while WE slept: USTs 'creeping' o/n bid ran into wall; S&P upgrade w/note on STOCKS > bonds, and 5000yrs of rates (BAML); daily 'evening stars' formed (CitiFX)

While the market has priced-out cuts in July, the Minutes show:

"Most participants assessed that some reduction in the target range for the federal funds rate this year would likely be appropriate, noting that upward pressure on inflation from tariffs may be temporary or modest, that medium- and longer-term inflation expectations had remained well anchored, or that some weakening of economic activity and labor market conditions could occur.

A couple said they would be open to considering a cut as soon as July if data evolved as they expected

Some saw the most likely appropriate path would involve no rate cuts in 2025. Those participants cited recent elevated inflation readings, elevated business and consumer inflation expectations and ongoing economic resilience.

Several said current Fed funds rate may not be far above its neutral rate.

All participants viewed it as appropriate to maintain Fed funds rate at the current target range…

… FOMC mins and 2 (auctions) down, $22bb long bonds to go … Now, worth noting that TLINE (and 200dMA) has held / is holding and so we’ll jump in to look at 30s with a fresh brand new set of crayola …

… as momentum has peaked, rolling over and having crossed BUT not yet getting a head of steam rollin’ down the hill … perhaps another push higher (yield, overSOLD momentum) will provide cushion and reason (ie dipORtunity) and I’d rather buy as market gets rollin’ OR on a cheaper / steeper dipORtunity …

NOTE — 55dMA more of a trend indicator than ‘support’ or ‘resistance’. A point of interest and especially as it appears to be relatively FLAT at moment (or maintaining a slight BEARISH bias) in contrast to overSOLD momentum as a signal.

Something ELSE not noted on the chart but in review … a step back, if you will, and one can start to see a H&S pattern formed / forming.

To be continued. Get those bids in for bonds early and often and i’ll move along but first … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT USTs saw another creeping overnight bid in USTs run into a wall at the Asia open, aggressive sellers emerging to push 10s ~2bps cheaper off the highs. Duration recovered somewhat with the help of the solid JGB 20y auction, while the LDN franchise saw good two-way activity in 5s & 10s, better selling in 10s from both RM and HF names. Cash volume was slightly over the recent average with 5s notably elevated, some dip-buying flows now being seen in the front end and intermediates from RM. SPX futures are showing -5pts here at 7am, the DAX +0.2%, and Crude -0.4%. Gold is supported +0.4%, while a bite of DXY weakness has resumed at -0.2% and AUDUSD +0.4%.

… 30yr Bond : Support at 5.00%. Resistance at 4.625%. Daily momentum: bearish

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: European bourses gain on potential China stimulus, US stocks and USD lacklustre despite trade updates …A contained start to the day, awaiting fresh trade updates. USTs in a narrow 11-06+ to 111-13+ band, the upper point is a marginal WTD high. Resistance ahead at 111-28, 111-20+ and 112-12+ from last week … Ahead, aside from Fed speak and a few data points, 30yr supply rounds off the week’s outings. A tap that follows relatively average 3yr and 10yr issuance this week, with no sustained move spurred by US supply thus far.

“It’s dangerous to underestimate Corporate America” Mea culpa for ignoring our own advice (above) on Liberation Day. The resiliency of large public companies in the face of macro uncertainty leads us to lower our equity risk premium (ERP) assumption. The benefit to valuation from a lower ERP is only partially offset by our higher normalized rates assumption based on persistent sovereign risk, yielding an increased S&P 500 year-end target of 6300 (from 5600) and a 12mth target of 6600.

The US isn’t exceptional, but Corporate America might be …

Short-term outlook: tepid to cool …

Medium to long-term: warm…

…and outright hot vs. bonds Remember, price return is only half the story –dividends are likely to contribute more from here. Dividend growth undershot earnings growth amid zero interest rate policy (ZIRP) which diminished the importance of cash return. But prior to 2013, dividends contributed ~40% of total returns. Aging demographics and sticky inflation create a compelling supply/demand case for inflation-proof income and easily favors stocks over bonds.

… Stagflation playbook: Value over Growth, stocks over bonds, dividends…

…Stocks > Bonds: corporate (stock) risk vs. sovereign (bond) risk

A few words from across the pond on our FOMC meeting minutes…

9 July 2025 Barclays: Federal Reserve Commentary: June FOMC minutes: Two step forward, some step back

The minutes of the June FOMC meeting reaffirm that participants are in no rush to adjust policy rates, even if "most" judged a rate cut would likely be appropriate this year. While "some" favor no rate cut this year, the minutes make clear that only "a couple" are considering a cut in July.

…We retain our baseline expectation that the FOMC will deliver a single 25bp cut this year, in December, with the economy slowing, the unemployment rate edging up, and the tariff-related inflation bump showing signs of having peaked. We then expect the FOMC to deliver three 25bp cuts in 2026. Our outlook remains highly uncertain and dependent on tariff rates.

Best in the biz (and yes, voting has begun once again …) on FOMC minutes and ‘the range’ …

July 9, 2025 BMO FOMC Mintues: Tariff Risks Elevated, "Most" Still Expect to Lower Rates in 2025

The Minutes from the June 18th FOMC meeting stuck with the prevailing messaging from the Fed -- persistent tariff inflation is a risk. Moreover, most officials look for lower rates this year while some saw no cuts this year. It was somewhat surprising to see the Minutes note that "A couple of participants noted that, if the data evolve in line with their expectations, they would be open to considering a reduction in the target range for the policy rate as soon as at the next meeting." Clearly the June payrolls report offers a counterpoint to any hopes of a July cut.

On the trade war, the Minutes highlighted that, “While a few participants noted that tariffs would lead to a one-time increase in prices and would not affect longer-term inflation expectations, most participants noted the risk that tariffs could have more persistent effects on inflation." In addition, "By contrast, if labor market conditions or economic activity were to weaken materially, or if inflation were to continue to come down and inflation expectations remained well anchored, then it would be appropriate to establish a less restrictive stance of monetary policy than would otherwise be the case.” This serves as a reminder that normalizing policy rates lower doesn't need the justification of a weaker economy or labor market, just cooler inflation and contained inflation expectations.

…Treasuries benefited from a mid-session, mid-week rally that left many market participants perplexed as to the underlying driver behind the price action. We’re squarely in the head-scratching camp. If nothing else, the 10- year auction should have provided enough incentive to prevent the market from rallying ahead of the supply event. Immediately ahead of the auction, 10-year yields had declined 8 bp from the session high print despite the conspicuous absence of any fundamental trigger. The observation was made on several occasions that the move appeared to be futures-led and presumably programmatic – which is classic coverall for inexplicable moves. Taking a step back, it isn’t all that surprising that the market managed to bounce after selling off for five consecutive sessions. Apparently, the market got a bit ahead of itself on pricing in a supply concession. The solid takedown of the 10-year auction only added to the buying interest.

There is a compelling argument that 10-year yields in the 4.40% to 4.50% zone represent attractive levels at which to add duration exposure. This is made all the truer in the context of a range-trading environment that we expect will hold for the next several weeks. The June payrolls report has effectively eliminated the path to a July cut and even brought into question the prudence of assuming that the FOMC goes in September – although the latter is still our base case. The June CPI details are unlikely to trigger a breakout further out the curve and a downside surprise would only solidify the case for a September cut – largely limiting any price response to the 2-year sector. Once the auctions have been fully absorbed, we’re open to the 10-year sector holding a range of +/-20 bp around the 200-day moving average, which is currently 4.33%.

This implies a reasonable range assumption of 4.13% to 4.53% this summer – parameters that resonate to us. For context, the Bollinger Bands (+/- two standard deviations versus the 20-day moving-average) currently come in at 4.210% and 4.484% – not dissimilar from our rough range estimate. 2s appear content toward the bottom end of the local yield range and any attempt to return above 4.0% will surely be bought. If for no other reason than the rhetoric surrounding Trump’s potential pick to replace Powell and all the dovishness such a move would imply…

France on tariffs and the read-thrus …

09 JUL 2025 BNP US: Taking stock of tariff pass-through

KEY MESSAGES

We introduce a six-point “taking stock” framework to track how quickly tariff costs may pass through to consumer prices.

With effective tariff rates moving close to full force in June, pre-tariff inventories likely to clear by late August, and firms planning near-immediate price hikes, we think a clear CPI pop should materialize in the July-September window.

Our base case – visible tariff pass-through in the July-September prints – keeps the Fed on hold through year-end. A cut later this year could be on the table if tariff-driven inflation fails to emerge this summer.

Interrupting macro / funDUHmentals for some technicals and levels to consider from best in the biz with regards to techAmentals … I’ll bring forward excerpt on long bonds but do note there are some levels for 2s as well as 10s which are equally funTERTaining …

Thursday, Jul 10, 2025, 3:23 CitiFX US rates: Change of pace

US treasury yields have posted evening star formations on the daily charts. These have been off notable resistance levels, and weekly momentum has been trickling lower. We think yields could come off in the short term as a result, but flag that support levels are relatively nearby.

…US 30y yields US 30y yields have also posted an evening star formation, after coming close tot he 5.00% handle again. Similarly, it suggests a turn lower in 30y yields. We see support at the 4.73% (Jul 1 low), followed by 4.66% (200d MA).

Weekly slow stochastics continue to tick lower after hitting 'overbought' territory. However, without accompanying breaks of support levels or a significant trend at the moment, it looks like 30y yields are likely to stay in a range.

German stratEgerist on a good auction helping the bond market to gains after 5 days of losses … also offering some thoughts / words / recap of FOMC minutes …

… Optimism largely returned to markets yesterday, even as the lingering threat of further US tariffs on August 1 remained in the background. Indeed, a tech-led rebound helped the S&P 500 (+0.61%) to stabilise after its losses at the start of the week, whilst the NASDAQ (+0.94%) and the German DAX (+1.42%) hit an all-time high. In fact, there was a significant milestone, as Nvidia (+1.80%) became the first company to surpass a $4tn market cap on an intraday basis, before closing just shy of that at $3.974tn. So for everything else that’s happening right now, from tariffs to fiscal fears, AI is the great hope for US exceptionalism to return. The rally also got a further boost as lower bond yields meant that fears eased about the fiscal situation, and a strong auction helped the 10yr Treasury yield (-6.7bps) to finally decline after 5 consecutive gains. So it was a strong day all round, even if there wasn’t really a fresh catalyst to drive things higher.

However, just when you thought it was safe to emerge from the July 9th tariff deadline day, we’ve had a fresh set of announcements after the US close that signalled a more aggressive stance. First, Trump confirmed overnight that the 50% copper tariff will come into place on August 1, which is an important one given its applications across various products. And second, he announced a 50% tariff on goods from Brazil, which is significant as it broke with the trend of tariffs being broadly in line with the Liberation Day levels set on April 2. Indeed, Brazil had a 10% tariff at that time, so that’s a notable escalation, and it follows Trump’s threats to place higher levies on the BRICS over recent days. So that meant the Brazilian Real weakened by -2.29% against the US Dollar yesterday, its biggest decline since April 4 amidst the turmoil after Liberation Day. We also heard about several other countries, but the Philippines was the only other in the US’ top 50 trading partners, and they were given a 20% rate.

Meanwhile on the fiscal side, there was a lot of attention on a 10yr Treasury auction yesterday given recent fears around the fiscal situation, but strong demand meant that yields continued to fall. So it helped to push back against concerns that demand for longer-dated bonds was waning. The auction saw $39bn of notes sold, and were awarded at 4.362% versus a 4.365% yield at the bidding deadline. The bid-to-cover was 2.61, above the average of the last six similar auctions (2.57). So attention will now focus on the 30yr auction later today.

That Treasury rally continued after the auction as the Fed minutes from the June meeting were released. They indicated a divide about how restrictive policy currently was, as well as the tariff impact on inflation going forward. With regards to the current policy stance, it said “ A couple of participants noted that, if the data evolve in line with their expectations, they would be open to considering a reduction in the target range for the policy rate as soon as at the next meeting.” So given recent commentary these could likely be Fed Governors Waller and Bowman. However, the minutes also highlight that “some participants saw the most likely appropriate path of monetary policy as involving no reductions in the target range for the federal funds rate this year.” Regardless, it said “several participants commented that the current target range for the federal funds rate may not be far above its neutral level”, indicating that any easing cycle may not lower rates significantly in the coming months. This growing divergence in expectations matches the dot plot distribution we saw last month, where 10 of 19 officials pencilled in at least two rate cuts this year while 7 officials saw no cuts, and the other 2 policymakers saw one cut.

On inflation, the difference of opinion was mainly on the effect of tariffs, even as there were questions on how inflation ex-tariffs was progressing. It said “Some participants observed that services price inflation had moved down recently, while goods price inflation had risen. A few participants noted that there had been limited progress recently in reducing core inflation.” Potentially the key sticking point going forward is that “while a few participants noted that tariffs would lead to a one-time increase in prices and would not affect longer-term inflation expectations, most participants noted the risk that tariffs could have more persistent effects on inflation, and some highlighted the fact that such persistence could also affect inflation expectations.” Looking ahead, the next FOMC meeting (July 29-30) will be just before the August 1st extension date for the “reciprocal” tariffs, so policymakers may still be awaiting clarity on what the trade levies going forward could look like even as they try and measure the impact from the tariffs already in place. In addition, oral arguments to the Court of Appeals on whether the International Emergency Economic Powers Act authorises the president to impose tariffs will be heard on July 31.

Ahead of the minutes, there had been fresh pressure from the administration to cut rates, as Trump posted that “Our Fed Rate is AT LEAST 3 Points too high.” And markets did move to price in more rate cuts yesterday, with the amount expected by the December meeting up +3.9bps on the day to 53.1bps. In turn, that helped sovereign bonds to rally across the board, with the 2yr Treasury yield (-4.8bps) down to 3.843%, whilst the 10yr yield (-6.7bps) fell to 4.332%. And that was echoed in Europe too, where yields on 10yr bunds (-1.4bps), OATs (-0.9bps) and BTPs (-1.3bps) all saw modest declines …

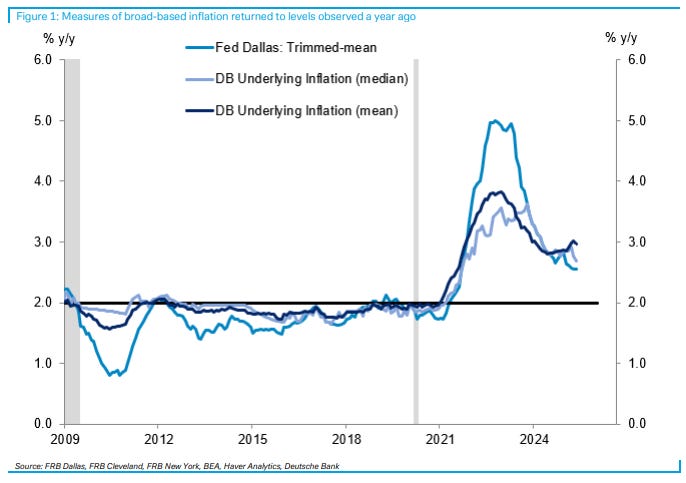

Germany on underlying inflation and what it may mean for cuts / NO cuts …

09 July 2025 DB: Fed cannot turn to trend inflation for cuts

The March PCE inflation readings marginally exceeded expectations; year-over-year headline PCE inflation rose 14bps to 2.34% while core PCE inflation increased by 10bps to 2.68%. Updating our suite of statistical models for the underlying inflation trend, we find that the monthly mean estimate for trend inflation fell by 5bps to 3.0%, while the median estimate dropped by 9bps to 2.7%. Both metrics suggest tentative signs of a resumption of disinflationary progress following a Q1 surge, although they remain elevated near levels observed a year ago.

Developments in trend inflation could become increasingly important over the coming months, as Fed officials try to differentiate between possibly one-off price level shocks triggered by tariffs and more persistent changes in inflationary pressures. We expect that these tariff effects could become more evident over the next few months. Proposals for further increases to tariff rates could pose additional upside risk to inflation over the next year. We recently noted that the newly announced round of tariff measures, slated to take effect on August 1st, would increase the average tariff rate by approximately 1.7 percentage points to 18.7% and add 15 basis points to inflation (see How high is the tariff rate? Updating our tracker to reflect Trump's letters).

A generic, yet always worthwhile, daily recap from a shop that is constantly tops in the II Excel voting …

USTs rally as solid 10y auction eases demand fears; BRL underperforms after US tariff announcement; June FOMC minutes show divergent Fed views; JGB curve twist-flattens after BoJ comments; global equities advance; BNM cuts rates; DXY at 97.50 (-0.0%); US 10y at 4.332% (-6.7bp).

…Bullish momentum returns with European and US rates rallying, and global equities advancing even amidst ongoing tariff developments.

Belly-led rally in USTs (10y: -7bp), after five consecutive sessions of losses. Rally accelerates after a robust 10y UST auction which comes 0.3bp through and is well-received (bid-to-cover ratio: 2.61x; 12m average: 2.56x), seemingly easing some concerns around demand…

… and an FOMC minute recap …

July 9, 2025 MS: June FOMC minutes: Still projecting cuts, but still a lot of concern about inflation persistence

The minutes to the June meeting highlight the tension between upside risks to inflation, which keep many projecting no cuts, and downside risk to labor markets, which keep many projecting cuts. The minutes read slightly hawkish to our ears in light of new tariff announcements.

Key takeaways

With growth in activity “solid”, the unemployment rate “low”, policy restrictive, and heightened uncertainty, the FOMC is still in wait and see mode.

"Most participants" still say that tariffs could lead to persistent inflation and risk destabilizing inflation expectations.

However, "many" say the effects of tariffs on inflation could be mitigated if "trade deals are reached soon" and others point to labor market concerns.

We continue to forecast no rate cuts in 2025, but 175bp of cuts in 2026 when any impulse to inflation is fading and real activity is slowing.

Another shop from across the pond weighs in on recent FOMC meeting minutes …

9 Jul 2025 NatWEST: US: Recap of the Minutes from June 17–18 FOMC meeting

The FOMC minutes did not shed too much new light on the policy outlook, which is not too surprising, in light of the post-meeting press conference and given all the Fed speakers since the meeting, including Chair Powell’s recent semiannual monetary policy testimony before Congress. The themes from Powell's press conference on June 18 (and several recent Fed speak) were evident in the FOMC minutes. (See our June FOMC recap here link.)

Ahead of the minutes some market participants wondered if the minutes might indicate whether anyone else on the committee was onboard with Governors Waller and Bowman of being open to the idea of a possible cut as early as the July FOMC meeting, but the minutes confirmed they are the only two officials with this view: "A couple of participants noted that, if the data evolve in line with their expectations, they would be open to considering a reduction in the target range for the policy rate as soon as at the next meeting."

As Powell has pointed out a few times since the meeting, the minutes stated that "Most participants assessed that some reduction in the target range for the federal funds rate this year would likely be appropriate, noting that upward pressure on inflation from tariffs may be temporary or modest, that medium- and longer-term inflation expectations had remained well anchored, or that some weakening of economic activity and labor market conditions could occur." (See our recap from Fed Chair Powell's congressional testimony here link.)

The minutes also noted that "Some participants saw the most likely appropriate path of monetary Minutes of the Federal Open Market Committee 11 policy as involving no reductions in the target range for the federal funds rate this year, noting that recent inflation readings had continued to exceed the Committee’s 2 percent goal, that upside risks to inflation remained meaningful in light of factors such as elevated short-term inflation expectations of businesses and households, or that they expected that the economy would remain resilient."

Of course, a variety of views among the committee allows the most flexible set of options around near-term policy, and was consistent with the wide dispersion we saw in the June dot plot (see dot plot recap here link). Our own forecast has not changed, we continue to expect that the Fed will hold off from any action until after Chair Powell’s term expires (May 2026).

One key passage in the June FOMC minutes which reiterated the policy outlook quite succinctly: "In considering the outlook for monetary policy, participants generally agreed that, with economic growth and the labor market still solid and current monetary policy moderately or modestly restrictive, the Committee was well positioned to wait for more clarity on the outlook for inflation and economic activity."…

Switzerland on the art of doing nothing (FOMC mins) …

9 July 2025 UBS: US Economic Perspectives An FOMC weighing conflicting risks

Outlook uncertainty, albeit diminished, remains the dominant theme At the June FOMC meeting, the Committee still faced tariff related uncertainty. Despite assessments that uncertainty had diminished somewhat, the basic message was policy was well-positioned to wait for more information or clarity. According to the minutes, most policymakers "assessed that some reduction” in the policy rate would be appropriate at some point this year. Only "some" disagreed, reflecting to some extent the division seen in the Summary of Economic Projections. Two participants considered a rate cut at the July meeting, presumably Governor Waller and Vice Chair Bowman, considering the post-meeting comments. There seemed to be little sentiment beyond those two for a July rate cut, despite somewhat wider sympathy for their concerns over downside risks to the labor market.

With a July cut seemingly off the table at this point, and we never expected one, two more months of data can make or break the case for a September rate cut, where we expect a 25 bp rate cut. Also of recent market focus, discussion of the monetary policy framework in the minutes was limited. The staff discussed risk management and ways of making monetary policy more robust to various conditions. Communications were also discussed. The minutes noted that the Committee expected to complete its review of monetary policy strategy by late summer, and that they would continue the discussion of communications after that review was completed.

Upside risks to inflation and downside risks to employment…

The Federal Reserve meeting minutes were a masterclass in the art of sitting on a fence. US President Trump’s trade tax inflation might be a one-off, or it might persist. The labor market may be weak enough to justify rate cuts, or not. Uncertainty over trade tax levels is a problem, but the real issue is the lack of clarity about the severity of second-round effects (e.g. profit-led inflation). Masterful inactivity seems the default policy option.

Most of Trump’s tax announcements yesterday were political theater—impressive sounding tariff rates on countries that are not major trading partners. The threat of a 50% tax on US consumers of Brazilian products is possibly more serious—Brazil does export food to the US, so a 1 August tax hike would raise these prices relatively quickly (given limited inventory). As a high frequency purchase, tariff-induced food inflation would be more visible to US consumers…

… Same (Swiss) shop with a rates update from a couple days ago which I’m just now stumbling on … Important as it’s a closing of a LONG (10s) …

8 July 2025 UBS: Global Rates Strategy Rates Map - Fiscal prolongs cycle like no other

US - Duration pick-up in 2027 smaller than expected but other caveats

We closed our long 10y US 10y at 4.40% in the current back-up of core yields. We had opened this long end May at 4.51% but then tightened the stop to 4.40% ahead of last week's jobs report. We think that we could see better levels to go long US duration again but the market has to get a better sense of US labour market dynamics, the impact of the Big Beautiful Bill (BBB) and a higher tariff regime without USD strength. We still think a 5-30s US steepener will perform in this environment. There is a risk that oil prices go below the UBSe $62/bbl base case for 4Q25 if OPEC+ adds another 548kb/d in September at its 3 August meeting, which would support duration.

A drop in US unemployment to 4.1% would indicate more labour market tightness, but the jobs report could be weaker than this headline suggests. The seasonally adjusted expansion of 74k in private employment would have been close to zero if the BLS had used the average seasonal adjustment of the previous three years (Figure 4). UBS economics points out that people stopped looking for work and left the labour force. Average hourly earnings also slowed. In addition, another challenge to duration longs would be the sudden emergence of tariffs in US CPI prices, but transmission seems to proceed more slowly than previously expected. The cumulative increase in imported goods prices at major retailers remains relatively modest at 3% since early March. UBS thinks that it could be not until the release of the July CPI data on August 12 that we see some tariffs reflected in prices. Our favourite position in US front-end rates remains the Z5-Z6 flattener.

Our revised estimates of US 10y equivalent supply as a percentage of GDP is still chunky albeit almost 2 percentage points lower in 2027 from our estimates at the start of the year (Figure 2Our evisdtmae ofUS10y equivalnt of+1ysverign suplyaercntg ofGDPis tlchunky albeitmos 2percntag pointslwer in207compared tousimae thsrofe ya.UBSeconmist welorbudget ficsvhe bginofthe yar,but ifrevnus adtblecoin dvelopmnts wilbeky factors ginforwad. ). UBS economists now see lower budget deficits vs the beginning of the year. Tariff revenues and stablecoin growth will be key factors going forward. The economics teams also thinks that BBB could support growth somewhat in 2025. UBS expects that US tariff revenues will average around $330 bn/yr or one percentage point of GDP annually. Stablecoin regulation looks set to support buying of US bills. More bill issuance could give the US treasury a little bit more time before it has to increase coupon auction sizes, but this will depend on growth of the stablecoin universe (currently at ~$240bn) and how much of the stablecoin demand will be net new demand for cash.

Also, if there is an economic slowdown now and a recovery in 2026-27, it may be that supply is rising just as demand is falling. So we think supply worries are significantly exaggerated right now, but the backdrop could be much more worrisome in late 2026/27 depending on the economic cycle.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

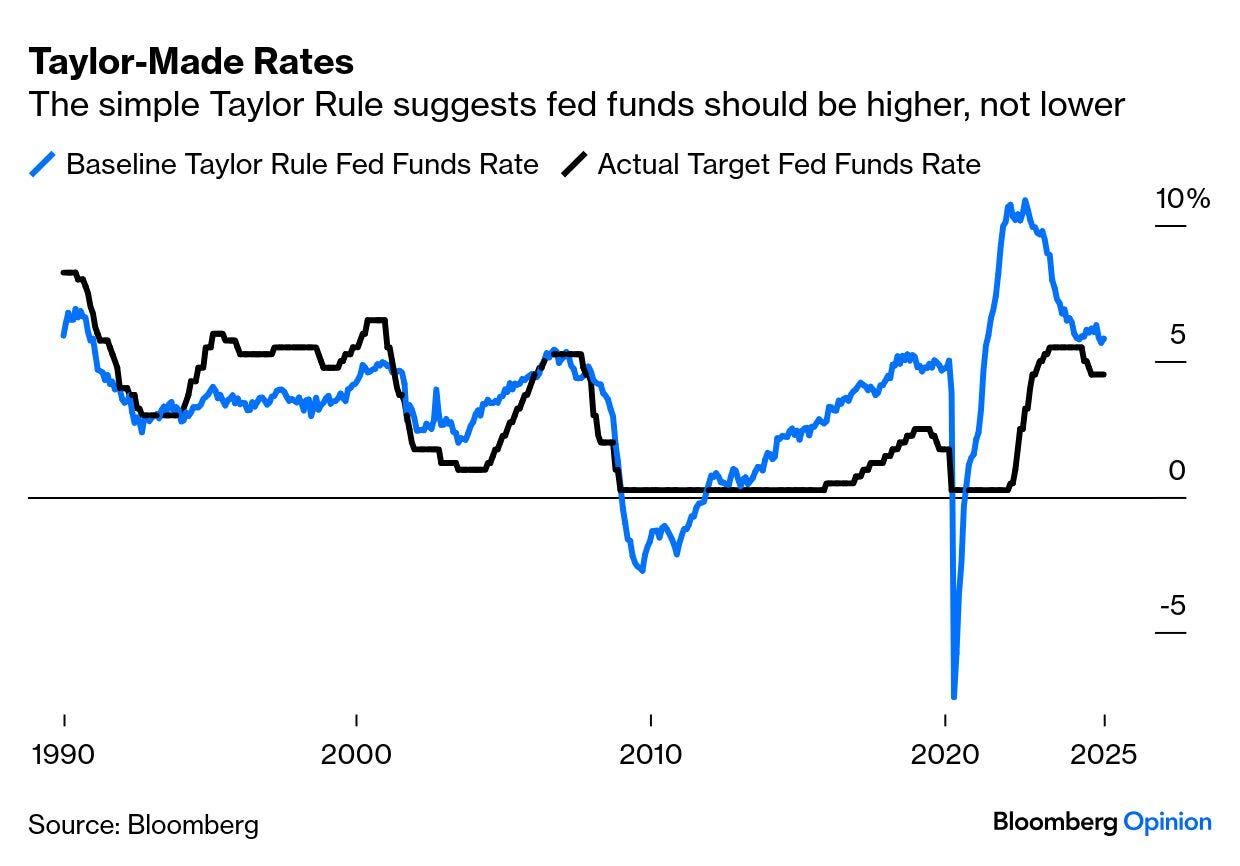

A view from The Terminal … with an excerpt on KEVIN (and how JT would have been worse, with his rules based FOMC setting idea) …

July 10, 2025 at 4:26 AM UTC Bloomberg: 50% tariffs are about punishment, not trade As if coffee didn’t already cost enough, squeezing Brazil means Americans will pay even more.

One little piece of history is of note. When Trump nominated Powell in 2017, the other top contender was John Taylor of Stanford University, who gave his name to the Taylor Rule, a mechanistic system for setting the fed funds rate using the output gap (the more output exceeds potential the higher the rate) and inflation (higher prices rises means higher rates). There’s room for argument over how good an idea this is, but it’s popular among conservatives as a sensible way to limit the Fed’s discretion. Applying the Taylor Rule now would require the Fed to raise rates:

The president may regret having chosen Powell, but by his lights Taylor would have been worse — and his case for massive rate cuts isn’t at all clear. Just witness the minutes from last month’s Federal Open Market Committee, published Tuesday. Nobody formally dissented, but there was evident disagreement. While “a few” participants said tariffs would not affect longer-term inflation expectations, “most”noted the risk that they could have persistent effects. It’s not just Powell.

Trump might bear that in mind. The Fed’s independence is a complicated issue, and the president’s advisers have made proposals for changing its governance. But in a crisis, the chair needs to be viewed as an independent actor. That will be hard for contenders now trimming their views to fit the presidential agenda. Last October, for example, Hassett said that the Fed’s “jumbo cut” a month earlier was justified. Now he says: “Jay Powell is the person who cut rates right ahead of the election to help Kamala Harris (and is) doing whatever it is that Elizabeth Warren wants.”

Should Hassett win the job, he’s likely to be viewed as a politician, not an independent. That could limit his room for maneuver. But at least it appears he wouldn’t follow the Taylor Rule.

AND with all THAT in mind, an IDEA for an updated portfolio construction model currently under review at some of the very largest managers in the world (no, not really) …