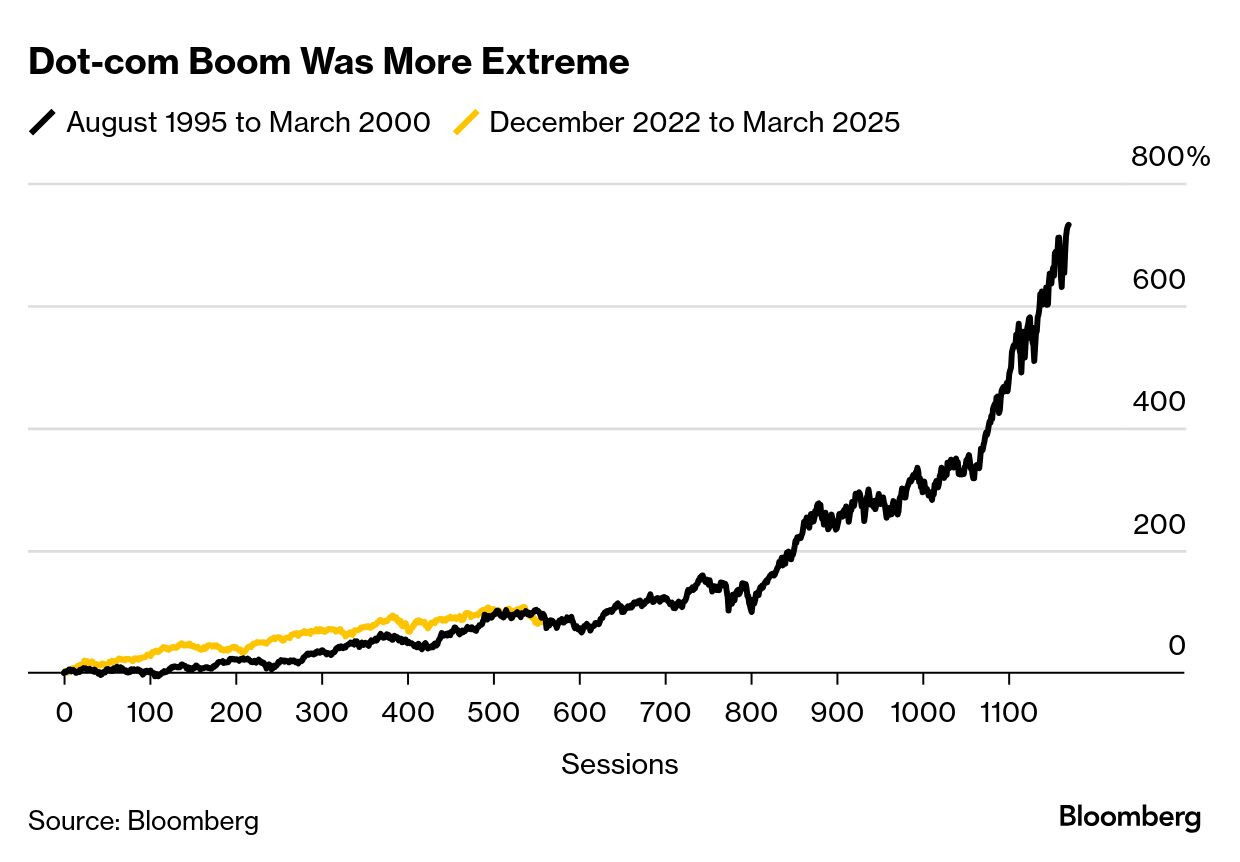

…A revolutionary new technology comes along and infatuates investors with its seemingly limitless possibilities. Euphoria sparks a stock market rally. Eventually things get overheated and share prices become ridiculous. Then it all collapses.

It happened exactly 25 years ago when the roughly five-year dot-com bubble popped, leaving trillions of dollars of investment losses in its wake. On March 24, 2000, the S&P 500 Index posted a record level it wouldn’t see again until 2007. Three days later, the tech-heavy Nasdaq 100 also closed at an all-time high, the last time it would do that for more than 15 years.

Those peaks marked the end of an electric run from August 1995 to March 2000. The S&P 500 would almost triple, while the Nasdaq 100 soared 718%. And then it ended. By October 2002, more than 80% of the Nasdaq’s value was gone, and the S&P 500 was essentially cut in half.

Echoes of that era are reverberating now. The technology this time is artificial intelligence. After a rally that sent the S&P 500 soaring 72% from its trough in October 2022 to its peak last month, adding more than $22 trillion of market value in the process, signs of trouble are emerging.

Stocks are starting to sink, with the Nasdaq 100 losing more than 10% to fall into a correction and S&P 500 briefly dropping to that level. And the symmetry is raising frightening memories from a quarter century ago…

Fitting, then, there seems to be a bit of an attempted ‘sticksave’ then …

PiQ The Overnight News Roundup - March 24

MACRO: Risk on after US President Trump is planning a more targeted tariff approach on April 2nd than initially thought, according to sources in both the WSJ and Bloomberg. Articles suggest the reciprocal tariffs will be focused on those with trade surpluses with the US whilst the planned sector-specific tariffs, such as chips, autos, and pharma, will now not be announced at the same time. (WSJ/BBG)

AND from ZH …

Sunday, Mar 23, 2025 - 11:37 PM ZH: Futures Jump On Report Trump Reciprocal Tariffs To Be "More Targeted" Than Feared

A Bloomberg article dropped yesterday and it suggests that the new tariffs on April 2 are poised to be more targeted than originally feared; this is helping spark a risk on move across global markets, and push US futures about 0.7% higher late on Sunday.

According to the report, "Trump is preparing a “Liberation Day” tariff announcement on April 2, unveiling so-called reciprocal tariffs he sees as retribution for tariffs and other barriers from other countries, including longtime US allies. While the announcement would remain a very significant expansion of US tariffs, it’s shaping up as more focused than the sprawling, fully global effort Trump has otherwise mused about, officials familiar with the matter say.

Trump will announce widespread reciprocal tariffs on nations or blocs but is set to exclude some, and — as of now — the administration is not planning separate, sectoral-specific tariffs to be unveiled at the same event, as Trump had once teased, officials said."

So while we wait for more color about what Trump will unveil on Liberation Day, below we share the latest thoughts from Goldman trader John Flood on where we stand right now…

… here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

The Trump administration is soon due to implement reciprocal tariffs on countries with which the United States has large trade deficits or places where it faces high tariffs and non-tariffs barriers. This chart shows how those deficits stack up. The latest news reports say the April 2 moves are likely to exclude a set of sector-specific tariffs, though the details of next week's moves remain sketchy…

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Don’t just do something. Sit there!

23 Mar 2025 BNP: Sunday Tea with BNPP: Wait and see

KEY MESSAGES

With upside risks to inflation and downside risks to growth, we think the Fed continues to favor an extended pause.

We think the Fed is more concerned about inflation risks than it lets on. It just doesn’t want to open the possibility of hikes right now.

After last week’s passage of debt brake reform in Germany, we will be watching this week’s refinancing announcement closely.

This next one is a German shop runnin a survey — while not THE ‘fund manager’ survey everyone talks ‘bout, I promise this is a close second …

24 March 2025 DB: March 2025 Global Markets Survey Results

Here are the results of our latest global markets survey with 400 responses between March 17th-20th 2025.

Some high level views:

Responses suggest perceived tariff risk is going up but that 62% still think Trump will put in sustained tariffs softer than his campaign pledges.

However the average sustained tariff rate expected to be imposed on the EU averages a whopping 18%.

European equities are aggressively favoured over the US over the next 12 months but over 5 years this flips back heavily in the US’s favour. So US exceptionalism is expect to return after a continued lull in 2025.

Germany is expected to grow at 1.2% on average over the next 5 years with a peak 10yr Bund rate of 3.7% over this period.

The US recession risk over the next 12 months is seen at 43% on average but the distribution of responses was very wide.

A surprisingly huge majority think this US administration actively want a weaker dollar.

…53% believe 10yr USTs will top out above 5% over the next 5 years but “only” 19% expect a peak above 5.5%. The average is around 5.2%, nearly 100 bps above current.

Another instance where we know what to ask but the answers what matters most and everyone’s got an OPINION …

March 23, 2025 MS: Sunday Start | What's Next in Global Macro: So What Happens Next?

Conversations in the past few days have centered on whether the market has stabilized. The Fed highlighted the risks to slower growth and higher inflation that the market had already internalized, so … is the worst over? The Fed dot plot was largely in line with Morgan Stanley US Economics' views of weaker growth and firmer inflation. The question for investors is whether the storm has passed or if we are in its eye. My view is that the market got the right answer on the economic slowdown in the US, but for the wrong reasons. The real slowdown has yet to show up in the hard data. Our equity strategists also caution about further risks to earnings downgrades. We think there is more bad news to come for the US economy as substantial shifts in policy wend their way through the economy…

…So are all the cries about a recession overdone? Probably. The strongest evidence to date is in “soft” data, and we will always lean on hard data over soft data. The January retail sales data spooked many investors, but last week’s February data showed that concerns were overdone. In our forecast, the meaningful slowing might not show up for over another quarter, but we will be following the nonfarm payrolls data even more closely than usual.

While we think the US will slow down and that we are only in a bit of a lull right now, we noted last week that the view on Europe has shifted notably as well. The change in fiscal stance has real upside for Europe, but we think optimism should be tempered. Our economists in Latin America are expressing similar sentiment. Ultimately, however, the world is still connected, so tariffs will hurt not only global trade but also corporate confidence, and the slowdown we expect in the US will weigh on other economies…

Same shop with some math help (don’t do math on the weekends so this a rough way to start the day BUT …)

March 24, 2025 MS: The Weekly Worldview: Balance Sheet Math

The Fed slowed the pace of balance sheet runoff. We delve into what this means for balance sheet mechanics.

Last week’s Fed meeting was largely in line with ours and the market’s expectations, but the decision on the balance sheet is worth a bit more discussion. Prior to the meeting, there was speculation that QT would end. We did not think it would, but the reality ended up in the middle. The Fed effectively cut the pace of QT in half, lowering the monthly cap for redemption of Treasury securities to $5bn, from $25bn, starting in April, but leaving MBS runoff unchanged. The latter has been averaging roughly $15bn/month. With that change in hand, some additional mechanics are worth revisiting.

First, one key issue for Fed officials was the debt limit. When the debt limit is binding, the U.S. Treasury begins to draw down its cash in the Treasury General Account (TGA) at the Fed by paying down maturing bills held in the market. This action leads to two effects. The payments out of the TGA lead to a rise in reserves in the banking system, with some spillover into ON RRP balances, which puts downward pressure in funding market rates. Simultaneously, the scarcity of Treasury bills pushes down those yields, and that factor further suppresses money market rates. But when the debt limit is lifted, the TGA is rebuilt by issuing Treasury bills again, which jointly drains reserves and pushes up bill rates. These factors push up all funding market rates and can induce volatility. Chair Powell noted last week that these developments cloud the signal the FOMC takes about when to end QT, hence the slowing in QT. By reducing the pace of the runoff, we think the runway for QT could now extend well into 2026.

When President Donald Trump was asked on Friday about his tariff policies, he said: "I didn’t change my mind. I don’t change. But the word ‘flexibility’ is an important word. Sometimes there's flexibility. So there will be flexibility, but basically it's reciprocal." A WSJ article posted at 5:26 pm today is titled "White House Narrows April 2 Tariffs." It reports: "The administration is now focusing on applying tariffs to about 15% of nations with persistent trade imbalances with the U.S.—a so-called “dirty 15,” as Treasury Secretary Scott Bessent put it last week." The tariffs might be effective immediately on April 2. Furthermore: "The administration’s shift comes after weeks of tough talk with trading partners and U.S. industries alike. Officials from Canada and Mexico said they were told there was no way to avoid reciprocal tariffs ahead of April 2, though they hoped Trump would be open to reducing tariffs through negotiations after that date."

The stock market may be bottoming on the prospects that the tariffs might be more targeted and negotiable. Trump certainly provided a one-day Trump Put on Friday, when the S&P 500 dropped sharply on the open but rallied to close slightly above Thursday's close.

We still expect the stock market to be choppy through mid-year, but it could be choppier to the upside now that it has been choppy to the downside since mid-February. Over the past 10 years, March has been a weak month for the S&P 500, with a zero return on a year-to-date basis on average (chart). Then the index rallied by six percentage points on average through late July.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Torsten Slok with some immigration and NFP perspectives …

March 24, 2025 Apollo: Lower Immigration Will Pull Down Nonfarm Payrolls Over the Coming Months

A US border encounter is defined as a law enforcement encounter with a person who unlawfully crossed the border between ports of entry or a person who entered at a port of entry but is inadmissible.

The chart below shows that there were almost zero border encounters in February 2025. The sharp decline in immigration in recent months will have very significant implications for nonfarm payrolls in March, April, and May because it could lower the population growth-consistent nonfarm payroll estimate to 60,000, down from as much as 200,000 in 2024.

Put differently, the ongoing sharp decline in immigration will automatically result in a sharp decline in nonfarm payrolls over the coming months.

The Terminal.com on what the bond market is watchin’ …

March 23, 2025 at 7:00 PM UTC Bloomberg: Bond Market Looks to Inflation Data to Back Steeper Yield Curve

… A highlight of this week’s busy economic data calendar is personal income and spending data for February, on Friday. The report includes the inflation gauge the Fed aims to have average 2% over the long run. It was 2.5% in January and economists expect it to remain there, while the core rate excluding food and energy is seen accelerating to 2.7% from 2.6%…

… while thats all well and good, we’re all really watchin whatever Bessent’s watchin (ie the 10yy) …

March 23, 2025 at 3:42 PM EDT Bloomberg: ‘Don’t fight Bessent’s Treasury’ is new mantra in US bond market

(Bloomberg) — Treasury Secretary Scott Bessent can’t stop talking about 10-year bond yields. In speeches, in interviews, week after week, he states and restates the administration’s plan to push them down and keep them down…

…In the past couple weeks, chief rates strategists at Barclays, Royal Bank of Canada and Societe Generale have cut their year-end forecasts for 10-year yields in part, they said, because of Bessent’s campaign to drive them lower. It’s not just the jawboning, they added, but the fact that Bessent can follow it up with concrete action like limiting the size of 10-year debt auctions or advocating for looser bank regulations to boost bond demand or backing Elon Musk’s frantic campaign to cut the budget deficit.

“What used to be often mentioned in the bond market is the idea of don’t fight the Fed,” said Guneet Dhingra, head of US interest rates strategy at BNP Paribas SA. “It’s somewhat evolving into don’t fight the Treasury.”

Yields have come down already, plunging a half-percentage point on the 10-year — and by similar amounts across the rest of the Treasury curve — over the past two months.

That sharp move, to be clear, is less about Bessent and more about his boss, President Donald Trump, whose tariff and trade-war threats have sparked fears of a recession and pushed investors out of stocks and into the safety of bonds.That’s not exactly the kind of bond rally Bessent had in mind — he wants it to be the product of fiscal discipline and sustainable economic growth — but it has only added to the sense among some in the market that this administration is going to bring down yields one way or another.

A representative for the Treasury didn’t respond to a request for comment…

… For Blake Gwinn, head of US rates strategy at RBC Capital Markets, it was both the likely negative impact from Trump’s tariff policies on growth as well as Bessent’s push to bring yields down that prompted him to cut his 10-year yield forecast to 4.2% from 4.75% earlier this month.

“The administration has almost kind of capped 10-year yields,” Gwinn said. “They’re kind of implicitly saying, if 10-year start to move higher or the economy starts to stumble and the Fed’s not playing ball, we’re just going to go out and slash 10-year issues.”

March 23, 2025 The DAILY NUMBER: The simplest trend following system

Today's number is... 10

S&P 500’s price is currently trading under its 10-month moving average.

Here’s the chart:

Let's break down what the chart shows:

The black line is the S&P 500 index price.

The red line is the 10-month moving average of the S&P 500 index price.

The gray lines highlight when the price is above the 10-month moving average.

The Takeaway: With just six trading days left in the month, there's one model I'm paying close attention to. The bulls need to work hard to push the S&P 500 price back above its 10-month moving average. At the moment, the S&P 500 is 1.7% below this moving average. If the price stays below it, this could create challenges for stocks.

I have done the math… Take a look at the table on the chart.

If you've been following me for some time, you know that I like to know what type of market environment we’re in. One of the simplest strategies I use for assessing the longer-term environment is: If the market is above the 10-month moving average, I’m long. If the close is below that moving average, I stay mostly in cash.

I do not recommend relying solely on one signal or indicator. However, this approach requires minimal effort and tends to provide slightly better returns than a buy-and-hold strategy while helping to avoid the drawdowns that a buy-and-hold investor might face.

Positions matter and there was a large jump in net spec short (10s) and this note / link / visual for your review …

22 MAR 2025 Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

This next note by Sam Ro is another excellent post where he pulls back the curtain a bit as to how he himself acts and while the headline grabber has ones attention it’s also worth a READ to understand … while he’s talking of his own experience, it’s ‘retail’ in nature, it’s also from one with a proven track record and a thoughtful process. This thoughtful process can also be found out there on ‘Global Wall’ (and why many HFs have lockups along with steep fees — ie 2 and 20 — so as they can give themselves time … the very most important and valuable commodity) …

Mar 23, 2025 TKer by Sam Ro: The unluckiest market timer I know made another poorly timed trade

… Like most people who invest in the stock market, I too get nervous when prices are going down. When the selling gets protracted, muscle knots sometimes form in my neck and upper back.

With that said, let me tell you about a recent personal experience that confirmed to me that I’m the unluckiest market timer I know.

I bought the top, again

… On Feb. 13, I met with my accountant to do my 2024 tax returns. I learned I had some room to lower my taxable income. And one of the actions I took was contributing more to my self-employed 401(k) plan.

Wasting no time, I transferred cash to that account. And on Feb. 18, I added to my S&P 500 index fund position. The trade confirmation came in on Feb. 19.

… Coincidentally, Feb. 19 was when the S&P 500 last touched a record high before rapidly tumbling into the correction we are living today.

(Source: Yahoo Finance)

This was not a small amount of money I put to work.

Was it poorly timed? Yes.

Was it a mistake? No…

Read on for more (and the charted recap of global macro) and learn / enjoy…

We know the BIG question but does anyone have THE answer?

Sun, March 23, 2025 at 8:30 AM EDT Yahoo: The biggest question facing the stock market

The biggest question facing markets right now is not when Nvidia (NVDA) stock will begin to go up every single day again.

Sorry to burst your bubble.

The biggest question staring markets in the face is this...

Does US economic growth in the first half of the year represent just a slowdown that settles in at a short-term bottom while still increasing? This would be an example of economic resilience in the face of major policy uncertainty out of D.C. Said slowdown, I can argue, is about nearly priced into stocks.

Or does the budding economic growth slowdown go off a cliff into a recession as businesses and consumers tighten up their spending, with tariffs permeating and Trump's tax cut extensions being unknowns? I fancy a recession is not priced into stocks.

"Things feel slower," one CEO of a large-cap consumer company told me over drinks this week…

…JPMorgan strategist Bruch Kasman made some hay this week by calling out a 40% recession probability for this year. To my knowledge, this is the second-highest recession probability on the Street behind BCA Research's veteran forecaster Peter Berezin — he's at 75%.

But comments like this aren't just playing out over cocktails or in hard-to-get research notes. They are beginning to surface on earnings releases and calls by large public companies. And the market is moving fast to price in something more than a simple economic slowdown…

This next one makes ME pause and ask if this is signal or noise … tend to think more noise but …

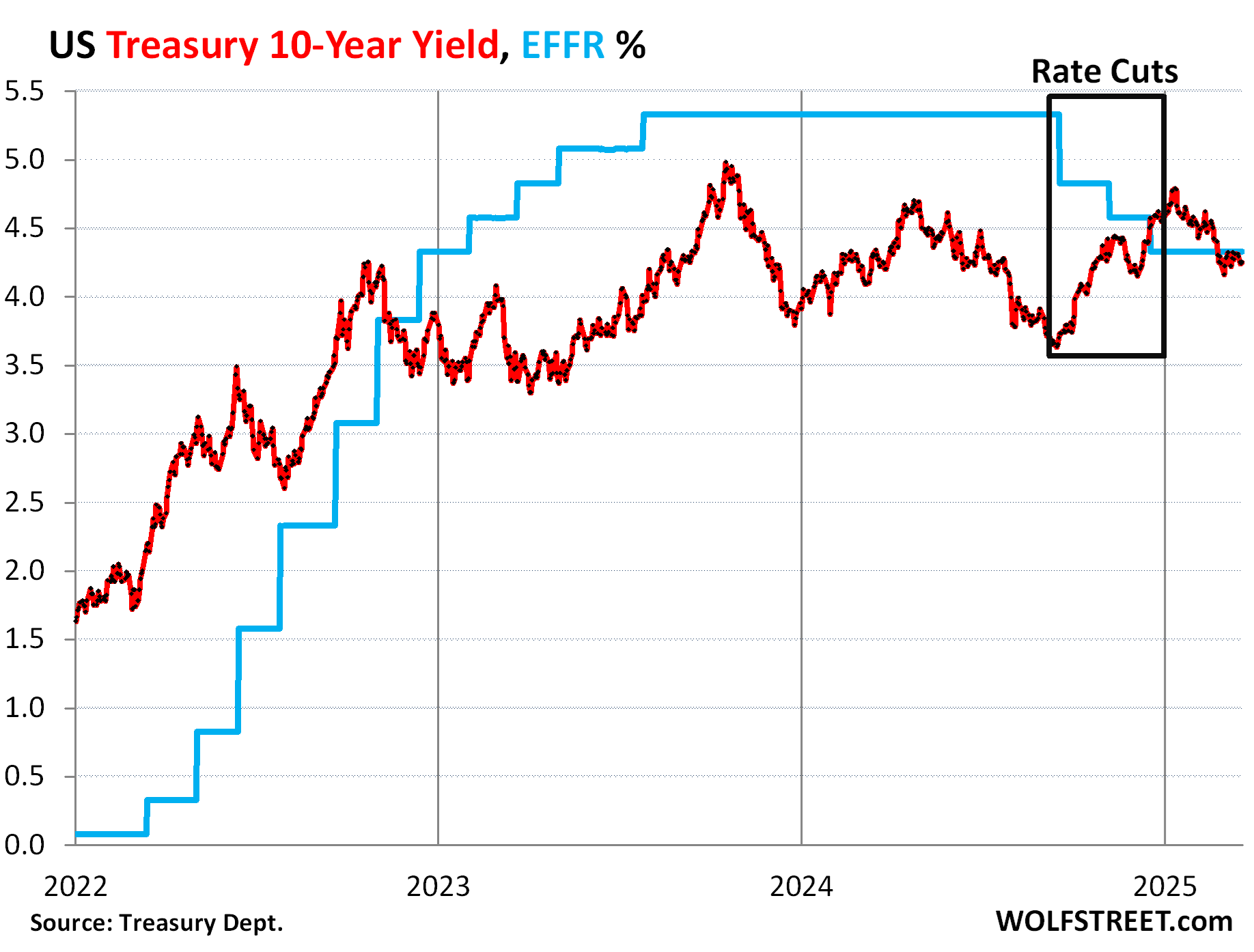

Mar 22, 2025 WolfST: Treasury Yield Curve Re-Inverts with Sag in the Middle, as Government Swats Down 10-Year Yield. But Mortgage Rates Don’t Follow all the Way, Spread Widens

Short-term Treasury yields of 6 months or less stay put above 4%.

…These efforts have been fortified by the Fed’s more hawkish stance on inflation and interest rates, which put the bond market at ease. The bond market had gotten spooked by the Fed’s 100-basis-points in rate cuts despite re-accelerating inflation, which triggered a bond selloff that had caused the 10-year yield to spike by 114 basis points, even as the Fed cut by 100 basis points. The long-term Treasury market fears out-of-whack inflation more than anything.

…But short-term yields of 6 months or less stay put above 4%. The six-month Treasury yield had already priced in a big part of the 100-basis-points in rate cuts by the time the first rate cut happened, having dropped by 90 basis points from 5.4% in May to 4.5% just before the September cut.

Today, it’s at 4.23%, still glued to the underside of the EFFR, pricing in only a minuscule chance of a rate cut within its window over the next few months.

Hey man my Forester only has an Olympic Valley Ski & Bike Shop sticker what you talkin bout Willis?! I don't wear my sandals mines a 5-speed manual. LOL hilarious!!!

Hey man my Forester only has an Olympic Valley Ski & Bike Shop sticker what you talkin bout Willis?! I don't wear my sandals mines a 5-speed manual. LOL hilarious!!!