Good (UNFORGETTABLE) morning and a happy Flash Crash-A-Versary …

On February 25, 2021, there was an unusual "flash" event in U.S. Treasury markets. The prices of Treasury securities dropped sharply amid strained liquidity conditions, before recovering within about an hour. This event follows several similar episodes in recent years, including the flash event of October 2014, which was discussed in the Joint Staff Report on the U.S. Treasury Market on October 15, 2014 (PDF). Given the key role played by the Treasury market as the largest and most liquid sovereign bond market in the world, it is important for policymakers to understand the nature and causes of these episodes. This Note discusses what happened on February 25, what we currently know about the likely causes, and how it compares with previous similar episodes… -FEDS Notes, May 14, 2021 (The Treasury Market Flash Event of February 25, 2021)

…And as we celebrate this milestone and at same time, wonder if they really know whatever happened, one thing is for certain. The more distance between now and then, the less and less folks will care.

Being ‘there’ that day, though, did instill an amount of uncertainty which was / IS unforgettable …

… backing up the tape a sec TO how yesterday panned out …

ZH: 'No Panic, But Discomfort Is High' - Bonds & Bullion Bid As Momo-/Meme-Stock Meltdown Continues

… As today's macro data just piled on the pressure for the "growth scare" narrative...

…Volumes remain elevated but, as Goldman notes, liquidity is getting a bit thin.

Futures were higher overnight on the now ubiquitous dip-buying after Friday's pain, but as soon as the US cash markets started trading, all the US majors puked into the red with only The Dow able to get back to even. The Nasdaq was the biggest loser on the day. A late-day puke (through key technical) levels left stocks at the lows of the day...

Critical technical levels were broken today across all the majors...

…US Treasury yields were down across the curve (2-4bps) extending Friday's decline..

… AND moving right along, here is a snapshot OF USTs as of 624a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: NQ underperforms amid reports US is looking to tighten chip controls on China, USD lower whilst USTs gain … USTs are firmer, picked up a touch on Monday’s strong 2yr outing before grinding marginally higher overnight and then lifting back above the 110-00 mark to a 110-09 peak in the European morning, a high the benchmark has remained in proximity to since. Ahead, the speakers continue with Barr & Barkin due before POTUS signs his latest executive order. Amidst that, the US will sell 70bln of 5yr notes; follows a 2yr which saw a slightly softer b/c than the prior but still a strong level of demand, particularly for the indirect figure.

KEY MESSAGES Our updated and expanded analysis shows that prominent seasonality patterns tend to persist each year for the major asset classes.

Q1 tends to start with a weaker USD, stronger EM FX, and an equities rally.

Q2 usually starts with a weaker USD and stronger commodities.

Q3 typically starts with declining yields and a rally in equities and EM FX, while the end of Q3 tends to see higher yields.

Risk generally rallies in October and declines in November. The pattern is most prominent in equities,rates and FX.

Our out-of-sample backtest shows reasonable risk–reward across asset classes, with an overall Sharpe ratio of 0.36. Some assets exhibit very strong seasonal dependence with a Sharpe ratio between 1.0 and 2.0, highlighting the importance of considering seasonality in the short-term outlook for assets.

Seasonality is the strongest in DM rates and EM FX.

Our update includes 2024 returns and increases the total number of assets analysed from 95 to more than 270, adding G10 FX crosses, DM rates (curves, ASW), EM rates (vs core), equity sectors (outright and RV vs benchmark)….

Ever find yerself wondering what has gotten smoked the most so far this year? Done BEST? Well, this morning is your lucky day …

Markets often behave inconsistently, with patterns that don't make obvious sense across asset classes. This got us thinking about where some of the biggest dislocations are today, considering what looks odd, and therefore what might be ripe for a correction.

Several sprung to mind over the last month. In particular, the market has simultaneously priced in higher US inflation over the next year, as well as more Fed rate cuts, even though the labour market has also surprised on the upside. Meanwhile in Europe, risk assets have seen a strong outperformance to their global counterparts, despite successive downgrades to growth forecasts and the looming threat of tariffs. And speaking of tariffs, it's clear markets are still highly sceptical they'll happen in full, with some of the most tariff-sensitive assets now above their levels prior to Trump's inauguration.

1. The last month has seen markets price meaningfully higher US inflation risk over the coming year, but more Fed rate cuts, even though the labour market has surprised on the upside as well.

In the last month, the US 1yr inflation swap has risen from 2.66% on January 24 to 2.98% on February 24. That follows several tariff threats, along with a January CPI report that surprised clearly on the upside, with headline CPI at its strongest monthly pace since August 2023. And there are further price pressures in the pipeline, with Bloomberg’s Commodity Spot Index currently around a two-year high.

But despite all that, futures were pricing in 50bps of cuts by the December meeting at last night’s close, clearly above the 42bps priced on January 24. So investors are pricing in slightly easier Fed policy than last month, even though they see more inflation risk.

Ordinarily, this could be explained via the other side of the Fed’s dual mandate, about the labour market. But the most recent jobs report was also stronger than expected, with unemployment falling back to 4.0%, and payrolls seeing decent upward revisions.

2. European risk assets have clearly outperformed their global counterparts, despite successive downward revisions to growth forecasts and the looming threat of tariffs…

…3. Some of the most tariff-sensitive assets are doing better now than before the tariff threats were being seriously made…

…4. Despite multiple high-impact events this year, broader measures of volatility have remained very subdued by historic standards…

…And the MOVE index of bond volatility recently traded around its lowest in the last 3 years. That speaks to the broad resilience of markets, with the S&P 500 having not seen a 10% peak-to-trough correction since October 2023.

Here’s a Treasury market daily note with a few choice words on 5s …

JPM: US Treasury Market Daily 5-year auction preview

The Treasury curve continued to bull steepen today with front-end yields falling 3bp. Tomorrow we will receive a slew of Fedspeak, and comments from Lorie Logan on the future of the balance sheet bears watching

Treasury is set to auction $70bn 5-year notes tomorrow. Overall given lower yield levels, mixed valuations, and poor technicals we think tomorrow’s auction will require more of a concession in order to be digested smoothly …

Dip-OR-tunity required OR … perhaps some sort of politically manufactured growth scare? That’s fine too …?

Moving along, here’s an interesting update that hit inbox just ‘bout midday …

MS: Cross-Asset Playbook: Everything Everywhere All At Once Our key views and top trades in one place.

Macro – Predictably Unpredictable

An uncertain macro impact from uncertain US tariff and immigration policies means the Fed stays restrictive even as disinflation progresses. Europe is at cruising speed. China remains at risk of protracted deflation but there are signs regulatory tightening could end soon.

…Macro Outlook | US – Slower Growth, Stickier Inflation Combined effect of imposition of new tariffs, immigration and fiscal policy changes lowers growth and lifts inflation. Fed cuts by 25bp in 2025, but leaves policy restrictive…

…Macro Outlook | Policy Rates – It’s Harder to Get Easier in the US Potential changes to trade, immigration and fiscal policy in the US drive the FOMC to stay restrictive. But in the euro area and UK, central banks continue to lower rates.

Markets – Up- and Downside Risks Rising

A base case of a ‘happy medium’ macro backdrop is good for risky and risk-free assets. Cycle-tight spreads show credit is priced for this, while rich equity valuations reflect animal spirits and assumptions around US exceptionalism, tariffs and geopolitical risks that cannot all hold true. The skew of outcomes is for equity and credit risk premiums to rise.

Strategy – Pare Back Equities, Add to Bonds

We move EW in global equities, paring some risk on deteriorating risk/reward; our preference for US and Japanese stocks remains unchanged. Turn OW on ‘core’ high-quality fixed income via adding to government bonds, while still maintaining an OW in spread products (e.g., leveraged loans, CLOs). Add long OTM puts in CDX as a cheap downside hedge.

…Top Trades | Long UST 5Y Investment theme: US yields peaking

Long 5s so, plenty of narrative selling assisting Bessent — country’s best bond salesman — this week?

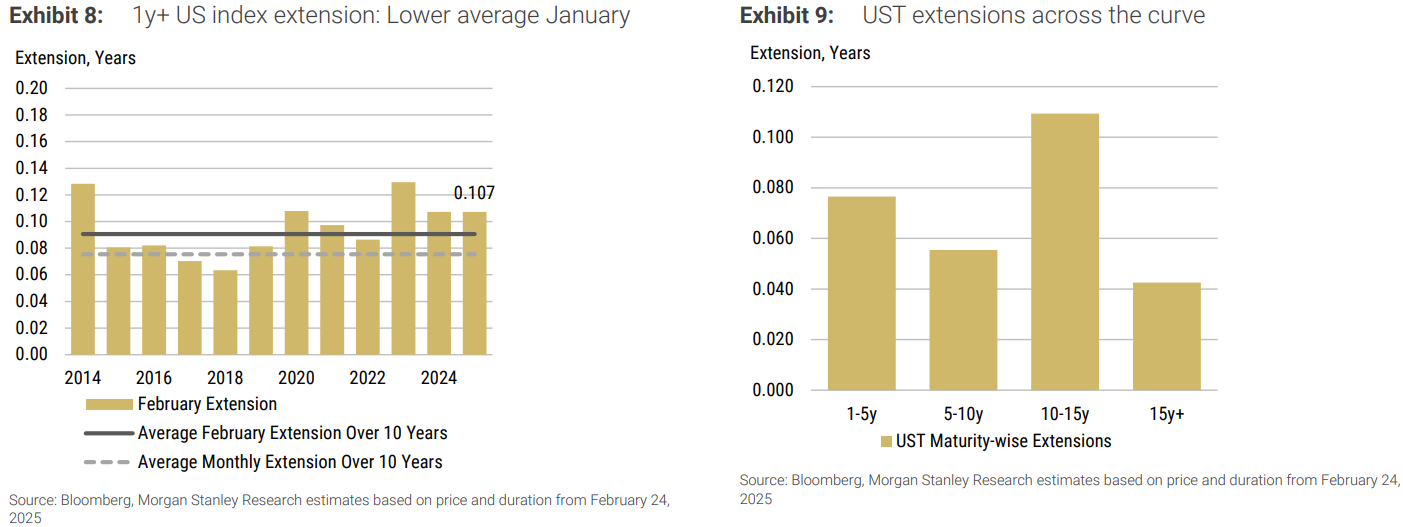

Eurogovies extend by 0.075y, marginally higher than Feb avg, higher than monthly avg; USTs 0.107y, higher than avg; UKTs to extend by -0.020y, lower than monthly avg; Eurolinkers extend by 0.010y, lower than average; TIPS to extend by 0.129y, higher than Feb avg of 0.123y.

…United States We expect the 1y+ UST index to extend by ~0.107y, compared to an average February (0.075y) and an average month (0.091y) – Exhibit 8 . A total of US$324 billion of supply (offered amount) will affect the extension, and US$301.5 billion market value of bonds will fall out of the index. The monthly issuance of 2y, 3y, 5y, 7y, 10y, 20y, and 30y will affect the respective maturity-wise indices.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

The Terminal with a FEW thoughts on bonds and DOGE …

Bloomberg: DOGE Chainsaw Is Setting Up Yields For A Soft-Patch Authored by Simon White, Bloomberg macro strategist

US yields are biased lower in the coming months as the economy adjusts from pro-growth Trump euphoria to the reality of a new administration that appears to be intent on making significant reductions to government spending.

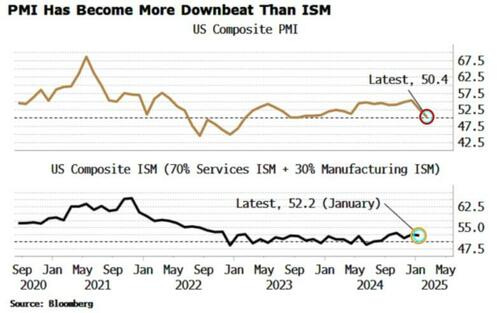

The flash PMI for February, released last Friday, may well have been the shot across the bows to expect a weaker period for the economy and therefore for yields in the coming months. The drop in the composite index was driven by a fall in the services component, due principally to greater uncertainty in the business environment, tariffs and government spending cuts(with DOGE figurehead Elon Musk recently holding aloft a chainsaw gifted to him by Argentina President Javier Milei).

The PMIs have had a much better read on the US economy over most of the last 12 months.

The ISMs were too pessimistic, anticipating much weaker growth that failed to materialize.

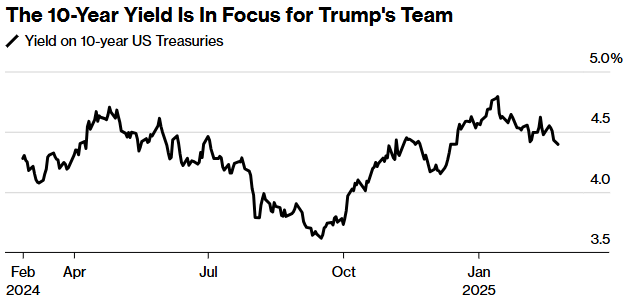

Yields were initially in sympathy with the ISM, but belatedly began to better reflect the PMI, rising from 3.6% in the run-up to the election to their current level around 4.4%.

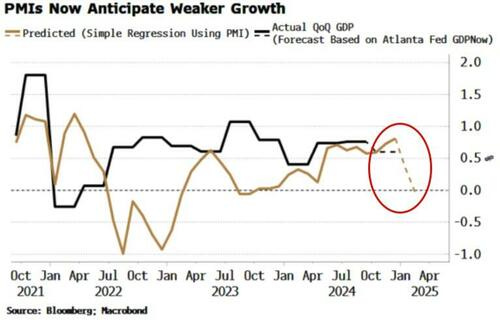

Now, though, the PMI expects a drop in growth. The chart below shows projected quarterly GDP based on a simple regression with the PMI.

The usual caveats apply, no regression is perfect, and month-to-month data is volatile. So while we don’t need to take the PMI literally at the moment in terms of it projecting flat growth in the current quarter, we should take it seriously given the impact from DOGE, and from tariffs, could be at least cyclically significant for growth (also making a re-acceleration in growth, which PMIs had been pointing towards, less likely).

That would mean a soft patch for US yields ahead.

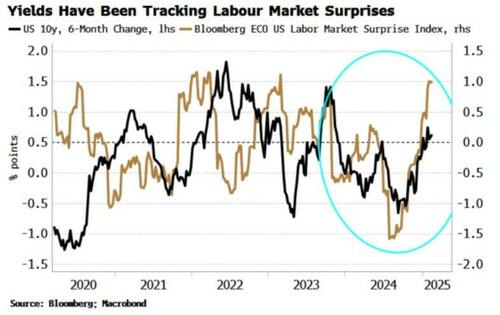

Yields have been rising along with labor-market economic surprises, as expected weakness in the jobs market also failed to materialize.

At the same time soft-data surprises (survey data such as the ISM and market-based data) have been falling, which yields have not yet so far been reacting to.

But that could soon change if sentiment is damaged by DOGE cuts, and yields fall.

Secularly, however, the picture for yields is supportive as Treasuries face a longer-term demand problem driven by supply, entrenched inflation, and a fall in demand for dollar reserve assets as the US considers a resetting of the global monetary system in a mooted “Mar-a-Lago” accord.

… AND

Bloomberg: The Bond Market Isn’t Fully Buying What Musk’s DOGE Is Selling US Treasury yields offer a scorecard for the White House’s cost-cutting vows

…“The bond markets do not currently reflect the savings that I’m confident we can achieve,” he said during a freewheeling, hour-long discussion he led on his social media platform, X. “If you’re shorting bonds, I think you’re on the wrong side of the bet.” …

… “The Fed has very little reason to cut rates,” says Kathryn Kaminski, chief strategist and portfolio manager at AlphaSimplex Group. Kaminski’s one of those investors Musk was speaking to the other day — the crowd who’s betting against Treasuries. She sees the whole policy mix, from the tax cuts to the tariffs, as an inflationary cocktail. “The trend in the bond market is still for higher long-term rates.”

Musk and the White House did not respond to requests for comment….

AND AND …

Bloomberg: Treasuries Rally as Traders Boost Bets on Fed Interest-Rate Cuts

… Markets are growing more confident that the US economy is weakening and interest-rate reductions will resume, as uncertainty around the Trump administration’s policies weighs on business expectations. An auction of two-year notes drew strong demand on Monday, after data Friday showed the services sector contracted for the first time in two years in February. “Red flags are emerging for the US economy,” said Elias Haddad, senior market strategist at Brown Brothers Harriman. “Another month or two of poor US economic data would deliver a blow to the US exceptionalism narrative.” …

For your inner global MACRO monday TOURIST …

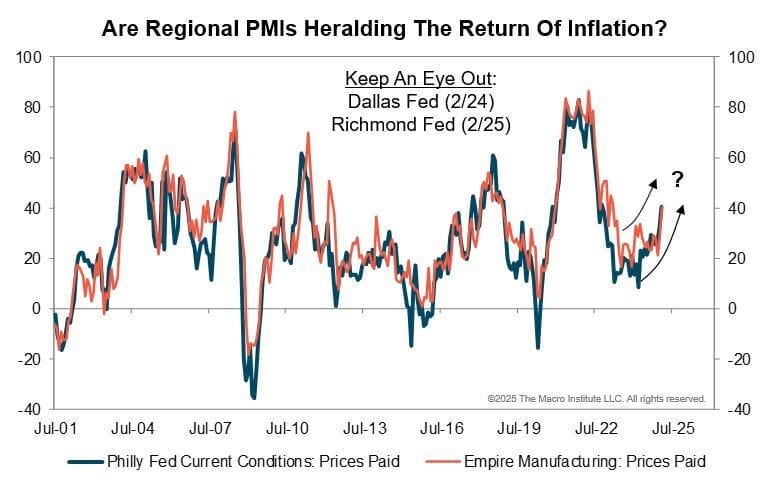

Macro Monday: Regional PMIs Are Telling An Important Story

This week is packed with key data drops, including Q4 GDP and core PCE inflation. Our main focus, however, will be on the regional PMIs. Inflation signals in both the NY Fed Empire Index and Philly Fed Index skyrocketed in January - if this trend holds, it could shake up the Fed’s playbook and rattle markets. Up next: the Dallas Fed Index later this morning and the Richmond Fed Index tomorrow. We’re zeroing in on their Prices Paid components to see if last week’s inflation warning was a fluke or the start of something bigger. Time will tell…

"Sex Castration and Butthole Zapping: NSA CIA confirm secret 'Kink' chatroom". As the mighty Musk so eloquently stated "at least we know what they were doing now" 😜😂🤣

"Sex Castration and Butthole Zapping: NSA CIA confirm secret 'Kink' chatroom". As the mighty Musk so eloquently stated "at least we know what they were doing now" 😜😂🤣