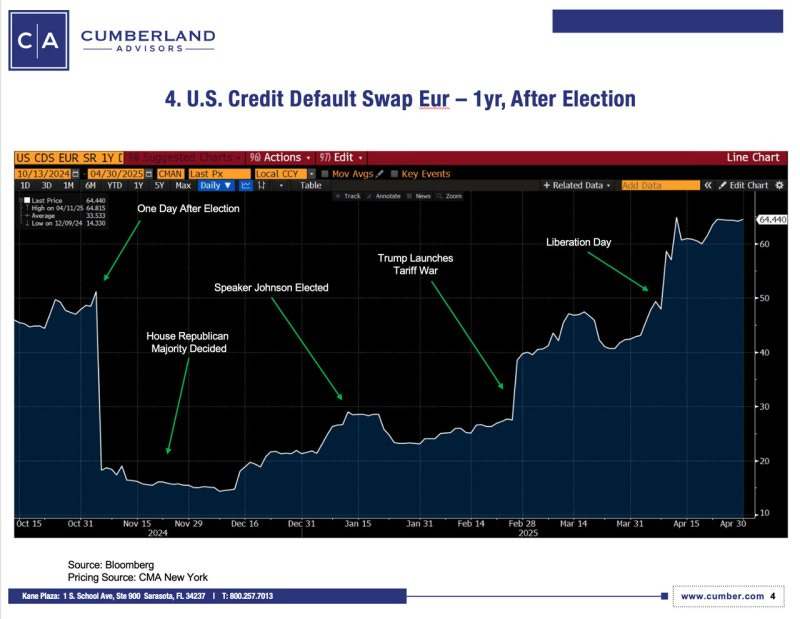

Today, a single chart provides a view of Trump’s first 100 days. Readers may evaluate the statement made by the president for themselves. The chart is sourced in market-based prices (Bloomberg terminal data).

A market-based price is simply the price at which a buyer and a seller agree to make an exchange. No one has to say why they are a buyer or a seller. The price speaks for itself. There are many opinions about why a price is what it is. But the price-setting mechanism reports only the results. All the rest is interpretation.

Here’s the chart, courtesy of Cumberland Advisors.

Here’s what the chart depicts. The United States is like any other debt-issuing country, company, individual, or enterprise. There is a market-based pricing mechanism to score the creditworthiness of the debt issuer. This mechanism is different from the opinion of a rating agency like Standard & Poor’s, Moody’s, or your personal credit score. This mechanism is an actual transaction price.

In the case of the United States, and other countries, the mechanism is the credit default swap (CDS). The CDS is a complex derivative contract, but what it does is very simple in concept. If the US pays, there is no default. If the US defaults, the defined default is the trigger. The referee is a global organization called ISDA, which stands for International Swaps and Derivatives Association. ISDA determines if there is a default by a published set of rules. ISDA has a reported 960 member institutions from 78 countries.

One party in the CDS contract collects a fee. (Think of that fee as an insurance premium.) The other party pays it. When there is an actual default, the insured party gets the settlement payment. If no default occurs, the insurer keeps the fee money. What you see in the chart is the pricing of the transactions by date on one of the CDS that insures the credit of the United States. The pricing in this chart is measured in basis points; each basis point is 1/100th of 1%.

Please note that, until now, the United States has never defaulted. We have noted a few dates on the chart to identify elements that may have changed the market pricing of the CDS.

The actual CDS trades are done worldwide and in the over-the-counter (OTC) market. CDS are not listed on American exchanges. The volume covered is in the billions. The US is a large-volume country because the US is the world’s largest debtor nation. About $29 trillion is the total marketable US Treasury debt, and that debt comes in various denominations from a very short maturity of only a few days for a cash management bill to as long as 30 years in the form of a bond. All American government debt is publicly known and is reported, audited, and monitored worldwide.

The takeaway from this chart and others like it is simple.

The behavior of Donald Trump in his first days as president has raised the cost of borrowing for the entire array of all federal agencies and all arms of the US government. The price shown is of one of the credit maturities.

The charts of the other maturities look about the same. Some key political dates and events are noted in the annotations. Readers are invited to draw their own inferences.

Here’s my bottom line in response to the president’s self-serving quote about how he is perfect and everything wrong is Biden’s fault. Trump has now achieved a market-based price for the creditworthiness of the United States that exceeds the single worst price on the single worst day of the Biden administration. There is one exception. That was the day before then-House Speaker Kevin McCarthy and then-President Joe Biden reached a handshake about avoiding a US debt default.

Note that, this time around, there is no imminent default risk. The so-called X date for the US Treasury is expected to arrive in August or September.

We have written ad nauseum about the disastrous economic tariff policies rolling out of the Trump 2.0 administration and how they are being advanced by the scandalous economist Peter Navarro. We have noted the worldwide broadcast of a mathematical error in a chart held by the president in the Rose Garden. Nothing is more revealing than that monster error when we are evaluating the economic policy of the US under President DT 2.0. (See “Math Gaffes,” https://kotokreport.com/trumps-math-gaffes/.)

I thank readers for their many emails and comments about our series on the impact of Trump tariff policy and Trumponomics.

There are some who still believe in him, as I have seen from reader replies. Others are now doubting their decisions about Trump.

IMO, this is all Trump now. He can finger-point at Biden all he wants. Biden, IMO, was weak and disappointing, and Biden didn’t act when he could have. But Biden is now gone. This is Trump. All Trump. And his enablers are accountable since he is a lame duck president who will do whatever he wants when he wants and as he wants without any apparent restraint.

The market-based prices of global CDS for the United States are saying that this is a dangerous time with a rising risk for the United States. I hope they’re wrong. I fear they may be right.

Wolf on FOMC

May 7, 2025 WolfST: Fed, Fully in Wait-and-See Mode, Keeps Rates at 4.25%-4.50%, Frets in All Directions: Higher Uncertainty, Inflation & Unemployment

QT Continues at Slower Pace, announced in March.

AND FINALLY, Consumer Credit …

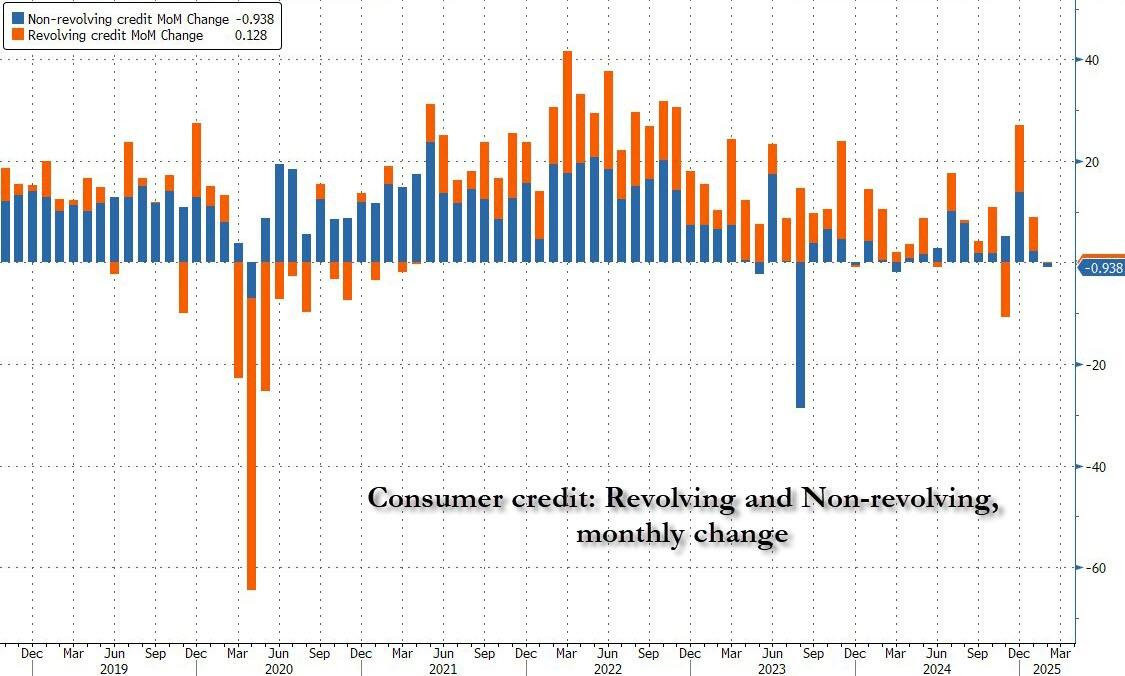

ZH: Consumer Debt Jumps In March As Student Debt Unexpectedly Soars

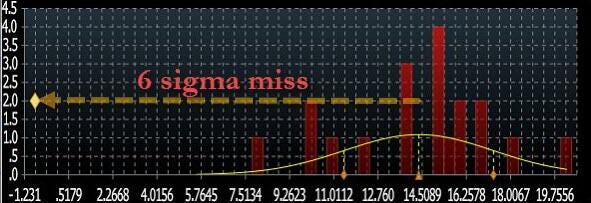

One month ago, just as our long-running narrative that US consumers had been living with maxed out credit cards for the past year was becoming mainstream, the Fed's February consumer credit data confirmed as much: a huge, 6-sigma miss to expectations of a $15BN print, when the actual number came in at a negative $1BN (and far below the lowest estimate)....

... as a result of both Revolving and non-revolving credit coming in flat or negative.

https://youtu.be/-OvQoCqXyjo?si=dzP5VQ3o2IVroxc5

Gundlach on Fed Uncertainty, Private Credit Pitfalls & Waning Momentum of U.S. Exceptionalism