ZH: 7Y Auction Stops Through Despite Muted Foreign Demand

… especially if you bot bonds this week (or since ‘47 took over …). A veritable three-peat with regards to supply. Which apparently created it’s own demand. Along with healthy dose of growth-scare …

After the bell, though, it would seem all was well …

ZH: Nvidia Blows Away Expectations As It Sells "Billions" Of Blackwell Chips, Stock Goes Nowhere

Bloomberg: Nvidia Gives ‘Underwhelming’ Report After Two Years of Blowouts

CNBC: Nvidia sales grow 78% on AI demand, company gives strong guidance

… Before NVDA, though, after the bell, there was lots to consider / price in leading up TO and then after the 7yr auction …

This all in mind, bonds are DOWN today and I’d think they are still a good ‘sale’ … here’s why …

10yy: bottom of the ‘channel’ is now ‘support’ up near 4.30 …

… and if we get up above 4.30% as momentum (stochastics, bottom) cross and hook higher, well, increasing confidence on RENTING of a short-position … just thinkin’ outloud and as always, keep your friends close, your STOPS closer …

AND with that in mind, lets jump in as always, here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWKUS Market Open: NVIDIA +1% in pre-market after Q4 results, a pick up in yields lift the Dollar ahead of US data … Pick-up in US yields provides reprieve for USD, USD/JPY eyes a test of 150 … USTs are softer, given the constructive US risk tone as NVIDIA results weren’t the near 10% move that options had been implying, though of course it remains to be seen how they will open in today’s session; with tariffs and energy strength also influencing. As it stands, USTs are at the bottom of a 110-14 to 110-26 band. While softer, the benchmark remains comfortably clear of yesterday’s 110-08 base. Ahead, a slew of Fed speak and Q4 GDP & PCE second readings and weekly claims are due.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Always good to begin with an update / look back on THE Fed Put …

ABNAmro: US - Trump policy forces Fed to stay put | Insights newsletter

The Trump administration is moving at a blistering pace, with little regard for institutions or law. Inflation and inflation risks picked up over the past month; labour market risks also increased. Fed effectively paralyzed, unlikely to change rates…

… While we wait for the impact of Trump’s policies to materialise, the underlying macro picture continues to evolve. GDP growth remained robust at 2.3% SAAR for 2024Q4, predominantly on the back of strong consumption. The January unemployment rate ticked down again to 4.0%, after a relatively solid jobs report. The big surprise came from January inflation which came in hotter than expected, with a headline CPI rate of 0.5% m/m, and core CPI also increasing by 0.4%. On the more positive side, PPI data suggests core PCE will come in at 0.3% m/m, and an update of seasonal adjustment factors made the last months of 2024 look marginally more benign. Still, disinflation has stalled, and while pressures from wages and shelter have largely subsided, the outlook compared to last month has moved towards increased upside risks stemming from both tariff and non-tariff pressures.

Considering the above, the prudent approach is for the Fed to stay put. Compared to the start of the easing cycle, the labour market looks better, and inflation risks tilted to the upside. Evolving fiscal policy is likely to have a bigger impact on the inflation rate than the unemployment rate, tilting the Fed towards a more restrictive stance in the future. Further easing in the near term would be risky. In light of the dual mandate, there appears to be no real benefit to easing at the current juncture, except to please Trump. Rather, easing risks a future U-turn, hurting credibility at a vulnerable time.

Like to think of myself as a global macro tourist of sorts so notes / thoughts like this next one I found particularly interesting, especially in the timing given the shift in the narrative happening in front of our very own eyes …

As US data soften, clients have started asking us about the prospect of a US recession. We think the odds are still low, but have clearly risen. A US recession remains improbable, but is no longer unthinkable in the coming quarters.

… There are other factors to consider as well. A $30trn economy cannot be boiled down into just four drivers. Tariff-related uncertainty could stall new business investment plans, especially with the incessant "will they-won’t they" that has been the pattern in recent weeks. There are some anecdotal signs that US Big Tech might be getting ready to slow the massive AI spend of the past two years, as evidenced by a recent interview by Microsoft's CEO. On the other hand, small business sentiment has improved sharply since November 6, and animal spirits coursing through the economy could be a growth positive. And household wealth has risen so much that equities would have to pull back very sharply for wealth effects to turn negative.

In sum, it would need a large number of things all going wrong simultaneously for the US to stumble into a recession this year. But a slowdown relative to 2024 is very likely – indeed, it is now our base case. And for the first time in months, the prospect of an eventual recession, while still improbable, no longer seems completely unthinkable.

Technicals, schmecnicals? I disagree and in addition TO some words of caution offered HERE …

…We’re cognizant that the closing level relative to the 200-day MA will be closely watched for a skew on the near-term direction of rates. Should we see a rally breakout toward lower yields, a modest volume bulge centered around 4.20% should offer some resistance before a yield trough from December at 4.126%. Note that daily stochastics remain convincingly in favor of lower rates but have very limited room to run before crossing into overbought territory. Should we see a bearish reversal, initial support comes in at the 100-day moving average of 4.383% before a narrow opening gap from Tuesday at 4.396% to 4.400%. If that zone is filled, there aren’t any obvious technical impediments in the path back toward 4.50%…

Ahead of tomorrow, Friday … weekend — good — but then there’s S&P price action …

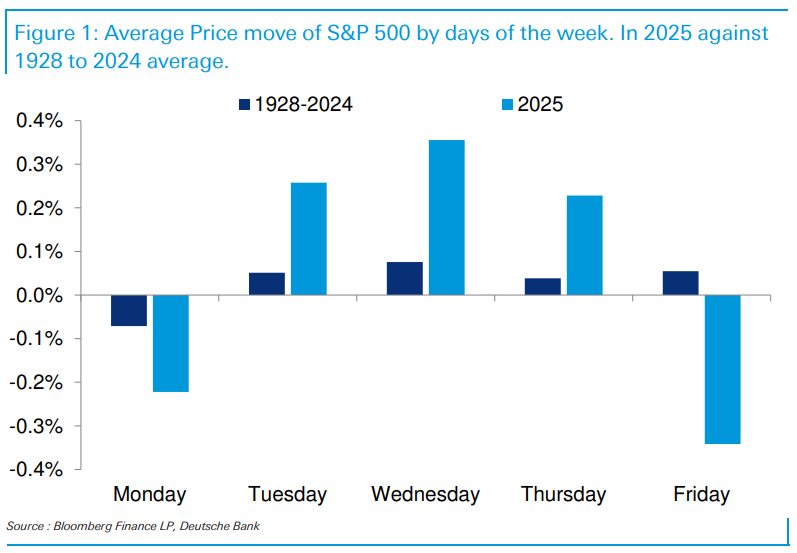

…It's been a funny year where it's been mostly risk-on for the US market but with huge under-performance on Mondays, and in particular on Fridays. Today's CoTD looks at this daily trend for the S&P 500 in 2025 against the long-term average from 1928 to 2024.

In 2025, Fridays have been terrible and Mondays only a little better. There does seem to have been a trend of potentially negative news coming through late in the week with the market wanting to reduce risk ahead of the weekend in case of escalation (e.g. tariffs on Mexico and Canada). Or, concerns that the weekend will bring fresh headline risk. The fact that Mondays haven't been a lot better suggests the threats haven't totally gone away but by the middle of the week markets have tended to come to terms with these stories.

In a world with lots of headline risk it's possible traders will continue to want to be lighter heading into weekends than they would be if markets were calmer.

Longer term, Fridays have been only just behind Wednesdays as best day of the week on average for US equities. In median terms it's the best. However, Mondays are still the worst day. So, in normal times, like with all things in life, we tend to get happier and more optimistic the closer to the weekend we are! Not in 2025 though.

… looking away from tomorrow, asking IF you’ve ever wondered about CapEX through history …?

We are currently in the midst of a once-in-a-generation private sector capex boom as AI mania sweeps the world. The largest US companies dominate this spending, and investment commitments announced by the top four in recent weeks suggest aggregate capex could rise by more than a third, to around $340bn this year. Amazon has indicated it will invest around $100bn, mostly on AI-related capabilities, and Microsoft nearly as much, with Alphabet spending around $75bn and Meta Platforms up to $65bn. That's higher than the annual GDP of Greece (population around 10 million) or similar to that of Egypt (population around 113 million).

Capex booms have recurred throughout economic history, often driven by transformative technologies or speculative fever. This report looks at several historical capex booms and busts – from 18th century canal building and 19th century gold rushes and railway mania, to late 20th century real estate and tech bubbles – and compares their dynamics to the ongoing 2020s boom in artificial intelligence (AI) investment. We examine each boom’s characteristics (asset price surges, leverage, overinvestment patterns), and why they saw a bust even though the underlying technology was ultimately transformative to the economy and productivity. We use this to understand whether there are similarities to the current AI capex boom, and importantly what the differences might be.

There are also capex booms that were transformative to economies and productivity, but which did not experience a bust phase. Those that did not see such volatility tended to be originated by public money. Both routes have seen transformative impacts on productivity, but different levels of financial market volatility.

As will be seen when we go through the examples, there are many parallels in today's AI capex boom to private-sector booms and busts through history. The most soothing conclusion is that today's capex boom is being paid for largely out of earnings and not debt. As such, if we do see a big unwind it likely will not be as systemic as some of those mentioned in this report. The biggest risk we see is perhaps through the wealth-effect channel, given how concentrated US equity markets are to the AI capex boom…

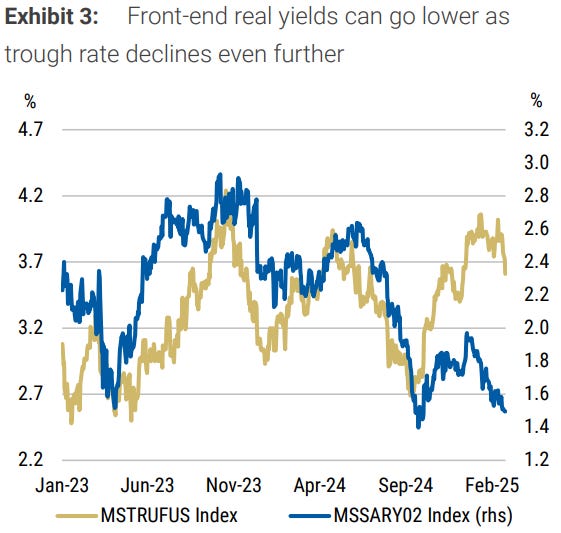

TIPS have rallied over the past month, & we think this momentum can continue as the carry profile turns positive starting in March. Front-end real yields can go lower from here as investors evaluate immigration and tariff policies lowering US GDP in 2025-26.

Key takeaways

Real yields fell significantly over the past month, and we think there is more room to go as carry for TIPS is positive for next 6 months.

We like 2-year TIPS as they offer a good volatility-adjusted carry profile & will likely benefit from lower repricing of trough policy rate on growth concerns.

Our estimates for core CPI fixing for the month of February is at 29bp M/M and March is at 9bp M/M, and the latter looks too cheap.

CPI fixings ex energy commodities have been pricing in 10 bp M/M higher inflation for May and June over the past month, likely because of the effect of tariffs

We maintain short 10-year breakevens as they look rich on a beta-weighted basis compared to 10 year USTs; we enter long 2-year TIPS.

…Our economists have modeled the impact of these policies independent of each other (see Exhibit 4 ):

1. Immigration: Our economists think immigration will fall to 1mn this year and 500,000 next year from the current rate of 3mn per year. In their base case, this could lower growth by 0.4% this year and 0.6% by next year.

2.Tariffs: The impact of 25% tariffs on Mexico and Canada and 10% on China would be around 0.7% to 1.1% . In an alternate scenario, 60% incremental tariffs on China and 10% blanket tariffs on all US imports would likely lower growth by 1.4%. The negative impact of tariffs on US growth is likely to be experienced in 2026.

The combined effect of both these policies would likely lower US growth by about 1.5% to 2% by 2026. This does not include the effect of counter-tariffs. We now recommend long 2-year real yields as a trade because:

Tariffs and retaliatory tariffs are both negative for economic growth

Uncertainty around tariffs is also negative for growth

It is a positive carry trade

It can benefit from market pricing of a lower Fed policy rate as growth slows down (see Exhibit 3 )

We are taking gains on our five-year Treasury long implemented in November, but remain long the intermediate part of the yield curve.

Recently, nominal yields have been coming down owing to the decline in real yields, indicating slower growth.

We continue to believe interest rates will decline by year-end, but trim some of our exposure, as the market is currently pricing in 60bps of Fed rate cuts in 2025.

…Yields rose steeply to start the year, as the Fed kept rates steady, the economy continued to prove resilient, and the new administration was viewed favorably by equity markets. However, with increased policy uncertainty there has been a temporary risk off sentiment which has flattened the yield curve (Fig. 3). We take the opportunity to reduce our interest rate risk and take our profits within our fixed income portfolio (Fig. 4).

Although we continue to believe in the disinflation trend, and anticipate a slower but solid growth environment, the market is currently pricing in 60bps of cuts in 2025, a large shift from only three weeks ago, as well as an expectation of an announcement of pause in QT at the March Fed meeting (Fig. 5). As a result, short covering form the investment community has pushed yields to our short-term objective. Our fixed income month end performance blog will be out this week, and we will give more detail around current environment and positioning. We remain long the belly (fiveto seven-year) area of the curve and look for rates to trend lower as the Fed begins to cut in the second half of the year.

… book em Danno and same shop with a few words on our poorly confused President …

US President Trump confused investors by appearing to delay taxing US consumers of Mexican and Canadian goods. The White House then “clarified” that the tax delay was not decided. Such taxes would be very visible to US consumers, at a time when Trump’s approval ratings on the economy and inflation have fallen, making repeated retreats likely.

Trump threatened to tax US consumers of EU goods by 25% (Trump seems emotionally attached to 25% tax rates). The threat was somewhat incoherent—either applying to all imports, or just autos. All imports seems unlikely because price increases would be very visible. Taxing autos could create additional inflation forces via prices of domestically produced cars, second-hand cars, and auto insurance.

Fourth quarter US GDP is due for revision. The consensus is for little change, with the core PCE deflator also staying around 2.8% y/y. This has been pulled higher by non-market prices. Where the forces of supply and demand dictate price changes, core inflation is at 2.4%…

… I do hate when this guy weighs in … I’ll move along.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up, another VERY relevant question at this point in time and the cycle …

Apollo: Sentiment Bad, Hard Data Good: How Long Can It Continue?

The Conference Board consumer confidence survey for February shows a big jump in the share of consumers who are worried about fewer jobs being available, see the first chart below.

Total employment in the US economy is about 160 million. With 3 million federal employees potentially worrying about their jobs and 6 million federal contractors worrying about their jobs, the risks are rising that households may begin to hold back purchases of cars, computers, washers, dryers, vacation travel plans, etc.

We remain bullish on the economic outlook, but we are very carefully watching the incoming data for signs if this is an inflection point for the business cycle.

On Saturday, we will be publishing our usual daily and weekly indicators for the US economy to monitor if the weakness in sentiment seen in the charts below is starting to show up in actual spending decisions for consumers and firms.

Source: Conference Board, Haver Analytics, Apollo Chief Economist

Source: Bloomberg, Apollo Chief Economist

… from a guy who recently started to see the writing on the wall in as far as the cycle turning to a somewhat less GOOD one …

AND on that there growth scare, a couple from The Terminal …

Bloomberg: Treasury Investors Anticipate Fed Shift Back to Growth Risks

Morgan Stanley says US 10-year can fall back below 4%

Expectations for interest-rate cuts this year are rising again

… Federal spending cuts being sought by firing government workers since President Trump took office last month may also allow rate expectations to decline, Morgan Stanley says …

… “Bonds are responding to the potential of lower supply,” Jim Bianco, president and macro strategist at Bianco Research, said on Bloomberg Television. “Now whether that happens, that’s for later this year. And whether that’s stimulative or inflationary, that’s for later this year.”

… and …

Bloomberg: US Workers Cite Growing Layoff Fear in Philadelphia Fed Survey

Finally, from Terminal, a view on topic EVERYONE’s been talkin’ bout (and a few words / visuals on NVDA) …

Bloomberg: Make Them a Mar-a-Lago Accord They Can’t Refuse Trump has the means of persuasion to get a broad dollar agreement — except with the country that really matters. February 27, 2025 at 5:52 AM UTC

… Nvidia Numbs Nvidia Corp., the dominant maker of the chips needed for artificial intelligence, has reported results for the quarter ending in January. In a remarkable achievement, they managed to produce a non-event.

Since the launch of ChatGPT set off an AI arms race that ignited demand for its products, Nvidia’s quarterly numbers have typically been followed by double-figure moves in its share price after hours. This time, it moved around a bit, but ultimately ended up more or less where it started:

This might seem odd. Profits came in ahead of market expectations, as did revenues. As it’s still only a month since the Chinese DeepSeek AI app sparked fear that Nvidia’s business model wasn’t as impregnable as had been assumed, this might have been expected to deliver quite a surge. At$131.28, the stock is still 8% lower than $142.65 before the DeepSeek shock. Growth in revenues continues to be astonishing. There are arguments about whether the company is overvalued, but its sales leave no doubt that something remarkable is happening:

The problem was that Nvidia’s profit margin was trimmed a little as it spent heavily to launch its new Blackwell range of chips. It’s never great when a company sees its margins trimmed, but this needs to be seen in context. Below is Nvidia’s operating margin each quarter going back to 2000:

This remains a stunningly profitable company, whose margins have multiplied several times since ChatGPT. If any shareholders really wanted it to keep pushing up margins, they might look a little greedy.

It’s always risky to extrapolate much from the immediate response to an earnings announcement in thin trading. If the market’s judgment stands up Thursday, it can perhaps be taken as a sign that Nvidia is indeed priced for perfection. Because these numbers were not that far from perfection.

Yesterday, Treasury yields declined as investors got nervous about growth, with the 10-year yield temporarily dipping below 4.30%.

Consumer confidence fell in February, creating the catalyst for a decline in yields.

Recent signs of a downshift in growth led markets to price in two cuts by the Federal Reserve (Fed) in the latter half of this year.

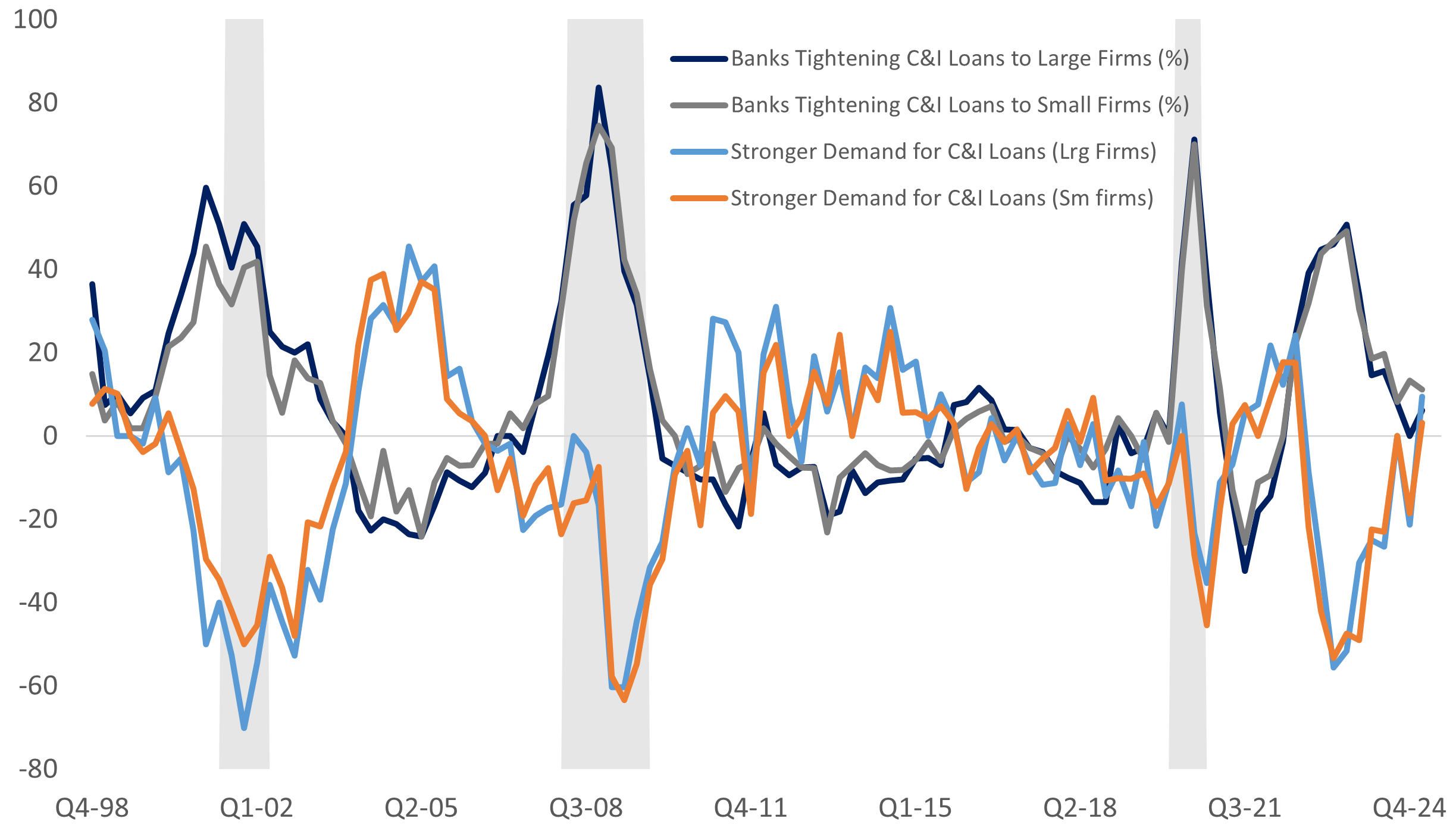

On the plus side, improving loan demand suggests more capital expenditures.

…Slowing but Still Growing

We expect the economy to downshift this year but still post growth in the first half of the year. Business spending appears to be on the cusp of improving this year. According to the latest Fed’s survey from senior loan officers, lending standards eased, and commercial and industrial (C&I) loan demand improved. If the downshift in growth is meaningful, the markets could be right about two rate cuts this year, but only if the inflation backdrop improves. No doubt easing inflationary conditions would be a positive catalyst for markets.