July 17, 2025 The Case for Cutting Now Governor Christopher J. Waller At the Money Marketeers of New York University, New York, New York

… I believe it makes sense to cut the FOMC's policy rate by 25 basis points two weeks from now. And looking to later this year, if, as I expect, underlying inflation remains in check—with headline inflation data reporting modest, temporary increases from tariffs that are not unanchoring inflation expectations—and the economy continues to grow slowly, I would support further 25 basis point cuts to move monetary policy toward neutral.

… You’ll see it being noted just ‘bout everywhere how he’s laid forth, again, his VIEW, rate cuts should happen. Soon.

Said another way, “May I play 1st base?”

As I always told MY 3 sons when coaching various rec league baseball teams … you NEVER ask but, whatever …

We’re still waiting for latest from HIMCO, too, and so, with all due respect … an updated and WEEKLY look at 10yr ‘breaks’ (definedas the diff between 10s and TIPS)…

… BREAKS breakin’ …

Mom always said, if you don’t have anything nice to say then don’t say nuthin, right? And so … IF one were inclined to view this chart technically — and I’m not sure I would given it’s via TradingView — no offense but NOT from a Terminal and so I’m not 100% confident of its content BUT — momentum (stochastics, bottom panel) IS suggesting BREAKS has moved towards overSOLD and so perhaps, just up above TLINE etched in here, there is reason for those betting on ‘flation to, say, put some hay in the barn.

Dare I say, read / re read Wall-E and cover shorts and go LONG, if, that is, you believe in the no-flation POV?

Just a thought and there are more, below, countering Wall-E and noting 10yr BREAKS breaking no bueno …

… helping shape shift the rates complex (along with all other, less important of markets on Global Wall :)) was some part of data …

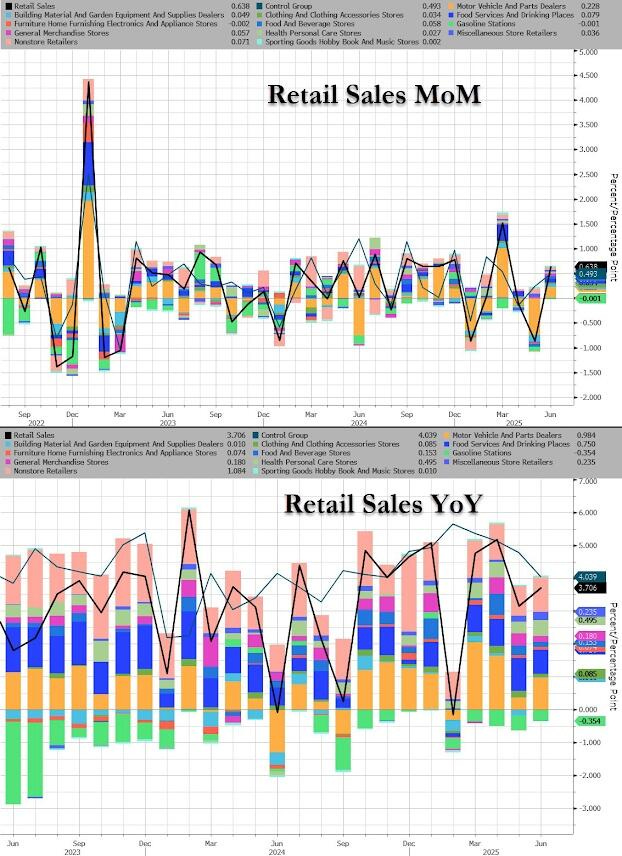

ZH: US Retail Sales Surged In June (Despite Sentiment Slump)

… Under the hood, Motor Vehicles and Auto Parts sales surged in June (yes this is AFTER the tariffs went into place and NOT due to any front-running)...

The Control Group - which feeds directly into GDP - also surged 0.5% MoM in June, leaving sales up 4.0% YoY..…

…So are spending outlooks from all those 'soft' survey just a load of partisan bullshit?

… lesson (never sell the ‘Merican consumer short) learned?

Nope. Nevermind … it was weak / bad and calling for the demand of rate cuts now!?!?

But what IF they — Americans — all losing jobs and economy about to fall off a cliff (Wall-E above), surely they’ll need more $$ handouts and rate cuts …

Bonddad: Jobless claims: the brightest spot in the entire economy right now

ZH: 'DOGE' Effect Accelerates As 'Deep Tristate' Jobless Claims Hit 4 Year high

The number of Americans filing for jobless benefits for the first time fell last week to 221k - the lowest in 3 months - as this high frequency labor market signal shows no signs of cracking for now. Initial jobless claims have gone literally nowhere for four years...

… Bright. Spot. So … in other words, rate cuts? Nope?

I give up and clearly been outta ‘the game’ far too long to offer a clear view. OR perhaps there isn’t one to be had?

Perhaps Dr. Lacy Hunt / HIMCO can / will help but for now … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Stocks gain, USD softer & USTs firm ahead of Fed’s Waller and earnings … USTs are firmer whilst Bunds underperform given the positive risk tone … USTs are trading higher by a handful of ticks today and currently within a 110-19 to 110-24 range and trading towards the peak from Thursday at 110-25. Focus has been on commentary from the influential Fed Governor Waller; he continued to bolster his calls for a 25bps cut in July; he is set to talk later today also. Elsewhere, on trade updates, the White House said the EU continues to be very eager in trade negotiations. Elsewhere, on US/China relations, US is set to impose a 93.5% tariff on graphite used for battery material from China. Attention now turns to US Housing Starts/Building Permits and UoM Prelim data.

Retail sales unwound a good portion of May's decline, posting a broad-based 0.6% m/m increase. June's estimates exceeded expectations, but come on the heels of downward revisions to April and May. In our view, the numbers are consistent with a soft, but resilient near-term trajectory of PCE.

Best in the biz on ReSale Tales and a daily recap …

July 17, 2025 BMO: Retail Sales Strong, Import Prices Soften, Claims Drop

Retail sales came in stronger-than-expected in June at +0.6% MoM vs. -0.9% MoM prior and +0.1% Mom anticipated. More relevant for growth estimates, the Control Group surprised on the upside at +0.5% MoM vs. +0.2% MoM prior (revised down from +0.4%) and +0.3% MoM anticipated. Import Prices came in at +0.1% for June vs. +0.3% consensus and -0.4% May (revised down from 0.0%). Ex-petroleum, Import Prices were 0.0% -- below the +0.2% forecast and matching May's revised level. On the employment side, Initial Jobless Claims unexpectedly fell to 221k in the week of July 12th (13-week low) compared to expectations for an increase to 233k. The prior week was revised up by 1k to 228k. On net, the 4-week moving-average fell to 229.50k (10-week low) vs. 235.75k prior. Continuing Claims printed at 1956k for the week of July 5th vs. 1965k surveyed and 1954k prior. The Philadelphia Fed Index surprised on the upside at 15.9 vs. -1.0 expected and -4.0 prior. This is a 5-month high. Prices Paid rose to 58.8 from 41.4. Employment jumped to 10.3 from -9.8. New Orders increased to 18.4 from 2.3 previous. Overall, the data netted upward pressure on yields as the consumer appears to be rebounding and employment is solid, even as imported inflation seems contained for the moment…

… Thursday’s trading session reiterated several of the key factors underlying the prevailing macro narrative. First, initial jobless claims printed below expectations at just 221k – the lowest since early-April and it was for NFP survey week. This implies that budding concerns regarding the trajectory of employment have been allayed for the time being. That being said, we’ll argue that the specter of a downturn in the labor market has been in place for months, and a single weekly claims print won’t alleviate the angst regarding the potential for a weaker jobs report at some point later this summer. The second key confirmation came in the form of a rebound in the pace of retail rales which surprised on the upside at +0.6% in June – well above the +0.1% consensus. Moreover, the Control Group outperformed expectations at +0.5% compared to estimates of +0.3%. This provided a meaningful offset to investors’ wariness regarding the overall health of the consumer when faced with the incoming price hikes linked to the new tariff regime.

A key caveat on retail sales is that the series isn’t inflation-adjusted and as a result, the upside might be partially a function of the uptick in ex-auto goods inflation revealed in the CPI release. We’ll reserve judgement until the real personal spending figures are available later this month. In terms of timing, the market will first get a look at the quarterly figures via the real GDP print on July 30 – FOMC decision day. The trajectory of real growth has been a bright spot for the US economy, despite the net exports-led dip in Q1. Anything that challenges the perception that US growth will continue will be new information – although we struggle to see anything immediately on the horizon that would do so.

The third point of reiteration from today’s data was the softer Import Price Index – with prices ex-petroleum now flat in May and June. There might be a looming wall of tariffs that will drive goods prices higher, but the current departure point for inflation remains benign. We’re not downplaying the risk of forward inflation linked to the trade war – rather, we’re reminded that the lower inflation was prior to the upcoming spike, the less likely it is that the next few months will prove to be a paradigm-shifting event for the macro landscape. There is undoubtedly an array of risks presented by Trump’s trade war, the ultimate outcome is still remarkably uncertain.

With this backdrop of confirmation, the relative stability in Treasuries indicates a market that has found a point of temporary equilibrium. The momentum measures also indicate that the market is oversold, a dynamic that implies a further consolidation or retracement lower in rates. 5-handle 30-year yields is a line in the sand, and we suspect that 4-handle long bonds won’t fade quietly into the background. Instead, the recent price action indicates that 30-year yields sustainably above 5.0% are yet another wildcard for the summer months. The Japanese election this weekend and any subsequent price action in longer-dated JGBs will be a contributing factor to the performance of US 30s – as well as the results of next week’s US 20-year auction. This all has created a set-up for choppy price action further out the curve as the 5.0% bond question is once again revisited….

German bank report on inflation expectations …

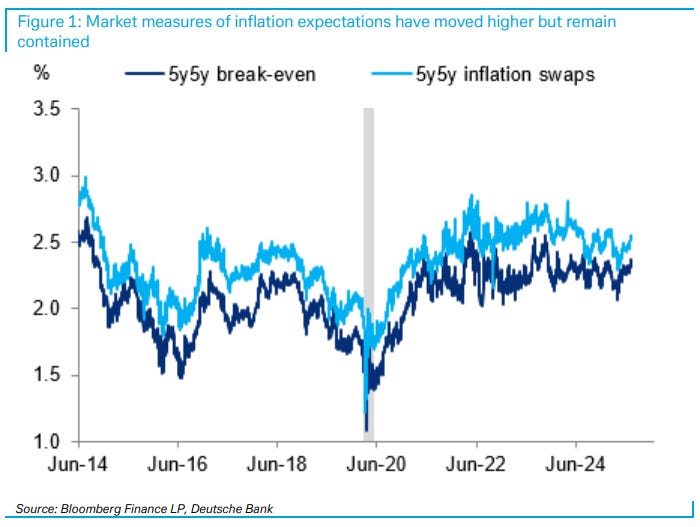

17 July 2025 DB: Market inflation expectations are less sanguine than they look

Despite a historic increase in tariffs and threats of more to come, as well as renewed risks that President Trump could decide to remove Fed Chair Powell (see “Is there a fire behind all the smoke?”), market measures of longer-run inflation expectations appear surprisingly well contained.

We show that the market signals are less sanguine once we strip out the impact of oil prices. On this metric, markets look to be pricing a premium that is near the highs over the past decade, a premium that may grow if the administration follows through on some of its threats around tariffs and the Fed.

… said another way, BREAKS breakin’ …

German bank note on hawkish fedspeak (save for the aforementioned Wall-E who spoke well AFTER this hit the inbox) …

17 July 2025 DB: Fedspeak stays slightly hawkish ahead of July FOMC meeting

We previously utilized our proprietary LLM tools to analyse the hawkishness/dovishness of various forms of Fed communications. Those analysis confirmed that by the May FOMC meeting, the scores of individual officials had become more hawkish – reaching a two-year high – as officials began considering tariff-induced inflation risks (see DB AI shows Fedspeak most hawkish since early 2023). In this piece we update this analysis to early July, prior to the latest round of tariff announcements, incorporating three additional regional presidents who will be voting next year.

The updated scores suggest that while there has been a slight dovish drift across many officials’ messages, the magnitude of change varied and the underlying divisions within the FOMC regarding near-term policy remain substantial. The scores for Governor Waller and Governor Bowman exhibited the most significant changes, with their scores now representing the most dovish levels within the Committee. This conforms with these two Governors being the only officials to possibly support a July rate cut. Conversely, scores from a majority of officials, including Chair Powell, were little changed and remained in hawkish territory, as they seek clarity on the tariff impacts over the coming months.

These scores were calculated after the last jobs report but before the latest inflation data and recent escalation of tariff threats. These recent events should reinforce the cautious signals we identify in prior Fedspeak. Our baseline expectation remains that some pickup in the near-term inflation data is likely to push the first cut out to December.

… AND a note from same German institution summarizing the day passed as well as the day ahead …

… Markets have put in a decent performance over the last 24 hours, with the S&P 500 (+0.54%) and the NASDAQ (+0.74%) both reaching fresh all-time highs with the global rally mostly continuing this morning. The advance was driven by another batch of positive US data, including higher-than-expected retail sales, and then a 5th consecutive weekly decline in initial jobless claims. So that reassured investors that the US consumer was still resilient, and that the mid-Q2 jump in jobless claims was a blip rather than a permanent trend. With the stronger data and a continued rise in market inflation pricing, investors dialed down the amount of Fed rate cuts expected this year to 43bps, the lowest this has been since February. So collectively there is a growing sense of the US economy continuing to run hot, despite there being less than two weeks now until the August 1 tariff deadline. Overnight Fed Governor Waller, regarded as a potential candidate to succeed Powell, has expressed his preference for a 25bps reduction at the forthcoming late July meeting, citing escalating risks to the economy and the strong possibility that tariff-induced inflation will not lead to a sustained increase in price pressures. Furthermore, Waller cautioned that he has observed signs of strain in the labor market, reinforcing the argument for lower interest rates. He'll likely largely be on his own for July which is why there's only been a couple of basis point change in December pricing overnight alongside a 1.5 to 2bps UST rally across the curve. So notable comments but not enough at the moment to get close to swaying the committee, especially given the other Fed speak yesterday that we outline later…

…Over on the rates side, US Treasuries saw some further unwind of Wednesday’s moves when speculation mounted about Powell’s firing. So we got the reverse trend of a flatter yield curve, a higher dollar and higher equities, which was consistent with growing confidence about Powell’s position. Admittedly, Trump issued a fresh call for lower rates, posting “Too Late:” Great numbers just out. LOWER THE RATE!!!” But that was consistent with his remarks for several weeks, and wasn’t interpreted as a fresh challenge to Powell’s position.

That curve flattening yesterday also came as investors dialled back the likelihood of rapid rate cuts, as the strong data was interpreted in a hawkish light. So the probability of a cut by September fell to 54%, down from 58% the previous day, although we're back to around 58% post Wallet in thinner Asian markets. At the US close the amount of cuts priced by December came down -3.2bps on the day to 43bps, its lowest since February 20 although its edged back up a basis point post Waller

The problem for the Fed contracts are that there are growing concerns about inflation, not least amid questions over how much of the upside in retail sales was due to price increases versus volume growth. In fact, the 2yr US inflation swap (+4.2bps) closed above 3% for the first time since March 2023, at 3.02%. And that concern was extending to longer horizons too, with the 5yr inflation swap (+3.0bps) also at its highest since March 2023, right before the regional banking crisis kicked off with SVB’s collapse. Matters also weren’t helped by higher oil prices, with WTI up +1.75% yesterday to $67.54/bbl…

ReSale TALES …

July 17, 2025 First Trust: Retail Sales Rose 0.6% in June

…Implications: The consumer showed some signs of life in June, with retail sales rising after two months of declines…Given that the retail sales report largely reflects goods purchases (which are import-heavy), we expect ongoing trade negotiations to keep volatility high going forward. Looking at the details of the report, June’s advance was broad-based with ten out of thirteen major sales categories rising. The largest increase, by far, was in the volatile auto sector, which rebounded 1.2% after a 3.8% drop in May (now up 6.5% in the past year). After stripping out autos along with the other typically volatile categories for building materials and gas stations, core retail sales posted a solid 0.5% gain. These sales are up 4.5% in the past year – above the 3.9% increase for overall sales – but have been slowing in 2025, up at a 3.8% annualized rate through June (which includes the bump from tariff front-running)…While this report appears to contrast with other signs of a slowing economy, we remain cautious given the potential delayed effects of tighter monetary policy…

Claims and ReSale Tales …

17 July 2025 ING: US jobs and spending numbers suggest little need for an imminent rate cut

Firmer retail sales and subdued jobless claims numbers suggest the Fed will keep rates on hold for now as officials assess the impact of tariffs on inflation

A couple from Mike Gapen as he’s hitting stride at his new shop …

July 17, 2025 MS: US Economics: Retail Sales: Consumer resilience continues

Retail sales rose 0.6% m/m and control group sales rose 0.5%. This print is in line with 2Q real consumption growth at 1.7% (q/q saar). Real consumption accelerated in June and held up in Q2, despite initial price increases from tariffs.

Key takeaways

Headline sales rose 0.6% m/m, surpassing MSe of +0.2% and consensus of +0.1%.

Control group sales rose 0.5% with most categories up except furniture and electronics. Tariff impacts on spending across different categories are inconsistent.

We now track 2Q real consumption growth at 1.7% q/q saar and 2Q real GDP growth at 2.2%. We expect real consumption in June accelerates to 0.3% m/m.

Auto sales rebounded by 1.2% m/m in June after two months of declines.

Restaurant sales recovered, rising 0.6% in June, with upward revisions to May as well.

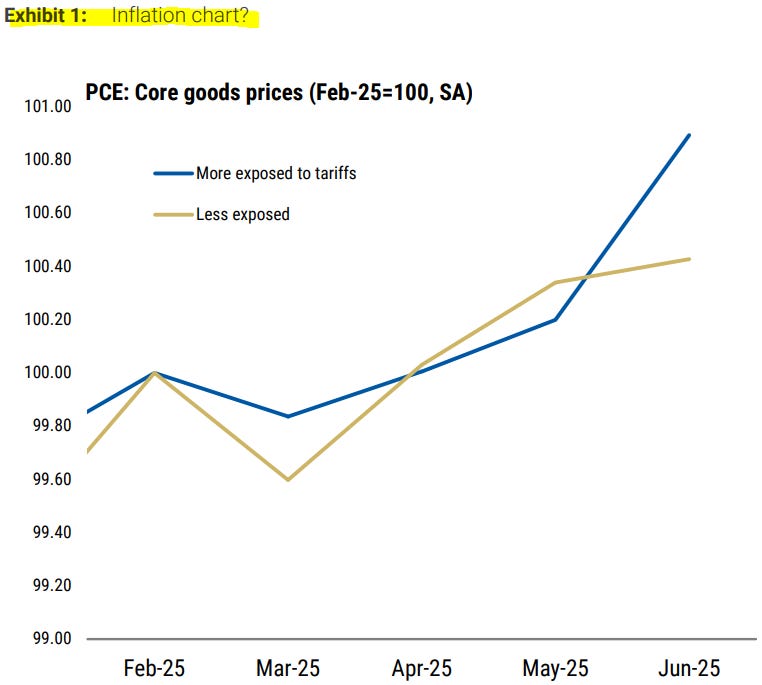

Clearer signs of a tariff-driven acceleration in core goods prices in CPI this week. Despite higher prices, consumption remained resilient. Looking ahead we expect more inflation over the summer, slowing growth, but a low unemployment rate due to restrictive immigration policy.

Key takeaways

CPI inflation accelerated in June with clearer signs of a tariff impulse. We see core PCE at 0.29%m/m.

Retail sales were solid. We expect real spending +1.6% q/q saar in Q2, including acceleration in June. Spending growth has slowed but no new signs of weakness.

We still expect slower growth, a tariff-driven H2 pickup in inflation, and backloaded Fed cuts.

Tariff announcements raise downside probabilities, but fiscal is now an upside risk for next year.

… hey Mike … you askin’ or tellin?

ReSale Tales recap / victory lap from across the pond …

Retail sales come in better than expected in June. Overall sales advanced by 0.6% m/m (consensus & NatWest +0.1%) in June after weakness in April (-0.1%) and May (-0.9%)…

…The details of the June retail sales report point to a reacceleration in the pace of spending in Q2 after the soft start to the year. Going into the retail sales report, we were expecting an increase of 0.4% or so in nominal personal consumption for the month of June and now estimate nominal PCE to have risen by 0.6%, which would translate to real PCE growth of 0.3% last month. If realized, that matches our Q2(25) real PCE spending estimate of 1.7% q/q, annualized rate after a 0.5% q/q, pace in Q1(25). (Note: We still forecast overall Q2(25) GDP at 1.5%q/q, ar.)

After this week’s events, the question is whether anyone can advocate for US rate cuts without being seen as a political puppet? Yesterday, Federal Reserve Governor Waller offered some (debatable, but valid) economic points in favor of US rate cuts, but the position is politically tainted. The problem for the Fed and markets is that the US administration’s policy continues to create considerable uncertainty about the economic outlook.

Political partisanship will be delayed in the Michigan consumer sentiment data (Republicans live in the best of all possible worlds, Democrats live in the worst of times—according to survey evidence). Inflation expectations are further distorted by frequency bias. Trade taxes are disproportionately weighted to durable goods, but the prices of these are less obvious to consumers as low frequency purchases…

Covered wagons on ReSale Tales and separately on tariffs …

July 17, 2025 Wells Fargo: Broad Gains Across Retailers as Sales Beat Expectations

Summary Strong June retail sales show consumers may have been spooked by tariffs, but they haven't fully gone into hiding. The fact that June is a slower month and that goods outlays comprise a fraction of overall outlays means that we are not completely rethinking our forecast for a soft second half for consumer spending.

… The June data indicate even if consumers have been spooked by tariffs, they haven't fully gone into hiding when it comes to spending. Control group sales, which exclude volatile categories that are captured elsewhere within GDP accounting and act as a good proxy for goods spending, rose 0.5% in June. While that out turn suggests some upside to Q2 personal consumption expenditures, taken with the downward revision to control-group sales in May, we expect PCE is still tracking relatively close to our estimate for a ~1% annualized gain for the second quarter…

July 17, 2025 Wells Fargo: Few Signs of Foreign Exporters Absorbing U.S. Tariff Hikes

Summary If foreign exporters were absorbing the cost of tariffs, U.S. import prices would be declining in proportion to the rise in the tariff rate. Yet, nonfuel import prices, which exclude the cost of tariffs, rose 1.2% year-over-year in June. The dollar's slide has likely incentivized foreign suppliers to bump up or hold the line on their invoice prices. With little relief on import prices, domestic firms are stomaching the cost of higher tariffs and starting to pass it on to consumers. We suspect import price growth has room to weaken in the coming months amid weaker demand but do not look for a plunge.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

There is a lot of chatter surrounding the Federal Reserve. The FOMC, etc. What the President will or will not do. What can be “successfully” done or not. Will Powell be fired?

Today, Kevin Warsh is floating the idea of better aligning the Fed and Treasury, as has been the case in the past (so I’m told).

Even if Powell is “fired” it is a committee and the committee won’t do anything drastic.

The front end might rally a bit, but “we” will lose control over the long end.

Why not think more outside the box? There are a few things we know:

The President thinks rates are too high.

The President (and Bessent) are focused on the 10-year and believe that is also too high.

The President has no problem (at least on tariffs) dictating specific numbers.

Why would this administration only do something halfway?

If you are going to do something radical – why not go all the way?

Cut interest rates – by ensuring the Chair and Committee are on board with it. I cannot say that I’ve given any thought to how to reset the committee, but I’d be surprised if that was more difficult than making changes at the top of the house?

And there are people on the committee who already have more rate cuts in their “dots” than is priced in. It may also be safe to presume that if the Chair was dovish, some people might move their dots, as a cut here or there is already probably too precise for all the guesswork involved.

Align the Fed and Treasury. Seems strange, but is it really that wild?

If rates out the curve don’t perform as expected (move significantly lower in response rate cuts) then why not just “set the curve”? The Fed has done QE (bought treasuries). The Fed has done Operation Twist (bought/sold treasuries to influence the shape of the curve). It isn’t the first time since the GFC that we’ve chatted about the potential for yield curve control: if the Fed is going to set rates in a world where longer term rates are likely more important than short term rates, why not set those too?

Who knows if anything will happen. But presumably, by May of next year at the latest (and that seems like a lifetime away) we will see changes in how the Fed behaves.

I’m not arguing against Fed independence and the dual mandate, etc., but you can see the appeal of going in a different direction.

Set yields across the curve. Issue debt to take advantage of these yields. Save “trillions” in interest rate expense. There is no easier way to lower projected annual deficits than by reducing costs. That would actually help lower yields too.

If long end treasury yields cannot bear the brunt of potential reckless Fed policy (because of yield curve control) then the dollar will likely be hit hard.

Yeah, there is always “strong dollar” rhetoric, but imagine a world with higher tariffs AND a cheaper dollar? Imports look way more expensive and the U.S. exports start to look a lot cheaper.

A materially weaker dollar may be viewed as a “feature” not a “bug” if your primary goal is more manufacturing in the U.S.

Again, no idea how this will play out, but expecting only one “radical” move seems a little “naïve”? If you are going to reshape something (like monetary policy) why not reshape it all the way?

In any case, maybe we should be spending less time thinking about “how much steeper will the yield curve go” if something happens to the Fed, to what would you do to ensure long end yields don’t rise?

Just thinking out loud, but if we are going to get “radical” why wouldn’t we get really radical?

Inflation expectations are breaking out and approaching 3-year highs.

Markets aren’t stupid.

While the talking heads debate whether tariffs are inflationary or deflationary, here’s what’s really unfolding:

▪️Money supply is hitting new highs ▪️A shadow Fed Chair is in the mix ▪️Commodities are broadly moving higher ▪️The U.S. dollar is on track for its worst year since the 1970s ▪️And a “Big Beautiful Bill” is already in the works

In my view, a resurgence of inflation is already underway.

When the Fed first started doing "Quantitative Easing (QE)" in 2009, it was a new concept. Nobody had ever seen the Fed do that before, so it was hard to know what the outcome was going to be. We now have seen 4 different rounds of QE, and the conclusion is pretty obvious that doing QE boosts liquidity in the banking system, and it boosts the stock market.

Similarly, doing the opposite known as "Quantitative Tightening (QT)" takes away liquidity and hurts the stock market when the Fed has done it too aggressively. But there are other ways that the Fed's interventions in the banking system can affect liquidity.

One of the wonkiest of these is via Reverse Repurchase (RRP) Agreements. Stay awake for a moment, please, as I explain why this is important. A regular "Overnight Repurchase Agreement" involves a transaction between the Fed and a member bank, where the Fed buys assets (usually Treasuries) from the bank and gives the bank cash equivalents. That boosts the bank's immediate liquidity, and it has helped the stock market in past years when the Fed used to do it more frequently. The transaction involves an agreement for the Fed to sell the same assets back to the bank sometime later.

The opposite transaction is a "Reverse Repurchase Agreement", which involves the Fed selling Treasuries to a bank in exchange for some of the bank's lesser quality holdings. This is done usually to make a bank's balance sheet look better, with more Treasuries and less stinky stuff on it. We see it happen in a big way at the end of every calendar quarter for window dressing, and now recently at the end of each month too. A RRP ties up banking liquidity, keeping it from doing other useful things like helping to lift stock prices. So not surprisingly there is a correlation between the total amount of RRPs the Fed is engaged in and the movements of stock prices.

That is what this week's chart shows, although I have made a couple of adjustments. The first is that I have inverted the scaling of the RRPs data, and then the second is I have shifted it forward by 5 trading days to show how there is a lag time between changes in RRPs and the echo in stock prices.

A few months ago, some analysts were worried about what would happen to the stock market uptrend when RRPs got to zero, and could not go any further. That premise is a bit flawed, because the Fed could always just do regular overnight repurchase agreements, and inject liquidity that way. And what we have seen is that RRPs bottomed out (topped in this chart’s inverse scaling) and have been trending to larger numbers since then.

It is normal to see big spikes for window dressing at the end of each month and quarter. But then the RRP data usually get back quickly to where they were before. That is not happening (yet) this time, which says that there is trouble brewing.

Because the close nature of the relationship between the SP500 and RRPs (inverted) may be a little bit hard to see in the chart above, I have replicated it in a different way, doing what I try almost never to do, and having the data from the two plots mix together in the same space on this next chart.

Doing this scaling adjustment allows us to better see the tight correlation between what RRPs did and how the SP500 reacts (5 days later). The large magnitudes of the end of month and end of quarter spikes may not show up so much as big moves in the SP500, but the dance steps are still there.

We just had the standard end of quarter spike at the end of June, and there was a minor dip a week later in the SP500 to honor that. But what is troubling is that the RRPs are not diminishing (going higher on the inverted scale) in the days after that end of June spike. Banks are continuing to hold onto the Fed's Treasuries, and that should be having an effect on financial market liquidity. The SP500 is not yet reflecting that change in the liquidity pool, but I sense that such a change is brewing. The two plots have gotten too far apart now, and so something is going to have to give.

Banks and the Fed are the best sources of solid liquidity, but sometimes liquidity can arise temporarily just out of bullish investor sentiment. The bombing of Iran's nuclear facilities arguably changed investor sentiment in a big way, and that optimism has helped to push up stock prices to a new price high without the backing of banking system liquidity due to the action in RRPs. Sentiment-based liquidity can very easily go away, though, which is the big risk for the market now, especially if the RRPs data stay like they are.

ReSale TALES …

Jul 17 2025 WolfST: My Thoughts about those June Retail Sales

Tariff-frontrunning ruffled the numbers earlier. That dust has settled.

…At gas stations (#6 category, 7% of total retail), sales move in near-lockstep with the price of gasoline. The price of gasoline started heading lower in mid-2022 and has continued to move lower. And so have gasoline sales in dollar terms.

Sales in June were roughly unchanged from May, at $50 billion seasonally adjusted, and year-over-year were down by 4.4%.

Three-month average sales fell by 0.6% month-to-month and by 5.6% year-over-year (red).

The three-month CPI for gasoline fell by 0.6% month-to-month and by 10.7% year-over-year (dotted purple):

https://open.substack.com/pub/growingupaspen/p/crash-crypto-and-the-conman?r=2g93c&utm_campaign=post&utm_medium=web&showWelcomeOnShare=false