ZH: Stellar 5Y Auction Stops Through Amid Surge In Foreign Demand

… almost forced ‘em down the throats of primary dealing community as bonds were on the run from the get go and were more so after the consumer confidence …

ZH: Conference Board Consumer Confidence Collapses As Inflation Fears Soar

… as momentum fading, concession needed (but lack of one hasn’t mattered so far)

… Before we get to this afternoons auction a quick look back at just how yesterday worked out …

ZH: 'In The Midst Of A Negative-Feedback Loop': Bonds Bid As Retail Rout Wrecks Everything Else

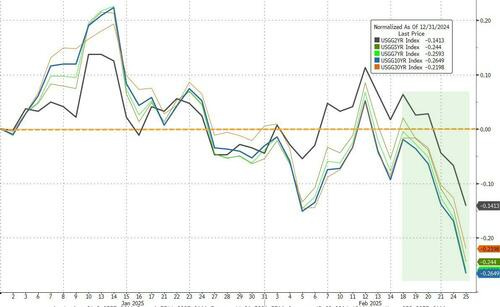

…While everything else was dumped today (retail liquidation) bonds were bid (short squeeze sent yields down 7-10bps on the day) sending yields down around 25bps YTD...

Source: Bloomberg

...pushing 2Y Yields to their lowest since October 2024...

Source: Bloomberg

And the most notable aspect of the yield curve (3m10Y) is about to re-invert...

Source: Bloomberg

....and in the meantime, the growth scare (and stock slump) has reinvigorated dovish calls for more rate-cuts (now up to 60bps for the year from just 25bps less than two weeks ago)...

Source: Bloomberg

Looks like Trump wins again: market now pushing Fed to restart cuts, even as Trump imposes tariffs on most trading counterparts.

NEWSQUAWK: US Market Open: NQ bid ahead of NVIDIA earnings; USD gains & copper benefits on Trump tariff investigations … USTs are off lows but remain in the red while EGBs inch higher … An upward bias is present, though USTs remain in the red, a move off lows which began in the European morning despite a lack of specific drivers at the time and was potentially a function of a bout of pressure in the crude space weighing on yields. As it stands, USTs are at the mid-point of a 110-08 to 110-19+ band and while they have been in the green on a few occasions the moves have been fleeting at best and minimal in nature. Today’s session is largely a waiting game until the after-hours numbers from NVIDIA. However, we do get Fed’s Barkin & Bostic alongside a 7yr auction and more executive orders from POTUS beforehand.

Yield Hunting Daily Note | Feb 25, 2025 | FMY Drops/Buy, Cornerstone Rights Offerings, BIGZ To BTX

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Confidence is waning …

Barclays: February consumer confidence: Pessimism about the future

The Conference Board's index of consumer confidence declined to 98.3 in February, as the assessments of current and future economic conditions dropped off. This comes alongside a 0.8pp increase in average inflation expectations to 5.3%.

US treasury yields saw a sharp slide on Tuesday, but held at strong support levels that we had flagged. The slide brings us very close to the head and shoulders indicated target in US 10y yields, which prompts us to turn neutral in the short term given the strength of the support levels nearby. See the details in our publication below…

…US 10y yields The slide in yields means that we have come just 4bps away from the head and shoulders formation's indicated target at 4.24%. This also coincides with finding very strong support at 4.24%-4.27% (200d MA, 55w MA).

At this level, we turn neutral on US 10y yields in the short term. We think we are likely to find support at this range in the near term. We see resistance at the ~4.50% area (head and shoulders neckline, November high, July high).

Medium term, we see weekly momentum continue to drift lower, suggesting we could still see another leg lower in 10y yields. However, given how strong the 55w MA has been as a support since 2023, we prefer to wait to see a decisive weekly close below to 'confirm' a break.

Germany offering some context to confidence, econ expectations and equity price action …

Markets saw another decent risk-off move over the last 24 hours, as concerns about the US economic outlook continued to mount. There wasn’t a single catalyst, but there’s been some disappointing US data recently, and yesterday we found out that the Conference Board’s consumer confidence indicator hit an 8-month low. By the close, no asset class was immune from the slump, with equities losing ground, credit spreads widening, bond yields falling, and commodities selling off too. In fact, it’s now been the biggest 4-day decline for the S&P 500 since early September, and the Magnificent 7 was back in technical correction territory, having now shed more than -10% since their peak back in December. So that’s heightening the focus on Nvidia’s earnings after the US close tonight. Meanwhile for Bitcoin (-5.59%), it was the biggest daily fall since early September.

Given a couple decent (front-end) auctions and lots of attention TO supply creatingh it’s own demand, this next note caught my attention …

DB: Concerns around long-end auction tails in refunding months

In light of the 10-, 20- and 30-year auctions that have all tailed in the past two weeks (indicating weak auction demand), today’s chart examines the historical performances of 10-year and long-end auctions during refunding months. As highlighted on the chart, the recent episode was the first time all three of these auctions have tailed in a refunding month since August 2023, and it marks only the third such occurrence since the 20yr maturity was introduced in 2020. While the auction tails in August 2023 may have been explained by the Treasury’s auction size increases, there was no such increase this month, with the Treasury stating that it “anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters” at the refunding announcement. In light of this, the auction tails suggest that the market has difficulties digesting the current supply of medium and longer-term USTs, and they raise potential concerns about future auction size increases and the direction of long-end yields.

Connecting auction tails to subsequent market performance, the weak auctions in August 2023 were followed by a notable rise in model-based measures of term premia (such as ACM and Kim-Wright) in the subsequent months. Additionally, although the 20yr auction in August 2024 stopped through by 0.1bp, the 10yr and 30yr auctions tailed significantly (3.0bps and 2.9bps respectively), and term premia also increased in the following months. We have previouslywrittenabout our expectations for higher term premia – which continue to trail historical levels – with factors such as a rising share of price-sensitive investors and greater inflation uncertainty continuing to exert upward pressure on term premia.

Bond folks are generally a ‘half empty’ kinda people and this note rightfully so, earns a place into ones heart and mind …

The drivers of Doge, Bessent and SLR have been added to in the guise of weaker consumer confidence and a ratchet down in expectations for the terminal rate. This market is now considering the possible downsides ahead. Can it last? Well yes for a bit. But we are constrained to the downside for yields, until or unless we seriously contemplate a recession of sorts

With the above / aforementioned techAmentals in mind, this next question being asked by many on Global Wall …

MS: How Low Can UST Yields Go? | US Rates Strategy

UST yields broke important technical levels to the downside and are now near 200-day moving averages. Most factors that led to higher yields from September reversed since the presidential inauguration, save for one: the Fed's mojo. A further Treasury market rally likely requires a dovish shift.

Key takeaways

A buyers' strike, momentum-driven duration shedding, macro fund reflation trades, and a hawkish pivot from the Fed catalyzed higher yields from September.

Every factor reversed after the presidential inauguration save for one. Rhetoric from FOMC participants is less dovish than before the election.

Treasury yields correlate positively to the market-implied trough policy rate of the Fed. We see more downside to market-implied trough rate pricing.

If the market-implied trough fed funds rate falls to its October 2024 way-point of 3.25% from levels near 3.65%, 10y Treasury yields could break below 4.00%.

We suggest investors remain overweight duration around the 5y point and stay in SFRM5Z6 curve flatteners, but exit longs in TYH5 basis, given the futures roll.

…Trade idea: Maintain long UST 5y notes at 4.15%, with a target of 3.75% and trailing stop of 4.32% …

Swiss shop has figured one way to generate clicks is to use large words … seems to good of a note to be true …

US equity markets were a little disturbed by a sharp decline in a consumer confidence survey—but these surveys are distorted by partisan politics. Depending on the cable news network one watches, the US is either an unpleasant version of Panem from “The Hunger Games” or a Panglossian paradise where all is for the best in this best of all possible worlds. Clear economic signals are hardly likely to come from economic surveys in such a situation.

There are risks to the US economic growth outlook. Inflation perceptions remain a concern—US President Trump has presided over soaring egg prices which they cannot control, but which might impact consumers’ fears for the future. Uncertainty over policy, and in particular trade taxes, might impact investment or consumer spending (yesterday, there were threats to tax US copper users).

The US House of Representatives passed, with some difficulty, a budget resolution. The process goes to the Senate, and then reconciliation, with investors likely to focus on resistance to larger deficits. Markets would not react well to suggestions that fictional fiscal savings are included in the accounting.

The data calendar is dangerously quiet, allowing politics to intrude into the markets’ consciousness. French and German consumer confidence data is also subject to partisan bias, though less transparently.

More on sentiment …

Wells Fargo: Consumer Pessimism Rising Sharply in February

Summary February brought the biggest drop in consumer confidence since 2021 as anxiety about the outlook for the broader economy manifested in a more-than nine point drop in the forward-looking expectation index, which now sits at an eight-month low and is just 7.3 points from its cycle low in 2022.

Finally, Dr. Bond Vigilante with a look in at consumers …

The stock market sold off this morning on a decline in February's Consumer Confidence Index (CCI), confirming a similar decline in February's Consumer Sentiment Index (CSI), which was reported at the end of last week. The CSI survey tends to be more affected by inflation, while the CCI survey is more affected by employment. The former was weak this month on concerns about rising inflation, while the latter was weak mostly on expectations of fewer job openings in six months. Both are very volatile on a monthly basis. Both may be reflecting extreme partisanship, with Democrats much less confident than Republicans, in our opinion. Let's review the CCI data in 10 charts...

(1) In February, there was a big drop in the expectations component of the CCI. The present situation component of the CCI dipped but remained relatively high. We think that the present situation component is a better indicator of the economy's current performance than is the expectations component, which is more volatile as well.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up, POSITIONS matter …

Bloomberg: Traders Bet Big on Bond Rally as Tariff Growth Shock Looms

Treasuries have rallied this past week, sending yields lower

Wager on 10-year note yield falling to 4.15% placed at premium

…One standout position targeting a 10-year yield drop to 4.15% and beyond emerged Tuesday morning. Around $60 million was spent on the bet, which stands to garner profits of approximately $40 million should yields drop as low as 4%, according to calculations by Bloomberg. If yields re-test the September lows, the position stands to amass a fortune of roughly $280 million…

AND an OpED from The Terminal this morning …

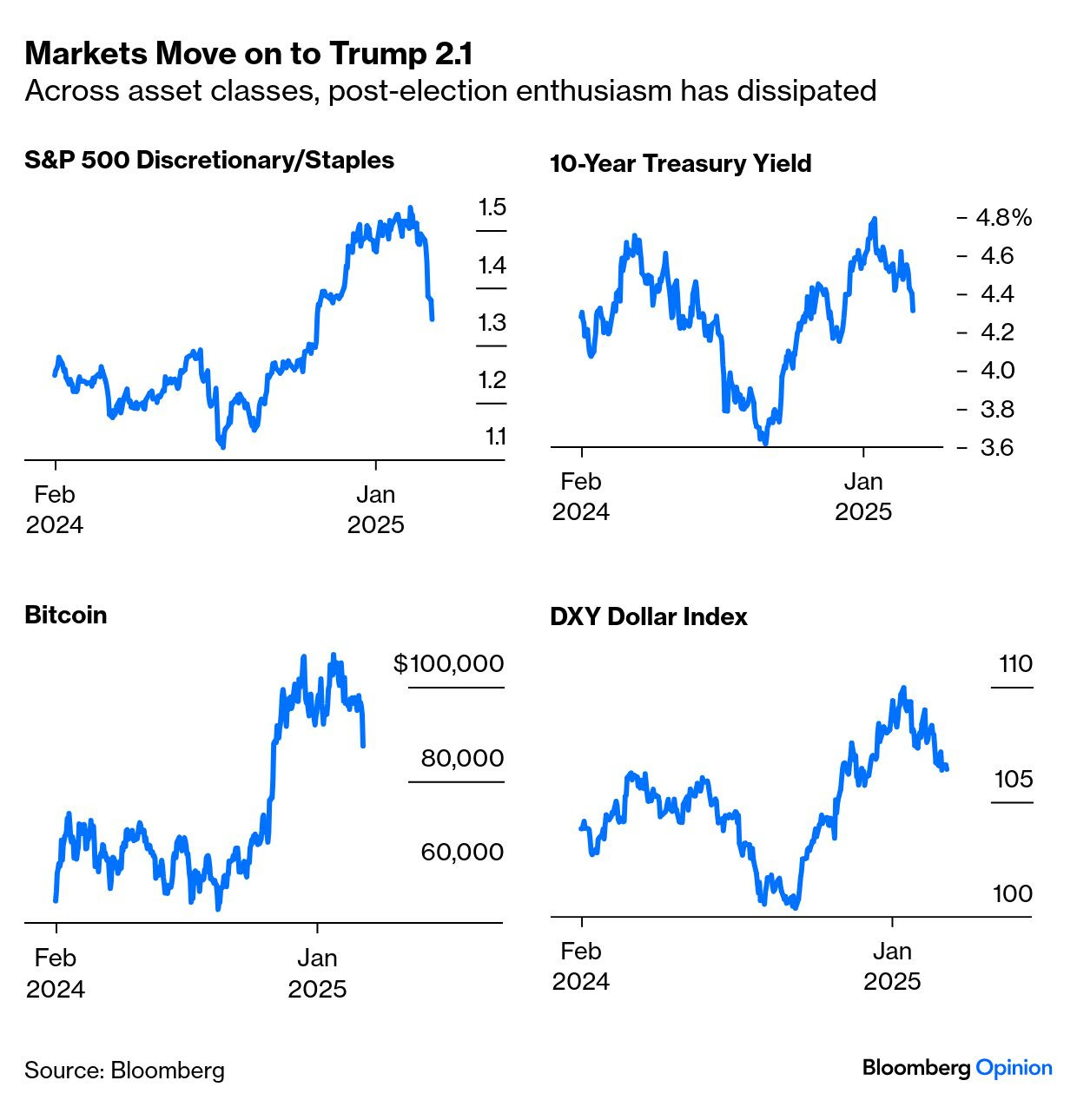

Bloomberg: Trump 2.1 arrives with a whimper rather than a bang His second presidential win has been accompanied by far more excitement, but consumers are becoming dubious. February 26, 2025 at 5:11 AM UTC

Whatever happened to the Trump 2.0 American Exceptionalism Trade? With a pro-growth president devoted to deregulation, and bent on asserting US dominance over everyone else, the conventional wisdom was to pile into US assets and crypto, and brace for bond yields and the dollar to surge higher. All that happened in the weeks after the election.But sinceDonald Trump actually took office on Jan. 20, and particularly in the last week, all the Trump trades have reversed:

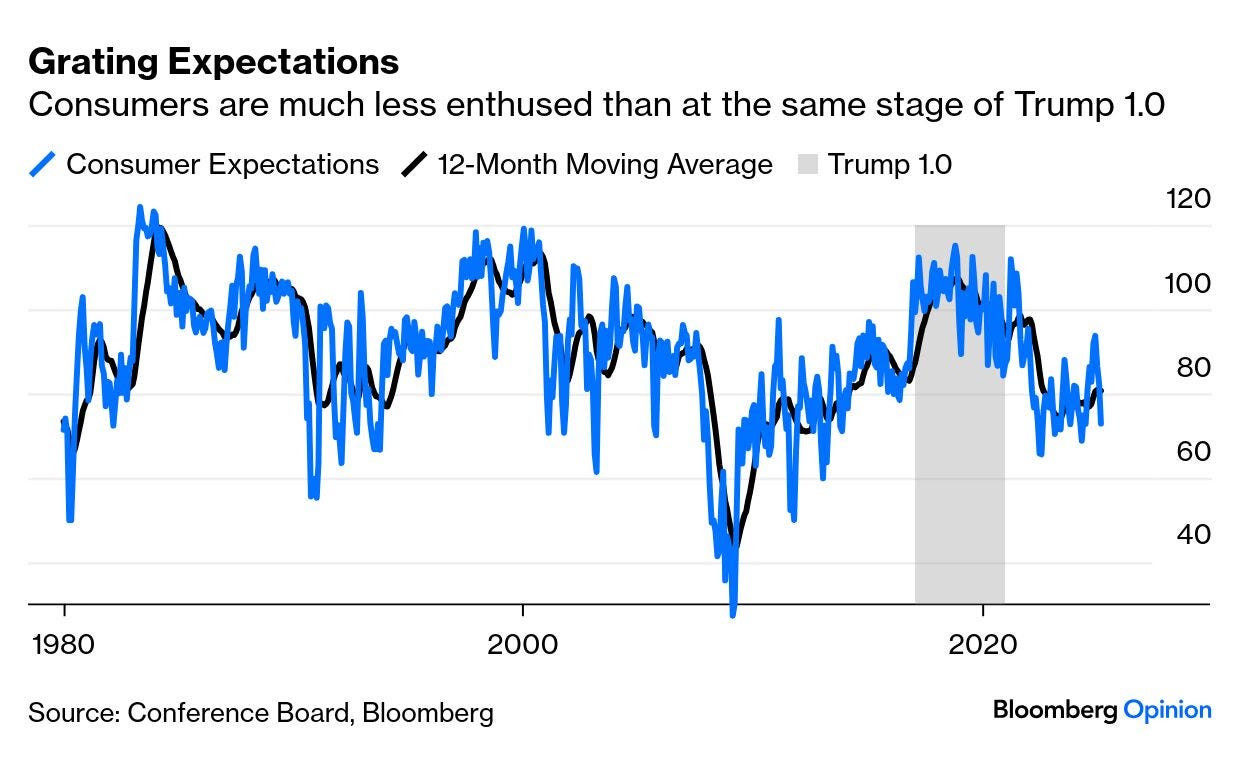

In large part, this is a renewed growth scare. Angst that the DOGE job cuts could slow the economy in the near term is part of it. Business surveys have been downbeat, while the latest Conference Board survey of consumer sentiment, published Tuesday and the first since Trump took office, dropped sharply. In his first term, expectations rose immediately; this time, even though his arrival in office has been accompanied by far more excitement and action than he generated in the first, it seems consumers are more dubious:

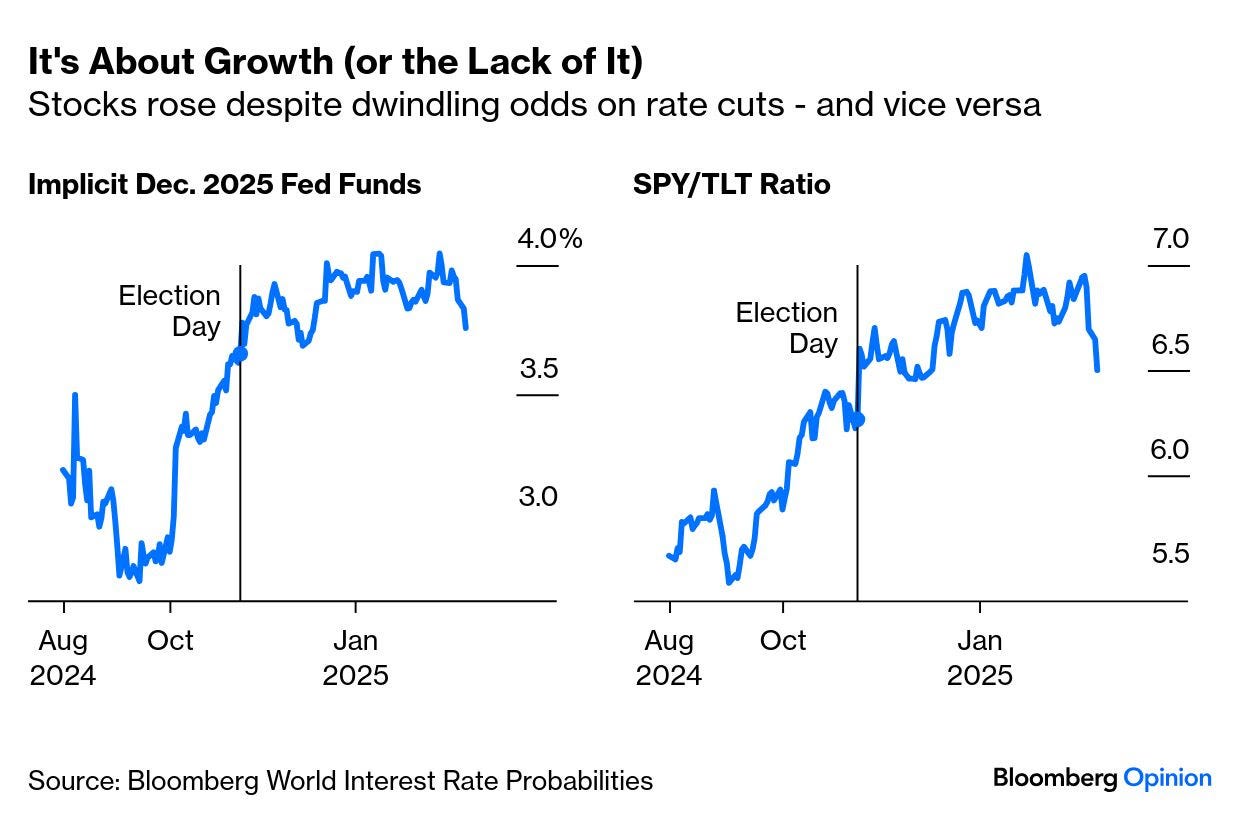

The growth scare has also shown up in a sharp move in rate-cut expectations from the Federal Reserve. The ratio of stocks to bonds (proxied by the popular ETFs SPY and TLT) has moved perfectly in alignment with the futures contracts trying to predict the fed funds rate at the end of this year. Stocks don’t appear reliant on rate cuts, as they surged in the last few months of 2024 even as projected December 2025 rates rose by more than a percentage point. What’s happening now is plainly a dose of nerves about growth:

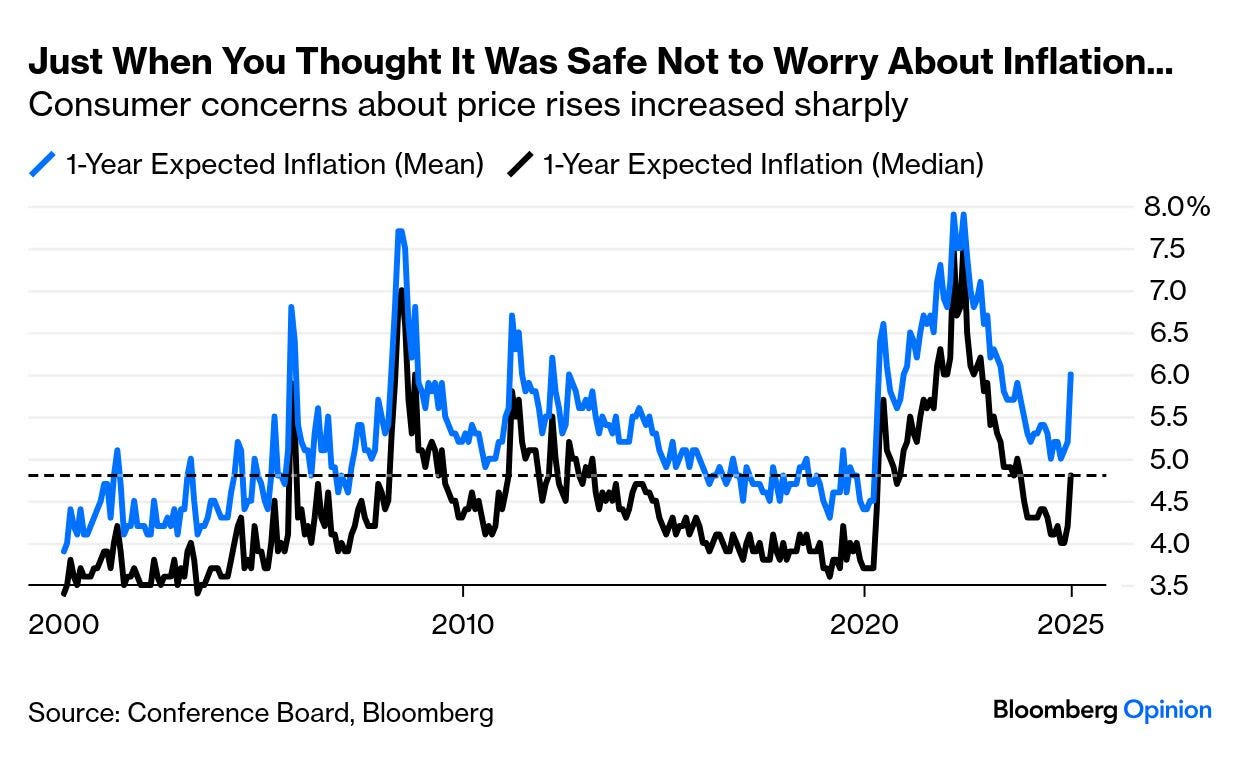

And yet, inflation expectations are also going up — a move that all else equal would imply that fed funds would have to rise, not fall. This is what just happened to the Conference Board’s measure of expected inflation for the next 12 months, on both a mean and median basis:

…There’s a name for a growth scare combined with rising inflation expectations. “If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck,” comments Vincent Deluard of Stonex Financial. “Similarly, if growth slows, inflation accelerates, gold soars, and the dollar rolls over, then it is probably stagflation.” …

AND same shop with an(other) OpED (missed yesterday) …

Opinion |Bill Dudley, Columnist Bloomberg: To Do Its Job Right, the Fed Must See What’s Wrong The central bank needs to recognize the flaws in its monetary policy framework. February 25, 2025 at 11:30 AM UTC

… Properly identifying mistakes matters. Otherwise, how can one be confident that the Fed won’t repeat them? Credibility is crucial: Without it, central bankers’ ability to influence financial markets and the economy will be impaired.

To that end, the Fed must recognize and remedy the 2020 framework’s flaws and omissions. It should scrap the regime that kept rates too low for too long. It should apply greater rigor to quantitative easing and quantitative tightening: Was QE, for example, worth the $500 billion to $1 trillion that it cost the US Treasury, or did it merely stoke inflation? It should stop targeting an interest rate — the federal funds rate — that is increasingly obsolete. Relying exclusively on the rate paid on bank reserves would be considerably simpler.

The framework review will take several months to complete. May the Fed use the time well. There’s plenty of room for improvement.