Good morning … elections have consequences. You know this. Markets know this. Yet somehow someone (enough of them) seem to be surprised and / or offsides and so, markets have swung wildly over the past 24hrs, since we’ve last met … yields dropped then POPPED right back above the ‘x’ that marked the spot (4.50% referenced HERE yest, on the long bond chart) … and have dropped again.

I know what I don’t know and cannot imagine we should all be jumping to the conclusions priced in by markets but I’ll leave all this to the ‘pros’ in just a moment.

First, I’ll give appropriate credit where credit is due, as Jim Bianco has earlier today, highlighting the FACT we’ve seen / heard ‘bout this all before AND from one of, if not THE most prolific of investors …

JB: 2003 Fortune article written by Warren Buffett worrying about the huge trade deficit, saying it is robbing our country, and proposed a solution that punishes importers.

Sound familiar?

NOVEMBER 10, 2003 FORTUNE: America’s Growing Trade Deficit Is Selling the Nation Out From Under Us. Here’s a Way to Fix the Problem—And We Need to Do It Now. by Warren E. Buffett

… In effect, our country has been behaving like an extraordinarily rich family that possesses an immense farm. In order to consume 4% more than we produce—that’s the trade deficit—we have, day by day, been both selling pieces of the farm and increasing the mortgage on what we still own …

… The time to halt this trading of assets for consumables is now, and I have a plan to suggest for getting it done. My remedy may sound gimmicky, and in truth it is a tariff called by another name. But this is a tariff that retains most free-market virtues, neither protecting specific industries nor punishing specific countries nor encouraging trade wars. This plan would increase our exports and might well lead to increased overall world trade. And it would balance our books without there being a significant decline in the value of the dollar, which I believe is otherwise almost certain to occur …

Times like these call for a somewhat longer-term look at 10s building on a MONTHLY look HERE …

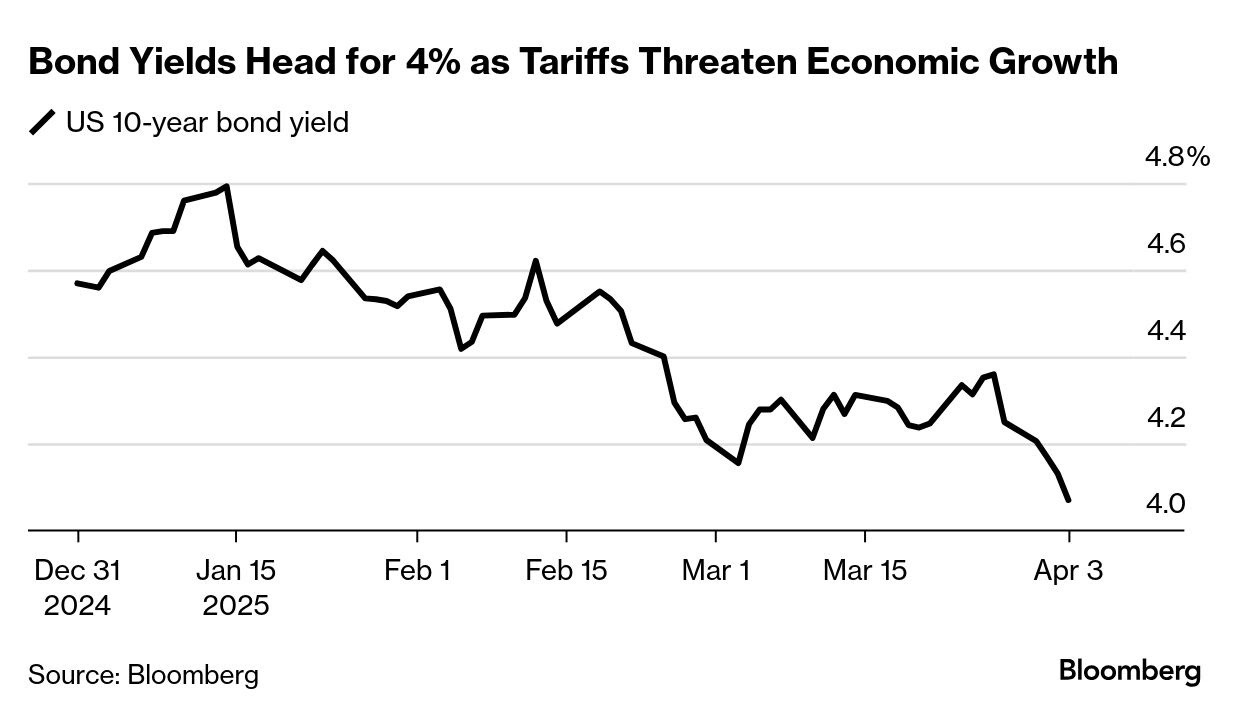

10yy: 4.00% is not just psychologically important but also, TLINE ‘resistance’ …

… and note other instances where this TLINE did not hold perfectly (summer of 2021 and then very end of 2021) but rather helped defined the (UP)trend … meanwhile, momentum becoming overBOUGHT and at this point, can / will remain so until stocks bounce …

… and NOW we know …

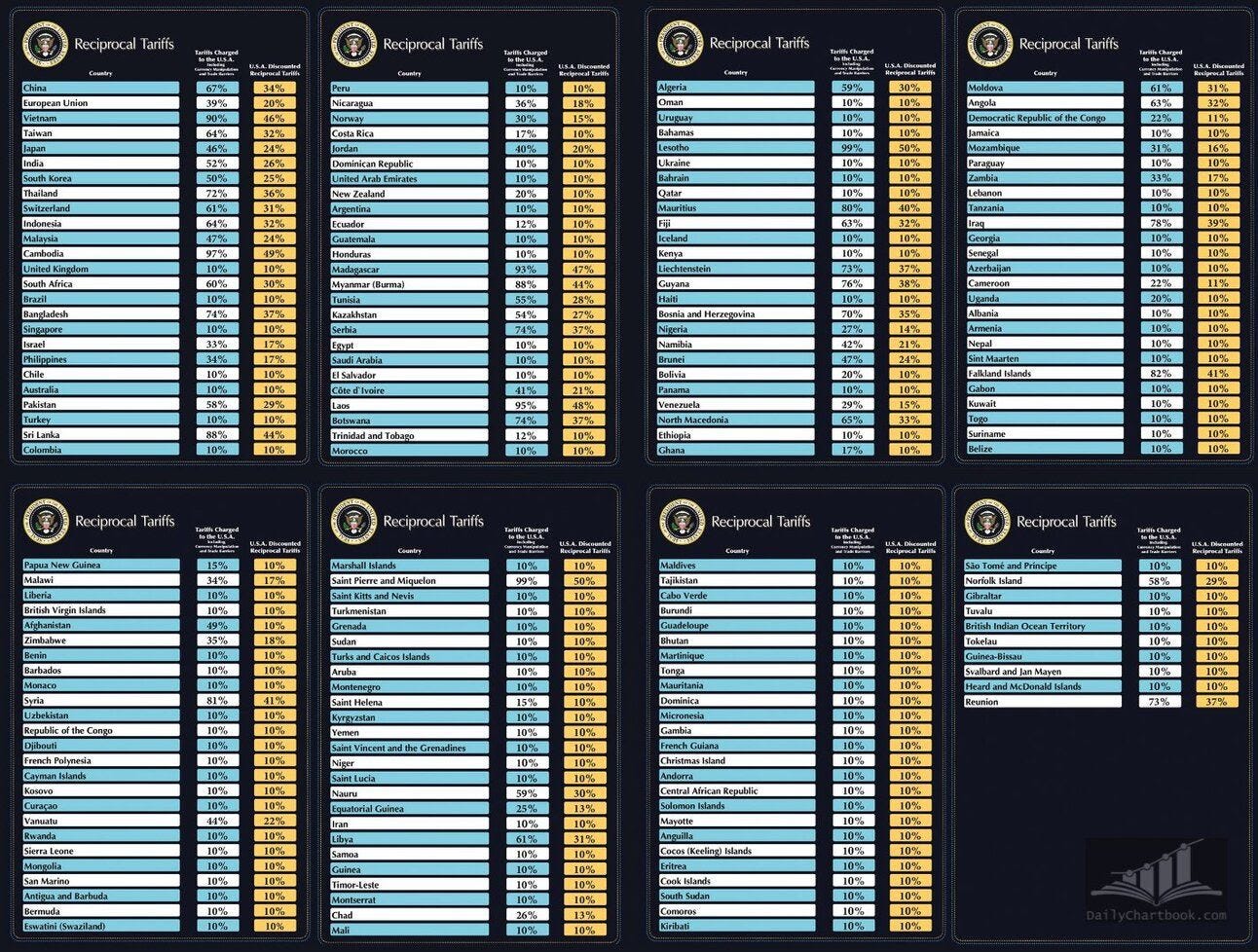

@whitehouse Liberation Day. Here is the full list of reciprocal tariffs. Noticeably absent: Canada, Mexico, Russia.

… AND a couple links …

ZH: Futures Tumble As President Trump Delivers "Declaration Of Economic Independence"

ZH: Goldman Panics: This Is Much Worse Than Expected

ZH: Wall Street Reacts To Trump's 'Liberation Day' Tariff Announcements

… With lots of news and knowns it’s gonna be busy few days ahead and sorry to say, yer on yer own after I hit SEND this morning (see scheduling update at the end) I’ll TRY and be brief …

Questions asked …

ZH: Is Trump's Plan Working? ADP Shows Biggest Jump In US Manufacturing Jobs Since Oct 2022

… unsure many want this answer and are equally quick to dismiss as its, well, ADP.

Turning then to some other data ahead of THE announcement …

ZH: US Factory Orders Surge Near Record Highs In Feb (Ignoring 'Soft' Data Slump)

… this makes somewhat more sense, I suppose … it’s both good AND bad so we can, thankfully, see it however we want.

By days end (ahead of tariff announcement above) …

ZH: Stocks Pump'n'Dump'n'Pump (Again) Ahead Of Trump's Tarrific Presser, 'Hard' Data Strengthens To One-Year Highs

I’ll quit while I’m behind … here is a snapshot OF USTs as of 705a:

… HERE’s a read of the snapshot just below, where US equity futures, ‘Earl and bond yields all cratering … saving this for posterity sake

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Risk sentiment hit after Trump’s tariff announcement, DXY below 102 whilst EUR/USD climbs above 1.11 … Yields wilt after Trump's Rose Garden speech, desks diverge on Fed implications … USTs are bid given the US tariff announcement where the initial relief on reporting around a 10% baseline gave way to marked risk-off as the reciprocal levels were announced. In brief the average US effective tariff rate is (once the measures are implemented) around 23% from around 10%. Further insight into Trump’s tariffs and how the administration feels about the initial comments/responses to the measures from various nations may be provided VP Vance and Commerce Secretary Lutnick who are due to speak from around 13:00BST. US Challenger Layoffs, Jobless Claims and ISM Services are scheduled…

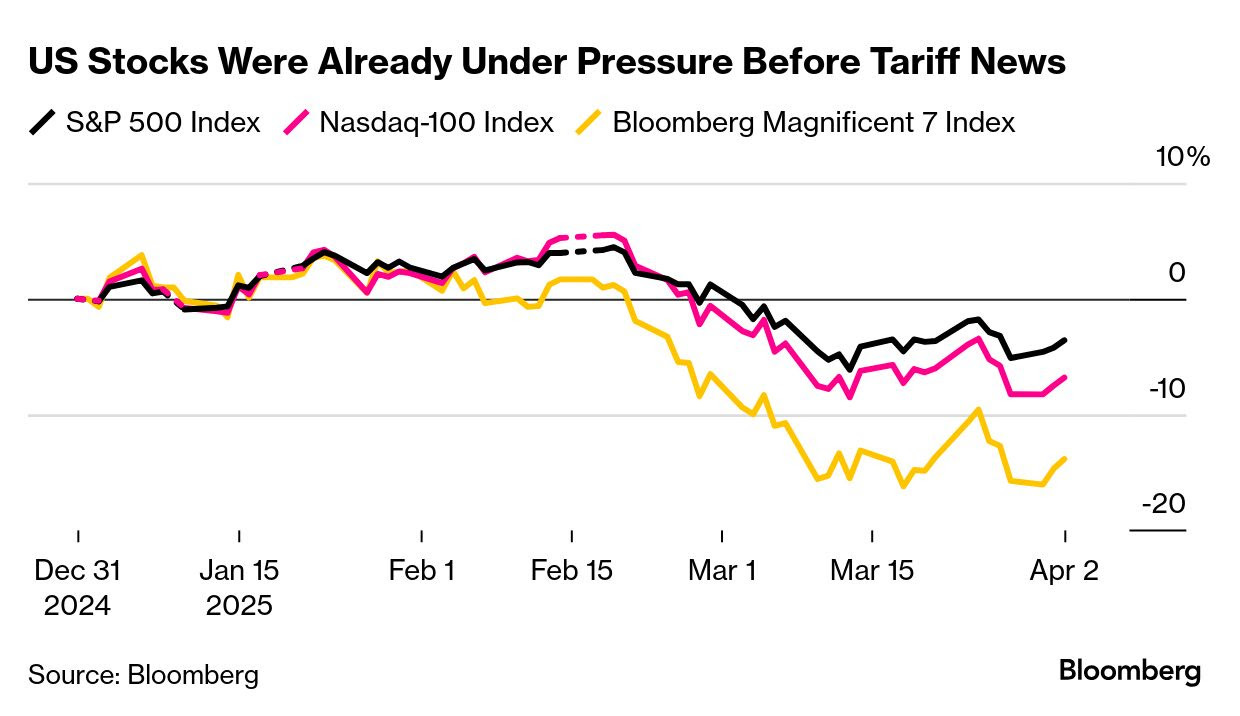

…The widespread selloff in global markets makes clear that investors don’t expect any winners from the latest — and by the far the largest — salvo in a growing trade war. But they also suggest the US itself might be one of the biggest victims of Trump’s protectionist policies.

The dollar headed for its steepest drop in almost two and a half years, as traders prepared for the economic impact.

Yield Hunting Daily Note | April 2, 2025 | Atlanta Fed, JLS Falls, FSCO Sell Opp, Blackrock Tenders

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Seems to me to be the worst of both worlds …

3 April 2025 Barclays: 'Liberation Day' tariffs set to boost inflation and risk a recession

President Trump's long-awaited reciprocal tariff announcement suggests an increase in traded-weighted tariff rates to about 23%. This causes us to change our forecast, and we now expect core CPI inflation to surpass 4% this year, real GDP to decline, and the unemployment rate to rise further.

A high price means its valuable, right? Here’s a TIPS for you …

Today’s larger-than-expected ‘Liberation Day’ tariff announcements increase the risk of a stagflationary shock to the US economy.

Even if tariffs are eventually negotiated lower, extreme uncertainty raises the likelihood of a global recession.

We see risks to equities as skewed to the downside and continue to like owning TIPS. There is increased scope for countries to let their exchange rates weaken to mitigate the impact of tariffs, thereby putting upward pressure on the USD.

… Fed: We tend to think that the Federal Reserve will, for now, remain on hold, as it struggles to manage the competing risks that the economy tips into recession, potentially a deep one, and the risk that LTIE move yet further away from the FOMC’s 2% target, entrenching inflation into the economy in way that is difficult to remove. Monetary policy will be easing in real terms in the coming months as inflation accelerates, and we believe that, in the end, protecting the Federal Reserve’s multigenerational project of delivering a sound currency and low and stable inflation will win out. But there is a notable risk that Chair Powell’s strong desire, in his last year in office, to leave a legacy of an economy on track for a soft landing will lead him to take significant risk to LTIE by easing policy regardless of inflation.

The tariff announcement opens a variety of unexpected doors. We believe the FOMC will pay close attention in the coming weeks and months to evidence that inflation is becoming entrenched into expectations and asset prices, and a range of outcomes is possible if such evidence emerges. The FOMC will also closely monitor labor market data, although we believe its ability to respond aggressively to a deterioration here is constrained by inflation considerations. Finally, we believe the Federal Reserve will also pay close attention to metrics of economic and financial stability to assess whether this rapid, unexpected, and very large fundamental restructuring of the US economy is creating large effects that require a monetary, supervisory or macroprudential response.

Rates: The rates market has reacted with a notable bull steepening in the Treasury curve. Real yields led the move lower, with breakevens wider, as the market prices in higher stagflation risks.

Going into the announcement, markets had already priced more rate cuts this year, taking a cue from Powell’s remarks at the March FOMC meeting, where he downplayed inflation concerns as “transitory” and put the focus on defending growth.

Going forward, we think rates investors will remain focused on growth concerns and, by extension, rising recession probabilities. We continue to suggest being long duration – with a stagflation kicker – and maintain our long 10y TIPS position. While we have preferred longer-dated TIPS, reflecting the bond-vigilant administration’s focus on limiting term premium, shorter maturities in TIPS also make sense given increased recession risk. We continue to suggest long 5y breakevens, with shorter-maturity breakevens also attractive, even at these levels.

… President Trump announced a reciprocal tariffs regime with a minimum 10% tariff on all exporters to the US. More than 50 countries will face even higher, customized rates based on how unfairly the Administration says the countries treat US exporters – in addition to their existing tariff rate. For context, today’s announcements include: China 34%, European Union 20%, Vietnam 46%, Taiwan 32%, Japan 24%, etc. The 10% baseline tariff will take effect April 5, 2025 at 12:01 a.m. EDT, but individualized levies will not take effect until April 9, 2025 at 12:01 a.m. EDT. Notably, Canada and Mexico will remain unaffected by the new levies, and instead will continue to operate under the USMCA Exemption. In Trump’s words, "This is not full reciprocal, it is kind reciprocal" … “We will calculate the combined rate of all their tariffs . . . and because we are being very kind . . . we will charge them roughly half of what they are charging us.”

‘Liberation Day’ saw 10-year yields trade an impressive 12 bp range in the run-up to the tariff announcements. After heading into the President’s comments at 4.18%, the kneejerk move to 4.23% was quickly faded as 10-year rates dropped as low as 4.11%. More notably, 10-year rates closed the session at the lowest level of the year. With Treasuries net richer and equity futures dropping back down to the lows, a risk-off tone has emerged in the wake of the tariff announcements. For the time being, it appears that the culmination of levy updates has resulted in a higherthan-expected read on the average US tariff rate. We’re seeing upwards of 30% compared to the ~20% ‘unofficial’ consensus, although that assumption will be under revision in the coming sessions….

Written / sent well before announcement …

02 April 2025 DB: Tariffs today matter less than you think George Saravelos

… To conclude, even though the tariff announcements this evening are likely to be historic in magnitude, we think a large market reaction this evening is unlikely to be sustained. Subsequent market moves and the central bank reaction function will probably be a lot more dependent on the forthcoming global fiscal news. The impact on the dollar follows: the more expansionary the US fiscal policy news, the better for the dollar. The more growth-supportive fiscal announcements are from the rest of the world, the more negative for the dollar. We have held to a bullish EUR/USD view through these tariff announcements. We will be closely assessing the evolution of fiscal policy across the globe in coming weeks to calibrate our views. We suspect today marks "peak tariff" day and the market will quickly move on to the follow-on drivers.

… At risk of oversimplifying, given that China and its connector economies are taking the brunt of the Trump tariff shock, the negative global spillover of this trade war to the rest of the world in coming days will largely be determined by the extent to which China allows the policy-determined USD/CNY to move materially above 7.20 or decides to do more fiscal stimulus instead. All eyes on USD/CNH and the CNY fixings. We will soon find out.

Are these tariffs the sharpest tools in the shed?

2 April 2025 DB: Tools of the trade war could top up inflation while tanking growth

The Trump Administration's interpretation of "reciprocal" appears more punitive than our prior calculations. The new tariff rate for each trading partner corresponds to half of that country's goods trade deficit with the US as a share of its goods imports to the US, with a 10% minimum baseline tariff for other countries. However, exemptions for certain industry sectors (at least for now) could lower the overall impact.

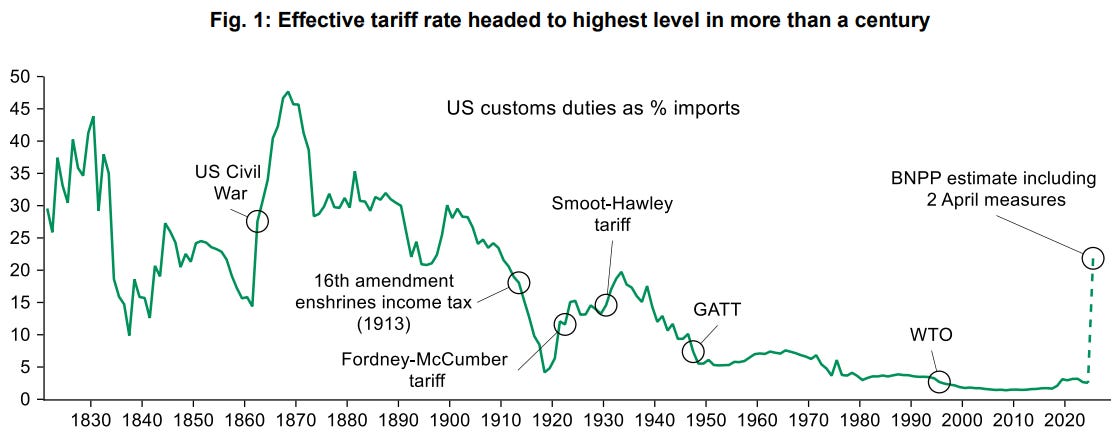

Our initial estimates of the reciprocal trade order suggest that the overall US tariff rate could rise into the 25-30% range if the new tariff rates are sustained for a significant period of time – the highest levels since the 1930s.

Though we have yet to formally review our forecasts for the US economy, the latest trade actions land in our downside growth scenario outlined in a recent note (see "When is it ok to break the (policy) rules? The Fed's response to tariffs"). Specifically, these actions could potentially shave 1 - 1.5 ppts from growth this year – meaningfully raising recession risks – while adding a broadly similar amount to core PCE inflation.

Beauty is in the eye of the beholder, amIright?

2 April 2025 ING: 'Beautiful' tariffs risk turning the growth outlook ugly

President Trump has announced a swathe of tariffs that he hopes will fund income tax cuts and incentivise manufacturing reshoring. In the long run it may deliver positives for the US economy, but the measures taken mean a painful transition period ahead

…Households are increasingly pessimistic regarding job prospects

… sleeping with one eye open …

2 April 2025 ING Tariffs: Europe’s worst economic nightmare just came true

A US 20% reciprocal tariff on the European Union will hurt. It's worsened the eurozone's short-term outlook. Now, so much depends on European governments to push through with their planned fiscal stimulus and reforms to strengthen domestic economies

Beauty and sleep aside …

2 April 2025 ING Market reaction to Liberation day - this is just the beginning

Impact effect? Risk-off, and lower Treasury yields. No break of prior ranges on market rates, but it smells like they want to go lower ahead. On FX, the new global trading regime still argues for a stronger dollar, but it won't be easy to convince markets protectionism is here to stay. Overall, it feels like this could unravel further in a negative fashion

…Look for convergence of Treasuries to lower yielders, while higher yielders can ease lower In terms of the international context, expect a period of reflection. To the extent that US yields fall in consequence, there is a downward effect on global rates, and a tightening versus lower yielders. Versus higher yielders, there is room being made for those rates to ease lower. No new news on Mexican tariffs, and Brazil was listed with a 10% tariff, which in net terms is a positive outcome for Latam.

For Asia, it a more troubling complex. China now averages at a 54% tariff, while Vietnam, Korea, India, Indonesia and Thailand are up for special extra tariffs mostly in the area of 25% to 45%. Then in Europe, a selection of countries are now on a 20% tariff, and we need to await retaliatory measures. Overall, there are negative kick-backs which likely mean a risk-off and lower yields combination dominating. See more detail on the tariff-impacted macro risks for Europe here.

Expect a degree of correlation in terms of performance ahead. So risk-off should be a common theme, and should lower market rates. Europe is the most likely to buck this trend further forward, as fiscal spending plans get fast tracked in the wake of a Trump that's not for changing. This can push yields up in Europe. Similar for Japan in terms of yield. At the other exteme, the likes of Mexico and Brazil can see market rates being pulled lower by lower Treasury yields.

Quick takeaways (from vocally bullish bonds shop) … I’ll paraphrase for you, “NO JUNE <cut> FOR YOU”

April 3, 2025 MS: US Public Policy, Global Economics, & Global Macro Strategy: Tariff Takeaways

The US meaningfully increased its average effective tariff rate. Today's White House announcement included a baseline 10% tariffs on all imports, in addition to incremental tariffs on a country-by-country basis.

Here's our initial read on the situation:

State of the tariff path: China tariffs, set to be 54% on imports (before accounting for potential exemptions), reach our expected levels faster than we anticipated. Canada and Mexico imports, in line with our expectations, remain relatively unimpacted given the continuation of USMCA exemptions. Rest of world tariff levels move higher than our expectations entering the year.

There's room for negotiation. The administration continued to reiterate the 'reciprocal' nature of the tariffs, implying the possibility that levels could move lower upon negotiation. Brazil, India, and the EU have all signaled a desire to start bilateral discussions, even ahead of today's announcements.

Assuming tariffs are durable, this announcement reinforces our view on the US economic outlook...that policy changes will weigh meaningfully on growth. Downside risks will be larger if these tariffs remain in place. Assuming tariffs are stackable, the effective tariff rate could be as high as 22%, compared to 3% at the start of the year. Risks to inflation lie to the upside. We think tariff-induced inflation will keep the Fed on the sidelines and we remove our June rate cut.

Court challenges are a wildcard. The president invoked authority under IEEPA to levy these tariffs. There’s debate among legal scholars about how this law can be used. Hence investors should keep an eye on the possibility of court challenges and injunctions.

We continue to suggest investors position for lower Treasury yields and a stronger JPY. Details below…

US President Trump unveiled a massive tax increase for US companies and consumers. Tariffs were set at 0.5 x bilateral trade deficit / US imports. This is a predictable formula, completely unrelated to trade openness. The uninhabited Heard and Macdonald Islands get a 10% tariffs (will the penguins retaliate?). This may cause investors to question the competence of the administration’s trade policy.

Trump has tended to retreat rapidly from tariffs that visibly hurt US consumers. Having a 10% near-universal tariff questions how far retreats go. If there is no retreat, markets will price a US recession. If there is a retreat, markets will assume US growth will weaken.

Trade under revised NAFTA is exempt. Negotiations for the patronage of exemptions now begin. Russian President Putin appears to have a strong bargaining position—Russia’s USD 3bn of exports to the US, which should earn a 41% tariff, are already exempt.

The direct effect of such taxes raises US price levels by 1.7% to 2.2%—the change in effective tariff rates multiplied by share of imports. Second-round effects matter. Will US manufacturers raise prices? Will US retailers indulge in profit-led inflation? A 10% tariff increase means around a 4% consumer price increase, but retailers may use the narrative to raise prices more.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Understatement of the year … so far …

April 3, 2025 Apollo: Higher Policy Uncertainty Having a Negative Impact on Capital Markets

When policy uncertainty went up, capital markets activity started slowing down, with a decline in loan issuance, IPO activity, and M&A activity, see charts below.

… ahhhh, Johnny MAC OpED to grab our attn …

April 3, 2025 at 4:42 AM UTC Bloomberg: You can NOT be serious! But any clear-eyed umpire would have to judge Trump’s tariffs as over the line.

FUGLY IF …?

Wednesday, Apr 02, 2025 - 03:00 PM Bloomberg (via ZH): It Could Get Ugly If... Authored by Simon White, Bloomberg macro strategist,

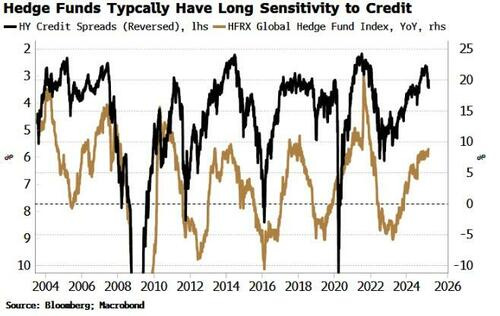

Hedge-fund performance is historically strongly linked to credit spreads.

Further weakness in credit may start to impact hedge-fund returns, and in extremis force them to unwind other trades that would stress markets.

Tariff day is here, but let alone the beginning of the end, we’ll be lucky if this is even the end of the beginning.

So murky is the outlook, the word “uncertainty” has not had to do as much work since the pandemic. Spending has been curtailed, but in some cases brought forward, and investment is stalling. All this plays havoc with corporate cash flows, which ultimately affect the likelihood bond coupons and principals can be repaid, therefore influencing credit spreads.

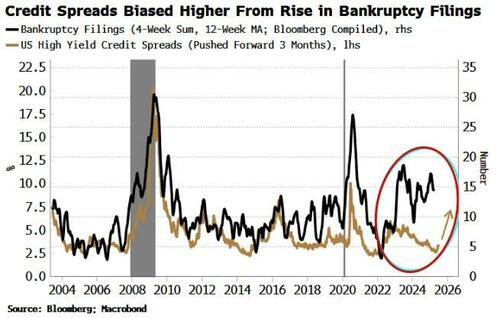

These have started to widen. There’s the direct effect from tariffs, and from the impact from falling stock prices and rising equity volatility. But it’s not just about tariffs. Fundamentally, credit conditions have started to weaken with, for instance, the rise in bankruptcy filings consistent with further spread widening.

The performance of hedge funds in the aggregate, based on Hedge Fund Research’s index, is historically closely linked to credit spreads.

As the chart below shows, there is a close inverse relationship between hedge-fund returns and high-yield credit spreads, i.e. hedge funds tend to lose money as credit spreads widen.

It turns out that almost all the main hedge-fund styles tracked by HFR have a persistent negative sensitivity to high-yield credit spreads, meaning they’re likely positioned to lose money when spreads widen.

Only macro, CTA and equity long/short funds have negative and positive sensitivity to spreads through time.

If it’s the case that hedge funds in the aggregate are long credit, it could get messy if spreads significantly widen, with tariffs a potential near-term catalyst.

That might prompt them to exit other trades if losses prompt redemptions. One that stands out as having potential systemic risk (and confined to only some of the largest funds) is the basis trade - selling bond futures against cash Treasuries. An unwinding of this trade can be hugely destabilizing, as we saw in March 2020. In an extreme case, it could even push the Federal Reserve into making its first direct hedge-fund bailout.

Either way, credit is the main vector of stress between markets and the economy. Significantly wider spreads - more so if the move becomes disorderly - could trigger a recession, and provoke instability across markets through hedge-fund unwinds.

… THAT is all for now … AND ‘til next week … taking some ‘time off for good behavior’ and will be outta pocket soon as I hit send today and HOPE to be back in seat and resuming regular spammation of the internet and yer inbox by Tuesday … for now, though … Off to the day job … but wishing you all very best as you plan your (#tariff and #NFP) trades and trade your (#tariff and #NFP) plans…

The Bond Market doing the Fed's work, for them...

10 yr going below 4 % ???

The answer is in: Tariffs are Deflationary, not Inflationary....