Good morning … given I was SUPPOSED to be outta pocket yesterday (I couldn’t have picked a worse day to travel in / outta NYC and Mother Nature then had plans in having travels ppd until NEXT Thurs — will mention again), I am doing a bit of catchup and cannot help but note that while Mother Nature working on school closings and travels in / out of NYC, Mr. Markets (are they related?) making some statements at least in as far as 10yy in / around 4.50% concerned …

10yy: 4.50% TLINE seems to be decisively broken, 50dMA too (4.489) …

… and while this TLINE break is bullish, am still concerned as momentum on daily charts remains overBOUGHT … note to self - overBOUGHT conditions can remain so longer than I — if I were trading and from the short-side, and I am NOT — could remain solvent … and this in mind, there’s ample room and REASON for even lower yields just ahead …

… On THAT and for much more and from a far better source than this humble ‘Stack, kindly see recent thoughts from best techAmentalists out there (CitiFX) discussing the US rates backdrop of the moment and the flattening bias …

…US 10y yields US 10y yields have just broken a very, very key support level at 4.48%-4.50% (55d MA, July 2024 high, November 2024 high, psychological level). The close below initiates a head and shoulders formation. This is an indicator of lower yields and would suggest a target of ~4.24%. That would be very near the next layer of support at 4.25%-4.26% (55w MA, 200d MA).

Weekly slow stochastics, which is crossing lower from 'overbought' territory, also supports the case for lower yields. Resistance is likely only at 4.80% (Jan high)….

More below and in as far as some of the ingredients in yesterdays market BID …

ZH: American Goods-Producers Suffer Biggest Job Loss In 2 Years, Services Employment Soars

ZH: US Trade Deficit Soars As Firms Front-Ran Trump Tariffs In December

ZH: Treasury To Keep Debt Sales Unchanged For "Next Several Quarters", Prepares To Drop Issuance Forward Guidance

ZH: US Services Sector Surveys Plunged In January As Prices Rose & Orders Fell

3 outta 4 more bullish than not as ADP strong BUT … supply NOT expected to grow to the sky and services soured … Far more below (see DBs EMR for good’er recap, for example) but for now, being more skeptical of further gains from HERE seems prudent to me (and ING below), there’s a case for lower yields ahead, still … Choose your own ending to this one and lots to THINK about and read, ahead of tomorrows NFP.

…Bond opportunities For all investors’ handwringing over Donald Trump’s unpredictability, it’s worth keeping in mind that market volatility creates all sorts of opportunities — if an asset you’re eyeing is too expensive, you may be just a Trump tweet away from a buying opportunity.

Just ask Daniel Ivascyn, chief investment officer at bond behemoth Pacific Investment Management Co.

“A little bit of volatility, a little bit of fear in markets, for us would likely be a good thing,” he said in an interview. “Volatility usually means opportunity for active managers.”

The Newport Beach, California-based asset manager is betting on five- to 10-year bonds, as they generate solid income, and are prepared to buy more if yields rise back toward 5%. Trump’s policies have put traders on their heels and clouded the outlook for the Federal Reserve’s next steps for monetary policy.

Ivascyn’s $175 billion Income Fund has a lot of liquid investments, he says. “If we get a pullback in credit markets, we would look to reduce some of the high-quality stuff and then be more aggressive in the credit market, high-yield and loans,” he says.

The fund has gained 1.3% this year, outpacing a 0.8% rise in the broad market index and beating 94% of rivals.

Pimco, with almost $2 trillion under management, is no run-of-the-mill firm. Under founder Bill Gross, it became the biggest name in fixed-income investing. While clients pulled assets after his departure a decade ago, his successors have steadied the ship. As you can read in today’s Big Take, though, some at the firm now fear Pimco has lost its edge as it fails to keep up with the industrywide push into private assets.

Pimco began this year making a case for owning Treasuries in the five- to 10-year zone as it saw an unpredictable policy agenda from the new White House burnishing the appeal of high-quality bonds compared with expensive equities and corporate debt.

“You’ve got to be respectful of the uncertainty here,” Ivascyn said, while being focused on staying “nimble and generate some pretty good returns.”

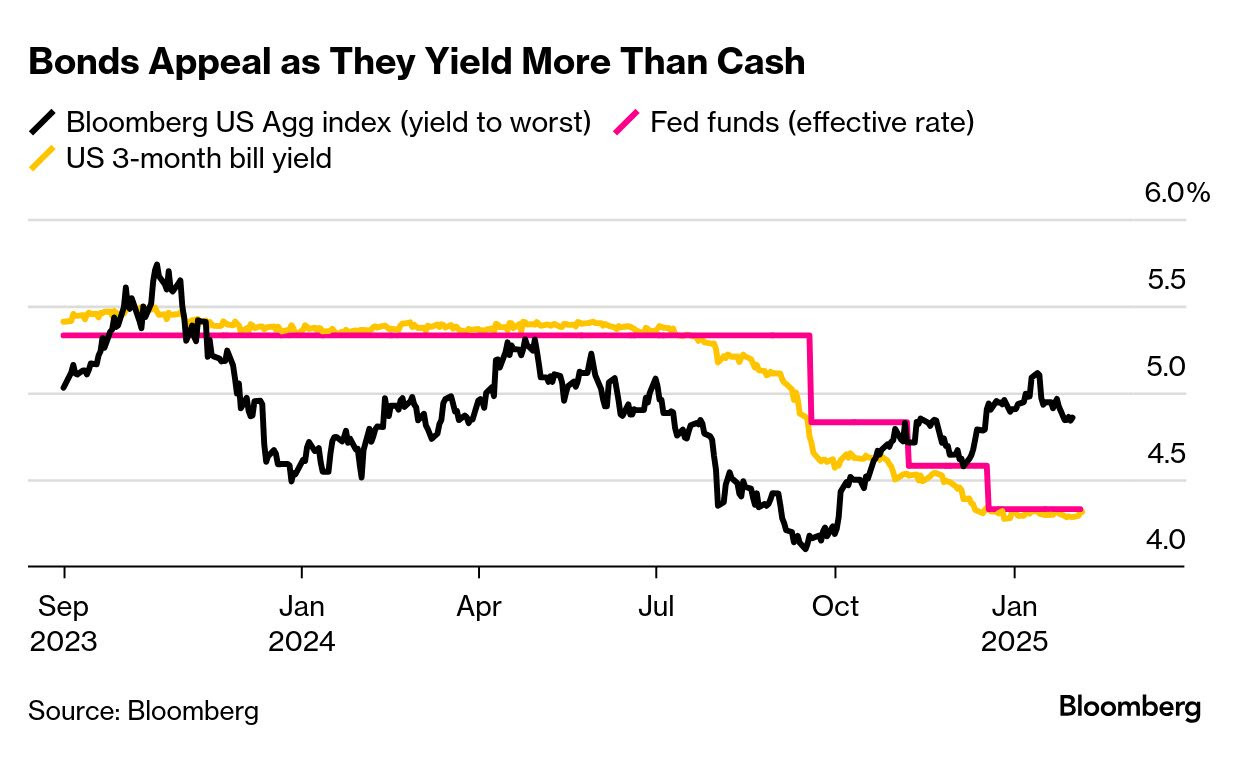

“To the extent that there continues to be this uncertainty around policy that could impact economic fundamentals, we think the Fed’s going to be on hold,” Ivascyn said, and that’s still good for owning longer-dated bonds as they yield more than the current cash rate, around 4.33%…

… here is a snapshot OF USTs as of 633a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US Market Open: Stocks gain, USD bid ahead of jobless claims, GBP lower with the BoE in view … Bonds in the red but off lows via a strong French auction & stagflationary UK data amid reports of a UK Cabinet reshuffle … USTs are in the red, weighed on overnight in tandem with JGBs on hawkish commentary from BoJ’s Tamura (hawk) who stated they must raise rates to at least around 1% in the latter half of FY25. More broadly, the benchmark is trimming some of the upside seen on Wednesday with yields picking back up after their pullback. Thus far, USTs down to a 109-16 base vs Wednesday’s 109-29 peak; if the move extends, support factors at 109-02 before the figure and then 108-25+. US Jobless Claims, Challenger Layoffs and a few Fed speakers due.

Although the ISM services PMI fell in January as the new orders and business activity components softened, it remained in territory consistent with solid service-sector growth. Respondents' comments indicate some apprehension about what tariffs and other policies will mean for costs and activity.

AND from best in stratEgery biz …

BMO (Feb 5): ISM Services Disappoints, TSY Bull Flattening Extends BMO February Refunding: Steady Issuance; Forward Guidance Unchanged BMO Close: Take That TBAC

…Wednesday’s price action was decidedly constructive for the Treasury market with 10-year yields dropping as low as 4.40%. The bid was inspired by a variety of events, although the bond bullish tone was already in place during the overnight session. The combination of disappointing ISM Services (albeit still >50) and an uneventful Refunding Announcement cleared that path for a duration grab. While no one expected the Treasury Department to increase nominal coupon auction sizes, the fact that the “for at least the next several quarters” language was retained added confidence for dip-buyers. We’ll argue that what’s playing out at the moment is a partial unwind of the Trump trade. Specifically, reflationary worries and supply concerns have been moderated by the developments of the last few sessions. On the trade front, what now appears to be a more measured approach – at least to Mexico and Canada – has eased concerns of a global trade war spinning out of control with retaliatory actions. As for Treasury supply concerns, auction sizes will eventually be increased, but not this quarter, nor for the foreseeable future.

It also warrants highlighting that the TBAC report specifically recommended dropping the “next several quarters” language. The report said, “In discussing issuance recommendations, the Committee uniformly encouraged Treasury to consider removing or modifying the forward guidance on nominal coupon and FRN auction sizes that has been in the refunding statement for the past four quarters. Some members preferred dropping the language altogether to reflect the uncertain outlook, though the majority preferred moderating the language at this meeting.” And yet, the statement stuck to the prior messaging. It’s tempting to take this as an especially strong pushback against the widely held supply concerns. We’ll offer the observation that Bessent has only been in his new seat since last Tuesday, so there might be more meaningful changes afoot in the coming quarters than one might have assumed by interpreting the statement at face value. Admittedly, we might be predisposed to reading too much into the degree to which the incoming Treasury Secretary desires to be a change-agent for borrowing policy…

Any (other)chartists out there among us? Best in this racket, IMO, a group of tech-A-mentalists offering a (flattening bias) on rates … and a more bullish one, at that …

Technical levels have broken, especially in US 10y and 30y yields. With 2y and 5y yields still looking like they're holding in a range, we see a short term flattening bias in US treasuries…

…US 10y yields US 10y yields have just broken a very, very key support level at 4.48%-4.50% (55d MA, July 2024 high, November 2024 high, psychological level). The close below initiates a head and shoulders formation. This is an indicator of lower yields and would suggest a target of ~4.24%. That would be very near the next layer of support at 4.25%-4.26% (55w MA, 200d MA).

Weekly slow stochastics, which is crossing lower from 'overbought' territory, also supports the case for lower yields. Resistance is likely only at 4.80% (Jan high).

…US 2s10s 2s10s is testing a very strong support range at 22.14-23.59 (55d MA, September high). IF we break below this, we only see support at 11.38 (Dec 18th low), followed by stronger support around the 0 level (Psychological level, Dec low, 200w MA).

Seasonal inflation bias? may just be …

DB Data DBrief: Does every seasonal factor update turn, turn, turn the inflation trend?

The upcoming CPI release with the January 2025 data will also come with, as it usually does, new seasonal factors as the BLS re-estimates them including the latest data. While not normally an issue, these updates can recontextualize short-run inflation trends, sometimes dramatically so.

Indeed, this happened in February 2023 when what looked like meaningful progress on disinflation over the second half of 2022 was revised away, severely undercutting arguments at the time that the Fed was restrictive enough. Conversely, the seasonal factor revisions in February 2024 were relatively benign.

Double-seasonally adjusted data would suggest that, though there could be some upward revisions to inflation over the second half of 2024, the result of the upcoming revisions should be much closer to the February 2024 experience. While the changes to the seasonal factors are unlikely to show worse inflation over the second half of 2024, neither are they likely to show a meaningfully better trend.

Same shop and fan favorite stratEgerist on Bessent, DJT and 10s AND what moved mkts yesterday …

…After a severe allergic reaction on Monday after the tariff news, markets continued to be relatively sedated yesterday as investors continued to price out the chance of aggressive tariffs, whilst the ISM services index showed inflationary pressures were weaker than expected. That meant the US dollar (-0.35%) continued to fall, reaching its lowest level in the last week, and the prospect of lower inflation also helped to bring down Treasury yields, with the 10yr yield (-9.4bps) down to 4.42%. On that around the time of the US close Treasury Secretary Bessent said in an interview with FOX that while President Trump wanted lower rates, they were both focused on the 10yr yield not the Fed policy rate, adding that policies to boost energy supply and reduce the budget deficit would help achieve this. He implied that the "jumbo rate cut", referring the 50bps cut in September, helped create the bond sell-off. So this was an important interview and all other things being equal will encourage a flattening bias. However as Bill Clinton's political advisor James Carville famously said back in 1993 when referring to the afterlife "... I want to come back as the bond market. You can intimidate everybody". So this is new important news that shows the Trump administrations' attitude to monetary policy and yields. However at the end of the day their fiscal and supply side policies and how they impacts growth, supply and inflation will still be the most important.

In terms of more detail on what drove the moves yesterday, the ISM services print added fuel to the bond rally, as the prices paid component fell back to 60.4, after spiking to 64.4 the previous month. Remember that the release a month ago was one of the main factors in turbocharging the bond selloff, so the fact we saw a pullback came as a relief to investors. Moreover, the headline indicator fell to 52.8 (vs. 54.0 expected), so that also helped to alleviate concerns about demand pressure, and whether the Fed might have to hike rates in the months ahead. Indeed, the Atlanta Fed’s GDPNow tracker took down their Q1 estimate from an annualised 3.9% to 2.9% after the various releases, suggesting the economy was still doing well, but not seeing a noticeable acceleration either.

So that helped investors to dial up their expectations for rate cuts this year, with 47bps now priced by the December meeting, up +2.3bps, and having briefly reached a full 50bps intra-day. A partial reversal later on came in part as Chicago Fed President Goolsbee said that “If we see inflation rising or progress stalling in 2025, the Fed will be in the difficult position of trying to figure out if the inflation is coming from overheating or if it’s coming from tariffs”. Goolsbee had been one of the more sanguine FOMC voices on inflation in the past year so it’s a notable comment for how Fed might be thinking about tariff risks. Later in the evening, we heard from Fed Vice Chair Jefferson that the Fed can remain patient with the economy in a good place. Overall, the view that the Fed would still cut rates in 2025 helped the 2yr yield fall -2.6bps to 4.19%.

From MAGA to MUS10yyLA? NOTE: bullishness appears to be limited from here (see momentum measures above?)

The latest Trump administration angle is for rates to be pushed lower through downward pressure on the 10yr yield, through lower inflation and a lower fiscal deficit. Achieve that and we'd agree. But achieve it first. Meanwhile, the Bank of England is likely to cut by 25bp, in line with market pricing. Going forward we see more GBP curve steepening

… We've been tactically bullish Treasuries in the past couple of weeks, so all of this is moving in our (short-term) direction. However, we also assert there is not huge room to the downside for the 10yr yield. An effective floor is in place at just under 4% as determinable from the funds rate strip. That floor can of course shift lower, but would need a better reason than an approaching 10yr rate. And the 10yr Treasury yield sits some 50bp over this. So enjoy the move lower while it lasts. Another 10-20bp and it will begin to look like its gone too far, and that’s where the backup starts…

On supply (reFUNding announcement) and the creating of its own demand (with some thoughts on central clearing worth a look) …

MS: February US Treasury Refunding Takeaways | US Rates Strategy

Treasury delivers no increases to coupon auction sizes and keeps guidance for no increases “for at least the next several quarters.” We continue to expect no increases to coupon sizes over the remaining quarters in 2025, as we see reason for more, not less, T-bill issuance.

Key takeaways

Treasury announced it plans to keep nominal coupon and FRN auction sizes unchanged over the February quarter, in line with our expectations.

The refunding statement continued to state nominal coupon and FRN auction sizes are not expected to be increased for "at least the next several quarters."

We continue to expect no increases to nominal coupon or FRN auction sizes over the remaining refunding quarters in 2025.

Due to debt limit constraints, we think reductions to bill auction sizes could soon be on the horizon.

A TBAC charge finds most market participants see a delay in implementation of the SEC rules on UST central clearing by a minimum of 12 months.

… Developments in Central Clearing Treasury also charged TBAC with investigating developments in central clearing for US Treasuries and repo transactions. TBAC concluded that the change to centrally cleared transactions will likely make the market more resilient, but will increase the complexity of many of the necessary systems.

While the switch to centralized clearing is deemed as a positive by many market participants as it likely reduces counterparty risk and balance sheet costs, several industry groups have asked the SEC to delay the implementation deadline by one year.

Additionally, attention was drawn to both the pros and cons of additional centrally cleared counterparties (currently FICC is the only CCP). TBAC noted more entrants could increase competition between different business and access models, but it could also split up liquidity into siloed pools…

SAME firm, thinking ahead to NEXT WEEKS CPI …

MS: US Inflation Monitor: CPI Preview: Push from wildfires and residual seasonality

We expect core CPI at 0.37% m/m in January (3.2% y/y). Wildfires and residual seasonality are behind the temporary acceleration. Both core goods and services come in firmer. Softer energy and food bring headline below core again: 0.35% m/m, 2.9% y/y, NSA Index: 317.416.

Late the to the year-in-review party (or perhaps early?) a note on FI flows …

NatWEST: US Fixed Income Flows – 2024 Year in Review

Fixed Income Inflows Picked Up In 2024 In this note, we review the US fixed income flows for 2024. With US elections in focus, it was a volatile year for the US 10y yields. The 10y yields peaked at 4.7% during late April and then shed more than 100bp around mid-September. With elections result outcomes becoming clearer starting October and expectations of tariffs in the Trump regime, yields walloped again to April highs by the end of the year. Fixed income inflows were net positive in 2024 with majority of the sectors seeing strong demand on the back of slump in yields for almost half of the year.

From our neighbors to the great white North …

RBC Quick Reid: What tariffs could mean for the U.S. economy

The threat of sweeping tariffs on Canada, Mexico, and China would have been (and may still be) the most significant trade shock in the U.S. since the Smoot-Hawley Tariff Act of the 1930s. And, while the worst of the shock may be delayed or reduced, we are still firmly focused on a fundamental shift in U.S. trade policy that’s persisted for nearly a century. It will likely have implications for growth and inflation—the magnitude of which will depend on the policy path ahead. Importantly, as we await the future of tariffs on Canada and Mexico (delayed until March 1st), the U.S. has implemented an additional 10% tariff on Chinese goods, and China has retaliated with tariffs on U.S. imports in a sign of what’s ahead for U.S. trade. U.S. President Donald Trump’s first term offers a limited economic playbook for the magnitude of trade policy changes now being discussed. As we highlighted in A U.S.-Canada trade shock: First economic takeaways, in 2018, we saw the effective U.S. tariff rate double from 1.5% to 3%. But at 25% tariff on Canadian and Mexican goods is nearly four times as impactful and would increase to the U.S. average tariff rate to 10.6%…

…What this means for the Fed Tariffs are a complicated shock for the Fed. They weigh on growth but increase inflation as they pull on both sides of the dualmandate in the opposite direction. It’s fair to say these tariffs will work against the Fed in terms of getting inflation back to target. That said, our US rates strategists expect the Fed will continue to be data dependent and not react to immediately to the tariff announcements. As Blake Gwinn, Head of US Rates Strategy wrote:

“We think the Fed is going to respond to the data, not expectations. Yes, policy (theoretically) works on a lag, and the Fed typically wants to skate to where the puck is headed, not where it’s been. But the path is too uncertain right now to try to preempt any particular view on where tariffs are going to be 9-12 months out and what that is going to mean for each side of the dual mandate.”

While the Fed will remain keenly attuned to underlying inflationary trends (i.e., within core services), the short-term shock will likely be most noticeable in the core goods space. This will almost certainly disrupt the deflationary forces we’ve seen of late and can cause core inflation to get stuck closer to 3.0% y/y. But the greater risks also include potential spillover to other sectors, namely higher construction and housing costs risk a re-acceleration. And if costs for housing, food, and other essentials continue to rise persistently, consumers will likely be quick to demand higher wages, setting off a potential wage price spiral.

Union Bank Switzerland weighs in with Paul Donovan VIEWS and a few notes otherwise worth knowing of and which might help you pass the time on this ‘moving day’ (between ADP and NFP) …

New US Attorney General Bondi issued a flurry of memos, allegedly including a request to investigate companies pursuing diverse and inclusive workforces. That is economically significant. At a time of rapid structural change, companies need to employ the right person in the right job at the right time to maximize technological gains, with diverse views to spot the opportunities of rapid change. Undermining that risks damaging trend economic growth and profitability…

…US 4Q productivity and unit labor cost data is important, but not reliable in real time. Automation and technology should increase productivity over time, as will social trends. Every time someone shops online, they are working (unpaid) for the retailer, increasing the productivity of (paid) workers.

ADP points to a private employment gain of 183K...decent ADP estimates private employment expanded 183K in January, and the December increase was revised up 54K to a 176K increase, leaving in place a pretty sturdy contour. Gains took place across all establishment sizes, and among the industries only manufacturing posted a decline. That estimated private sector gain by ADP is above our expectations for the BLS's estimate of private employment to be released Friday, where we expect a 160K increase, and a gain of 200K for total nonfarm payroll employment.

Recall that over the last two years the monthly changes in the ADP estimate of private employment have been almost completely uncorrelated with the BLS estimate of private employment, even in the revised data. Over the 12 months of 2024, the two series had a correlation coefficient of 0.12 and over the last two years a correlation coefficient of 0.17. Consider last January's data as a specific example. ADP estimated private employment expanded 107K when the data was released, while on that Friday when the BLS January employment report was released, private employment was estimated to have expanded 317K over the month, 210K above the ADP estimate…

… We also wrote a note recently outlining our thoughts on the ISM indexes in more detail — highlighting that, despite the ISM non-manufacturing composite being above 50 and in expansionary territory for most of the last two years, the recent levels may not be all that strong in the historical perspective, roughly consistent with ~1 ¾% real GDP growth pre-pandemic. The January decline reinforces our view that the above-50 level is not an indicator of strong growth …

…Uncertainty, what next? We expect an economic deceleration is underway (summary forecast table below), and the labor market is slowing on the back of that. Inflation improvement should resume in 2025. More rate cuts seem likely. The slower growth signals that policy is restrictive. The FOMC appears to be responding by normalizing monetary policy, and does not appear to want to pre-emptively assume something about tariffs. And what tariffs?

Covered wagon folks weighin’ in …

WFC: Services Demand Softens At Start of the Year WFC: Sharp Widening in Trade Deficit to End 2024 Driven by Temporary Factors

Finally, from Dr. Bond Vigilante on the day of the reFUNding …

YARDENI: Bessent Follows Yellen’s Lead & Gold Price Rises To New High

The bond market relaxed today after Treasury Secretary Scott Bessent's debut Quarterly Refunding Announcement (QRA) proved to be a non-event. The 10-year Treasury yield fell 9bps to 4.43%, its lowest level since the Federal Reserve's last rate cut, in mid-December (chart).

Bessent had been critical of Janet Yellen's usage of short-term Treasury bills to finance the federal budget deficit. Many investors, therefore, were worried that he would issue more longer-term notes and bonds, which would boost bond yields. The QRA said that auction sizes for notes and bonds would remain the same for the coming quarters, which means that bills will remain at a historically high percentage of the Treasury market for the foreseeable future (chart). This also is a positive for the stock market…

… And from the Global Wall Street inbox TO the WWW … a few curated links …

Bloomberg. Is always worth a look … this first one helps at least justify my recent obsession with 10s in / around 4.50%

Treasury chief highlights importance of energy in inflation

Asked about DOGE, Bessent says payments not being touched

Treasury Secretary Scott Bessent said the Trump administration’s focus with regard to bringing down borrowing costs is 10-year Treasury yields, rather than the Federal Reserve’s benchmark short-term interest rate.

“He and I are focused on the 10-year Treasury,” Bessent said in an interview with Fox Business Wednesday when asked about whether President Donald Trump wants lower interest rates. “He is not calling for the Fed to lower rates.”

Bessent repeated his view that expanding energy supply will help lower inflation. For working-class Americans, “the energy component for them is one of the surest indicators for long-term inflation expectations,” he said….

…The former hedge fund manager also said that, with regard to the Fed, “I will only talk about what they’ve done, not what I think they should do from now on.” He said that 10-year Treasury yields climbed after the Fed’s “jumbo rate cut,” referring to the 50 basis-point reduction that Chair Jerome Powell and his colleagues enacted in September.

While the Fed’s short-term benchmark serves as a key reference for money markets, 10-year Treasuries are a benchmark for 30-year mortgage rates along with other key borrowing rates…

AND then there’s a VIEW on Bessent, who’s explaining DTJ … seems to ME this is very much HINDSIGHT TRADING and Monday Morning quarter-backing and explaining away price action already occurred …

BLOOMBERG: Bessent Explains Trump. It Won't Be the Last Time At least their economic strategy on the 10-year yield takes the focus off the Fed. By John Authers

… Bessent also has to contend with the almost universal belief on markets that Trump 2.0 means higher 10-year yields. The argument is that tax cuts will mean higher deficits and higher yields to finance them, while tariffs will raise inflation. That brings higher yields in its wake. Thus yields rose sharply during the last quarter of last year, from a low in the brief period around the president’s debate with Kamala Harris when his chances looked to be weakening. It’s natural that the administration wants lower rates, the argument goes. Who wouldn’t? But their agenda will make it mighty difficult to achieve.

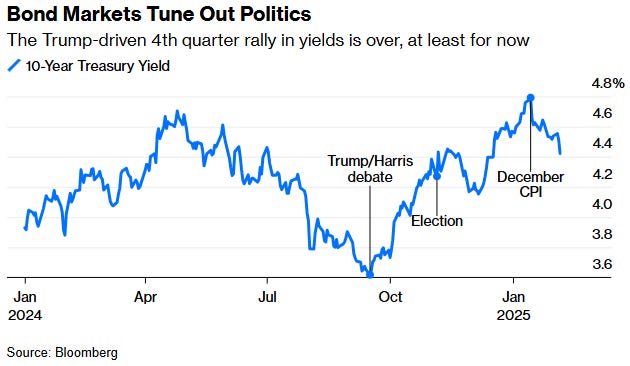

And yet. Bond yields are falling. The 10-year has shed 40 basis points in barely a month. And despite every other headline as the new president behaves like a bull in a china shop, the big bond market event of the year so far was the December inflation data. Nothing else comes close:

That was the decisive turnaround, even though the inflation data wasn’t that exciting. Disinflation is happening painfully slowly. However, the numbers were quiescent enough to dispel the notion that price rises were already resurging, and the Trump Trade had been overdone. Since then, traders reacting to hisactions rather than his words have continued — with occasional interruptions — to step back from bets on rising rates and inflation. In the process, they’ve also stepped back from bets on American Exceptionalism.

Relative to long Treasuries (proxied by the TLT exchange-traded fund), the S&P peaked on inflation day and has now dipped below its 50-day moving average. The post-election rally went a bit too far, and now it’s over. Relative to Europe, the US market enjoyed a massive post-election rally, which peaked in December and is now reversing. Not only have traders lost their conviction about higher inflationary pressure, but they’re less convinced that the administration will go through with significant tariffs against the European Union:

So if big tariffs become a reality, the bond market could reverse. For now, the administration is benefiting from a belief that it doesn’t mean what it says. In the longer term, Bessent and Trump face an even greater obstacle to pushing down the 10-year yield while growing the economy. Over history, the best way to reduce yields has been to bring down economic growth:

… Ruh Roh … but to all this VIEW, higher yields on rate CUT and lower since DEC CPI, it’s as IF we’ve no recollection of a Fed ‘conundrum’ …

Furthermore, if you actually listened to the interview, bringing down growth would seem to ME to be the furthest thing from ‘47 and Bessent’s mind. Wanting low rates ≠ wanting lower economy … HERE’S the full interview and starts talkin’ 10s about 10min in (halfway)

One MORE VIEW from The Terminal …

BLOOMBERG: The Job Market Is Weaker Than It Looks Education, health care and government have kept payroll numbers buoyant, but hiring momentum even in those areas is fading. By Conor Sen Conor Sen is a Bloomberg Opinion columnist. He is founder of Peachtree Creek Investments.

As the BIG game approaches, the world is rootin’ for the Chiefs and here’s why …

Carson Group: Welcome to the Worst Month of the Year in a Post-Election Year (and Why American Doesn’t Want the Eagles to Win)

…First things first, don’t ever invest based on who wins the Super Bowl. Or what color Taylor Swift will wear at the big game, or the coin toss, or how bad the refs will be (who are we kidding, we know they want the Chiefs to win). With that out of the way, it is Super Bowl season, and that means it is time to talk about the always popular Super Bowl Indicator!

The Super Bowl Indicator suggests stocks rise for the full year when the Super Bowl winner has come from the original National Football League (now the NFC), but when an original American Football League (now the AFC) team has won, stocks fall. Of course, this is totally random, but it turns out that when looking at the previous 58 Super Bowls, stocks do better when an NFC team wins the big game.

This fun indicator was originally discovered in 1978 by Leonard Kopett, a sportswriter for the New York Times. Up until that point, the indicator had never been wrong.

We like to make it a little simpler and break it down by how stocks do when the NFC wins versus the AFC, ignoring the history of the franchises. As our first table shows, the S&P 500 gained 10% on average during the full year when an NFC team has won versus 8.1% when an AFC team has won. Interestingly, the AFC and NFC have each won 29 Super Bowls.

So, it is clear-cut that investors want the Eagles to ground the Chiefs and win, right? Maybe not, as stocks have gained over the full year 12 of the past 13 times when a team from the AFC won the championship, going back 21 years. In fact, the only time stocks were lower was in 2015, when the full year ended down -0.7%, so virtually flat.

By my math, there have been 58 Super Bowls and 22 different winners. I broke things up by franchise and city. For instance, Baltimore has won three championships, but one for the Colts and two for the Ravens. So I differentiated the two. Then the Colts won one in Indy, so I broke that out as well. Either way, I still don’t see my Bengals on here, but I expect that to change next year! Remember, Joe Burrow is the only man who can beat Patrick Mahomes and Josh Allen with a 5-3 record against them combined and a winning record against both, but I digress…

…Who should you root for? Personally, I can’t stand either team, but I guess I’ll just say when Philly wins a Super Bowl or World Series really bad things tend to happen. I’m honestly still not sure I can root for Mahomes and his ref buddies handing him another trophy even knowing this, but it is worth at least knowing.

Here are 12 other takeaways I noticed while slicing and dicing the data

Front-runnin’ the Fed? This next one’s got you covered …

As a reminder, the UST 2yr Yield is my Fed Front-Runner. It’s where incremental interest rate policy decisions get priced-in before the consensus crowd gets the Macro Awareness memo.

Wolf of Wall on imbalance of TRADE …

WOLFST: Trade Deficit in Goods Worsens to All-Time Worst in 2024, Small Surplus in Services Rises, Overall Trade Deficit Worsens by 17%

Goods deficits & Corporate America: Vietnam jumps to #3 on transshipments from China to dodge tariffs. Tiny Ireland jumps to #4 on trade invoicing to dodge US corporate income taxes.

Finally, while Mother Nature and Mr. Markets battle it out, Mother Nature having ppd my plans to travel in to NYC today — GOOD — the downside is my future resembles this, loosely (not expecting THIS much but…)