FT: Top Federal Reserve official says market angst over inflation would be ‘red flag’ Austan Goolsbee’s warning comes after key survey shows consumers expect soaring price growth

Signs that investors in the US bond market are baking in higher inflation would be a “major red flag” that could upend rate-setters’ plans to cut interest rates, a top Federal Reserve official warned.

The remarks from Austan Goolsbee, president of the Chicago Fed and a voting member of the Federal Open Market Committee, come just over a week after a closely watched University of Michigan poll showed households’ long-term inflation projections hit the highest level since 1993.

“If you start seeing market-based long-run inflation expectations start behaving the way these surveys have done in the last two months, I would view that as a major red flag area of concern,” Goolsbee told the Financial Times…

…Goolsbee said he believed borrowing costs would be “a fair bit lower” in 12-18 months from now, but cautioned it may take longer than anticipated for the next cut to come because of economic uncertainty.

“My view is that when there’s dust in the air, ‘wait and see’ is the correct approach when you face uncertainty,” he said. “But ‘wait and see’ is not free — it comes with a cost. You gain the ability to learn new information, [but] you lose some of the capacity to move gradually.”…

… for more, to the twitter-sphere …

at stlouisfed

From the FRED Blog: Before COVID-19, markets expected inflation to be higher in the longer term (30 years) than in the medium term (five years). How did inflation expectations change during the high inflation of 2021-22? https://ow.ly/VSHZ50VnLF7

5yy DAILY: 4.06% (50% of range visualized just below) …

… (up)TLINE remains in place and so, resistance ‘round 3.95 while ‘support’ up nearer 4.25% … with TLINE and momentum still lined up for further cheapening I suppose I’d wait for some greater sort of dipORtunity (north of current levels) on the odd chance could pick something up on the cheap … I know I know, famous last words …

… for somewhat more from that site with a Terminal …

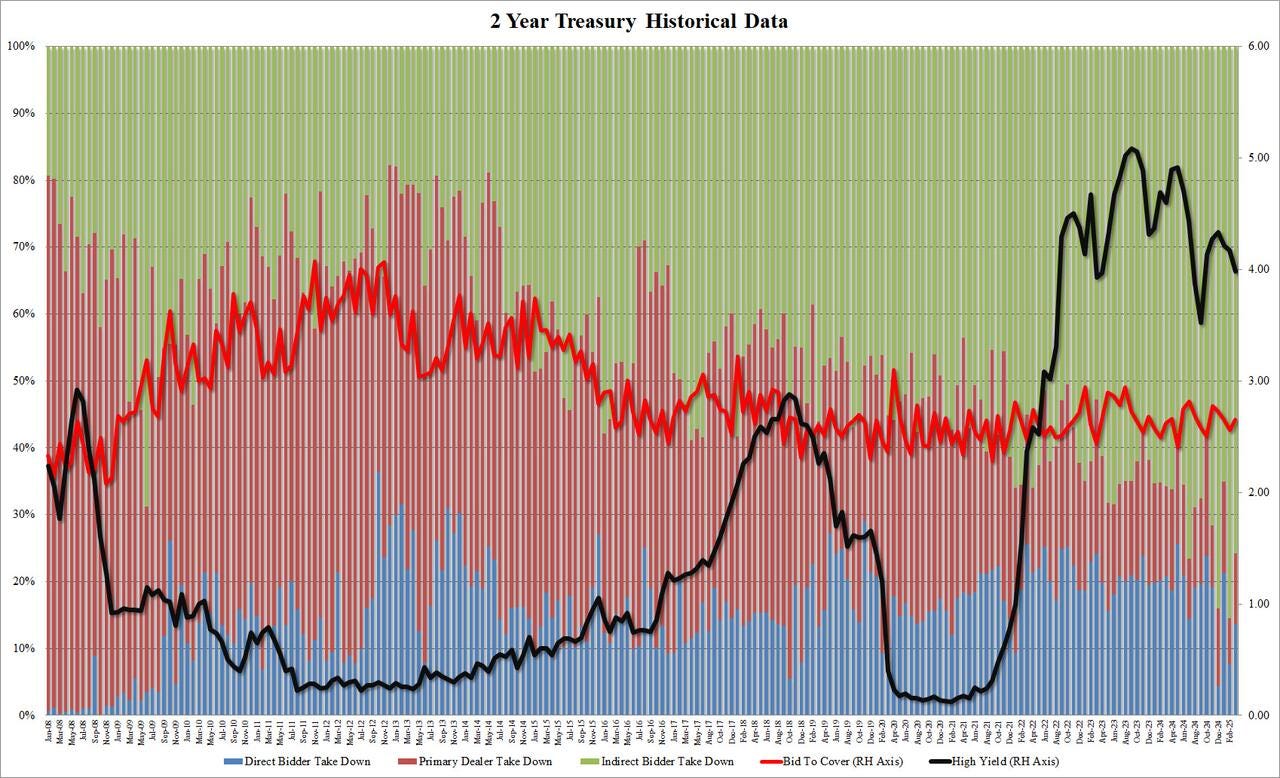

… AND in context of yesterday’s 2yr auction, the bar has been raised …

ZH: Stellar 2Y Auction Stops Through Amid Solid Foreign Demand

…The internals were solid, as Indirects took down 75.8%, down from 85.5%, but above the recent average of 71.7%. And with Directs awarded 13.6%, Dealers were left holding 10.7%, above last month's near record low 6.9% below the recent average of 12.0%.

Overall, this was a very strong auction and one which obviously did not need a concession (10Y yields slid 6bps from session highs of 4.36% earlier to 4.30% at the time of the sale) to price on highly beneficial terms.

… which was, to some degree, a product OF the data …

ZH: Philly Fed Services Survey Crashes To Weakest Since COVID ZH: US Home Prices Hit A New Record High In January... Except In Tampa

… AND …

Tuesday, Mar 25, 2025 - 02:12 PM ZH: Conference Board Consumer Expectations Plunge To 12 Year Lows; Inflation Expectations Rise

Another day, another sentiment measure disappoints...

The Conference Board Consumer Confidence headline print fell from 100.1 (upwardly revised) to 92.9 (below 94.0 exp). Under the hood, it was not pretty with the measure of expectations for the next six months dropped nearly 10 points to 65.2, the lowest in 12 years, while a gauge of present conditions declined more modestly.

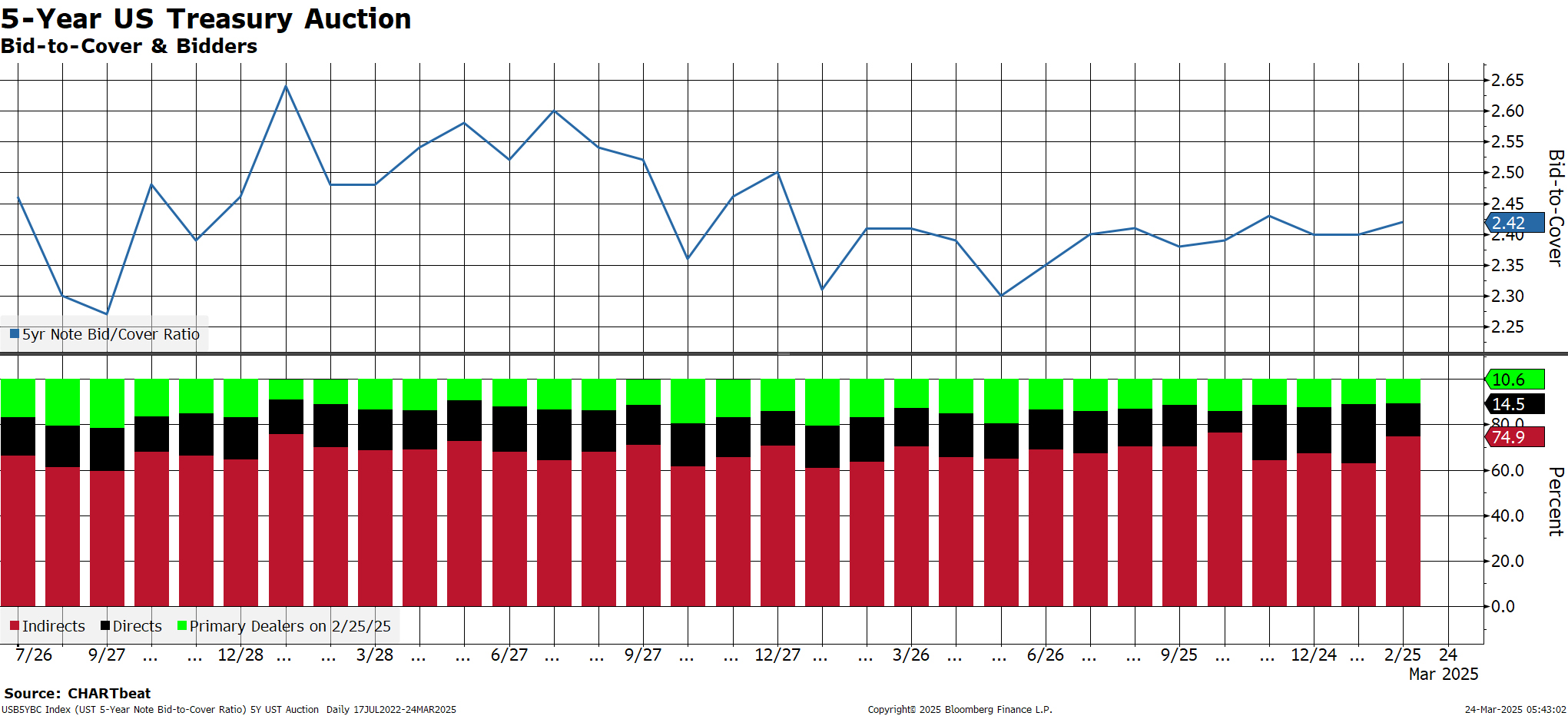

AND … here we are. Get those bids in for 5s early and often. Meanwhile … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly cheaper and steeper after a brief spike higher into the LDN crossover, with WTI rallying towards $70/bbl on lower stockpiles and the BCOMIN simmering near 6-month highs as copper import tariff duties are re-floated. S&P futures are showing -5pts here at 7am, while Eurostoxx are a tad softer after Chinese/APAC bourses softened a bit as well overnight (CNT -0.3%, SENSEX -0.9%, HSI +0.5%). The 2s10s curve is +3bps, 2s510s +2.5bps with long-end reals leading the nominal backup. The DXY is basically flat, with USDJPY +0.3%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWKUS Market Open: US futures modestly lower amid tariff reports, GBP lags & EUR/USD attempts to reclaim 1.08 … USTs in the red but only modestly so with action relatively steady in the European morning as we await updates to numerous catalysts in addition to Fed speak, data and supply with 70bln of 5yr Notes due and following the 2yr tap on Tuesday which was strong when compared to recent averages though not quite as well received as the outing in February.

Yield Hunting Daily Note | March 25, 2025 | Pioneer Muni CEFs, JQC, VVR/VLT Mess, SWZ Special & Update

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

What’s the end game, you ask? I’m not sure but others have ideas …

24 March 2025 ABN AMRO: US Watch - Tariffs are not the endgame | Insights newsletter

There is increasing noise on a ‘Mar-a-Lago accord,’ an idea outlined in a paper by CEA Chair, Stephan Miran. The accord is part of a grand plan to devalue the dollar, similar to the 1985 ‘Plaza Accord,’ that is envisioned to increase US manufacturing competitiveness, and revitalize the economy.

The framework of this plan uses tariffs and defence support as strategic tools in negotiations

The US’ business cycle stage, and changes in configuration of the global economy since 1985, make a successful repeat of the 1985 Plaza Accord unlikely, thought that may not deter the Trump administration

A statement of the Trump’s administration intent, and shifts in fiscal outlooks, both in the US and its major trading partners, have already pushed the dollar down but not enough to reduce the need for the accord

The overall plan is inflationary and suppresses growth.

…What does orthodox economic theory say about how a government can simultaneously decrease the trade deficit and depreciate the dollar? The standard approach would be fiscal tightening; cut spending and responsibly raise taxes. As domestic demand for goods decreases, imports decline. Higher taxes can encourage higher savings rates, which reduces the need for foreign capital to finance investments, improving the current account deficit. Lower demand is also likely to lead to lower inflation, which may lower Fed interest rates, which in turn depreciates the dollar. This improves the competitiveness of US exporters, boosting exports, leading to further reductions in the current account deficit.

British shop on confidence …

25 March 2025 Barclays: March consumer confidence: Pessimism all around

The Conference Board's index of consumer confidence declined to 92.9 in March, the lowest level since January 2021 amid broad-based pessimism in the survey. This comes alongside a 0.4pp increase in average inflation expectations to 6.2%.

Downgrade 2025 estimates and price target in response to tariffs and weakening survey data; bull & bear cases capture trade policy uncertainty, with bear market potential in the latter; in our base case of gradual recovery, prefer Financials/Healthcare/Big Tech to Industrials/Consumer/Commodities.

… whatever goes UP must come down?

Best in show on confidence …

March 25, 2025 BMO: Consumer Confidence Lowest Since Jan. '21; Expectations Lowest in 12 Years

Conference Board Consumer Confidence disappointed at 92.9 in March, underperforming the 94.0 BBG consensus. This represented a 7.2-point drop from February's upwardly revised 100.1. For context, this is the lowest read on headline confidence since January 2021. Present Situation fell to 134.5 from 138.1 in February. This is the lowest in six months. Expectations dropped to 65.2 from 74.8 in this prior month. This is the lowest since March 2013. Within the details of the report, the observation was made that, "Consumers’ expectations were especially gloomy, with pessimism about future business conditions deepening and confidence about future employment prospects falling to a 12-year low. Meanwhile, consumers’ optimism about future income—which had held up quite strongly in the past few months—largely vanished, suggesting worries about the economy and labor market have started to spread into consumers’ assessments of their personal situations.” Moreover, average 12-month inflation expectations rose to 6.2% vs. 5.8% in February, the highest in almost 2 years. The Labor Differential was effectively unchanged at 17.9 vs. 17.6 prior…

… As for Tuesday’s monetary policy discourse, Fed Governor Kugler maintains that the FOMC can hold the current federal funds rate for ‘some time’ as it monitors the evolution of the economy. Aside from Kugler’s reiteration of the waitand-see messaging, there were two more noteworthy observations made by the dovish-leaning Fed Governor in Washington DC. First, “while goods inflation was negative in 2024—as was the norm before the pandemic—it has turned positive in recent months. This development is unhelpful because goods inflation has often kept a lid on total inflation and also affects inflation expectations.” Policymakers have become increasingly worried about the implications for total inflation from losing the drag of core goods long before the full impact of tariffs has been realized. Second, “In addition to the increase in prices already captured in official data, surveys show that consumers are expecting further increases in the near term. For instance, both short-run and long-run inflation expectations from the Michigan survey have climbed in recent months.” While Powell characterized U-Mich inflation expectations as ‘kind of an outlier’, the data series is clearly weighing on the aggregate inflation confidence of the Committee – even the doves…

RATES IN A RANGE … here’s a short-term look from one of if not THE best in the techAmental biz…

US yields are testing the upper end of short term ranges. We continue to think that there is limited room for a move higher in yields, despite coming close to a crossover in weekly slow stochastics. Longer term, we retain our view for a further move lower in yields…

…US 10y yields US 10y yields broke above 4.35% (March 13 high) briefly, though we failed to close below it. Subsequent resistance is at 4.45% 55d MA).

Short term, 10y yields continue to look within a range, and we continue to think we are more likely to see a move towards 4.13% (December low) in a reversion.

Weekly slow stochastics has crossed over, but did not enter 'oversold' territory, which nulls the potential signal for a large move higher in yields.

We continue to think we will see a move much lower towards 4.00-4.06% psychological level, 61.8% Fibonacci) in the medium term, and 3.40%-3.60% (200w MA, 2024 low) in the longer term.

US 30y yields Briefly broke above the 4.68% resistance (Nov 2024 high), and tested 4.71% (55d MA). Similarly, we see limited upside in yields, despite the cross higher in weekly slow stochastics.

For now, we continue to see support at the 4.46%-4.49% (200d MA, 55w MA) region.

Pausing a moment from the confidence review for this note on a new ‘user fee’ concept for those in UST market …

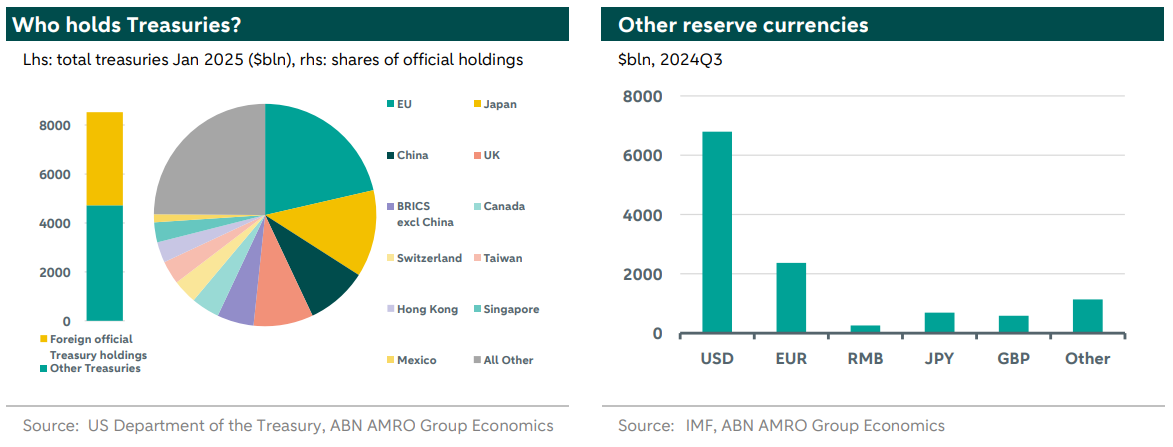

The “Mar-a-Lago Accord”, a term and idea coined by Council of Economic Advisers chair Stephen Miran in a paper last November, has received significant attention from market participants given the uncertainty created by the current administration’s policy mix. Our research colleagues recently released a piece evaluating the rationale and potential implications of the accord, as well as the obstacles for implementing different aspects of it. One idea Miran floated was the implementation of a “user fee on foreign official holders of Treasury securities, for instance withholding a portion of interest payments” with the goal of reducing the accumulation of dollar reserves.

As one method of examining which countries have the most to lose if a user fee is introduced, today’s chart highlights foreign holdings of Treasuries from the Treasury International Capital (TIC) January data release. Two things to note about the chart: it is not limited to foreign official holdings as it includes all foreign holdings of Treasury securities, and a country’s holdings include custodial holdings for other parties. Taking the TIC data at face value, we see that Japan, China, and the UK are the three non-US countries with the most holdings of Treasuries by a large margin, and so they would bear the brunt of the impact if a user fee were to be implemented.

Same shop on a marketing trip here in The States using this slide deck … a couple visuals I thought worth sharing …

Whether US equities are one of the most highly correlated markets to free global trade and hence have most to lose if this reverses?

The reawakening of Europe

One of the best starts to the year for European versus US equities on record

One of the worst periods for US equities and the Dollar at this stage post inauguration since we moved to the January 20th date in 1937.

The fact that US equity markets are still very expensive historically but this depends on whether tech super normal earnings are sustainable or not.

A look at capex boom and busts through history and how it pertains to AI.

Finally, a brief look at what are worrying demographics longer term and the very high correlation between this and economic growth.

…This is around the joint second-largest rally post inauguration since daily UST data starts… bond yields have been higher 13 out of 16 occasions since 1965.

…It is not so surprising that the US is turning to tariffs if you look at the full sweep of history. The US has a long history of tariffs, which played a key role in the early industrialisation stage

We show that the Treasury market is not discounting a recession currently – even with the US consumer somewhat navel gazing. Still spending, but not thrilled about the future, it seems. In the UK, the Spring Statement lends itself for another look at fiscal trajectories. In fact, Germany compares rather well, despite the planned spending splurge…

Still playing the 4.25% to 4.35% trading range for the US 10yr till 2 April …We still see the US 10yr yield as trading between 4.25% to 4.35% for this week, and at least into 2 April when we can finally get some steer as to what it all means, even if only as a first passthrough with more to come. We need to get there first though…

Covered wagons circlin’ consumers and their confidence …

March 25, 2025 Wells Fargo: Consumer Confidence: Inflation Worries Lead to 12-Year Low in Expectations

Summary Consumer confidence continued a four-month string of declines in March, and consumers reported a broad deterioration in their assessment of the inflation outlook and business conditions. The Expectations Index fell to its lowest point in 12 years, as the uncertain impact of tariffs continues to cloud the outlook for consumers.

Consumers are feeling okay about the present situation, but they are losing their confidence in the future. The obvious cause of their anxiety is Trump Turmoil 2.0. The Trump administration admits that its trade and DOGE policies might cause some economic pain in the short run but says they should lead to big gains in the long run ("The Golden Age of America").

The problem is that we Americans don't do pain very well. Americans are worrying that a recession is becoming more likely and that means fewer jobs. As a result, yesterday's big rally in the stock market stalled today following the release of the March consumer confidence report this morning. We continue to expect a choppy stock market for the next couple of months.

Consider the following:

(1) Confidence. The Consumer Confidence Index (CCI) dropped sharply to 92.9 during March, to the lowest reading since January 2021 (chart). The drop was led by the CCI expectations component to 65.2, the lowest reading in 12 years. The CCI present situation component dipped but remained relatively high.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

I love a parade … not so much a healthy debate which clearly due to lack of certainty …

The chart below shows individual FOMC members’ forecast of where they think interest rates will be over the coming years. The degree of disagreement on the committee is remarkable, with one FOMC member saying that in 2026, the Fed funds rate will be almost 4%, and other FOMC members saying that they think interest rates in 2026 will be just above 2.5%.

The dot plot also shows that there is debate about where the Fed funds rate will be in the long run, also with a range between 2.5% and 4%. Perhaps most importantly, none of the FOMC members are predicting a sharp decline in the Fed funds rate to zero, telling the market that nobody on the FOMC is expecting a recession.

Here’s an updated look at positions from the view of one of the very best The Terminal has to offer …

March 25, 2025 at 4:30 PM EDT Bloomberg: Options Traders Cut Back Expectations for US Rate Cuts This Year

(Bloomberg) -- As President Donald Trump moderates his approach on tariffs, options and futures traders are betting that the Federal Reserve won’t have to cut interest rates as much to fend off a recession…

…The shift has been noticeable in the market for options on the Secured Overnight Funding Rate, which is closely tied to the fed funds rate. On Monday and Tuesday of this week, one new position was established, with a premium of more than $10 million, that would benefit if the Fed avoids making any moves this year, and do even better if the next change is a rate hike, rather than a cut.

The expectations for a more hawkish Fed pursuing fewer rate cuts was also visible in the market for futures tied to the fed funds rate. Short positions that would benefit if rates don’t fall have been building this week.

Traders are also becoming more bearish on Treasury bonds as the chances of rates cuts go down. A survey of JPMorgan clients released Tuesday showed that net long positions in the Treasury market are at the lowest level in five weeks as outright longs dropped for the third consecutive week.

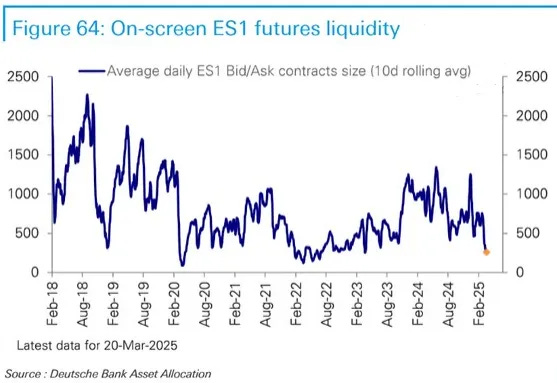

Another from The Terminal on liquidity … water water everywhere yet not a drop to drink …?

March 26, 2025 at 9:30 AM UTC Bloomberg: US Stock Market Liquidity Drying Up as Trade War Concerns Mount

… Liquidity — the ease of buying or selling an asset without affecting its price — has been dwindling for years due to factors such as tighter regulations and the rise of automatic trading. Tariff concerns have introduced a new wrinkle, stoking gyrations in individual stocks that have made it harder for institutions to trade in size.

The phenomenon can be seen in a pair of widely tracked liquidity measures. Liquidity in S&P 500 stock-index futures, as measured in the most active contract, stands at a two-year low, data compiled by Deutsche Bank AG show. Meanwhile, the five-day moving average of Citigroup Inc.’s liquidity index, which is based on futures volumes for the S&P 500, is also hovering near its lowest level in two years.

“This concerns us and it’s really frustrating,” said Rob Friesen, chief operating officer at Las Vegas-based Bright Trading. “Tariff fears exacerbate swings in individual stocks, so then you feel like you’re getting run over every time the algo trades kick in when volatility spikes.”

Low liquidity can push up the costs of portfolio hedging for traders large and small, while widening the spread between buy and sell prices until it becomes difficult for investors to determine what is fair to pay. In broader markets, it can magnify stock routs if investors aren’t able to sell shares at the desired level, forcing them to take a worse price….

An OpED from The Terminal.com …

March 26, 2025 at 5:03 AM UTC Bloomberg: With a world like this, who needs a Bond villain? They only live twice — how global imbalances are more dangerous than a trade war.

… After a while, people worked out that China had a lot at stake in the value of its Treasury holdings, and that any such threat would also inflict terrible damage on its own economy. Global imbalances remained, peaking after the GFC. A very gradual decline in Chinese holdings has in the last three years accelerated, in a way that does overlap with the beginning of a secular bear market for Treasuries. But now, this is perceived as an act of self-defense as China battles its own problems, and not as anything aggressive:

The reason to bring this up now, as the world braces for a concerted attempt to deal with imbalances in trade flows, is as a reminder that it hasn’t been long since the greatest worry was over imbalanced capital flows. And ironically, capital imbalances have accelerated since the GFC, to a far, far greater extent than trade flows.

AND … ugh …

Just … UGH … THAT is all for now. Off to the day job…